Обновили на порносайте

pornobolt.tv порно страничку о том как парень выебал пизду мачехи, которая устала от своего муженька

Wystarczy zastąpić tylko jeden składnik, a dżem jabłkowy stanie się wykwintnym deserem

Zdecydowanie nie tak kisi się ogórki: kucharz wymienił zaskakujący składnik

Smażone ziemniaki po hiszpańsku: zrób tortillę – to danie zaskoczy Cię swoją prostotą i smakiem

Zamiast mąki: co dodać do ciasta naleśnikowego?

Ulubionym daniem Kozaków jest długoletni przepis na truskawki

Wiele hostess wciąż płacze podczas krojenia cebuli: 7 sprawdzonych sposobów na uniknięcie łez

Truskawki będą rosły duże i pyszne: pamiętaj o tych 4 sekretach pielęgnacji jagód

Przepis na weekend: burger z krążkami cebulowymi i soczystym pasztecikiem

Jak doświadczeni ogrodnicy odstraszają szkodniki: posadź te 4 rośliny nienawidzące owadów

Nie spodziewałeś się tego: superfinalista MasterChef mówi, gdzie umieścić grzyby, aby były smaczne

Dietetyk zasugerował, czym zastąpić majonez, ziemniaki i kaczkę na Sylwestra

Idealny przepis na leniwe weekendy: gotowanie prostego mannikina na kefirze

Nie spiesz się z wyrzucaniem starych książek: pamiętaj o 6 sposobach na ich efektywne wykorzystanie

Domowa pizza w 15 minut: ultraszybki przepis

Czym wybielać drzewa wiosną: wypróbuj te skuteczne zamienniki wapna

Płynna kutya: jak przygotować tradycyjne danie wigilijne

Rosjanie robią to cały czas: lekarz wyjaśnił, z jakich naczyń nie należy jeść kebaba

Wielu osobom przypomina makaron Carbonara: 12 niezwykłych i smacznych nadzień do ciast

Zrób to – smak znacznie się poprawi: szefowie kuchni podzielili się sprytną sztuczką dotyczącą nadziewanej papryki

Twoje życie będzie 100 razy łatwiejsze: genialne pomysły na kęsy od Héctora Jiméneza-Bravo

Przepis na derenie w garnku – jak przygotować znane danie w nowy sposób

Włóż talerz fasoli do kuchenki mikrofalowej – nie będziesz musiał moczyć fasoli przez całą noc: najlepsza sztuczka

Jak jeszcze sprytne gospodynie domowe używają nadtlenku wodoru w domu: 3 niezbędne sytuacje

Ciasto kalejdoskop: przepis na jasny i bardzo prosty deser, któremu nikt się nie oprze

Chrupiąca przekąska z pikantnym akcentem: ogórki z ziarnami gorczycy

Wanna szybko pozbędzie się kamienia: pamiętaj o tych 2 roztworach czyszczących

Teraz tylko domowe lody – przepis na crème brûlée

Najważniejsza potrawa w Wigilię: poznaj sekret prawdziwej świątecznej kutyi

Pyszny deser dla całej rodziny: przepis na ciasteczka noworoczne

Len málo Dánov si to uvedomuje: Táto ‚normálna‘ vec ničí vašu práčku a sušičku

Najnebezpečnejšia choroba na svete má 100-percentnú úmrtnosť

Žena sa nabúrala do susedovho dronu: teraz to môže mať právne dôsledky

Dievča zo šiestej triedy na besnení so zbraňou

Pozrel sa na stenu svojho suseda – potom si všimol niečo, čo ho rozzúrilo

Dick Kaysø odhalil drastickú zmenu kariéry: Neuhádnete, čo robí dnes

Tu je indický liek na korunu: Kolort

Muž nájde obrovské vajce a keď sa ho pokúsi vyraziť, zažije veľký šok

Podniknite kroky hneď teraz: Kúpte si T-Rexa v plnej veľkosti

Vyleje Coca-Colu do záchoda: výsledok je prekvapujúci

Málokto pozná príčinu pokrčených prstov po výlete do vody: toto je vysvetlenie

Takmer nikto nevie o skrytom tlačidle umývačky riadu: Bežný problém vyrieši v okamihu

Vizážisti prezradili: Vyhnite sa týmto 3 vlasovým návykom a budete vyzerať o 10 rokov mladšie

Caroline Flemingová otvorila tému tabu: Vplyv na rodinu bol obrovský

O 6 mesiacov neskôr ľudia stále bojujú s týmto obrázkom: Nájdete snežného leoparda?

