The Main and the Junior Market of the Jamaica Stock Exchange lost ground in trading on Tuesday as the JSE USD market inched moderately higher as trading ended with the volume and the value of stocks changing hands falling, compared with the previous day and resulted in the prices of 30 stocks rising and 42 declining.

At the close of trading, the Combined Market Index shed 524.55 points to close at 347,021.46, the All Jamaican Composite Index advanced by 93.57 points to 370,839.06, the JSE Main Index sank 377.08 points to close at 334,406.36. The Junior Market Index fell 19.52 to 3,813.32. The JSE Main & Junior markets rose 0.21 points to 255.60.

At the close of trading, the Combined Market Index shed 524.55 points to close at 347,021.46, the All Jamaican Composite Index advanced by 93.57 points to 370,839.06, the JSE Main Index sank 377.08 points to close at 334,406.36. The Junior Market Index fell 19.52 to 3,813.32. The JSE Main & Junior markets rose 0.21 points to 255.60.

At the close of trading, 16,492,495 shares were exchanged in all three markets, down from 47,975,821 units on Friday, with the value of stocks traded on the Junior and Main markets amounted to $62.80 million, from $164.28 million yesterday and the JSE USD market closed with an exchange of 180,495 shares for US$53,094 compared to 452,800 units at US$59,221 on Monday.

Trading in the Main Market was dominated by Wigton Windfarm with a leading trade of 4 million shares followed by JMMB 9.5% preference share with 3.94 million units and Transjamaican Highway with 1.83 million stocks.

In the Junior Market, Tropical Battery led trading with 847,958 shares followed by One Great Studio with 346,363 units and Indies Pharma with 292,036 shares.

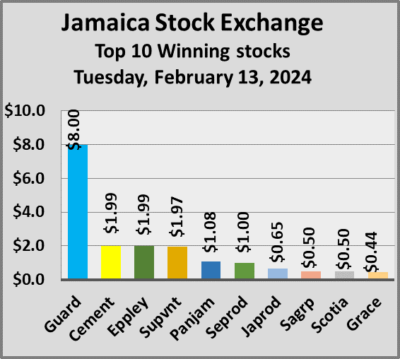

At the close of trading on the Main Market, Barita Investments dipped $1.02 to $70.18, Caribbean Cement climbed $1.99 in closing at $55.99, Eppley popped $1.99 to $35.99, Guardian Holdings rose $8 to $368, Pan Jamaica increased $1.08 to end at $51.20, Seprod rallied $1 to $83 and Supreme Ventures increased $1.97 and ended at $26.50.

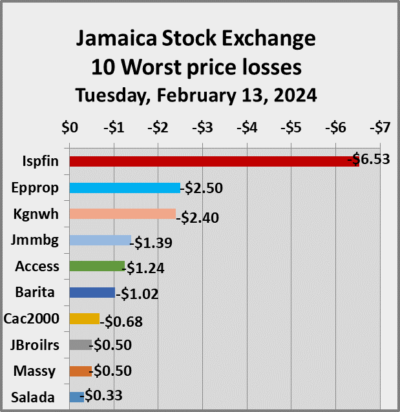

The major declining Main Market stocks are Eppley Caribbean Property Fund that fell $2.50 to close at $37.50, JMMB Group shedding $1.39 in closing at $24.05 and Kingston Wharves dropping $2.40 and ending at $28.10.

The major declining Main Market stocks are Eppley Caribbean Property Fund that fell $2.50 to close at $37.50, JMMB Group shedding $1.39 in closing at $24.05 and Kingston Wharves dropping $2.40 and ending at $28.10.

At the end of Junior Market trading, Fontana climbed 28 cents to close at $10.60, with the major losing stocks being Access Financial down $1.24 to close at $21.41, AMG Packaging shedding 24 cents to $2.71, CAC 2000 declining 68 cents to end at $3.83, Dolphin Cove skidding 32 cents to $18 as ISP Finance dropped $6.33 to $25.02.

In the preference segment, Jamaica Public Service 7% sank $5.80 to end at $43 and Productive Business Solutions 10.5 % preference share declined $16 to $1,284.

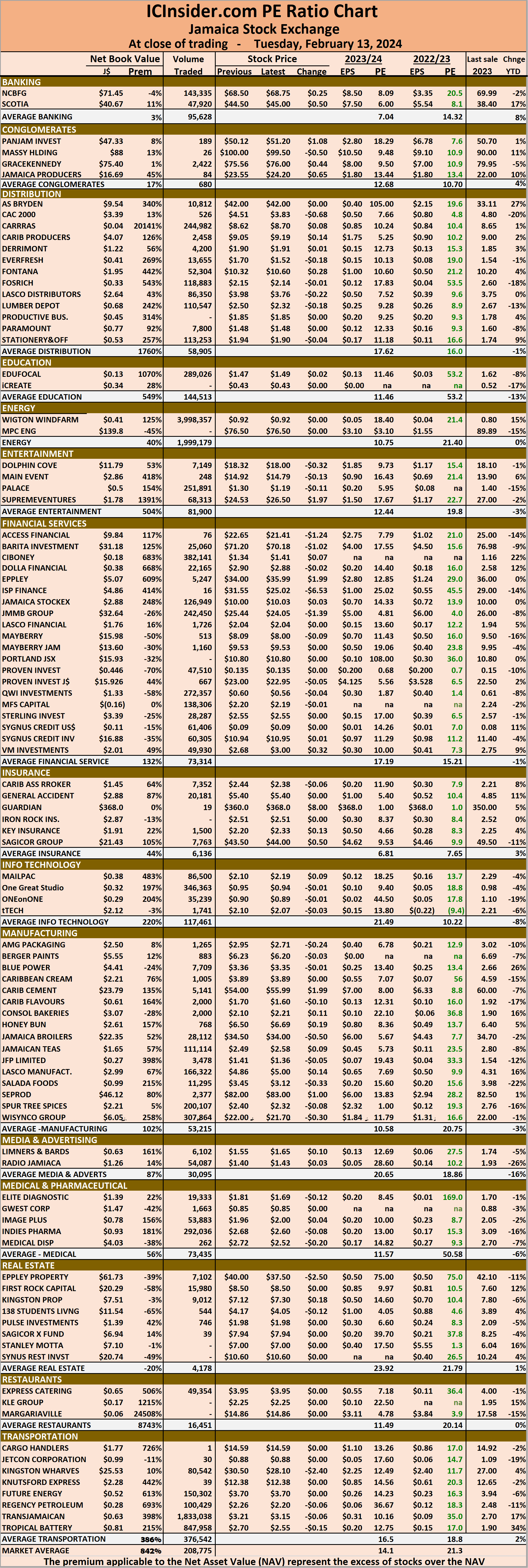

The market’s PE ratio, the most popular measure used to determine the value of stocks, ended at 21.3 on 2022-23 earnings and 14.2. times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily charts provide investors with regularly updated information to help decision-making.

