Main Event backed with IC BUY RATED status

Growth in revenues while not an exact proxy for increased profits, is often a very good indicator of greater gains ahead. That may be exactly what is happening at the Junior market listed Main Event.

The results for the nine months to July show strong sales growth but flat profits. Revenues for the July quarter surged nearly 26 percent to $364 million, but profit fell 7 percent to $24.5 million from $26.3 million in 2017. For the nine months to July, profit was up just 4 percent to $105.5 million that flowed from a 13 percent rise in revenues to $1.07 billion, compared to net income of $101 million in 2017.

The company incurred increased cost as it seeks to expand its service offerings. The results to date suggest that the full year earnings will not vary much from the 2017 full year results of 37 cents. But 2019 could be a blow out year for them, if revenue growth seen so far for this year, continues into 2019.

Profit margin in the first half of the year, was held to the same level as in 2017, at 48 percent and declined in the July quarter to 45 percent from 49 percent in the 2017, the impact, operating profit rose just 15 percent in the quarter to $164 million from $143 million but fell to 14 percent for the year to date, to $512 million from $447 million in 2017.

Administrative expenses rose 20 percent to $111 million in the quarter and increased 15 percent in the nine months period to $311 million. Marketing and sales expenses increased by 44 percent to $15 million for the nine months. Depreciation rose 49 percent to $24 million in the quarter and increased 29 percent in the nine months to $69 million, an indication of increased capital spend to accommodate expansion and increased income. Finance cost was flat in the quarter, at $5.2 million and rose just 5 percent to $13.6 million for the nine months.

Earnings per share came out at 9 cents for the quarter and 37 cents for the nine months and should end the fiscal year around 40 cents. For 2019 earnings should be in the order of a string increase to 75 cents.

“Performance has been negatively impacted by write downs on trade receivables to align to reporting standard, IFRS 9, continued start up expenditure for new service offerings and cost with higher head counts and incentive compensation,” the Chairman Ian Blair and Chief Executive Officer reported to shareholders in their commentary accompanying the quarterly.

Gross cash flow brought in $175 million but growth in receivables, inventories, addition to fixed assets of $160 million, offset by net loan inflows and increased payables resulted in net cash flow ended at a negative $63 million and leaving $29 million in cash at the end of July. Shareholders’ equity stood at $551 million with borrowings at just $185 million, including amounts due to related parties. Net current assets ended the period at $141 million, inclusive of trade and other receivables of $304 million, cash and bank balances of $29 million. Current liabilities amounted to $209 million inclusive of short term borrowings.

The stock traded at $5.50 on the Junior Market of the Jamaica Stock Exchange with a relatively low PE ratio of 7.3 times 2018 earnings and is elevated to BUY RATED status.

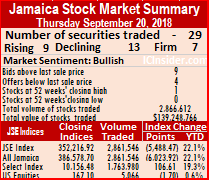

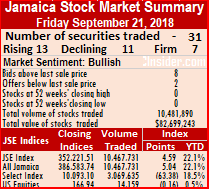

During the past week, the main market of the Jamaica Stock Exchange, racked up more record closes but pulled back on sharply on Thursday and Junior market hit new highs during the week but dropped sharply on Friday due mainly to