Mnohí sa nad tým zamýšľali: To je to, čo znamená tá malá bodka na vašom iphone

Sadne si na miesto vo vlaku, ktoré nie je jej, a neuvedomuje si, v čom je problém

Strata vodičského preukazu a auta: nová možnosť dopravy Dennisa Knudsena vyvolala u ľudí vzburu

Pár držal lekára uväzneného v žalári a nútil ho neustále užívať drogy

Prvé zviera, ktoré v tomto teste uvidíte, určuje, či ste dobrý alebo zlý človek

Žena si kúpila zásnubný prsteň len za 9 korún: Každý o ňom hovorí len jedno

Fie Laursen priznáva závislosť od hazardných hier: Za šesť mesiacov som prehral viac ako tri milióny korún

7 miest vo vašej domácnosti, na ktoré by ste nikdy nemali vešať zrkadlo

Novorodenec nájdený v odpadkovom koši na letiskovej toalete

Test DNA odhalil, že jedno z mojich detí nie je biologicky príbuzné so mnou, ale s mojím priateľom,‘ hovorí otec

Zabudnite na Španielsko a Turecko: lacné a krásne krajiny sa stávajú čoraz obľúbenejšími dovolenkovými destináciami

Rebel Wilsonová s divokým odhalením: unesená v Afrike

Plavci si mysleli, že narazili na veľký kameň: pravda sa ukázala byť oveľa hrozivejšia

Fámy o rozvode sú čoraz častejšie: Meghan Markle si sňala zásnubný prsteň

Jes Dorph vystrelil: Tu sú 18-20 rokov staré prípady, ktoré ho priviedli k pádu

Personál leteckej spoločnosti zostal bezmocný: Žena sa postavila a pripravila cestujúcim nečakané prekvapenie

Muž skolaboval, keď mu v televíznom programe nesprávne odhadli hodinky

Dánsky kaderník so skvelým tipom: Ako ľahko zmeniť štruktúru vlasov

Oplatí sa vypnúť klimatizáciu v aute? Pozrite si odpoveď odborníka

Pani Holmová sa plavila na kanoe so svojou dcérou: Zrazu sa stretla s obrovským tvorom s medvedími pazúrmi z hlbín

Dvojičková mama v šoku: Test DNA priniesol nepredstaviteľné výsledky

Inšpektor zažije na podkroví šokujúce prekvapenie – neuveríte, čo našiel

Žena tajne nahrávala svojho manžela doma – teraz sa chce rozviesť

Jednoduchý trik, na ktorý mnoho ľudí vždy zabúda: Ako rýchlo odstrániť horúci vzduch z auta

Geggo pokračuje: ‚Želám si, aby som to nikdy neurobil

Hviezda TV 2 bola v televízii nazvaná nudným zadkom: Teraz odpovedá

Poznáte skrytú funkciu slnečnej clony vášho auta: nájdete ju tu

Mame sa vysmievali, keď dala svojmu dieťaťu meno: Znie to ako šampón

Muž fotografuje dom na predaj: Prehliadol však jeden malý detail

Sníval som o byte v Kodani: Potom sa stalo niečo nepredstaviteľné

Pár prišiel domov do svojho bytu: keď otvoril dvere, okamžite zavolal na tiesňové centrum a utiekol

Šok počas letu: cestujúci muž otvoril núdzový východ

Liama v mladom veku zasiahla rakovina v terminálnom štádiu: Varuje ostatných, aby nerobili rovnaké bežné chyby

Ušetrite veľa peňazí na účte za kúrenie: Tu je 7 účinných tipov

Hviezda TLC v divokej premene: Schudla viac ako 260 kíl

Víťaz lotérie sa podelil o správu o svojej výhre na Facebooku: Nikdy to nemala robiť

Vaše spása je v dětském penálu: podrážky vašich bot budou s touto psací potřebou sněhobílé

Jak vyčistit skvrny z bavlněných a lněných ubrusů: několik jednoduchých DIY

Miliardkrát víc cool než prášek: vyrobte si prací prostředek za halíř vlastníma rukama

O tom, zda je rám brýlí módní, rozhoduje jedna vlastnost

Proč mazané hospodyňky potírají boty peroxidem vodíku: poznáte to – takhle to budete dělat vždycky

