The number of shares issued by publicly listed companies is very important information for investors to know, but investors would not think so when examining interim financial statements in Jamaica and Trinidad and Tobago of some of the companies.

There have been so many occasions one has to search high and low to find it if at all it is reported in the interim numbers. This is such a simple matter and the stock exchanges in the region could cure it easily, by making it one of the items that must be included in quarterly reports. It should be included as a part of the statement of movement in Shareholders’ equity.

There have been so many occasions one has to search high and low to find it if at all it is reported in the interim numbers. This is such a simple matter and the stock exchanges in the region could cure it easily, by making it one of the items that must be included in quarterly reports. It should be included as a part of the statement of movement in Shareholders’ equity.

The latest shocking reporting is that of Cargo Handlers that shows the number of shares issued as a part of the statement of shareholders’ equity. The oddity is the company reporting only 37.466 million issued shares since 2018 when it increased to more than 374 million units. The Jamaica Stock Exchange website shows them as having 416.25 million shares issued and the audited accounts show that the change took place in 2018 the numbers moving from 37.485 to 374.653 million shares. One wonders why no one discovered this glaring error when the list of top 10 shareholders show four of them having more shares than what they list as issued. The error goes back to 2018 for all of the quarterly reports.

This is such a glaring error and neither the Stock Exchange, the Financial Services Commission the directors of the company or its accounting staff have found out.

Our reporting standards are not up to scratch and some persons in the financial system love to talk about best practices globally.

Take the matter of segment reporting. Some companies report it quarterly and some only annually. Most correctly report the current period and the comparative previous year’s period. Why can’t the JSE insist on some minimum standards for the benefit of investors so they get information consistently? Limners and Bards is the latest company to provide a quarterly report with no segment results yet they report it in the audited report albeit just one year forcing investors to have to go back to the previous year’s report for the comparison. Seems if that is the approach they should just report the current year’s figures and let investors go back to the previous year’s reports for profit and balance sheet information.

Take the matter of segment reporting. Some companies report it quarterly and some only annually. Most correctly report the current period and the comparative previous year’s period. Why can’t the JSE insist on some minimum standards for the benefit of investors so they get information consistently? Limners and Bards is the latest company to provide a quarterly report with no segment results yet they report it in the audited report albeit just one year forcing investors to have to go back to the previous year’s report for the comparison. Seems if that is the approach they should just report the current year’s figures and let investors go back to the previous year’s reports for profit and balance sheet information.

The vast majority of listed companies report profit results with direct and indirect costs and gross profit. But others do not. The group shockingly includes GraceKennedy, 138 Student Living, Knutsford Express. It is full time that companies lift the standard of reporting so that investors can get pertinent information to use in their investment decision making. In response to a question put to Don Wehby about the bulking of all cost on the profit statement suggest that they are in compliance with accounting standards, but that is such a lame and shocking excuse from a company of such standing in the country. Seprod produces it, Jamaica Broilers does it and several other listed companies so why not Grace. Are grace directors suggesting that their shareholders are lesser persons than those of other companies? The case of 138 Student Living is shocking when one considers that the Chairman, Ian Parsard is also Group Senior Vice President – Finance & Corporate Planning at Jamaica Broilers.

Communication with investors is a subjective matter but there are some simple matters that it just takes some thinking or consulting to get right.

Communication with investors is a subjective matter but there are some simple matters that it just takes some thinking or consulting to get right.

AMG Packaging is in a class by itself when it comes to poor communication. The company has embarked on a major capital project, but the directors appear to be of the view that minority shareholders are best kept in as much darkness as possible about it. The audited accounts for 2020 are silent on any commitment to the project.

The latest quarterly the only capital spend, is shown as work in progress on the balance sheet in the amount of $57 million, with no comments on the progress, the total commitment and when it is expected to be complete and be in use. Worse there are no comments on its use. It is noted that the purpose has moved from a warehouse to a factory between 2018 and now.

In the 2018 annual report, the Chairman stated that “the Company recently took an option to purchase an adjoining property. If the transaction is completed, the additional space will be used to alleviate some of the space constraints in the existing facility, making operations more efficient.”