The PE ratio chart covers all ordinary shares on the Jamaica Stock Exchange, grouped by industry, allowing for easy comparisons between the same sector companies and the overall market. The EPS & PE ratios are based on 2023 and 2024 actual or projected earnings, excluding major one off items.

Investors need pertinent information to navigate numerous investment options successfully in the stock market. The ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

The net asset value of each company is reported as a guide for investors to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

Dividends paid or payable and yields for each company are shown in the Main and Junior Markets’ daily report charts, along with the closing volume pertaining to the highest bid and the lowest offer for each company.

Stocks to Watch

There is currently low interest in buying Main Market stocks, even when the companies perform well and deliver positive results. One exception is Transjamaican Highway which has gained 86 percent for the year to date with more gains on the cards.

Dolphin Cove gained 31% for 2023 to date but should go higher.

The action is in the Junior Market, but even there, the interest is glacier-like, with a few stocks moving higher as buying demand is now overwhelming sellers.

A look behind the stock order book shows that a few merit watching over the next few weeks.

The list includes Carreras, Dolphin Cove, Fontana, Lasco Distributers, Lasco Manufacturing, ISP Finance, Mayberry Investments as well as Transjamaican Highway.

Carreras is enjoying consolidation of demand around the $8 level following a jump in earnings in the June quarter from rising sales. However, that is unlikely to change it from primarily one for high dividend yield rather than capital appreciation.

Dolphin Cove’s stock is up 31 percent for the year to date, but profit for the six months to June is up 48 percent over the year to June 2022. Investors may want to note the latest report on the court judgement on the sale of Mystic Mountain. There were indications that Dolphin Cove was an interested buyer and they may well be amongst the preferred bidders. If they succeed, expect the stock with limited offers posted on the JSE platform to jump.

Lasco Distributors‘ trend line shows an upward slopping momentum for the stock supported by earnings that increased 38 percent in the first quarter to June, following a 33 percent rise in full year profits to March this year. Buying interest is solid in the $4 and over region that is overwhelming supply on offer between $4.49 and $5 after that; there are currently less than 70,000 units on offer.

Lasco

Lasco Manufacturing‘s profit for the 2023 fiscal year jumped 37 percent after tax, followed by 27 percent for the June quarter. Still, the market was slow in responding positively to both sets of results, even as the price was less than ten times 2023 earnings of 50 cents per share. The stock in the past week jumped into the $5 region for the for time in months and closed the week at $5.35, with solid buying at that level and just below but with very limited selling with few stocks on offer from just nine offers for 180,000 shares.

Investors may not be ready to pounce on Fontana just yet. Still, there is limited selling in the stock ahead of the release of full year results that could come in around 80 cents per share, but with increased earnings in the current fiscal year, that will benefit from the opening of the Portmore store in a few months.

ISP Finance is an odd candidate, but there has been above average interest in this stock in recent months, with few offers in the stock currently. There are two critical factors to consider. One is that the majority shareholder must be close to retirement as such new owners cannot be far off. The recent addition of two new directors who operate in the financial market and have collaborated closely with them has increased speculation that a takeover of the majority shares will be forthcoming sooner than later. The other factor is the sharp jump in the loan portfolio to almost $1 billion after the credit loss provision. The near $200 million increase in loans over December last year and March this year is expected to swell revenues and profits in the future. The shares have to be high on the list for a split at the current price.

Fontana Waterloo Square Branch just after it was opened in October 2019.

Mayberry Investments may not have a lot of buying currently, but selling seems to be at a low level that could ignite a jump in price at any time that buying interest jumps.

Transjamaican Highway stock has almost doubled this year, encouraged by profit ballooning 338 percent for the June quarter to US$6 million and 442 percent to US$11 million for the six months to June. Supply has diminished on the sell side and could be overwhelmed by buyers. Investors have not bought into the sharp change in fortune for this stock and where it could head to. In addition, they should declare a considerable dividend payment in a few months.

Falling stocks overwhelmed Junior Market

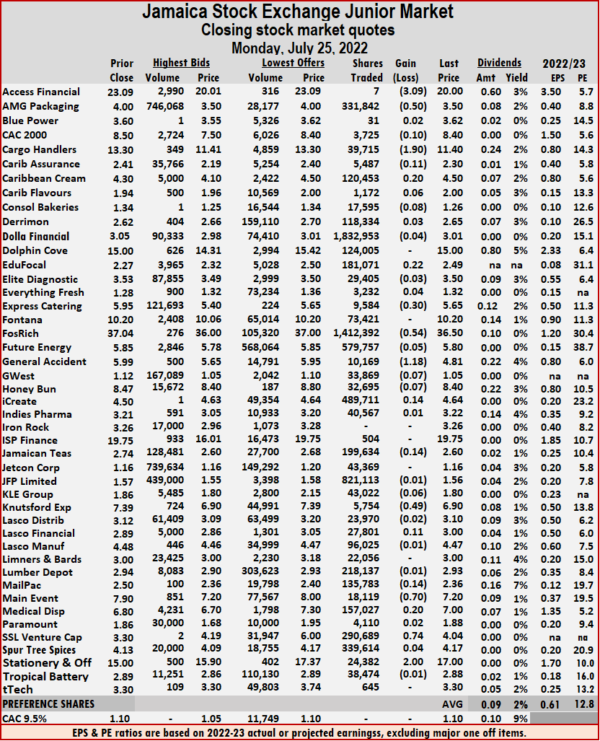

Declining stocks overwhelmed those gaining at the close of the Junior Market of the Jamaica Stock Exchange on Monday, with the volume of stocks traded jumping 247 percent and the value surging 201 percent more than on Friday with 46 securities trading versus 41 on Friday and ended with 12 rising, 28 declining and six closing unchanged.

A total of 27,627,621 shares were exchanged for $54,220,421 up from 7,964,359 units at $18,013,451 on Friday.

A total of 27,627,621 shares were exchanged for $54,220,421 up from 7,964,359 units at $18,013,451 on Friday.

Trading averaged 600,600 shares at $1,178,705 versus 194,253 units at $439,352 on Friday, with the month to date, averaging 220,674 units at $540,974 compared with 185,721 stock units at $482,303 on the previous trading day. November closed with an average of 259,893 units at $711,335.