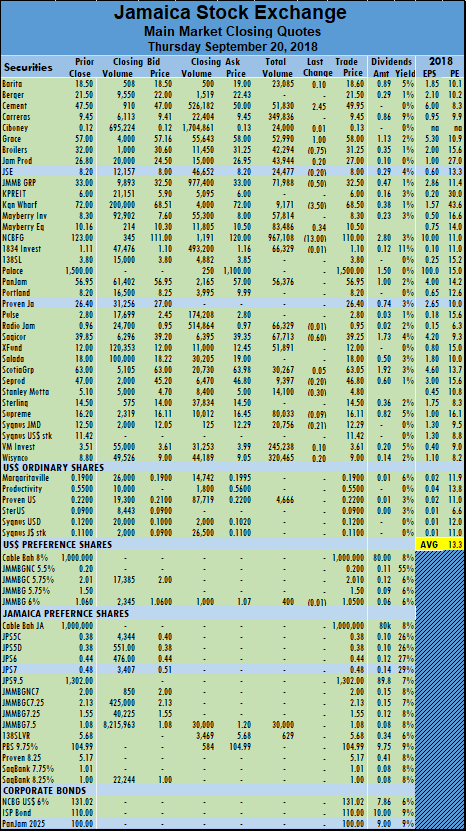

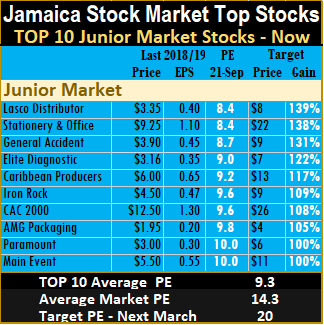

During the past week, the main market of the Jamaica Stock Exchange, racked up more record closes but pulled back on sharply on Thursday and Junior market hit new highs during the week but dropped sharply on Friday due mainly to  The PE ratio for Junior Market Top 10 stocks average 9.3 up from 8.9 last week, as the market continues to revalue the multiple higher and the main market PE is now 9.1, up from 8.8 last week, for the top stocks.

The PE ratio for Junior Market Top 10 stocks average 9.3 up from 8.9 last week, as the market continues to revalue the multiple higher and the main market PE is now 9.1, up from 8.8 last week, for the top stocks. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

The above list has no contract in connection with the issue of preference shares to shareholders prior to the IPO.

The above list has no contract in connection with the issue of preference shares to shareholders prior to the IPO. Further, by an ordinary resolution dated November 28, 2017 the 10,000 shareholdings of shareholders on register at November 27, 2017 were split such that their holdings of ordinary shares became 10,000,000 ordinary shares. Additionally, the shareholders who were allocated the 9,800 available shares at March 31, 2017, were further allocated 314,848,485 ordinary shares for the consideration of $50 million of interest converted to capital on March 31, 2017. (13.3) On December 7, 2017 the company made an offer for subscription to the public (IPO), of 160,000,000 of its ordinary shares at a price of $2.50 per share through the Junior Market of the Jamaica Stock Exchange (JSE). The company was officially registered on the Junior Stock Market on December 21, 2017. Total cost of the IPO of $30.848 million has been off-set against the issued share capital.”

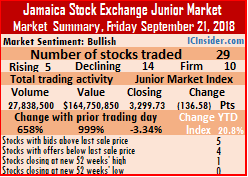

Further, by an ordinary resolution dated November 28, 2017 the 10,000 shareholdings of shareholders on register at November 27, 2017 were split such that their holdings of ordinary shares became 10,000,000 ordinary shares. Additionally, the shareholders who were allocated the 9,800 available shares at March 31, 2017, were further allocated 314,848,485 ordinary shares for the consideration of $50 million of interest converted to capital on March 31, 2017. (13.3) On December 7, 2017 the company made an offer for subscription to the public (IPO), of 160,000,000 of its ordinary shares at a price of $2.50 per share through the Junior Market of the Jamaica Stock Exchange (JSE). The company was officially registered on the Junior Stock Market on December 21, 2017. Total cost of the IPO of $30.848 million has been off-set against the issued share capital.” The Junior Market dropped by an unusually large 136.58 points to close at 3,299.73 on Friday as

The Junior Market dropped by an unusually large 136.58 points to close at 3,299.73 on Friday as