In the 2019 annual report “The Company completed the acquisition on the property at 12 Retirement Crescent which will allow us to expand our operations and to better serve our customers.” The company also stated that they “obtained funding from Proven Wealth Limited to assist with the development of 12 Retirement Crescent. The KSAC is in the process of reviewing the architectural drawings for 12 Retirement.”

The 2020 annual report states, “the company plans on utilizing the strong cash and cash equivalents position into developing 12 Retirement Crescent. The pandemic had caused the development of 12 Retirement Crescent to delay from 2020 to 2021. A contractor has been chosen and the building of an additional 11,370 square feet is set to begin in February 2021.”

In the results to February this year, the only comment made about the development is “that the new steel frame warehouse purchased from China arrived and construction commenced. The financial statement shows WIP at $49 million, with a zero balance in the November quarter.”

Wigton price collapses

Wigton Windfarms’ shares traded below the IPO price of 50 cents on Friday as attempts to shield the price from falling after announcing a drop in revenues is finally giving way to selling pressure. The Wigton syndrome continues to plaque the Jamaica Stock market with irrational behavior of investors to be seen in the prices of many stocks.

Wigton traded nearly 90% of shares on Thursday.

On August 25, investors bought 5 million shares of Future Energy, up to $2.85 and for the next two trading day’s they just over 10 million units up to $3.29, with 15 million shares trading on the 30th at an average of $2.96. The stock is now trading at $2.04, with a PE ratio of 16, to be one of the more highly priced Junior Market stocks. What is happening here, when viewed against stocks with much lower PEs and good growth prospects?

Radio Jamaica another stock that traded as high as $4.65 on August 25, traded on Friday at $3.11 at a PE ratio of 7. Salada Foods continues to trade around the $7 region at a PE ratio of 43 times current year’s earnings. Wigton Windfarms that investors were not informed until late last year that the contract for their number 2 turbine provide for a reduction in rates for the supplying of electricity to JPS, belatedly traded down to 46 cents on Friday with few bids left in the system, and now trades at a PE of 12.5.

The stock market is a wonderful creation that has helped to enrich participants over the years, like any endeavor the more time spent studying and understanding it the better off those investors will be.

There are thousands of new investors in the market brought on by several new listings on the market, with most listings creating good returns in a relatively short time for early investors.

There are thousands of new investors in the market brought on by several new listings on the market, with most listings creating good returns in a relatively short time for early investors.

In the past, investors and scholars developed systems and methods to act as a guide to better investment decisions and thus reduce the love or dislike for a stock or other types of investments and thus reduce emotional decisions.

Technical analysis is a very useful tool used in the investment arena that carries coded messages for persons who understand them. They help investors to avoid excessive behavior in markets and telegraph future trends by using past market movements as the base.

The recent price movements for Radio Jamaica and Fesco show them breaking out of a channel that goes back for months, both companies released results that were price movers and both broke out, with the market not fully there as yet as prices moved too far too fast as such prices pulled back.

A few months after Wigton shares were listed in 2019, ICINsider.com wrote a piece to help investors better understand stock market behavior and prevent losses in the market. The piece captioned “Wigton price dreamers” was published in May of 2019. In light of the irrational trading in Fesco and Salada shares, elements of the article are highlighted below.

Salada Foods traded at a all-time high of $18 on Tuesday.

“Buy now, Ride the $3 wave”. That is the advice of one online investor to another, regarding the likely performance of the Wigton Windfarm stock after trading, on the first day of listing at 83 cents with a PE of 14, placing the value in the upper half of the most valued main market stocks. The premium over net asset value another measure of valuation is 291 percent above the net asset value. At $3, the stock would trade at a stunningly high PE ratio of 50 times 2019 and 2020 earnings. The only main market stock close to that valuation is Kingston Wharves (KW) at 35 times 2019 earnings and that is coming down from more than 50 times 2018 earnings when it traded at $85.

Unlike KW, which has less than 10 percent of the shareholding that will trade, amounting to a few million units, Wigton has billion of shares that will trade. The high liquidity of the shares almost ensures that they will not become overvalued.

Most investors who would be big buyers are more professional and are versed in the valuation levels of stocks. Accordingly, they are unlikely to be buying a stock that has doubtful expansion credentials at an inflated value. The most popular valuation tool, the PE ratio does not support a price much higher than $1.20, with EPS of 60 cents per share. A price of $1.20 equates to a high PE ratio of 20. Only a few stocks are valued close to this multiple and many of them have prospects for profits to grow. Wigton has no immediate prospects for growth in earnings, pricing it at 20 times EPS would therefore be unwise. The market will speak but the heavy selling on Friday when it first traded is more in line with the thinking that the top is not far off. Investors who buy shares above the accepted market norm will likely get crushed.