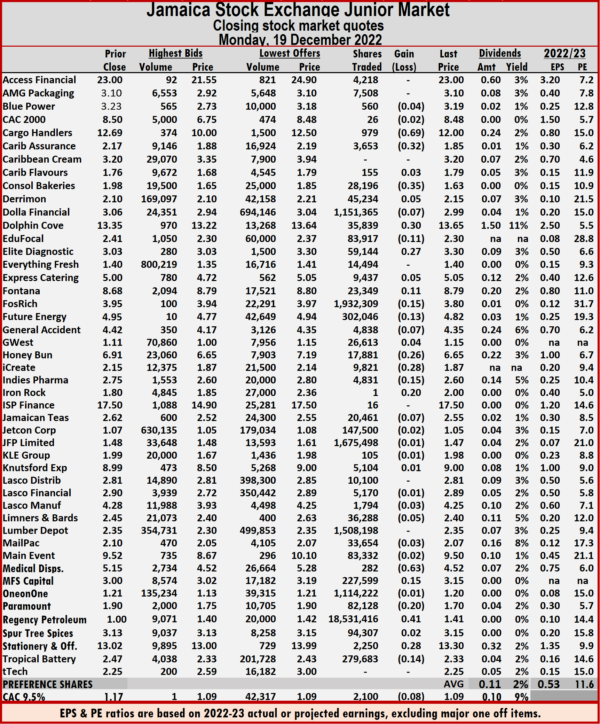

Regency Petroleum led trading with 18.53 million shares for 67.1 percent of total volume followed by Fosrich with 1.93 million units for 7 percent of the day’s trade, JFP Ltd ended with 1.68 million units for 6.1 percent market share, Lumber Depot traded 1.51 million units for 5.5 percent of the market, Dolla Financial closed with 1.15 million units for 4.2 percent of total shares traded and ONE on ONE Educational exchanged 1.11 million units for 4 percent of stocks traded.

At the close, the Junior Market Index shed 37.46 points to settle at 3,856.03.

At the close, the Junior Market Index shed 37.46 points to settle at 3,856.03.

The PE Ratio, a measure of computing appropriate stock values, averages 11.6. The PE ratios of Junior Market stocks incorporate ICInsider.com projected earnings for companies with financial year end that falls between November this year and August 2023.

Investor’s Choice bid-offer indicator shows seven stocks ended with bids higher than their last selling prices and two with lower offers.

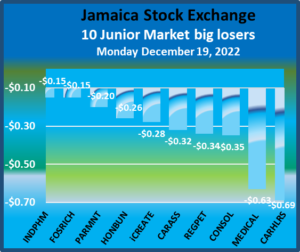

At the close, Cargo Handlers lost 69 cents to end at $12 in switching ownership of 979 stock units, Caribbean Assurance Brokers fell 32 cents in closing at a 52 weeks’ low of $1.85 with an exchange of 3,653 units. Consolidated Bakeries dipped 35 cents to close at $1.63 after 28,196 stocks changed hands, Dolphin Cove rallied 30 cents to $13.65 after an exchange of 35,839 units, EduFocal declined 11 cents in closing at $2.30 with investors transferring 83,917 stocks. Elite Diagnostic gained 27 cents to close at $3.30 after a transfer of 59,144 shares, Fontana popped 11 cents to $8.79, finishing after 23,349 stock units changed hands, Fosrich dipped 15 cents in ending at $3.80 in an exchange of 1,932,309 stocks. Future Energy Source shed 13 cents to close at $4.82 with the swapping of 302,046 stock units, Honey Bun dipped 26 cents to end at $6.65 after investors exchanged 17,881 shares, iCreate lost 28 cents in closing at $1.87, with 9,821 units crossing the market. Indies Pharma fell 15 cents to $2.60 with a transfer of 4,831 shares, Iron Rock Insurance increased 20 cents to $2 with one share crossing the market, Medical Disposables declined 63 cents to close at $4.52 with an exchange of 282 units. MFS Capital Partners rose 15 cents to end at $3.15 in trading 227,599 stock units, Paramount Trading dropped 20 cents to close at $1.70 as investors exchanged 82,128 stock units,

Consolidated Bakeries dipped 35 cents to close at $1.63 after 28,196 stocks changed hands, Dolphin Cove rallied 30 cents to $13.65 after an exchange of 35,839 units, EduFocal declined 11 cents in closing at $2.30 with investors transferring 83,917 stocks. Elite Diagnostic gained 27 cents to close at $3.30 after a transfer of 59,144 shares, Fontana popped 11 cents to $8.79, finishing after 23,349 stock units changed hands, Fosrich dipped 15 cents in ending at $3.80 in an exchange of 1,932,309 stocks. Future Energy Source shed 13 cents to close at $4.82 with the swapping of 302,046 stock units, Honey Bun dipped 26 cents to end at $6.65 after investors exchanged 17,881 shares, iCreate lost 28 cents in closing at $1.87, with 9,821 units crossing the market. Indies Pharma fell 15 cents to $2.60 with a transfer of 4,831 shares, Iron Rock Insurance increased 20 cents to $2 with one share crossing the market, Medical Disposables declined 63 cents to close at $4.52 with an exchange of 282 units. MFS Capital Partners rose 15 cents to end at $3.15 in trading 227,599 stock units, Paramount Trading dropped 20 cents to close at $1.70 as investors exchanged 82,128 stock units,  Regency Petroleum shed 34 cents to end at $1.41, with 18,531,416 shares crossing the exchange, after hitting a new high of $1.79 in early trading, Stationery and Office Supplies climbed 28 cents ending at $13.30 in an exchange of 2,250 units and Tropical Battery fell 14 cents in closing at $2.33 after 279,683 shares changed hands.

Regency Petroleum shed 34 cents to end at $1.41, with 18,531,416 shares crossing the exchange, after hitting a new high of $1.79 in early trading, Stationery and Office Supplies climbed 28 cents ending at $13.30 in an exchange of 2,250 units and Tropical Battery fell 14 cents in closing at $2.33 after 279,683 shares changed hands.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Trading jumps on Junior Market

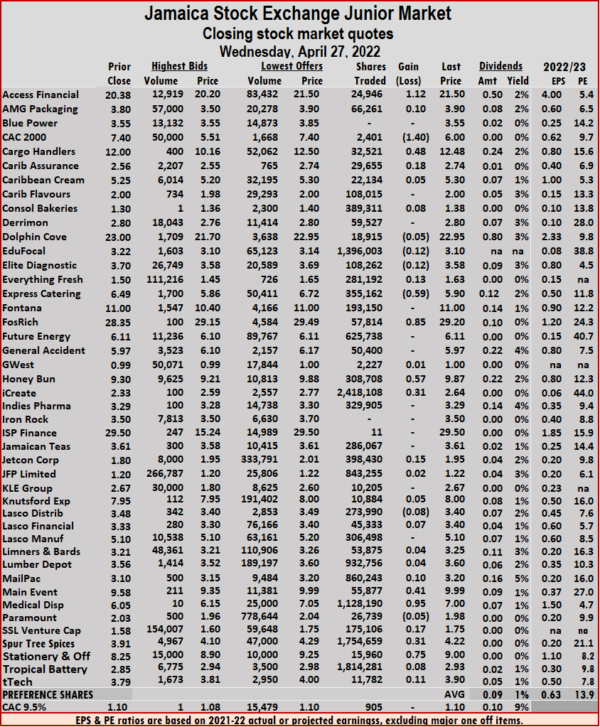

Trading jumped on the Junior Market of the Jamaica Stock Exchange Wednesday, with the volume of stocks traded rising 11 percent with 111 percent greater value than on Tuesday, following trading in 43 securities versus 44 on Tuesday and ended with 23 rising, 15 declining and five closing unchanged.

