“Jamaica’s debt ratio is on a downward trajectory and, by March 31, is expected to be eight percentage points lower than it was at the end of fiscal year 2012-2013”, Finance and Planning Minister Dr. Peter Phillips said.

By the end of March, it is expected to be lowered to about 139 percent of GDP, the finance minister said. Dr. Phillips further stated, “the Government would continue to implement measures to reduce the debt, as it aims to have a balanced budget for the next financial year (2014/15). Part of the way forward is to ensure that we convince the market that we are not about to return to our national addiction of excessive borrowing, and that means running a very tight set of budgetary arrangements”.

By the end of March, it is expected to be lowered to about 139 percent of GDP, the finance minister said. Dr. Phillips further stated, “the Government would continue to implement measures to reduce the debt, as it aims to have a balanced budget for the next financial year (2014/15). Part of the way forward is to ensure that we convince the market that we are not about to return to our national addiction of excessive borrowing, and that means running a very tight set of budgetary arrangements”.

The government ran a deficit of $55 billion for the fiscal year ended March 2013 but slashed that to $8 billion in their projection for 2013/14, but the final outturn is expected to be a near balanced fiscal outcome. That is a sharp reduction from what was achieved in 2012/13. Phillips, as indicated above, is planning for another year of balance as he strives to cut the impact of debt on government’s operation.

Minister of Finance Audley Shaw carried on from where Phillips left off.

The approach is not only positive for government’s operations but has far reaching implications for the wider economy.

Lower fiscal deficits mean less borrowing and less government spending. All of these will lead to lower interest rates locally, lower inflation and less pressure on our exchange rate ultimately. The initial stage will be a more sluggish economy as the country moves from an economy driven a lot by government spending to one where the private sector is the driver. Currently, the private sector confidence level are not high but is slowly improving based on data from the central bank. With improvement taking place in the global economies, Jamaica is likely to benefit, as such, we may see slow but continuing growth for a while. Against this background, interest rates are likely to be lowered, providing government with lower interest costs with the measures now being pursued.

Investors could therefore be seeing the end of an era of super high interest rates, to an extent this has been happening, but rates have not yet reached levels enjoyed by some of our neighbouring countries.

Investors should not ignore the impact of the logistic hub on demand and on foreign exchange inflows in the construction phase.

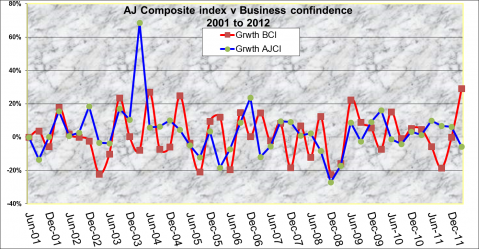

Falling Interest rates rising stock market.

The local stock market is overdue for a strong rally, having remained in the doldrums from 2005, to record one of the longest periods when it has remained below a high for so long. There are three things for those interested in real estate investments to consider. Property values are likely to be pushed by the fall in the value for the Jamaican dollar, which will push up input cost, already a number of new units are priced above $20,000 per square foot, with some at $24,000. The number of new units on the market over the last four years has been low, as demand slowed. The advent of the logistic hub is likely to spur demand within the corporate area for more space. Mortgage rates should fall going forward, which is likely to exert upward pressure on prices.

Investors should be making the shift in their portfolio from now to be there when the change takes full effect.

This article was published by the Investor’s Choice in 2014.