Seprod after climbing from $34.85 at the end of the first full week in February to $39 in the week following, the price made more gains this past week, to end at $48 and dropped out of the TOP 10 main market listing.

Seprod after climbing from $34.85 at the end of the first full week in February to $39 in the week following, the price made more gains this past week, to end at $48 and dropped out of the TOP 10 main market listing.

Another main market stock, Sygnus Credit Investments garnered increased buying interest after the company posted positive December quarter results and moved back to the 2018 IPO price of $13.72 to leave the TOP 10. Grace Kennedy and Stanley Motta moved in to fill the breach left by the above two companies.

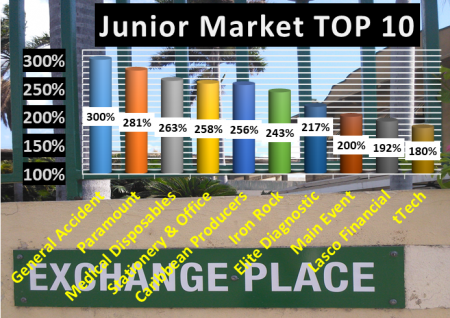

Caribbean Cream and Jamaican Teas entered the TOP 10 last week but left the list, by the end of this past week. Also moving on, was Lasco Manufacturing. Entering the Junior Market TOP 10 are tTech, Main Event with the price dropping to $5 and Iron Rock with the price declining to $3.50.

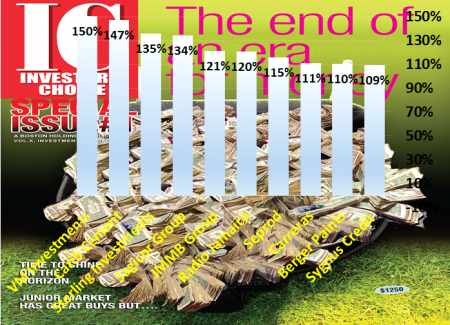

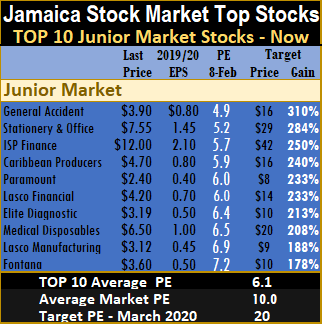

The three leading Junior Market stocks are General Accident, with potential gains of 300 percent, Paramount Trading with potential gains of 281 percent but not likely until the second half of 2019 when the company starts releasing the 2020 fiscal year results and Medical Disposables with 263 percent projected gains.

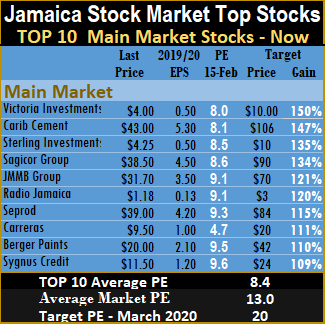

The three leading main market stocks are, Victoria Mutual investments with 153 percent likely gain, Sterling Investments with 135 percent and Sagicor Group with likely gain of 125 percent. Strong gains in the  price of Carib Cement pushed it down to number 4 from 2 last week following strong increased profit for 2018.

price of Carib Cement pushed it down to number 4 from 2 last week following strong increased profit for 2018.

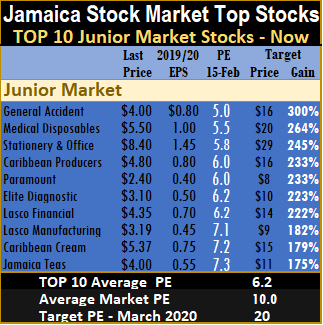

The main market closed the week with the overall PE at 13.9 and the Junior Market at 10.2. The PE ratio for Junior Market Top 10 stocks average 6 and the main market PE is now 8.7.

The TOP 10 stocks now trade at an average discount of 41 percent to the average for the Junior Market Top stocks and main market stocks trade at a discount of 38 percent to the overall market.

TOP 10 stocks are likely to deliver the best returns within a 12 months period. Stocks are selected based on projected  earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

Seprod & Sygnus jump IC Top 10

Fontana & Wisynco jump IC Top 10

Fontana Waterloo Road branch now new completion.

There were some major price movements for the TOP 10 stocks. By the end of the week, Fontana moved up in price to $3.95 and moved out of the list.

ISP Finance closed with the bid at $13, forecasted earnings was adjusted down to $1.65 for 2019, with the stock existed the TOP 10. Caribbean Cream and Jamaican Teas replaced the above two companies.

TOP 10 main market selection last week, Wisynco closed the week at $11 and that was enough to move it off the list with Carreras moving back on to the list. Radio Jamaica made a big surge from 80 cents to end the week at $1.20 but with the offer at $1.18 after the company posted strong gains in profit in the December quarter of $168 million versus $79 million in the similar period in 2017. Seprod also enjoyed a big move from $34.85 to $39, both remain in the TOP 10.