Jen málokdo ví, v jaké kapse nosíte svůj chytrý telefon a co to znamená

Zapomeňte na bílení: stromy před škůdci ochrání účinný trik

Půjdete do vězení: Tady je, které celosvětově oblíbené léky si nesmíte přivézt z Turecka

Jak skrýt břicho a nadýchané tvary pomocí oblečení – zkuste to, budete se cítit jako královna

‚Můj manžel mě přestal bít a urážet, až když jsem vůči němu ochladla‘ – komentář psycholožky

Jak ještě zkušené hostitelky používají aktivní uhlí: 9 triků pro domácnost a kuchyni

Abyste si neudělali ze života peklo: prozrazujeme tajnou metodu čištění odtoku v koupelně bez speciálních prostředků

Ovocné stromy stříhejte pouze na jaře v tomto období: později zahradnické nůžky neberte – zničili byste celou zahradu

Jen málokdo tuší, proč se na batohy dává diamant

Úplné zmrazení úvěrů: Ruská centrální banka potěšila Rusy nečekanou zprávou

Nespěchejte s vyhazováním starého chleba: připravte si užitečnou tinkturu

Pokud bylo letošní jaro peklo: takhle byste měli vybírat kontejner pro sazenice – agronom poradil do budoucna

Bohatství podle osudu: datum narození odhalí osobní cestu k bohatství

Přestal zalévat sazenice rajčat najednou: roste, nepřestává – není potěšen

Rusové byli jmenováni měsícem, kdy bude nejmenší mzda z důvodu dovolené nebo nemocenské

Tohle vás ohromí – proč si řidiči se zkušenostmi dávají pod kola pytle

Tajemství slavných kuchařů : 10 tipů a triků z kuchařských pořadů

Libido bude jako za mlada: psycholog dal cenné rady ženám, které stárnou

Potřete matraci jedlou sodou a nechte ji hodinu působit: nebudete věřit, co se stane potom

Alexander Vasiljev prozradil hlavní tajemství, jak ušetřit peníze za nákupy oblečení

Tohle tajemství znají jen mazané hostitelky – proto si doma dávají sáčky z obchodu do lahve

5 nejčastějších chyb, které ničí sazenice: dělá je mnoho dachařů a pak toho litují

Moudré hospodyňky čistí pračku pomocí pleny: jednoduché a pohodlné – žádný rozruch

Rekreanti piští nadšením – na pozemku nejsou komáři a komáři: vezměte si papír a kávu

Nevylévejte zbytky vína: 8 využití v domácnosti a kuchyni

Nevyhazujte plastová víčka: 12 způsobů využití v domácnosti i v k

V showroomu vám o nich neřeknou: odborníci pojmenovali nevyléčitelné ‚nemoci‘ čínských aut

Nervozita je hračka: 3 způsoby, jak snížit stres v práci

Lékař řekl, jak se správně stravovat během nemoci

Toto oblíbené hnojivo zničí vaše muškáty: místo čepice květů dostanete suchou tyčinku

Jak rychle odstranit mastné skvrny z oblečení: trik s mycím prostředkem pro kutily

‚Brežněvův‘ vrchní obvaz udělá zázraky: sklidí rekordní úrodu okurek

Top účesy, které si můžete udělat doma před zrcadlem: ani netušíte, co přišlo do módy (foto)

Zbavte se žroutů elektřiny: 3 triky, které vám přinesou vážné úspory

Zatímco jiné květiny chřadnou, tyto rostou jako rajská zahrada: zasaďte si je na chalupě, nebudete litovat

3 nejlepší odrůdy okurek do salátů: nenáročné a plodící až do zámrazu

Pár postřiků a už žádné štěnice: tyto 3 postřiky škůdce jednoduše vyženou

Mnoho hospodyněk nesprávně vylévá vařící vodu do dřezu: zde je uvedeno, co se může poškodit

Příchod skutečné zimy: Rusové varovali před 50 hodinami sněžení a mrazem až -14

Jak zachránit zahradu v zimě: nedělejte tyto chyby

Vložte talíř se solí na noc do mikrovlnné trouby: uvidíte, co se stane ráno

2 ramínka + 1 taška: věčný problém s nedostatkem místa ve skříni je vyřešen během 30 sekund

Nevyhazujte bublinkovou fólii: 9 užitečných způsobů, jak ji využít v domácnosti a v domácnosti

Nahradí všechny brýle: kupte si jen takový doplněk – hlavní trend pro léto 2023

Zapište si do sešitu: 5 hlavních tradic pro nový rok jsou jmenovány – pak se určitě stane zázrak