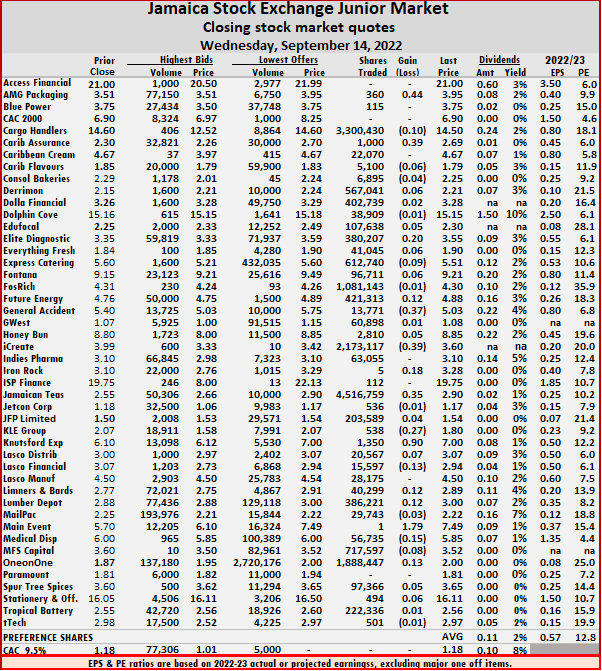

Jamaican Teas led trading with 4.52 million shares for 25.6 percent of total volume, followed by Cargo Handlers with 3.30 million units for 18.7 percent of the day’s trade, iCreate closed with 2.17 million units for 12.3 percent of the market, ONE on ONE Educational had 1.89 million units for 10.7 percent market share and Fosrich with 1.08 million units for a 6.1 percent share.

Jamaican Teas led trading with 4.52 million shares for 25.6 percent of total volume, followed by Cargo Handlers with 3.30 million units for 18.7 percent of the day’s trade, iCreate closed with 2.17 million units for 12.3 percent of the market, ONE on ONE Educational had 1.89 million units for 10.7 percent market share and Fosrich with 1.08 million units for a 6.1 percent share.

At the close, the Junior Market Index gained 11.10 points to end at 4,202.18.

The PE Ratio, a measure of computing appropriate stock values, averages 12.8. The PE ratios of Junior Market stocks incorporate ICInsider.com projected earnings for companies with financial year end that falls between November this year and August 2023.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and four with lower offers.

At the close, AMG Packaging rallied 44 cents to close at $3.95 with the swapping of 360 shares, Cargo Handlers shed 10 cents in closing at $14.50 after trading 3,300,430 units, Caribbean Assurance Brokers increased 39 cents to $2.69, with 1,000 stocks crossing the market. Elite Diagnostic climbed 20 cents to $3.55 after a transfer of 380,207 stock units, Future Energy Source advanced 12 cents to end at $4.88, with 421,313 stock units crossing the exchange, General Accident lost 37 cents in closing at $5.03aim trading 13,771 stocks. iCreate dropped 39 cents to close at $3.60 as investors exchanged 2,173,117 shares, Iron Rock Insurance rose 18 cents to $3.28, with five units changing hands, Jamaican Tea popped 35 cents to $2.90 and closed with an exchange of 4,516,759 stock units. KLE Group declined 27 cents to end at $1.80 in switching ownership of 538 stocks, Knutsford Express gained 90 cents to end at $7 while exchanging 1,350 units, Lasco Financial fell 13 cents to $2.94 in exchanging 15,597 shares. Limners and Bards added 12 cents in closing at $2.89, with 40,299 units clearing the market,

At the close, AMG Packaging rallied 44 cents to close at $3.95 with the swapping of 360 shares, Cargo Handlers shed 10 cents in closing at $14.50 after trading 3,300,430 units, Caribbean Assurance Brokers increased 39 cents to $2.69, with 1,000 stocks crossing the market. Elite Diagnostic climbed 20 cents to $3.55 after a transfer of 380,207 stock units, Future Energy Source advanced 12 cents to end at $4.88, with 421,313 stock units crossing the exchange, General Accident lost 37 cents in closing at $5.03aim trading 13,771 stocks. iCreate dropped 39 cents to close at $3.60 as investors exchanged 2,173,117 shares, Iron Rock Insurance rose 18 cents to $3.28, with five units changing hands, Jamaican Tea popped 35 cents to $2.90 and closed with an exchange of 4,516,759 stock units. KLE Group declined 27 cents to end at $1.80 in switching ownership of 538 stocks, Knutsford Express gained 90 cents to end at $7 while exchanging 1,350 units, Lasco Financial fell 13 cents to $2.94 in exchanging 15,597 shares. Limners and Bards added 12 cents in closing at $2.89, with 40,299 units clearing the market,  Lumber Depot advanced 12 cents to close at $3 with a transfer of 386,221 shares, Main Event rose $1.79 and ended at $7.49 after exchanging one stock unit. Medical Disposables dipped 15 cents to $5.85 in an exchange of 56,735 stocks and ONE on ONE Educational popped 13 cents to $2, 1,888,447 units crossing the market.

Lumber Depot advanced 12 cents to close at $3 with a transfer of 386,221 shares, Main Event rose $1.79 and ended at $7.49 after exchanging one stock unit. Medical Disposables dipped 15 cents to $5.85 in an exchange of 56,735 stocks and ONE on ONE Educational popped 13 cents to $2, 1,888,447 units crossing the market.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

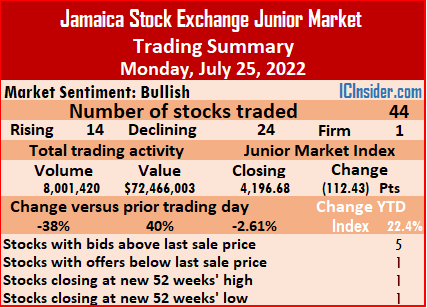

Junior Market plunges 112 points

On Monday, trading closed on the Junior Market of the Jamaica Stock Exchange, as the market Index plunged 112.43 points to settle at 4,196.68. The volume of stocks traded declined 38 percent and the value 40 percent more than on Friday, leading to 44 securities trading versus 42 on Friday and ended with 14 rising, 24 falling and six closed unchanged.

The Volume of stocks traded fell sharply to 8,001,420 shares but with a much larger value of $72,466,003 versus 12,922,133 units at $51,588,178 on Friday. Trading averaged 181,850 shares at $1,646,955 in contrast to 307,670 shares at $1,228,290 on Friday with month to date, averaging 565,323 units at $2,952,498 compared to 590,210 units at $3,037,223 on the previous trading day. June closed with an average of 429,016 units at $1,630,104.

The Volume of stocks traded fell sharply to 8,001,420 shares but with a much larger value of $72,466,003 versus 12,922,133 units at $51,588,178 on Friday. Trading averaged 181,850 shares at $1,646,955 in contrast to 307,670 shares at $1,228,290 on Friday with month to date, averaging 565,323 units at $2,952,498 compared to 590,210 units at $3,037,223 on the previous trading day. June closed with an average of 429,016 units at $1,630,104.