Stocks falling out of the TOP 10 should not be ignored, they have much more gains ahead of them, in 2019. Both Fontana and Wisynco earnings are based on June 2019 year-end. Results for the 2020 year will start coming out before the end of this year and could result in increased interest in the stocks.

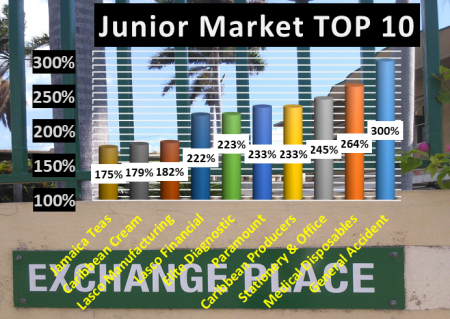

Medical Disposables fell in price during the week and rose in the TOP 10 to number 2 while Sygnus Credit Investments garnered increased buying interest with the price moving up with the stock just holding on to the number 10 spot on the main market list.

The three leading Junior Market stocks are General Accident, with potential gains of 300 percent, Medical Disposables with 264 percent projected gains and Stationery and Office Supplies 245 percent.

The three leading main market stocks are, Victoria Mutual investments 150 percent likely gains, Caribbean Cement with likely gains of 150 percent and Sterling Investments with 135 percent.

The main market closed the week with the overall PE at 13 and the Junior Market at 10. The PE ratio for Junior Market Top 10 stocks average 6.2 and the main market PE is now 8.4.

The TOP 10 stocks now trade at an average discount of 38 percent to the average for the Junior Market Top stocks but it’s a third of what the average PE for the year is likely to be of 20 times earnings. The main market stocks trade at a discount of 35 percent to the overall market.

TOP 10 stocks are likely to deliver the best returns within a 12  months period. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

months period. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

Fontana & Wisynco watch alerts

A close look at the main market shows clear bullish signs, with the market breaking out from a wedge formation and is being steered upwards by a long term upward sloping support line, that goes back to early 2016.

A close look at the main market shows clear bullish signs, with the market breaking out from a wedge formation and is being steered upwards by a long term upward sloping support line, that goes back to early 2016.

Unlike the rally in December that was dominated by NCB Financial, this rally is more broad based. Over the past two weeks, several company released results and seem to be stirring investors’ interest in a number of the companies.

Fontana and Wisynco were highlighted last week, as compelling stocks to watch. Demand for the two stocks drove prices higher on strong demand and increasing traded volumes, during the past week.

These two stocks remain on the watch list and IC Insider.com expects to see continued demand for them. Importantly, the supply of Wisynco’s shares is drastically reduced, since the release of the December quarterly. There are further reports that apart from a likely big new distribution contract that being discussed the company will be distributing sugar for a factory in the western end of the island.

Radio Jamaica

A block of nearly 61 million AMG Packaging shares traded during the week and stopped the price from moving higher. Buying interest remains as many investors see prospects of continued profit and stock price.

Elite Diagnostic closed the past week at $3.10 as results released showed a big improvement over the first quarter to September of $5 million versus $1.6 million on a pretax basis. The reported profit was not good enough to excite investors looking for immediate stock price gains. The price may well remain anchored around current levels for a while. The quarter over quarter growth in revenues points to higher revenues in the March quarter. There now appears to be a gap developing between the bids at $3.10 and sellers at $3.40. Watch to see how this develops. PanJam Investment traded as high as $82 on Friday with limited supply of the stock offered for sale. This one seems poised to move higher as just limited supply of the stocks is on offer for sale.

Demand for Fontana shares ate away at supply of the stock during the week but seems to have the $4 mark to take out before moving higher.

Section of Fontana Waterloo road branch now under construction.

General Accident 2018 results came out in the region of 29 cents per share but with $129 million less investments income and a big bump up in Management fee expense of 40 percent to $803 million. Importantly, net premium income rose a strong 28 percent for the full year. Selling pressure may be easing up with buying picking up.

ISP Finance reported flat profit for the year to December but revenues rose 18 percent in the last quarter over that of 2017 driving profit in the quarter 30 percent to $25 million. The results was strong enough to drive the bid above the last traded price and push selling of the stock on to the sideline. The growth in the final quarter of 2018 points to improving fortunes for the company and so could ignite demand for the stock at a higher price than the closing bid of $13.

Jamaica Stock Exchange shares hit a new high of $17.95, during the past week, with increasing interest shown in the stock. Exposed supply is currently not high, with expected continued buoyancy in the market and a big increase in new listings this year, investors seem more aggressive to buy into what should be another year of increased profit for the company. Seprod’s price moved up to $39 with increased demand for the shares continuing against the background of declining supply. The price seems poised to move even higher in the coming weeks as the stock remains attractively priced and in limited supply.

Some of Seprod”s products.

NCB Financial remains on the Watch List with strong gains in operating profit for the December quarter, but the stock is finding it hard to break through resistance at the $150 level and may need something out of the ordinary if the price is to move decidedly higher before the summer months.