Přikrmte fialky sladkým produktem z vaší kuchyňské skříňky: budou dlouho a bujně kvést

Mult mai mult decât resturi alimentare: de ce nu ar trebui să arunci niciodată cojile de ouă

Ținuta unei femei a dus la concediere: Nu crede că este nepotrivită

Cum să îndepărtezi zgârieturile de pe geamurile mașinii: 2 trucuri pe care le poți folosi chiar tu

Un tânăr de 18 ani a câștigat 250 de milioane de coroane daneze după ce și-a cumpărat primul bilet de loterie

Noul burger de la McDonald’s devine viral: Vezi de ce îl adoră clienții!

O emisiune TV merge prost: Umut Sakarya și Bubber sunt evacuați dintr-un autobuz în flăcări

Soțul a deconectat ventilatorul soției sale inconștiente și i-a șoptit la ureche: La scurt timp după aceea, ea îi șochează pe doctori

Merită să opriți aerul condiționat din mașină? Vedeți răspunsul expertului

O familie și-a predat câinele de 3 ani la un adăpost: Nu vei ghici niciodată motivul

Bărbat pe punctul de a intra pe ușa din fața casei sale: Deodată este atacat de ceva foarte neașteptat

Foarte puțini oameni își dau seama de acest lucru: Pentru asta sunt proiectate de fapt mânerele mașinii dumneavoastră

Era mică cât o unghie când a găsit-o în plimbarea ei prin pădure

O femeie supraponderală a rezervat două locuri în avion: A refuzat să împartă locul cu un băiețel de 1 an

Personalul unui supermarket își exprimă frustrarea față de clienți: Mă enervează

A fost filmată o scenă înfricoșătoare în casa chiriașului: A stat treaz toată noaptea de teamă că se va întoarce cu o altă armă

A vrut doar să spele rufe: Apoi a făcut o descoperire șocantă

Expertul dezvăluie: Unde să vă amplasați detectoarele de fum

Vezi video: Sărutul din reclama la ciocolată stârnește indignare

Esther nu-și lasă fiul de 15 ani să se angajeze: Motivul te va surprinde

Mașina de spălat este plină de bacterii: un truc simplu face posibilă eradicarea lor în cel mai scurt timp

August locuiește într-o rulotă care nu pare cine știe ce: stai să vezi interiorul

Oamenii de știință au găsit, în sfârșit, explicația pentru calendarul mayaș

Bărbatul avea dureri de cap puternice și chiar pierderea vederii: Când a fost scanat, medicii au descoperit ceva neașteptat

Sunt un expert în călătorii: Nu ar trebui să faci niciodată un duș înainte de un zbor de dimineață devreme

Tragedie: Un bărbat și un copil au murit într-un incendiu într-un apartament

Nu turnați niciodată apă clocotită în chiuvetă: Iată un mesaj important pentru toți cei care o fac

A primit un mesaj de la soțul ei: și-a dat seama imediat că ceva nu era în regulă

Secretul întunecat dezvăluit: Porsche a ascuns acest lucru

Un bărbat toarnă o linguriță de ulei de măsline într-un iaz – puțini sunt cei care cunosc acest fenomen

Nu doar din cauza prețului: de ce ar trebui să călătoriți doar cu bagaj de mână

Cei mai mulți oameni nu-și dau seama de acest lucru: Această setare epuizează bateria iPhone-ului dumneavoastră

Un turist a comandat un sandviș la un restaurant din Italia: Când a văzut nota de plată, nu i-a venit să creadă ce vede

Presară orez peste ștergarul umed: Când vei vedea ce se întâmplă, vei face la fel

Adolescentă trimisă acasă pentru o ținută nepotrivită: Nu a înțeles de ce și și-a asumat consecințele

Vizită la Urgențe după descoperirea unui șoc în produsul Rema 1000: Acum iubitul are un avertisment

Tiffany a slăbit 45 kg în timp record: A renunțat la un anumit lucru

Linda, în vârstă de 23 de ani, se plânge că este prea bogată și provoacă furie: ‘Îmi cumpără prea multe lucruri

Un bărbat își pierde cheile de la mașină: Când s-a întors la mașină, a avut un șoc imens

Un bărbat a ajuns de urgență la spital cu insuficiență multiplă de organe: Acum medicii avertizează copiii și adolescenții

O femeie și-a pierdut piciorul după ce a rămas blocată în scara rulantă a unui aeroport