In the investment world staying close to the crowd with pricing is a prudent investment practice that tends to be less costly than trying to predict lofty heights for stocks to reach.

PE ratios are there to give a sense of appropriate values, when investors try to break away from where the bulk of investors place a value of a stock, they usually end up regret the move.

Timely data critical for proper market functioning

Persons running the financial market seem not to understand the import of data to the proper functioning of the Jamaica market.

The Jamaica Stock Exchange has granted 45 days extension for companies to file their audited financial statements for 2021 to July 14, 2021. The extension assists management and auditors in managing the execution of audits at a challenging time and that may be fine, but what about the users of the reports?

The Jamaica Stock Exchange has granted 45 days extension for companies to file their audited financial statements for 2021 to July 14, 2021. The extension assists management and auditors in managing the execution of audits at a challenging time and that may be fine, but what about the users of the reports?

While that can be appreciated, insufficient thought has gone into the decision. The companies and auditors are not the only persons to be accommodated in this issue. Investors need timely information to make decisions. Management of the companies are clearly not concerned about their shareholders either and the Jamaica Stock Exchange seems to care even less even though they will state otherwise.

This publication wonders why could the decision to extend the time by 45 days not have required the companies concerned to file interim results to obtain the extension, that way investors would be in a far better position than having to wait more than three months to get up to date position on the finances of such companies.

After all, minority shareholders have rights too and deserve better than what they are getting.

Trinis missing the salient points

Another Trinidad company (Massy Holdings) is set to list on the Jamaica Stock Exchange on the basis that the sophistication and growth opportunities are evident in the Jamaican securities market that has become increasingly more dynamic over the past few years.

![]() They may be right about the Jamaican capital market, but they are missing the real issues. The stock prices of listed companies in T&T Stock Exchange have been priced out of the reach of the average Trinidadians and the directors don’t seem to understand that or worse seem to care about the smaller investors. Guardian Holdings with 232,024,923 million shares issued and Massy with nearly 98 million shares will just not have the liquidity to trade frequently in good volumes in either the Trinidad or Jamaican market. Unfortunately, those are not the only companies in that market that are so affected. The companies need to have the issued number of shares increased. for decent trading in the Jamaican market around two to three billion issued shares will be an appropriate level.

They may be right about the Jamaican capital market, but they are missing the real issues. The stock prices of listed companies in T&T Stock Exchange have been priced out of the reach of the average Trinidadians and the directors don’t seem to understand that or worse seem to care about the smaller investors. Guardian Holdings with 232,024,923 million shares issued and Massy with nearly 98 million shares will just not have the liquidity to trade frequently in good volumes in either the Trinidad or Jamaican market. Unfortunately, those are not the only companies in that market that are so affected. The companies need to have the issued number of shares increased. for decent trading in the Jamaican market around two to three billion issued shares will be an appropriate level.

The other factor is the need to put the companies on a growth path for profits that investors can have confidence in acquiring and holding the shares. The weakness in this area of profitability, is not the sole purview of the companies, as the government has a role to play in this.

Guardian Holdings hit 52 weeks high on TTSE.

The evidence is crystal clear, investors love stock splits and they help move stock prices as investors buy up shares they previously ignore for being overpriced. This has been without a doubt the clear case in the Jamaican market. For years PanJam Investments directors resisted recommending to shareholders the splitting of the company’s stocks but relented a few years ago, with the stock price that was stagnant for years coming to life and rewarded shareholders with much higher value afterward. It is therefore difficult to understand why directors, with the evidence so clear, want to have elevated stock prices and limited liquidity of their stock. Last year Apple and Tesla sand split their stocks to much investors acclaim, just this week Nvidia Corporation in the USA, with the price jumping after announcing a four for one split.