Cement & General Accident top IC Top 10

IC Insider.com TOP 10 selections return after a break. The selections, are based on 2019 earnings. Quite a number of the 2018 TOP 10 listings appear again in this year’s lists.

IC Insider.com TOP 10 selections return after a break. The selections, are based on 2019 earnings. Quite a number of the 2018 TOP 10 listings appear again in this year’s lists.

New to the Junior Market, are Fontana that was listed in December last year, Lasco Manufacturing, ISP Finance and Medical Disposables. New to the TOP 10 main market list are Caribbean Cement, Sterling Investments, Radio Jamaica and Sygnus Credit Investments.

The three leading Junior Market stocks are General Accident, with potential gains of 310 percent, Stationery and Office Supplies 284 percent and ISP Finance with 250 percent.

The three leading main market stocks are, Caribbean Cement with likely gains of 152 percent, Radio Jamaica, 150 percent and Victoria Mutual investments 147 percent.

Fontana, is projected by IC Insider.com, to earn at 50 cents per share for the current year and should go on to boost earnings for the June 2020 much higher with the opening of its newest branch this year. The prospects for the stock is very good over the next two to three years with the expansion plans that the company has for it. Lasco Manufacturing’s profit for the December quarter was effectively flat at $197 million but is up a strong 32 percent for nine months period.

With EPS at 17 cents for the year, to December, full year results could hit 25 cents per share with 2020 moving higher as new product lines deliver more sales and profit. ISP Finance has been gradually building the loan portfolio and reporting improved annual profits but investment in increased staffing to manage expansion has increased cost faster than growth in revenues. The company exhausted the cash on hand in 2018 and borrowed additional funds to expand their loan portfolio. 2019 should be the year that profit break out and justify the current stock price. Medical Disposables delivered improved results in the six months to September last year with increased revenues coming from the new consumer lines that have been added to the product range.

With EPS at 17 cents for the year, to December, full year results could hit 25 cents per share with 2020 moving higher as new product lines deliver more sales and profit. ISP Finance has been gradually building the loan portfolio and reporting improved annual profits but investment in increased staffing to manage expansion has increased cost faster than growth in revenues. The company exhausted the cash on hand in 2018 and borrowed additional funds to expand their loan portfolio. 2019 should be the year that profit break out and justify the current stock price. Medical Disposables delivered improved results in the six months to September last year with increased revenues coming from the new consumer lines that have been added to the product range.

In the main market, the way seems clear for Caribbean Cement to break out this year with the plant upgrade now behind them and the discontinuation of costly import of cement to fill the gap left by lower production as the plant  upgrade took place in 2018. The company will benefit from increased sales as the construction sector continues to grow and demand more cement to use in building. Sterling Investments’ share has been undervalued for sometime and remains so, even after a 5 for 1 stock split in late 2018 that help move the price up. Additional funds from a recent rights issue will place the company in a position to take advantage of other investment opportunities and boost profit. Radio Jamaica has not delivered on the improved profitability after merging with the Gleaner but with income showing some growth against an improving economy, the 2020 fiscal year could start showing improved results. Sygnus Credit Investments is an undervalued stock with earnings to the September quarter negatively affected by the slippage in the rate of exchange of the local currency. Exchange movements does not affect the underlying fundamentals of the company going forward.

upgrade took place in 2018. The company will benefit from increased sales as the construction sector continues to grow and demand more cement to use in building. Sterling Investments’ share has been undervalued for sometime and remains so, even after a 5 for 1 stock split in late 2018 that help move the price up. Additional funds from a recent rights issue will place the company in a position to take advantage of other investment opportunities and boost profit. Radio Jamaica has not delivered on the improved profitability after merging with the Gleaner but with income showing some growth against an improving economy, the 2020 fiscal year could start showing improved results. Sygnus Credit Investments is an undervalued stock with earnings to the September quarter negatively affected by the slippage in the rate of exchange of the local currency. Exchange movements does not affect the underlying fundamentals of the company going forward.

The main market closed the week with the overall PE at 13 and the Junior Market at 10. The PE ratio for Junior Market Top 10 stocks average 6.1 and the main market PE is now 8.2.

The TOP 10 stocks now trade at an average discount of 39 percent to the average for the Junior Market Top stocks but it’s a third of what the average PE for the year is likely to be of 20 times earnings. The main market stocks trade at a  discount of 37 percent to the overall market.

discount of 37 percent to the overall market.

TOP 10 stocks are likely to deliver the best returns within a 12 months period. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

Big leap in BUY RATED Wisynco profit

Profit at Wisynco attributable to shareholders, rose a strong 36 percent to $776 million for the December quarter and 30 percent for the half year, to $1.54 billion.

Profit at Wisynco attributable to shareholders, rose a strong 36 percent to $776 million for the December quarter and 30 percent for the half year, to $1.54 billion.