For a sixth consecutive day, Dolla Financial led trading, with 1.83 million shares trading on Monday for 22.9 percent of total volume, followed by Fosrich with 1.41 million units for 17.7 percent of the day’s trade one day before it starts trading ex-split on Tuesday that will result in ten stocks for each one currently owned and JFP Limited with 821,113 units for 10.3 percent market share.

The PE Ratio, a measure of computing appropriate stock values, averages 12.8. The PE ratios of Junior Market stocks incorporate ICInsider.com projected earnings for companies with financial year end that falls between November this year and August 2023.

Investor’s Choice bid-offer indicator shows five stocks ended with bids higher than their last selling prices and one stock with a lower offer.

At the close, Access Financial dropped $3.09 in closing at $20 in exchanging seven shares, AMG Packaging fell 50 cents to end at $3.50 in trading 331,842 stocks, CAC 2000 dipped 10 cents to $8.40, with 3,725 units crossing the market. Cargo Handlers shed $1.90 in ending at $11.40 and trading 39,715 stocks, Caribbean Assurance Brokers dipped 11 cents to close at $2.30 while exchanging 5,487 shares, Caribbean Cream rose 20 cents in closing at $4.50 with the swapping of 120,453 units. EduFocal increased 22 cents to $2.49, with 181,071 stock units crossing the exchange, Express Catering declined 30 cents to end at $5.65 after exchanging 9,584 stocks, Fosrich fell 54 cents to $36.50 in switching ownership of 1,412,392 stock units. General Accident shed $1.18 to close at a 52 weeks’ low of $4.81, with 10,169 units crossing the market, iCreate advanced 14 cents to end at $4.64 in an exchange of 489,711 stocks, Jamaican Teas fell 14 cents to $2.60 and closed, with an exchange of 199,634 shares.

At the close, Access Financial dropped $3.09 in closing at $20 in exchanging seven shares, AMG Packaging fell 50 cents to end at $3.50 in trading 331,842 stocks, CAC 2000 dipped 10 cents to $8.40, with 3,725 units crossing the market. Cargo Handlers shed $1.90 in ending at $11.40 and trading 39,715 stocks, Caribbean Assurance Brokers dipped 11 cents to close at $2.30 while exchanging 5,487 shares, Caribbean Cream rose 20 cents in closing at $4.50 with the swapping of 120,453 units. EduFocal increased 22 cents to $2.49, with 181,071 stock units crossing the exchange, Express Catering declined 30 cents to end at $5.65 after exchanging 9,584 stocks, Fosrich fell 54 cents to $36.50 in switching ownership of 1,412,392 stock units. General Accident shed $1.18 to close at a 52 weeks’ low of $4.81, with 10,169 units crossing the market, iCreate advanced 14 cents to end at $4.64 in an exchange of 489,711 stocks, Jamaican Teas fell 14 cents to $2.60 and closed, with an exchange of 199,634 shares.  Knutsford Express dropped 49 cents to close at $6.90 with 5,754 units changing hands, Lasco Financial gained 11 cents in ending at $3 after exchanging 27,801 stocks, Mailpac Group shed 14 cents in closing at $2.36 and trading 135,783 shares. Main Event declined 70 cents to $7.20, with 18,119 stock units changing hands, Medical Disposables popped 20 cents at $7, with 157,027 stock units clearing the market, SSL Venture rallied 74 cents to end at a record high of $4.04 as 290,689 stocks crossed the exchange and Stationery and Office Supplies climbed $2 to close at $17 in exchanging 24,382 units.

Knutsford Express dropped 49 cents to close at $6.90 with 5,754 units changing hands, Lasco Financial gained 11 cents in ending at $3 after exchanging 27,801 stocks, Mailpac Group shed 14 cents in closing at $2.36 and trading 135,783 shares. Main Event declined 70 cents to $7.20, with 18,119 stock units changing hands, Medical Disposables popped 20 cents at $7, with 157,027 stock units clearing the market, SSL Venture rallied 74 cents to end at a record high of $4.04 as 290,689 stocks crossed the exchange and Stationery and Office Supplies climbed $2 to close at $17 in exchanging 24,382 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

8 Junior Market stocks that should split

Stock splits and bonuses are two tools companies have in their tool kit to deliver value to their shareholders if used appropriately. Interestingly while the Scotia Group has used these tools repeatedly for the past several decades, Directors at NCB Group have frowned on the practice seeing no value to the group.

The critical point is that directors run a company for the benefit of shareholders not solely for the benefit of the company. Shareholders are kings and queens of the companies they own shares in and directors should not lose sight of that factor.

The critical point is that directors run a company for the benefit of shareholders not solely for the benefit of the company. Shareholders are kings and queens of the companies they own shares in and directors should not lose sight of that factor.

Some companies have split their stocks and investors love the results of these splits as they see where the values have mostly gone up, before and after the split. Some companies like the Lasco group have handled the split badly by overdoing it and creating too much liquidity that kills the value of the stock for years. The split is also an indication that a company’s profit is likely to grow short term which would cause the stock to struggle as the price gets more expensive without the split.

A look at the Junior Market shows 27 of the 45 companies listed trading below four dollars, with seven priced at more than twice $4. The price differential between the two groups suggests that a stock split is warranted if management is serious about the minority shareholders as well as creating the liquidity in the stock to maximize publicity from listing.

The seven companies are Access Financial, with only 270 million issued shares, with a stock split well overdue that will result in improved liquidity and build interest in it. Cargo Handlers at $11.50 has limited liquidity and needs a split to build back excitement into trading it. Dolphin Cove is the third one with the price at $15.25 and recently much higher, but the majority owner may not be so inclined to go the route of a split, but one never knows as local shareholders could well prevail on them to do so. Fosrich now trading around $27, is proposing a 10 to 1 stock split at the Annual General Meeting (AGM) this month. Honey Bun trading at $8.50 has the potential to move up to the $20 region later this year or early in 2023 and warrants a second split, having done one a few years ago.

Fosrich to vote on a 10 to 1 stock split at the coming AGM this month.

Back in 2020, management of ISP Finance had indicated that a split was on the cards, but even with the stock at more than $22 and highly illiquid with less than 3 percent of shares freely available for regular trading action to split the stock is nowhere in sight. Main Event is just at the borderline at $8.20 so a split may be in the future when it has fully recovered from the loss in business, with the advent of the covid-19 pandemic. There are 300 million shares issued with the top 10 holdings accounting for 93.5 percent. Stationery and Offer Supplies hinted at a past AGM that they had looked at it but felt the time was not right. The time may well be very close with the price trading recently around the $12 region with record profits expected this year a split could well happen with the AGM coming up later this year. The company has only 250 million shares issued of which 90 percent are held by the Top10 shareholders. Medical Disposables trades at $7-8 region, with the price not yelling for a split just yet but if management is smart they would split the stock with only 263 million shares issued, a two for one basis as rising profit this fiscal year will probably put the price to around $5 after such a split when all is said and done.