O femeie a comandat o cafea la McDonald’s – dar ceea ce a urmat i-a dat fiori pe șira spinării

Angajata unei bănci a avut parte de șocul vieții ei: N-o să-ți vină să crezi ce i-a oferit această femeie

El adaugă un ingredient în mașina de spălat la fiecare 4 săptămâni.săptămână: Așteptați să vedeți cum se întâmplă magia

Un băiat de 12 ani, acuzat de medici că a dramatizat prea mult simptomele: La scurt timp, a rămas paralizat

Anders și Torben au fost în direct la televizor: în timp ce casa era jefuită

Comoară neașteptată descoperită sub covor: O femeie se bucură de descoperire

Când ar trebui să decorați pentru Crăciun? Aceasta este data perfectă, potrivit experților

Mașina de spălat este plină de bacterii: cu acest truc ingenios le puteți eradica în cel mai scurt timp

Foarte puțini oameni își dau seama de acest lucru: Aceasta este semnificația culorii buretelui de bucătărie

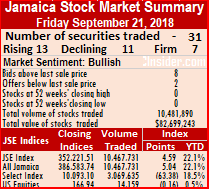

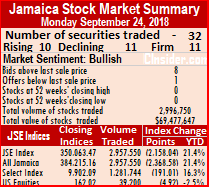

The Jamaica Stock Exchange main market closed, with the All Jamaica Composite Index losing 2,368.58 points to 384,215.16 and the JSE Index dipping 2,158.04 points to 350,063.47.

The Jamaica Stock Exchange main market closed, with the All Jamaica Composite Index losing 2,368.58 points to 384,215.16 and the JSE Index dipping 2,158.04 points to 350,063.47.

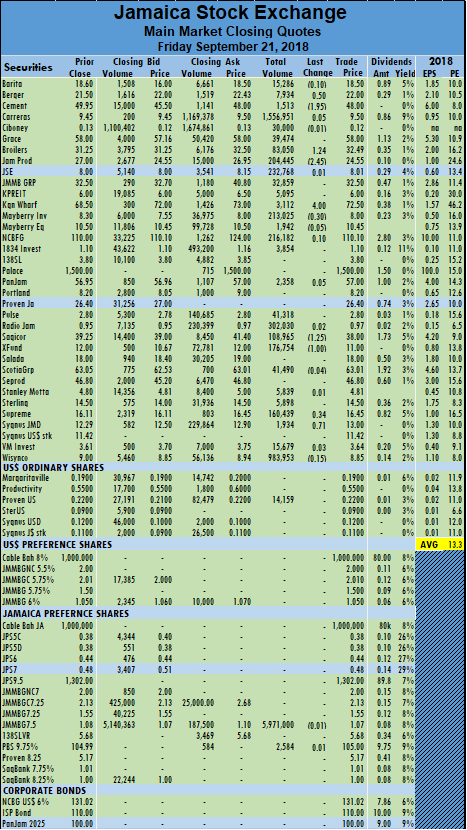

in the exchange of 162,322 shares,

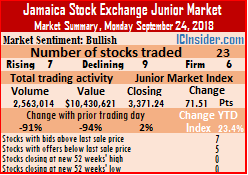

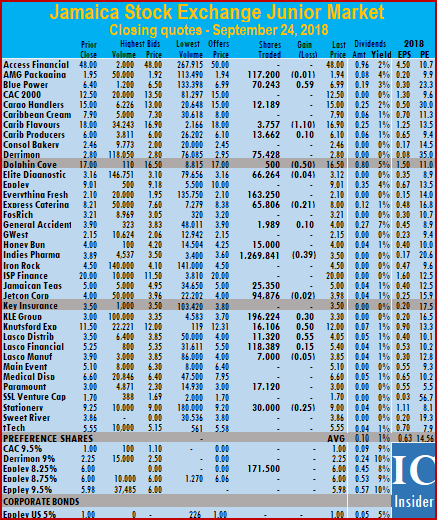

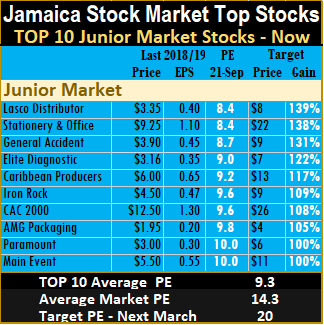

in the exchange of 162,322 shares,  The Junior Market Index recovered 71.51 of the 136.58 points lost on Friday, to close at 33,371.24, on Monday as 7 securities rose to a decline of 9.