Profit for the period would have been even better had the company not picked up a foreign exchange loss of $128 million in the December quarter. Profit before Taxation increased 24 percent to $942 million over the $760 million realized in 2017. The company earned of 21 cents per share for the quarter and 41 cents per share for the six months.

Revenues for the December quarter rose 16 percent to $7.1 billion over the $6.1 billion achieved in the corresponding quarter of 2017, while revenues rose 14 percent to $13.9 billion in the half year period.

Gross profit increased 18.3 percent, to $2.8 billion over the $2.4 billion achieved in the same quarter of 2017, for the half-year gross profit grew 18 percent to $5.4 billion. The company is eking out greater operational efficiencies with gross profit margin of 39.8 percent bettering the 39 percent for the 2017 second quarter. For the six months, gross profit margin grew to 38.8 percent from just 37.4 percent in 2017.

Sugar canes from which sugar is made.

Selling and distribution cost rose at a much slower pace than revenues, with a 12 percent increase for the quarter to $1.47 billion and 11 percent for the half year to $2.94 billion. Administrative Expenses increased 21 percent for the quarter to $284 million and grew by a sharp 79 percent to $544 million for the six months.

“Sales of Worthy Park spirit brands which include Rum-Bar Rums, Rum Cream and Vodka, commenced in November. The distribution of the Worthy Park packaged sugar commenced at the beginning of January,” Wisynco stated. The expanded products range, will lead to increased sales and profit, this fiscal year.

The company closed out the calendar year, with healthy looking financials, with just under $10 billion in equity capital, borrowing of $2.3 billion, cash funds of $3.63 billion and net current assets at $5 billion.

Wisynco is an IC Insider.com BUY RATED stock with the potential to earn around $1.10 per share in 2019 and $1.55 for the next fiscal year that starts in July, with the stock price hitting at least $15 by the end of this year. Usally reliable reports is suggesting that the company could land the distribution rights for another major local brand that would ahve a big impact on revenues and sales. The stock traded on the Main Market of the Jamaica Stock Exchange at the close on Friday at $10.40 for a PE of less than 10 times this year earnings compared with an average of 16 based on earnings for the market at the end of 2018.

TOP 15 JSE main market Stocks

TOP 15 JSE main market stocks for 2019

While Junior Market stocks seem poised to deliver better returns in 2019 than main market ones, there remain some attractive buys with great potential gains in the JSE premier market.

The average PE of the Main market for 2019 is 13 times estimated 2019 earnings, compared to nearly 16 at the end of 2018. This suggests potential for gains above 20 percent on average, for stocks in 2019. Stocks selling below the average for 2019, are poised to deliver above average growth for the year. Added to this, is the current PE ratio at 16 times 2018 earnings that should rise further before prices fully reflect earnings for 2018, which will take place by March. Stocks with PE at 8 or lower are likely to at least double during 2019.

Seprod – PE 7.5. The company acquired new business from Facey Group in 2018 as well as taking ownership of the former Nestle’ production facility in Bog Walk. Both activities will help swell revenues and profit as cost are lowered, giving greater leverage in the local and overseas markets. The sugar operation that has been bleeding for years, is getting greater attention with a view to cutting out the large loss. It should not be too long before action is taken to stop the bleeding. Elimination of the sugar losses will result in even more profit.

Sterling Investments – PE 7. The company underperformed the overall market for most of 2018 but has room for growth with the price bouncing after the announcement of a 5 for 1 stock split. They are now raising additional capital to diversify their investment objective, which could help expand profitability and lessen reliance on movements in foreign exchange gains. Investors should not expect explosive growth from this one but with the stock undervalued there is some amount of healthy gains that can be realised.

Victoria Mutual Investments – PE 7.5. The company recorded increased profit from ongoing operations in 2018 to September but the booking of $118 million impairment on Barbados bonds negatively affected the profit for year to date. The company also reported other comprehensive income separately from regular profit but this is likely to change for the full year and could well provide a kick to the final result, for the year. The company is active in seeking areas of growth. It has also added new unit trust funds to the market. The continued buoyancy of the local stock market bodes well for increased profits from this area as well as a result on its impact on fee income from its equity linked unit trust fund.

Caribbean Cement – PE 8. Caribbean Cement has not yet delivered on its potential. The plant that was previously leased, was acquired in 2018, and is now saving nearly $2 billion per annum. Shareholders enjoyed none of those savings last year. That could change this year, as the company raised prices late in 2018 and will now be producing all of the cement they sell, thus lowering direct selling cost. For most of 2018, the company imported cement to meet a part of its demand while they were working on upgrading the plant to meet both local and export markets. With continued growth in the economy and strong expansion in the construction sector, the company should continue to enjoy increasing revenues and profit. Cement has partially refinanced some of its US dollar debt and started to pay down the US based debt as well, thus limiting FX losses.