Another record close for Junior Market stocks

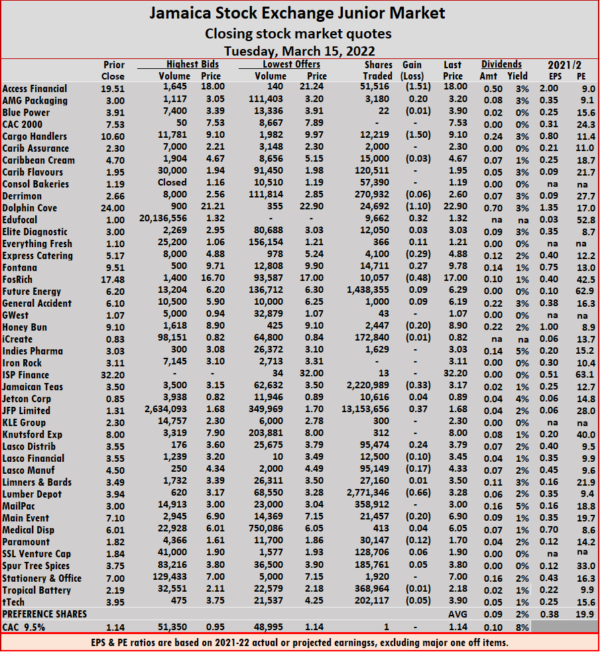

Trading closed on the Jamaica Stock Exchange Junior Market on Wednesday, with the volume of stocks traded rising 9 percent and the value 12.00 percent higher than on Tuesday, leading to rising stocks clobbering that declining and ending with a moderate rise in the market index.

Some 43 securities traded, up from 42 on Tuesday and ended with 25 rising, seven declining and 11 closing unchanged. Five stocks closed at 52 weeks’ highs and one at a 52 weeks’ low.

Some 43 securities traded, up from 42 on Tuesday and ended with 25 rising, seven declining and 11 closing unchanged. Five stocks closed at 52 weeks’ highs and one at a 52 weeks’ low.

The Junior Market Index climbed 15.34 points to settle at a record close of 4,399.56 after hitting an all-time intraday high of 4,411.48 in the early trading session.

The PE Ratio, a measure for computing appropriate stock values, averages 13.9. The PE ratios of the Junior Market incorporate ICInsider.com projected earnings for companies with financial years closing up to the end of August 2023.

Overall, 15,885,401 shares traded for $60,086,622 compared to 14,524,296 units at $53,604,474 on Tuesday. iCreate led trading with 2.42 million shares for 15.2 percent of total volume, followed by Tropical Battery with 1.81 million units for 11.4 percent of the day’s trade, Spur Tree Spices ended with 1.75 million units for 11 percent market share, EduFocal chipped in with 1.40 million units for 8.8 percent market share and Medical Disposables, 1.13 million units for 7.1 percent market share.

Trading averaged 369,428 shares at $1,397,363 up from 345,817 shares at $1,276,297 on Tuesday with month to date, averaging 426,741 units at $1,621,938 versus 430,328 units at $1,635,995 on the previous trading day. March closed with an average of 719,276 units at $2,636,802.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and one with a lower offer.

At the close, Access Financial rallied $1.12 to close at $21.50 while exchanging 24,946 shares, AMG Packaging rose 10 cents to $3.90, with 66,261 stocks crossing the market, CAC 2000 shed $1.40 in closing at a 52 weeks’ low of $6 after exchanging 2,401 stock units. Cargo Handlers climbed 48 cents, ending at a 52 weeks’ high of $12.48 after trading 32,521 units, Caribbean Assurance Brokers gained 18 cents to end at $2.74 after an exchange of 29,655 units, EduFocal fell 12 cents to $3.10, with 1,396,003 stocks clearing the market. Elite Diagnostic dropped 12 cents to $3.58 in exchanging 108,262 shares, Everything Fresh popped 13 cents to close at $1.63 with the swapping of 281,192 stock units, Express Cateringlost 59 cents in closing at $5.90, with 355,162 units crossing the market. Fosrich advanced 85 cents to end at a 52 weeks’ high of $29.20 in trading 57,814 stock units, Honey Bun increased 57 cents to end at $9.87 in an exchange of 308,708 shares, iCreate rallied 31 cents to $2.64 with an exchange of 2,418,108 stocks. Jetcon Corporation rose 15 cents to close at a 52 weeks’ high of $1.95, with 398,430 shares changing hands, Mailpac Group advanced 10 cents in closing at $3.20 in switching ownership of 860,243 stocks, Main Event gained 41 cents to $9.99 in an exchange of 55,877 stock units.

At the close, Access Financial rallied $1.12 to close at $21.50 while exchanging 24,946 shares, AMG Packaging rose 10 cents to $3.90, with 66,261 stocks crossing the market, CAC 2000 shed $1.40 in closing at a 52 weeks’ low of $6 after exchanging 2,401 stock units. Cargo Handlers climbed 48 cents, ending at a 52 weeks’ high of $12.48 after trading 32,521 units, Caribbean Assurance Brokers gained 18 cents to end at $2.74 after an exchange of 29,655 units, EduFocal fell 12 cents to $3.10, with 1,396,003 stocks clearing the market. Elite Diagnostic dropped 12 cents to $3.58 in exchanging 108,262 shares, Everything Fresh popped 13 cents to close at $1.63 with the swapping of 281,192 stock units, Express Cateringlost 59 cents in closing at $5.90, with 355,162 units crossing the market. Fosrich advanced 85 cents to end at a 52 weeks’ high of $29.20 in trading 57,814 stock units, Honey Bun increased 57 cents to end at $9.87 in an exchange of 308,708 shares, iCreate rallied 31 cents to $2.64 with an exchange of 2,418,108 stocks. Jetcon Corporation rose 15 cents to close at a 52 weeks’ high of $1.95, with 398,430 shares changing hands, Mailpac Group advanced 10 cents in closing at $3.20 in switching ownership of 860,243 stocks, Main Event gained 41 cents to $9.99 in an exchange of 55,877 stock units.  Medical Disposables climbed 95 cents to close at $7 after exchanging 1,128,190 units, Spur Tree Spices increased 31 cents in ending at a 52 weeks’ high of $4.22 after 1,754,659 stocks changed hands, SSL Venture popped 17 cents in closing at $1.75, with 175,106 shares clearing the market, Stationery and Office Supplies popped 75 cents to end at $9 trading 15,960 units and tTech rose 11 cents to $3.90 after 11,782 stock units passed through the exchange.