TTSE ends year to date with miniscule gain

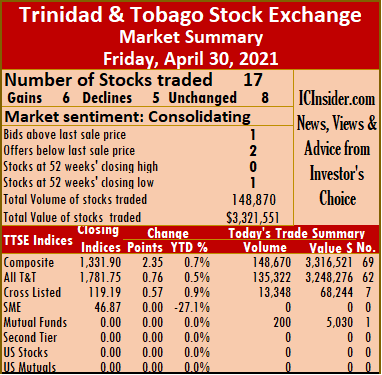

Market activity ended on Friday, with the market indices rising after the trading of 64 percent fewer shares than on Thursday, resulting in rising stocks just edging out those declining at the close of the Trinidad and Tobago Stock Exchange, leaving the market to hold on to a modest gain of less than one percent for the first four months of the year.

Trinidad & Tobago Stock Exchange Head Quarters

Trading ended with 17 securities changing hands up from 15 on Thursday, with six stocks rising, five declining and six closing unchanged. The Composite Index rose 2.35 points to 1,331.90, the All T&T Index rose 0.76 points to 1,781.75 and the Cross-Listed Index increased 0.57 points to close at 119.19.

At the close, 148,870 shares traded for $3,321,551 compared to 408,693 units at $3,296,893 on Thursday.

An average of 8,757 units traded at $195,385 compared to 27,246 at $219,793 on Thursday. An average of 1,472 units traded at $184,946 for the month to date versus 11,621 units at $184,376. The average trade for March ended at 12,610 units at $342,338.

Investor’s Choice bid-offer indicator shows one stock ended with the bid higher than their last selling prices and two with lower offers.

At the close, Agostini’s fell 15 cents to $24.25 in trading 375 shares, Angostura Holdings ended at $15.49 in an exchange of 2,091 stocks, Clico Investment Fund ended at $25.15 after trading 200 units, First Citizens Bank traded 4,562 stock units to close at $46.50. FirstCaribbean International Bank dipped 1 cent to end at a 52 weeks’ low of $6.50, with 1,177 shares changing hands, JMMB Group fell 1 cent to $1.79 in exchanging 6,216 shares, Massy Holdings shed $1.01 to end at $63.99 after trading 350 shares.  National Enterprises gained 1 cent to close at $2.81 in switching ownership of 10,000 units, National Flour Mills traded 1,500 shares at $2.35, NCB Financial Group rose 28 cents to $8.50 in exchanging 5,955 stock units. Prestige Holdings dropped 49 cents to close at $7.01 with an exchange of 2,800 units, Republic Financial Holdings rose 72 cents to $132.98 trading 8,690 shares, Scotiabank climbed 15 cents in closing at $54.65 after exchanging 2,942 units. Trinidad & Tobago NGL settled at $13.50 with an exchange of 49,947 shares, Trinidad Cement gained 40 cents in ending at $3.40 while exchanging 19,255 shares, Unilever Caribbean inched 1 cent higher to close at $16.33 while exchanging 12,000 shares and West Indian Tobacco closed at $32.98 after exchanging 20,810 stock units.

National Enterprises gained 1 cent to close at $2.81 in switching ownership of 10,000 units, National Flour Mills traded 1,500 shares at $2.35, NCB Financial Group rose 28 cents to $8.50 in exchanging 5,955 stock units. Prestige Holdings dropped 49 cents to close at $7.01 with an exchange of 2,800 units, Republic Financial Holdings rose 72 cents to $132.98 trading 8,690 shares, Scotiabank climbed 15 cents in closing at $54.65 after exchanging 2,942 units. Trinidad & Tobago NGL settled at $13.50 with an exchange of 49,947 shares, Trinidad Cement gained 40 cents in ending at $3.40 while exchanging 19,255 shares, Unilever Caribbean inched 1 cent higher to close at $16.33 while exchanging 12,000 shares and West Indian Tobacco closed at $32.98 after exchanging 20,810 stock units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Phillip’s missed opportunity to shine

This publication made some suggestions in an article in January, on minimum wages and taxes that mirrors some of Dr. Nigel Clarke’s basket of gifts to the country ahead of the general elections due by 2020.

Dr. Peter Phillips – former Minister of Finance

Earlier this year, Phillips proposed to lower the GCT rate to help those less privileged in the Jamaican society but completely missed the mark with a proposal to hike the minimum wages substantially, to spur economic growth sharply.