Radio Jamaica – PE 9.5. RJR has so far not been able to deliver on the promise when the media business and that of the Gleaner, were merged. While they have cut out some cost, revenues have not grown to deliver improved results. They remain profitable and yet results have been below expectation and has dragged the stock price below 90 cents. Tightness in the local economy in the past few years and cost incurred to switch Television to digital telecast, added to the pressure on results. The biggest part of the problem is the failure to pull in more revenues. The improving economy is likely to help to improve revenues going forward as advertisers increase their marketing spend. Of note is the fact that the stock now trades below net asset value of 95 cents. Importantly, even as the company reported a loss of $133 million for the six months to September, operating cash flow generated was a positive $120 million.

Sagicor Group PE 9. The company has not delivered much in 2018 partially due to losses incurred in the write down of Barbados bonds that it holds. The company will benefit from increased revenues from the acquisition of the Scotia Group’s insurance business going forward and will also gain from investments in the local stock market as well as from the growth in the local economy and increased employment that should facilitate increased sales of life policies.

Sagicor Group PE 9. The company has not delivered much in 2018 partially due to losses incurred in the write down of Barbados bonds that it holds. The company will benefit from increased revenues from the acquisition of the Scotia Group’s insurance business going forward and will also gain from investments in the local stock market as well as from the growth in the local economy and increased employment that should facilitate increased sales of life policies.

Sygnus Credit – PE 9.2. This company is relatively new and it listed in 2018. The company provides financing to viable but growing businesses by direct lending or other types of funding including factoring that will provide above average rate of return. The original concept was to deliver around 8 percent per annum to its investors, but depending on the nature of the investments they make the rate could be better. They have investments in two Portfolio Companies with profit sharing features attached. Up to September, return on invested funds was almost 11 percent. At the end of the September quarter US18 million was invested in various companies, with a similar amount available to be invested. The company incurred a loss for the September quarter due to exchange rate movement, which resulted in foreign exchange loss of US$7,000. Since then the local dollar has revalued and this will reduce the loss incurred. The stock pulled back after reporting the release of the last results and now offers investors a nice entry point for appreciation, especially with PE ratios mostly around the 15 mark. The Company intends to pay out up to 85% of the earnings generated from these investments as dividends on a quarterly basis, after the end of the first financial year.

JMMB Group

JMMB Group – PE 9.5. JMMB shares have suffered from selling by insiders from time to time that has left it undervalued. It has a long history of good performance. Revenues and profit rose in the half year to September as a number of areas performed very well. Going forward, the group has a great deal of room to expand in the Dominican Republic with a population of 11 million, compared to Jamaica with 3 million. Effective April 1, 2018, the Group adopted IFRS 9 “Financial Instruments”. Prior period amounts are in accordance with IAS 39 “Financial Instruments: Recognition and Measurement”. IFRS 9 has resulted in changes in accounting policies related to the classification, measurement and impairment of financial assets and liabilities, the company stated.

Carreras – PE 9.5. Regular increases in taxes on cigarettes have pressured demand for the product and squeezed profits for several years. There was no increase in prices in the last year but revenues grew in the half year to September while administrative cost fell. The company should earn around 80 cents per share to March this year and that should increase for the 2020 fiscal year. Growth in the economy and more importantly, the buoyancy in the construction industry will increase disposable income for smokers and thus drive increased demand for the company’s products. The stock is currently trading at just over 11 times earnings, based on 2019 earnings well below the market average of 16. With the dividend yield around 7 percent, investors will get good value for an investment in the stock, but not big capital gains in the short term.

Proven Investments – PE 9.5. Proven has been expanding with new acquisitions in 2018 and recently the purchase of 20 percent of JMMB Group shares. Access Financial Services in which it owns the largest block of shares, just concluded the acquisition of a loan company in Florida, while Proven concluded the acquisition of brokerage business in Cayman Islands and their St Lucian bank was in the process of acquiring a Latin American bank. IC insider.com expects more acquisition going forward and this should augur well for continued growth of the group.

Jamaica Broilers – PE 10. The company has been expanding by acquisitions and agronomic growth, leading to group revenues for the October quarter increasing 18 percent to $13.6 billion, over the $11.5 billion achieved in the similar period in the previous year. Gross profit for the quarter was $3 billion, a 3% increase over the previous year. Profit for the quarter was not as positive as the gains in revenues but that will change going forward as the company improves on profit margins.

Wisynco Group – PE 9.5. Shares are selling at a discount to the average of the market. At the same time, profit for 2019 should rise well ahead of the 2018 results as the company fully overcome the added cost associated with the damage and dislocation caused by fire that destroyed their warehouse in 2016. Profit growth should increase with the addition of the distribution of sugar and rum as well as improvement from the operating from one site as opposed to two in 2018. Growth in the local economy will be beneficial to sales growth and profit as well.

Berger Paints – PE 10.5. The company has been undergoing changes since Ansa McAl took control in 2017. The Penta brand of paints is added to the product line, along with the strongly in demand Berger brand. Penta paints were previously imported, by a third party, with production locally, cost will be reduced and allow for greater profit margin. Other changes within the company will lead to increased sales at lower cost and greater profits going forward.