Medical Disposables climbed 95 cents to close at $7 after exchanging 1,128,190 units, Spur Tree Spices increased 31 cents in ending at a 52 weeks’ high of $4.22 after 1,754,659 stocks changed hands, SSL Venture popped 17 cents in closing at $1.75, with 175,106 shares clearing the market, Stationery and Office Supplies popped 75 cents to end at $9 trading 15,960 units and tTech rose 11 cents to $3.90 after 11,782 stock units passed through the exchange.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

New listings enjoy big price bounce

In trading on the Jamaica Stock Exchange Junior Market on Tuesday, newly listed EduFocal moved from its IPO price of $1 to close at $1.32 on the first day of trading, while JFP Limited continued from its opening price on Monday to $1.68 at the close on Tuesday and helped maintained the volume of stocks and the value traded moderately above that on Monday.

Market activity led to 43 securities trading compared to 42 on Monday and ended with 14 rising, 18 declining and 11 closing unchanged.At the close, the Junior Market Index shed 38.05 points to settle at 3,995.43.

Market activity led to 43 securities trading compared to 42 on Monday and ended with 14 rising, 18 declining and 11 closing unchanged.At the close, the Junior Market Index shed 38.05 points to settle at 3,995.43.

The PE Ratio, the most used measure to compute stock values, averages 19.9. The PE ratios in the chart below are based on ICInsider.com earnings forecast for companies with financial years to August 2022.

Overall, 21,910,635 shares traded for $55,555,327 versus 19,487,231 units at $50,742,595 on the Monday. JFP Limited led trading with 13.15 million shares for 60 percent of total volume followed by Lumber Depot with 2.77 million units for 12.6 percent of the day’s trade, Jamaican Teas ended with 2.22 million units for 10.1 percent market share and Future Energy Source ended with 1.44 million units changing hands for 6.6 percent market share.

Trading averaged 509,550 shares at $1,291,984 compared to 463,982 shares at $1,208,157 on Monday and month to date, averaging 510,084 units at $2,249,855, compared to 510,146 units at $2,360,875 on the prior day. February closed with an average of 370,064 units at $1,402,517.

Trading averaged 509,550 shares at $1,291,984 compared to 463,982 shares at $1,208,157 on Monday and month to date, averaging 510,084 units at $2,249,855, compared to 510,146 units at $2,360,875 on the prior day. February closed with an average of 370,064 units at $1,402,517.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and one with a lower offer.

At the close, Access Financial dropped $1.51 in closing at $18 after 51,516 shares changed hands, AMG Packaging rose 20 cents to $3.20 while exchanging 3,180 stocks, Cargo Handlers fell $1.50 to end at $9.10, trading 12,219 stock units. Dolphin Cove declined $1.10 to close at $22.90, with 24,692 units crossing the market, EduFocal increased 32 cents to $1.32, with 9,662 shares clearing the market, Everything Fresh popped 11 cents to $1.21, with 366 stocks crossing the market. Express Catering lost 29 cents in closing at $4.88 in exchanging 4,100 units, Fontana advanced 27 cents to close at $9.78, with 14,711 stock units changing hands, Fosrich shed 48 cents to end at $17 with 10,057 units crossing the exchange.  Honey Bun fell 20 cents to end at $8.90 after exchanging 2,447 stocks, Jamaican Teas dropped 33 cents to close at $3.17 with an exchange of 2,220,989 shares, JFP Limited rallied 37 cents in closing at $1.68 after exchanging 13,153,656 stock units. Lasco Distributors bounced 24 cents to $3.79 in switching ownership of 95,474 units, Lasco Financial declined 10 cents to $3.45 in an exchange of 12,500 shares, Lasco Manufacturing lost 17 cents to end at $4.33 trading 95,149 stock units. Lumber Depot shed 66 cents to close at $3.28 in trading 2,771,346 stocks, Main Event fell 20 cents to $6.90 with the swapping of 21,457 stocks and Paramount Trading shed 12 cents to $1.70 with 30,147 stock units. Changing hands.

Honey Bun fell 20 cents to end at $8.90 after exchanging 2,447 stocks, Jamaican Teas dropped 33 cents to close at $3.17 with an exchange of 2,220,989 shares, JFP Limited rallied 37 cents in closing at $1.68 after exchanging 13,153,656 stock units. Lasco Distributors bounced 24 cents to $3.79 in switching ownership of 95,474 units, Lasco Financial declined 10 cents to $3.45 in an exchange of 12,500 shares, Lasco Manufacturing lost 17 cents to end at $4.33 trading 95,149 stock units. Lumber Depot shed 66 cents to close at $3.28 in trading 2,771,346 stocks, Main Event fell 20 cents to $6.90 with the swapping of 21,457 stocks and Paramount Trading shed 12 cents to $1.70 with 30,147 stock units. Changing hands.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Top 15 Junior market stocks for 2019

Selection of stocks is not isolated from the environment in which the companies operate. Accordingly, investors need to take developments in the wider economy and in certain sectors that can impact profit.

Selection of stocks is not isolated from the environment in which the companies operate. Accordingly, investors need to take developments in the wider economy and in certain sectors that can impact profit.

The data available suggest that Junior Market stocks should do better than those in the main market, in 2019. The TOP 15 Junior market stocks, selected based on the lowest PE ratio, using 2019 projected earnings and stock prices at the start of the year, are listed below.

AMG Packaging – PE 6. AMG suffered from losses incurred in their venture into the production of toilet tissue that failed, resulted in losses and dragging down profit in the box making business. Now that the segment of the business is closed, focus can be on their core business for which there is demand. Revenues should grow along powered by growth in the wider economy. The company reported a big jump in profit for the first quarter to November, from an increase in revenues and improved profit margin. The earnings projected is that for the fiscal year that ends in June 2020, when they would have implemented price adjustments to recover the fall in profit margin. IC Insider.com sees management as a weak area of its operation. Hopefully, changes in the composition of the board will address this frontally. Since the start of the year the price has moved up to $2.70 in response to the strong gains in the first quarter profit.Caribbean Cream – PE 9. The company enjoyed increased sales for the nine months to November last year but with flat sales in the second quarter and pick up in the third quarter. Importantly, the raw material prices for a number of production items fell sharply on the world market and will lower cost for them. The latest is the fall in the price of crude oil that will result in cheaper electricity cost as well and as JPS switches to lower electricity production the savings should gather steam during the year. The combination of lower input cost and increased sales will make the stock a winner in the current year. An investment in the stock around the $5.50 level that it is trading at may not pay off until the second half on 2019 when higher profit is expected.

growth in the wider economy. The company reported a big jump in profit for the first quarter to November, from an increase in revenues and improved profit margin. The earnings projected is that for the fiscal year that ends in June 2020, when they would have implemented price adjustments to recover the fall in profit margin. IC Insider.com sees management as a weak area of its operation. Hopefully, changes in the composition of the board will address this frontally. Since the start of the year the price has moved up to $2.70 in response to the strong gains in the first quarter profit.Caribbean Cream – PE 9. The company enjoyed increased sales for the nine months to November last year but with flat sales in the second quarter and pick up in the third quarter. Importantly, the raw material prices for a number of production items fell sharply on the world market and will lower cost for them. The latest is the fall in the price of crude oil that will result in cheaper electricity cost as well and as JPS switches to lower electricity production the savings should gather steam during the year. The combination of lower input cost and increased sales will make the stock a winner in the current year. An investment in the stock around the $5.50 level that it is trading at may not pay off until the second half on 2019 when higher profit is expected. Caribbean Producers – PE 6. The company has more going for it that it has so far

Caribbean Producers – PE 6. The company has more going for it that it has so far

delivered. The interim report to September recorded a loss of $1.3 million, but that was mostly due to write down of computer software cost and cut in the selling prices of some items that affected profit margins negatively. The core business is not affected and margins were, restored in the second quarter. The company benefits from growth in the tourism sectors in both Jamaica and St Lucia where it operates.