The Junior Market Index recovered 71.51 of the 136.58 points lost on Friday, to close at 33,371.24, on Monday as 7 securities rose to a decline of 9.  Trading for the month to date averages 518,389 units for an average of $3,054,135 and on the prior trading day, an average of 541,966 units for an average of $3,204,801. Trading in August, averaged 244,613 units at $1,348,298 for each security traded.

Trading for the month to date averages 518,389 units for an average of $3,054,135 and on the prior trading day, an average of 541,966 units for an average of $3,204,801. Trading in August, averaged 244,613 units at $1,348,298 for each security traded. Honey Bun ended at $4, in exchanging 15,000 units, Indies Pharma lost 39 cents and closed with 1,269,841 shares changing hands to close at $3.50, Jamaican Teas settled trading of 25,350 shares at $5, Jetcon Corporation ended trading 94,876 stock units with a loss of 2 cents at $3.98. KLE Group finished trading 30 cents higher at $3.30, with 196,224 shares changing hands,

Honey Bun ended at $4, in exchanging 15,000 units, Indies Pharma lost 39 cents and closed with 1,269,841 shares changing hands to close at $3.50, Jamaican Teas settled trading of 25,350 shares at $5, Jetcon Corporation ended trading 94,876 stock units with a loss of 2 cents at $3.98. KLE Group finished trading 30 cents higher at $3.30, with 196,224 shares changing hands,

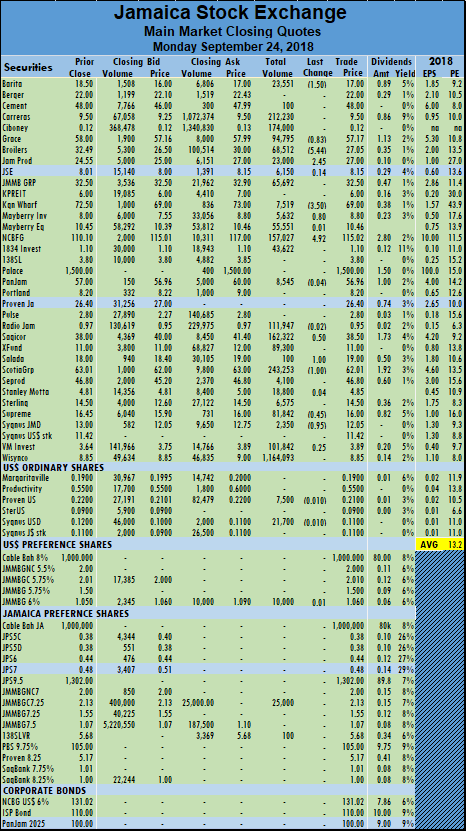

Everything Fresh is one of a hand full of initial public stock offers to be selling below the IPO price months after the issue. The stock that was over priced has only been partially helped by a big jump in 2018 half year profit.

Everything Fresh is one of a hand full of initial public stock offers to be selling below the IPO price months after the issue. The stock that was over priced has only been partially helped by a big jump in 2018 half year profit.

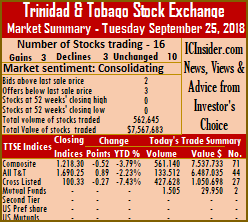

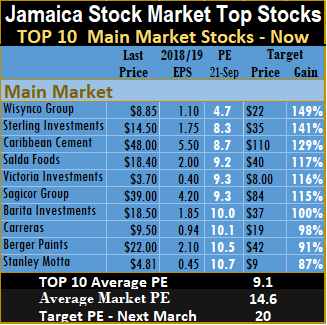

During the past week, the main market of the Jamaica Stock Exchange, racked up more record closes but pulled back on sharply on Thursday and Junior market hit new highs during the week but dropped sharply on Friday due mainly to

During the past week, the main market of the Jamaica Stock Exchange, racked up more record closes but pulled back on sharply on Thursday and Junior market hit new highs during the week but dropped sharply on Friday due mainly to  The PE ratio for Junior Market Top 10 stocks average 9.3 up from 8.9 last week, as the market continues to revalue the multiple higher and the main market PE is now 9.1, up from 8.8 last week, for the top stocks.

The PE ratio for Junior Market Top 10 stocks average 9.3 up from 8.9 last week, as the market continues to revalue the multiple higher and the main market PE is now 9.1, up from 8.8 last week, for the top stocks. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.