Jamaica Stock Exchange – PE 10.5. The JSE enjoyed its best year in trading ever, in 2018 with the value traded, almost doubling and bettering the highest level enjoyed in 2004. The company enjoyed more listings on the market last year and they expect a 20 percent increase in 2019. News listing not only bring added listing fee income but increased trustee fees as well. Additionally, new listings open up the market for new investors some of whom will start to be more frequent stock market traders, thus increasing fee income as further.

NCB Financial – PE 10.5. The group’s shares are not likely to be the top performer in 2019 but is expected to put in a decent return and could continue to increase in value for a number of years. NCB is currently on a strong growth path with operating profit increasing strongly with the December 2018 results rising 40 percent before onetime income. The planned acquisition of more shares in Guardian Holdings will only enhance the bright prospects ahead for the Group.

NCB hikes dividend 29%

NCB hiked dividend to 90 cents from 70 cents in 2018.

Profit after taxation and one-time gains, resulted in net profit of $7.4 billion for the first quarter of the 2019 financial year, slightly lower than the prior year’s results that included a gain (negative goodwill) of $4.4 billion relating to the acquisition of Clarien Group. Profit for the latest quarter, includes a gain of $3.3 billion from the disposal of 326,277,325 JMMB Group shares at $28.25 per share.

The strong improved results climbed on the back of 24 percent in net income, to $20.7 billion from $16.7 billion in 2017, offset by a 21 percent increase in expenses. Included in expenses is loan loss provision of $1, up from just $146 million in 2017 and seems tied to the need to adjust loan provisioning in line with new Accounting Standards. Depreciation and amortization cost almost doubled to $1.3 billion, from $667 million in 2017. Other operating expenses jumped 29 percent to $6 billion from $4.7 billion in the prior year. The big improvement in revenues flowed from increases in net interest income from $7.55 billion to $9.85 billion, an increase of 30 percent, while exchange trading delivered a third more, at $4.2 billion.

Retail and Small Business Banking segment profit grew a strong 36 percent to $1.34 billion, but Payment Services fell just 2 percent to $1.2 billion. Corporate Banking jumped sharply by 76 percent to $1.25 billion, Treasury and Correspondent Banking was up by just 14 percent to $1.65 billion. Wealth, Asset Management and Investment Banking, grew attractively by 39 percent to $1.2 billion, Life Insurance & Pension Fund Management rose 29 percent to $1.3 billion while General Insurance moved from a loss of $107 million to a profit of $227 million.

NCB giving back to the community.

The Group’s loans and advances, net of provision for credit losses, rose 16 percent to $373.5 billion. NCB stated that “the growth was driven by our Jamaican that increased by 22 percent or $50.4 billion. Non-performing loans totalled $18.5 billion as at December 2018 (December 2017: $15 billion) and represented 4.9 percent of the gross loans compared to 4.6 percent as at December 2017.” Customer deposits grew just 7 percent to $461 billion. The varied growth rate between loans and deposit is a strong positive for profit as the revenues climb faster than cost.

The group re-launched a revised take-over to acquire up to 32.01 percent of the outstanding shares of Guardian Holdings which, when combined with NCB’s existing 29.99 percent holding will bring the total to 62 percent. The profit of the group will get a further boost from this acquisition. IC Insider.com has updated the earnings per share for 2019 to $14 from continuing operations and with the stock price at $145, the PE is just over 10 times earning making the stock BUY RATED with a 2019 target price of $225.

Top 15 Junior market stocks for 2019

Selection of stocks is not isolated from the environment in which the companies operate. Accordingly, investors need to take developments in the wider economy and in certain sectors that can impact profit.

Selection of stocks is not isolated from the environment in which the companies operate. Accordingly, investors need to take developments in the wider economy and in certain sectors that can impact profit.

The data available suggest that Junior Market stocks should do better than those in the main market, in 2019. The TOP 15 Junior market stocks, selected based on the lowest PE ratio, using 2019 projected earnings and stock prices at the start of the year, are listed below.

AMG Packaging – PE 6. AMG suffered from losses incurred in their venture into the production of toilet tissue that failed, resulted in losses and dragging down profit in the box making business. Now that the segment of the business is closed, focus can be on their core business for which there is demand. Revenues should grow along powered by growth in the wider economy. The company reported a big jump in profit for the first quarter to November, from an increase in revenues and improved profit margin. The earnings projected is that for the fiscal year that ends in June 2020, when they would have implemented price adjustments to recover the fall in profit margin. IC Insider.com sees management as a weak area of its operation. Hopefully, changes in the composition of the board will address this frontally. Since the start of the year the price has moved up to $2.70 in response to the strong gains in the first quarter profit.Caribbean Cream – PE 9. The company enjoyed increased sales for the nine months to November last year but with flat sales in the second quarter and pick up in the third quarter. Importantly, the raw material prices for a number of production items fell sharply on the world market and will lower cost for them. The latest is the fall in the price of crude oil that will result in cheaper electricity cost as well and as JPS switches to lower electricity production the savings should gather steam during the year. The combination of lower input cost and increased sales will make the stock a winner in the current year. An investment in the stock around the $5.50 level that it is trading at may not pay off until the second half on 2019 when higher profit is expected.