In the January publication captioned, “Minimum wage hike will hurt Growth,” Phillips was urged to revisit the GCT reduction issue and back off the idea of a major hike in the minimum wage that would lead to many minimum income earners losing jobs. We note that Phillips in recent days again recommended a cut in the GCT even as one of the shadow cabinet members came out publicly against it shortly after it was initially announced.

In the January 2020 article we stated, “Between 2008 and 2017, the Jamaican government increased taxes sharply to close the fiscal deficit and thus reduced disposable income significantly, which led to lower consumption. The cuts also led to a decline in productivity as businesses had to absorb higher unit costs per output as sales contracted. With the economy growing for the past five years, tax intake has been much higher in each year from the 2017 fiscal year. It is time we return some of the taxes imposed during the years of austerity back to the people”.

“What is needed is not just an arbitrary cut in one tax or the other, but a proper assessment of those that are inhibiting production. Yes, GCT should probably be reduced to 15 percent, which could well result in increased inflows as the lower tax rate would lead to increased consumption and less leakage.

Nigel Clarke, Jamaica’s Minister of Finance

Corporate taxes need to be reformed. Businesses and their owners should pay one rate based on profits. The tax rate on companies should be around 20-25 percent with no taxes on dividends. As such, shareholders would pay taxes on profits once not twice, with the latter being the case. All asset taxes that drive up borrowing costs must be removed and thereby reduce the distortion in the system. Payroll tax credits must be eliminated; they are a wasteful use of the country’s taxes. The excessive tax on financial institutions must also be eliminated as they are taxes on the end users, not the financial institutions, and they drive up the cost of production.”

“On close examination, there are several other categories of taxes that should be removed as they bring in a relatively small portion of the country tax revenues, leaving around ten in all. This would reduce the government’s operating cost for tax collection. Small businesses are burdened with all sorts of tax compliance issues and need relief from them so that they can focus on running their businesses and earning a decent income for their owners.”

“The above are some of the tax proposals that Phillips and his team should be addressing as reforming them could push economic growth.” He missed the opportunity to drive the agenda on tax reform, an important area of the economy that could stimulate growth and make lives easier for all.”

Phillips left the way completely clear for Clarke to strike some important blows and push the gap between the two parties further apart. This publication notes that a number of the above proposals made were addressed in Minister Dr. Nigel Clarke’s opening budget presentation on Tuesday. Importantly, his comments about the Asset tax not being a cost on the banks and is an inhibiting factor for faster economic growth is precisely what this publication has been saying for some time.

The minister continued on a sound footing in slowly reforming the system. We are confident that he will continue the process of reform to remove most of the other distortion in the system as tax revenues increase. The minister’s SME tax credit of $350,000 is welcomed, but that will only benefit businesses with profit. What is need is a bolder move to help ease pressure upfront. In this regard, these small businesses should be freed from some of the employer’s portion of payroll taxes like NHT, education taxes and HEART, and it is not too late to implement these.

Minimum wage hike will hurt Growth

Dr. Peter Phillips – former Minister of Finance

Dr. Peter Phillips, leader of Jamaica’s opposition party, was on to a good thing when he proposed lowering the GCT rate to help those less privileged in the Jamaican society. But he has completely missed the mark with the proposal that sharp hike in minimum wages will spur economic growth.

Phillips should revisit the tax matter and back off from what would be an ill-advised huge hike in the minimum wage that would lead to many minimum income earners losing their jobs. The evidence is there to prove it. Study the details on Jamaica’s employment numbers and the proof will be very clear.

Between 2008 and 2017, the Jamaican government increased taxes sharply to close the fiscal deficit and thus reduced disposable income significantly, which led to lower consumption. The cuts also led to a decline in productivity as businesses had to absorb higher unit costs per output as sales contracted. With the economy growing for the past five years, tax intake has been much higher in each year from the 2017 fiscal year. It is time we return some of the taxes imposed during the years of austerity back to the people.

What is needed is not just an arbitrary cut in one tax or the other, but a proper assessment of those that are inhibiting production. Yes, GCT should probably be reduced to 15 percent, which could well result in increased inflows as the lower tax rate would lead to increased consumption and less leakage.