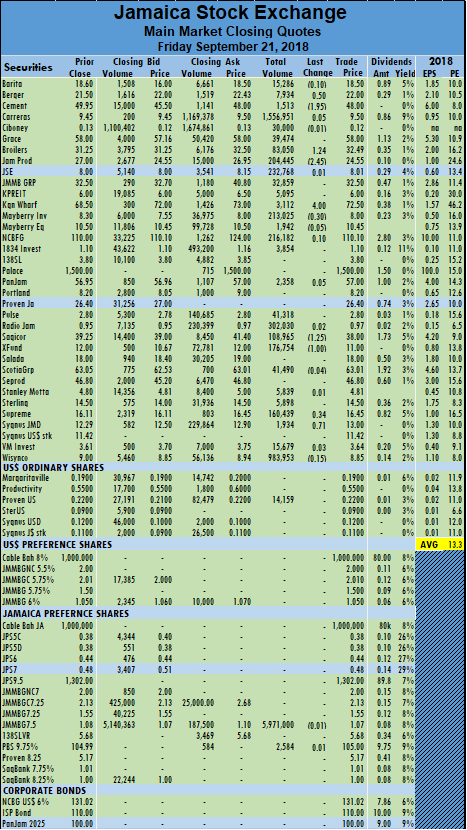

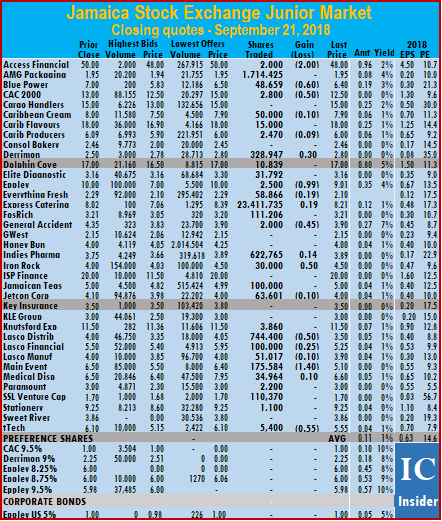

General Accident finished trading 2,000 shares with a loss of 45 cents at $3.90, Indies Pharma gained 14 cents and closed trading with 622,765 shares changing hands at $3.89,

General Accident finished trading 2,000 shares with a loss of 45 cents at $3.90, Indies Pharma gained 14 cents and closed trading with 622,765 shares changing hands at $3.89,  Express Catering traded more than 23 million with the price dropping from $8.02 at the close on Thursday to $6.40 in the morning session of trading on the Junior Market and along with Lasco Distributors that fell to $3.50 and Main Event that traded at $5.10 from $6.50 did immense damage to the market index on Friday.

Express Catering traded more than 23 million with the price dropping from $8.02 at the close on Thursday to $6.40 in the morning session of trading on the Junior Market and along with Lasco Distributors that fell to $3.50 and Main Event that traded at $5.10 from $6.50 did immense damage to the market index on Friday. All market indices of the Trinidad & Tobago Stock Exchange, ended with modest gains on Friday as 17 securities changed hands up from 13 on Thursday.

All market indices of the Trinidad & Tobago Stock Exchange, ended with modest gains on Friday as 17 securities changed hands up from 13 on Thursday.  ended at $56, with 416 stock units changing hands, Ansa Merchant completed trading at $38, with 1,226 units, Clico Investments settled at $19.90, after exchanging 11,000 shares, First Citizens completed trading at $32.60, with 50 units, JMMB Group ended at $1.65, with 7,439 stock units changing hands, Massy Holdings ended at $47.20, in exchanging 6,764 stock units NCB Financial Group completed trading 19,050 units at $5.73, Republic Financial Holdings ended at $103.69, with 187 stock units changing hands, Sagicor Financial completed trading at $7.70, with 50,000 units, Scotiabank ended at $64.94, in exchanging 10,512 stock units and West Indian Tobacco concluded at $88.45, after exchanging 1,062 shares.

ended at $56, with 416 stock units changing hands, Ansa Merchant completed trading at $38, with 1,226 units, Clico Investments settled at $19.90, after exchanging 11,000 shares, First Citizens completed trading at $32.60, with 50 units, JMMB Group ended at $1.65, with 7,439 stock units changing hands, Massy Holdings ended at $47.20, in exchanging 6,764 stock units NCB Financial Group completed trading 19,050 units at $5.73, Republic Financial Holdings ended at $103.69, with 187 stock units changing hands, Sagicor Financial completed trading at $7.70, with 50,000 units, Scotiabank ended at $64.94, in exchanging 10,512 stock units and West Indian Tobacco concluded at $88.45, after exchanging 1,062 shares.