growth in the wider economy. The company reported a big jump in profit for the first quarter to November, from an increase in revenues and improved profit margin. The earnings projected is that for the fiscal year that ends in June 2020, when they would have implemented price adjustments to recover the fall in profit margin. IC Insider.com sees management as a weak area of its operation. Hopefully, changes in the composition of the board will address this frontally. Since the start of the year the price has moved up to $2.70 in response to the strong gains in the first quarter profit.Caribbean Cream – PE 9. The company enjoyed increased sales for the nine months to November last year but with flat sales in the second quarter and pick up in the third quarter. Importantly, the raw material prices for a number of production items fell sharply on the world market and will lower cost for them. The latest is the fall in the price of crude oil that will result in cheaper electricity cost as well and as JPS switches to lower electricity production the savings should gather steam during the year. The combination of lower input cost and increased sales will make the stock a winner in the current year. An investment in the stock around the $5.50 level that it is trading at may not pay off until the second half on 2019 when higher profit is expected. Caribbean Producers – PE 6. The company has more going for it that it has so far

Caribbean Producers – PE 6. The company has more going for it that it has so far

delivered. The interim report to September recorded a loss of $1.3 million, but that was mostly due to write down of computer software cost and cut in the selling prices of some items that affected profit margins negatively. The core business is not affected and margins were, restored in the second quarter. The company benefits from growth in the tourism sectors in both Jamaica and St Lucia where it operates.

General Accident –PE 4.5. Investors are not seriously looking at this stock but they should. The stock is undervalued based on a PE and net asset value. Up to September, the company posted strong gains in profit for the nine months. Reports suggest that the company is looking to expand outside of Jamaica. Increased premium rates and a large pool of investible funds, are expected to deliver higher revenues and profit for the company for awhile. Continued growth in the Jamaican economy will provide a basis for above average growth in premium income and profit.

Fontana – PE 10. The PE is 10 based on current fiscal year’s earning but 7 times based on the next fiscal year results. Investors are unlikely to get this stock in the secondary market close to the IPO price any time soon. Expansion plans will  make it a good investment for long term investors if bough in the $3 region. The company will be opening their newest branch in Kingston by the second half of 2019. That will result in increased revenues and profit for the 2020 fiscal year that ends in June. They also have plans for the opening of 3 more stores in the island, when completed they will result in above average growth in revenues and profit.

make it a good investment for long term investors if bough in the $3 region. The company will be opening their newest branch in Kingston by the second half of 2019. That will result in increased revenues and profit for the 2020 fiscal year that ends in June. They also have plans for the opening of 3 more stores in the island, when completed they will result in above average growth in revenues and profit.

Elite Diagnostic PE is 6. The company recorded increased cost in 2018 as expenses associated with two new branches impacted profit negatively. The second branch is now in operation and reporting profit, while the one to open in St Anns Bay in the middle of this year should lay the foundation for continued above average growth for another year or two.

Iron Rock Insurance – PE 6. Iron Rock made profit in the September quarter for the first time and was set to report a full year of profit. Moving into 2019, revenues from increased premium income and low overhead cost and growth in the local economy are set to land a decent profit for them.

ISP Finance – PE 6. One of the smaller micro lenders ISP continues to grow and had to float a new bond to raise funds to service increased demand for loans. The September 2018 quarterly results show that interest rates charged on loans fell and that may have helped in stimulating increased demand. Loans should continue to rise and profit as well going into 2019, as cash flow from profits is invested in new loans.

Jamaican Teas – PE 7.5. The group will benefit from continued growth in the local economy and increased purchasing power of Jamaicans. The star performer, export sales have grown healthily for a number of years and should continue the growth path again. Added to this, some cost incurred in 2018, are unlikely to repeat in 2019. Importantly, accounting policy IAS 9 will see all gains or losses on investments being booked through the regular profit and loss statement and that could lift profit in 2019 as local stocks continue to grow in value.

Lasco Financial – PE 6.5. The company continues to earn from Money transfer business but the real growth potential rest in the micro lending area that enjoys high profit margin. The area is crowded but entities with size can have an advantage. Additionally, Lasco has a wide network of branches, used to reach a wide potential group for granting loans.

Lasco Manufacturing – PE 8. New products and the streamlining of the business with potential for more product lines that can be added make this entity a compelling long term investment.

Medical disposables – PE 7.5. The company started as a distributor of medical and pharmaceutical distributors but has now broadened their offering to involve consumer products. The base is established for a wider range of products, using a lot of the existing infrastructure that is adding to the attractiveness of the stock. Results for the June quarter showed strong increased revenues and profit but their usually slow second quarter saw modest increased revenues and flat profit. Importantly, gross profit increased well ahead of the growth in revenues and but for a big increase in foreign exchange losses, profit in quarter and six months would have climbed strongly. Revaluation of the Jamaican dollar in the December quarter will result in a reversal of some of the foreign exchange losses.