Corporate taxes need to be reformed. Businesses and their owners should pay one rate based on profits. The tax rate on businesses should be around 20-25 percent with no taxes on dividends. As such, shareholders would pay taxes on profit once not twice, with the latter being the case. All asset taxes that drive up borrowing costs must be removed and thereby reduce the distortion in the system. Payroll tax credits must be eliminated; they are a wasteful use of the country’s taxes. The excessive tax on financial institutions must also be eliminated as they are taxes on the end users, not the financial institutions, and they drive up the cost of production.

Corporate taxes need to be reformed. Businesses and their owners should pay one rate based on profits. The tax rate on businesses should be around 20-25 percent with no taxes on dividends. As such, shareholders would pay taxes on profit once not twice, with the latter being the case. All asset taxes that drive up borrowing costs must be removed and thereby reduce the distortion in the system. Payroll tax credits must be eliminated; they are a wasteful use of the country’s taxes. The excessive tax on financial institutions must also be eliminated as they are taxes on the end users, not the financial institutions, and they drive up the cost of production.

On close examination, there are several other categories of taxes that should be removed as they bring in relatively a small portion of the country tax revenues, leaving around ten in all. This would reduce government’s operating cost for tax collection. Small businesses are burdened with all sorts of tax compliance issues and need relief from them so that they can focus on running their businesses and earning a decent income for their owners.

The above are some of the tax proposals that Phillips and his team should be addressing as reforming them could push economic growth. Hiking the minimum wage sharply will not only hurt economic growth, but it will also surely lead to reduced employment.

The above are some of the tax proposals that Phillips and his team should be addressing as reforming them could push economic growth. Hiking the minimum wage sharply will not only hurt economic growth, but it will also surely lead to reduced employment.

Contrary to Danny Roberts’ comments a few years ago that raising the minimum wage does not cut jobs, the data clearly shows the opposite. The category of workers most vulnerable to job losses, based on increased minimum wages, are those in private households, who suffered major declines in employment as the minimum wage rose above the country’s overall earnings. In fact, between 2003 and 2009, the minimum wage was increased 35 percent faster than the country’s average earnings and had a telling effect on employment in the sector. Employment in private households peaked at 74,200 in April 2004 and went downhill, hitting 56,000 in 2010 ―a loss of 16,000 jobs or a 22 percent decline. The proposed increase in minimum wages by Phillips is likely to lead to a 30 percent or more cut in jobs at that level.

Unlike many sectors that began to shed jobs with the advent of the global crisis, household employment started to fall off from 2004, making some recovery in 2006 and 2007 and continued to decline, reaching a low of 51,400 in the summer of 2009.

Fontana another IPO another set of errors

Fontana operators of a series of Pharmacies in Jamaica has now released the Prospectus for their initial public offer but like Elite Diagnostic last year, there are errors in this document that needs correction and explanation.

Fontana operators of a series of Pharmacies in Jamaica has now released the Prospectus for their initial public offer but like Elite Diagnostic last year, there are errors in this document that needs correction and explanation.

This is an unfortunate development for yet another issue, that seems very attractively priced. The directors have all signed off on the document that has gone through the Financial Services Commission, the Jamaica Stock Exchange and the Company Office of Jamaica, so why the errors and important ommission.

The introduction in the prospectus speaks to a price of $1.88 except for reserved shares at $1.69 but later on in the body of the document it speaks to a price of $2 for each share, making it unclear exactly what the price really should be? In the interim results to September, there are two issues, one is an error and the other, information that really needs clarification. The interim cash flow has no profit, nor depreciation and it therefore is not balanced and needs correcting.

The gross profit in the interim results jumped sharply,even as revenues grew just 5.5 percent with inventories are up 19 percent at the end of the quarter over 2017 and 15.5 percent over June this year. Why the big jump in inventories with sales are just rising moderately? Importantly, this raises questions about the accuracy of the inventory levels and the gross profit margin for 2018. Management should explain the sharp changes in this area so that investors can better understand why there is such a sharp jump in the quarterly profit.

This publication finds it difficult to once more raising issues relating to a prospectus. We are concerned that enough care is not going into them. The breach of GWest Corporation relating to the non-disclosure of information relating to an extraordinary meeting that was said to approve the issue of preference shares that was never brought to investors’ attention is fresh and has not been properly dealt by the regulators or the company. The regulators seem to have turned a blind eye to it. We need to raise the standards if the capital market integrity is the be enhanced.

Investors not properly protected in Jamaica

C&W should release to shareholders December 2017 results and 5 years forecast that was given to the valuators.