General Accident –PE 4.5. Investors are not seriously looking at this stock but they should. The stock is undervalued based on a PE and net asset value. Up to September, the company posted strong gains in profit for the nine months. Reports suggest that the company is looking to expand outside of Jamaica. Increased premium rates and a large pool of investible funds, are expected to deliver higher revenues and profit for the company for awhile. Continued growth in the Jamaican economy will provide a basis for above average growth in premium income and profit.

Fontana – PE 10. The PE is 10 based on current fiscal year’s earning but 7 times based on the next fiscal year results. Investors are unlikely to get this stock in the secondary market close to the IPO price any time soon. Expansion plans will  make it a good investment for long term investors if bough in the $3 region. The company will be opening their newest branch in Kingston by the second half of 2019. That will result in increased revenues and profit for the 2020 fiscal year that ends in June. They also have plans for the opening of 3 more stores in the island, when completed they will result in above average growth in revenues and profit.

make it a good investment for long term investors if bough in the $3 region. The company will be opening their newest branch in Kingston by the second half of 2019. That will result in increased revenues and profit for the 2020 fiscal year that ends in June. They also have plans for the opening of 3 more stores in the island, when completed they will result in above average growth in revenues and profit.

Elite Diagnostic PE is 6. The company recorded increased cost in 2018 as expenses associated with two new branches impacted profit negatively. The second branch is now in operation and reporting profit, while the one to open in St Anns Bay in the middle of this year should lay the foundation for continued above average growth for another year or two.

Iron Rock Insurance – PE 6. Iron Rock made profit in the September quarter for the first time and was set to report a full year of profit. Moving into 2019, revenues from increased premium income and low overhead cost and growth in the local economy are set to land a decent profit for them.

ISP Finance – PE 6. One of the smaller micro lenders ISP continues to grow and had to float a new bond to raise funds to service increased demand for loans. The September 2018 quarterly results show that interest rates charged on loans fell and that may have helped in stimulating increased demand. Loans should continue to rise and profit as well going into 2019, as cash flow from profits is invested in new loans.

Jamaican Teas – PE 7.5. The group will benefit from continued growth in the local economy and increased purchasing power of Jamaicans. The star performer, export sales have grown healthily for a number of years and should continue the growth path again. Added to this, some cost incurred in 2018, are unlikely to repeat in 2019. Importantly, accounting policy IAS 9 will see all gains or losses on investments being booked through the regular profit and loss statement and that could lift profit in 2019 as local stocks continue to grow in value.

Lasco Financial – PE 6.5. The company continues to earn from Money transfer business but the real growth potential rest in the micro lending area that enjoys high profit margin. The area is crowded but entities with size can have an advantage. Additionally, Lasco has a wide network of branches, used to reach a wide potential group for granting loans.

Lasco Manufacturing – PE 8. New products and the streamlining of the business with potential for more product lines that can be added make this entity a compelling long term investment.

Medical disposables – PE 7.5. The company started as a distributor of medical and pharmaceutical distributors but has now broadened their offering to involve consumer products. The base is established for a wider range of products, using a lot of the existing infrastructure that is adding to the attractiveness of the stock. Results for the June quarter showed strong increased revenues and profit but their usually slow second quarter saw modest increased revenues and flat profit. Importantly, gross profit increased well ahead of the growth in revenues and but for a big increase in foreign exchange losses, profit in quarter and six months would have climbed strongly. Revaluation of the Jamaican dollar in the December quarter will result in a reversal of some of the foreign exchange losses.

Stationery & Office Supplies MoBay Office

PTL- PE 7.5. The company reported growth in revenues for the half year to November resulting in improvement in gross profit. Administrative cost grew higher than revenues with depreciation accounting for 25 percent of the increased cost. The company’s joint venture lubricant plant, was operational during the period and resulted in cost and revenues excluded from the six months results but included in the 2017 figures. Only the company’s share of profit is now included in the results amounting to $2 million. The company had moved into the repackaging of chlorine and bleach production in 2018. The last quarterly results have not shown much increased business from these two ventures, while they incurred increased staff cost to serve the market. Major improvement in profit, is not expected until the 2020 fiscal year that starts in June 2019 and will probably hold back the stock price for the greater part of the year.

Stationery and Office Supplies – PE 6. SOS delivered two good years on the Junior Market for early investors. IC Insider.com is forecasting another year of strong stock gains for the company. The company moved into the production of exercise books, mostly for schools and added note pads for the local and overseas markets. Other products could be added to their line up in 2019.

tTech – PE 6. Results for the September quarter almost doubled, with earnings per share reaching 12 cents, versus 6 cents in 2017, with operating revenues rising an attractive 25 percent. Profit for 2018 should hit 40 cents for the year. Management indicates that they are proactive in seeking new business locally and overseas and sees past marketing effort to attract new business now bearing fruit.

20% profit rise for ISP Finance

ISP Finance Services reported growth in net profit of 20 percent for 2017 to $48.5 million from $41 million in 2016. For the final quarter of the year profit was flat at $17.9 million versus the same period in 2016. The company reported earnings per share of 46 cents.

ISP Finance Services reported growth in net profit of 20 percent for 2017 to $48.5 million from $41 million in 2016. For the final quarter of the year profit was flat at $17.9 million versus the same period in 2016. The company reported earnings per share of 46 cents.

Increased loan provision of $7.5 million versus a recovery of $1 was the reason for the flat out turn for the December quarter. Interest income from loans rose 24.6 percent to $287 million from $231 million in 2016 while for the December quarter revenues form loans grew 24 percent to $78.5 million. Net interest income ended at $261 million compared to $205 million for the prior year, an increase of 27 percent while for the December quarter net interest income rose by 40 percent to $71 million. Employees cost rose 32 percent in the quarter to $27 million and 18 percent for the year to $108 million while other operating expenses closed the year 6 percent higher for the quarter to $17 million and 18 percent for the full year at $76 million.

ISP concluded the year with equity capital of $285 million that generated an average return of 19 percent for the year. The loan portfolio ended at $439 million, up 40 percent from $313 million in 2016 with cash funds of $30 million and borrowings of $208 million.

IC Insider.com projects earnings of $1.20 per share for 2018, the stock that is in limited supply now trades at $13.50 at a PE of 11, the great attraction for the stock is one of long term growth rather than short term gains.