Stationery & Office Supplies MoBay Office

PTL- PE 7.5. The company reported growth in revenues for the half year to November resulting in improvement in gross profit. Administrative cost grew higher than revenues with depreciation accounting for 25 percent of the increased cost. The company’s joint venture lubricant plant, was operational during the period and resulted in cost and revenues excluded from the six months results but included in the 2017 figures. Only the company’s share of profit is now included in the results amounting to $2 million. The company had moved into the repackaging of chlorine and bleach production in 2018. The last quarterly results have not shown much increased business from these two ventures, while they incurred increased staff cost to serve the market. Major improvement in profit, is not expected until the 2020 fiscal year that starts in June 2019 and will probably hold back the stock price for the greater part of the year.

Stationery and Office Supplies – PE 6. SOS delivered two good years on the Junior Market for early investors. IC Insider.com is forecasting another year of strong stock gains for the company. The company moved into the production of exercise books, mostly for schools and added note pads for the local and overseas markets. Other products could be added to their line up in 2019.

tTech – PE 6. Results for the September quarter almost doubled, with earnings per share reaching 12 cents, versus 6 cents in 2017, with operating revenues rising an attractive 25 percent. Profit for 2018 should hit 40 cents for the year. Management indicates that they are proactive in seeking new business locally and overseas and sees past marketing effort to attract new business now bearing fruit.

Aggressive growth stocks pay big

Stocks of companies that have the potential for active expansions, are likely to do better than those companies relying mainly on agronomic growth.

Stocks of companies that have the potential for active expansions, are likely to do better than those companies relying mainly on agronomic growth.

Investors in these aggressive growth companies may well enjoy slower growth in the early years of a large expansion, but pick up explosive growth in the latter stage of the investment cycle. Smaller companies in strong growth cycle are likely to do better than large companies unless the latter makes a really big expansion.

Listed companies with aggressive growth based on actual or planned expansion are: main market stocks – NCB Financial, Barita Investments, PanJam Investment, Jamaica Broilers, Jamaica Producers, Kingston Wharves, Proven Investments and Seprod. Others in the main market to have above average growth include Jamaica Stock Exchange due to continued new listings and increase in the number of investors coming to the market. Caribbean Cement, who have completed an upgrading of the plant in 2018, Palace Amusement with expansion into Portmore with a new cinema house comprising 4 separate cinemas and Wisynco Group that continues to focus on expanding its range of products either to manufacture or distribute for third parties are three that offer above average growth prospects.

In the Junior Market- Access Financial, Derrimon Trading, Elite Diagnostic, Eppley, Express Catering, Fontana, Indies Pharma, Jamaican Teas, Knutsford Express, Lasco Financial, Lasco Manufacturing, Medical Disposables and Paramount Trading,

Cargo Handlers may not be an aggressive growth company but it has amassed a good pool of cash that will allow it to expand by acquisitions if the directors so desire.

Fontana listing on Tuesday

Fresh from a successful initial public offering of 250 million shares, Fontana is not expected to start trading until early January on the Junior Market of the Jamaica Stock Exchange.

Fresh from a successful initial public offering of 250 million shares, Fontana is not expected to start trading until early January on the Junior Market of the Jamaica Stock Exchange.

Scotia Investments, the brokers for the offer stated that the offer of Two Hundred and Forty Nine Million Eight Hundred and Seventy Four Thousand Nine Hundred and Sixty Five (249,874,965) ordinary shares opened and closed on Thursday, December 13 and attracted a total of 3,406 applications for a total of 982,194,569 shares.

Applications for the Public Pool received the first 25,000 units applied for, with amounts in excess of 25,000 units allocated approximately 8.82 percent.

The brokers indicated that multiple applications from a single person or entity were removed, except where they were entitled to apply for shares in a reserved and the public pool. Once that process was completed, 2,770 applications remained for 944,150,335 shares.

SIJL advised that the methodology and allotment of the shares as follows: Employee Gift, Company Reserved and Key Customers & Doctors pools applicants were fully allocated. Strategic Partners were received a minimum of 50% of the amounts applied for.

Fontana shares, will only be allowed to trade up to a maximum of $2.44 on the first day of trading or a maximum of 30 percent above the $1.88 the public bought the shares at. Thereafter, the maximum price will be dependent on the highest  closing bid at the end of the previous day.

closing bid at the end of the previous day.

The Company recorded revenues of $3.4 billion in the financial year 2018, representing an increase of $272 million or 8.66 percent over the prior year and an increase of approximately 91 percent from $1.76 billion in 2014. Pretax profit for 2018 declined 6 percent from $322 million in 2017 to $303 million after rising from $237 million in 2016 that was up more than 100 percent over the 2015 profit of $115 million. The slowdown in 2018 is attributed to the state of emergency in Montego Bay and road construction in the Barbican area.

Fontana, is projected to earn around 35 cents for the current fiscal year and that should place the price at just over $5 during the course of the year.