All concerned should be pleased that good sense has prevailed and the Elite IPO has been put off for now the IPO while they correct the errors in the prospectus, in keeping with this publication’s recommendation.

The matter brings to the fore once again, the inadequacy of capital market monitoring leaving investors’ with a false sense of security that they are being lead to believe.

What are some of the facts? The rules for takeover on paper is meant to protect minority shareholders, in fact they hardly do. Minority shareholders in many cases are not in a strong position to assess if they should or should not surrender their shares in a takeover bid. Worse the directors’ recommendations are fraught with problems. Most directors are not serious stock market investors and are not equipped to make a proper assessment of the company’s value, in order to make a proper recommendation to shareholders.

A good example of this, is the takeover attempts for all the shares of Berger Paints last year which was accompanied by directors’ report recommending acceptance of the offer and contained false information which was used to try and convince shareholders that they should surrender their shares. No one in authority seems to have called for proof of the information included in the circular to support their view or asked for correction of the error. Nor were the company required to provide shareholders with up to date financial information, which is not now a requirement but ought to be.

Berger Paints

Cable & Wireless directors are recommending the sale of the shares to the majority owner but have not provided shareholders with results to December, last year or forecast earnings. There is no rationale for this critical information to be provided to valuators but not to the persons who count – shareholders. So Why have the shareholders not be given such information?

The C&W offer is being made at a time when the company’s fortunes have improved considerably and could end with a profit or small loss in 2017. From IC Insider.com assessment, the company is in a very good position to report a good level of profit in 2018 with interest cost set to fall by around $1 billion per year and revenues set to rise. Investor should get more information as to the 2017 results and forecast for two or so years to enable them to make an informed decision.

The market place has dealers who blatantly breach agreements with clients but no regulator in the sector does anything about. So while the Minister of Finance is proud of the success of the Junior Market, he is unaware of the tsunami that lies just below in the system that he is minster over and one day could explode.

Steady trading on Trinidad market

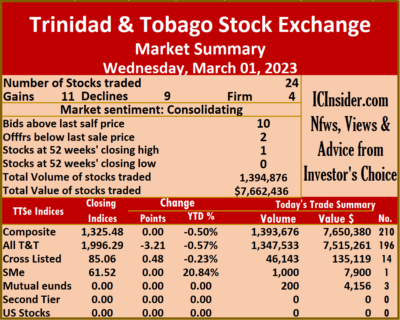

Trading maintained Tuesday’s robustness on the Trinidad and Tobago Stock Exchange on Wednesday, with the volume of stocks traded marginally lower than Tuesday’s, with a 14 percent higher value, resulting from activity in 24 securities up from 18 on Tuesday, with 11 stocks rising, nine declining and four remaining unchanged.

Investors traded 1,394,876 shares for $7,662,436 versus 1,400,887 stock units at $8,927,824 on Tuesday.

Investors traded 1,394,876 shares for $7,662,436 versus 1,400,887 stock units at $8,927,824 on Tuesday.

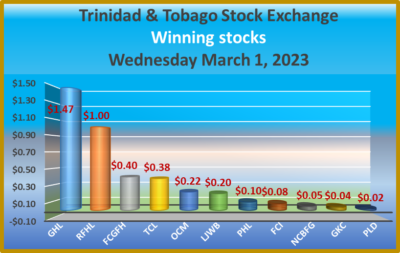

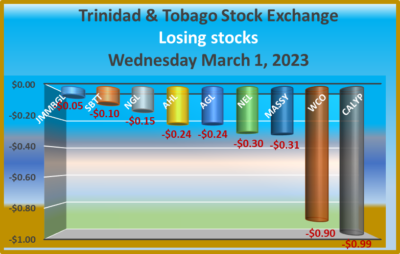

At the close, Agostini’s dipped 24 cents to $59.75 with investors trading 1,808 shares, Angostura Holdings declined 24 cents in closing at $23.50 in an exchange of 2,258 stocks, Ansa McAl remained at $50.75 after a transfer of 9 stock units. Ansa Merchant Bank ended at $45 with 250 units clearing the market, Calypso Macro Investment Fund shed 99 cents in ending at $20.51 as investors exchanged 200 units, CinemaOne remained at $7.90 and closed with 1,000 shares changing hands. First Citizens Group rallied 40 cents to close at $50.50, with 2,084 stocks crossing the exchange, FirstCaribbean International Bank climbed 8 cents to $6.30 after an exchange of 9,416 stocks, GraceKennedy gained 4 cents to end at $4.44 with an exchange of 1,727 shares. Guardian Holdings popped $1.47 in ending at $26.99 after investors traded 3,088 stocks, JMMB Group fell 5 cents ending at $1.75, with 32,500 stock units changing hands, L.J. Williams B share rose 20 cents to end at $2.75, with 100 units crossing the market. Massy Holdings dropped 31 cents in closing at $4.64 in switching ownership of 105,804 shares, National Enterprises lost 30 cents to close at $3.60 after 1,095,000 stock units crossed the market, National Flour Mills ended at $1.50 with a transfer of 12,088 units.

At the close, Agostini’s dipped 24 cents to $59.75 with investors trading 1,808 shares, Angostura Holdings declined 24 cents in closing at $23.50 in an exchange of 2,258 stocks, Ansa McAl remained at $50.75 after a transfer of 9 stock units. Ansa Merchant Bank ended at $45 with 250 units clearing the market, Calypso Macro Investment Fund shed 99 cents in ending at $20.51 as investors exchanged 200 units, CinemaOne remained at $7.90 and closed with 1,000 shares changing hands. First Citizens Group rallied 40 cents to close at $50.50, with 2,084 stocks crossing the exchange, FirstCaribbean International Bank climbed 8 cents to $6.30 after an exchange of 9,416 stocks, GraceKennedy gained 4 cents to end at $4.44 with an exchange of 1,727 shares. Guardian Holdings popped $1.47 in ending at $26.99 after investors traded 3,088 stocks, JMMB Group fell 5 cents ending at $1.75, with 32,500 stock units changing hands, L.J. Williams B share rose 20 cents to end at $2.75, with 100 units crossing the market. Massy Holdings dropped 31 cents in closing at $4.64 in switching ownership of 105,804 shares, National Enterprises lost 30 cents to close at $3.60 after 1,095,000 stock units crossed the market, National Flour Mills ended at $1.50 with a transfer of 12,088 units.  NCB Financial increased 5 cents to $4.10 in trading 2,500 stocks, One Caribbean Media advanced 22 cents in closing at $3.50 following an exchange of 5,000 stock units, Point Lisas popped 2 cents to close at $3.60 while exchanging 1,711 units. Prestige Holdings climbed 10 cents to $7 as 6,509 shares passed through the market, Republic Financial rose $1 to $138 after exchanging 11,372 stocks, Scotiabank shed 10 cents to end at $78.10 with the swapping of 171 shares. Trinidad & Tobago NGL fell 15 cents to close at $20.85 trading 2,521 units, Trinidad Cement rallied 38 cents after ending at $3.90 with the swapping of 62,582 stocks and West Indian Tobacco lost 90 cents in closing at $19 in an exchange of 35,178 stock units.

NCB Financial increased 5 cents to $4.10 in trading 2,500 stocks, One Caribbean Media advanced 22 cents in closing at $3.50 following an exchange of 5,000 stock units, Point Lisas popped 2 cents to close at $3.60 while exchanging 1,711 units. Prestige Holdings climbed 10 cents to $7 as 6,509 shares passed through the market, Republic Financial rose $1 to $138 after exchanging 11,372 stocks, Scotiabank shed 10 cents to end at $78.10 with the swapping of 171 shares. Trinidad & Tobago NGL fell 15 cents to close at $20.85 trading 2,521 units, Trinidad Cement rallied 38 cents after ending at $3.90 with the swapping of 62,582 stocks and West Indian Tobacco lost 90 cents in closing at $19 in an exchange of 35,178 stock units.

An average of 58,120 units were exchanged at $319,268 down from 77,827 shares at $495,990 on Tuesday. The average trade for February amounts to 51,996 shares at $458,520.

The Composite Index closed unchanged at 1,325.48, the All T&T Index declined 3.21 points to 1,996.29, the SME Index remained at 61.52 and the Cross-Listed Index rallied 0.48 points to end at 85.06.

Investor’s Choice bid-offer indicator shows five stocks ended with bids higher than their last selling prices and none with a lower offer.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.