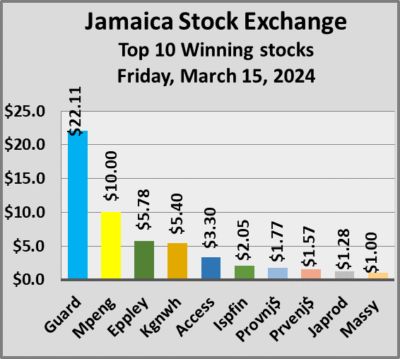

All three markets of the Jamaica Stock Exchange closed high in trading on Friday with trading ending with the number and the value of stocks changing hands falling, compared with the previous trading day and resulting in prices of 39 shares rising and 30 declining.

At the close of trading, the JSE Combined Market Index climbed 1,883.78 points to 341,888.19, the All Jamaican Composite Index climbed 1,253.54 points to end at 367,796.95, the JSE Main Index gained 1,821.11 points to wrap up trading at 328,795.31. The Junior Market Index popped 20.08 points to culminate at 3,828.57 and the JSE USD Market Index advanced 5.05 points to finish at 249.19.

At the close of trading, the JSE Combined Market Index climbed 1,883.78 points to 341,888.19, the All Jamaican Composite Index climbed 1,253.54 points to end at 367,796.95, the JSE Main Index gained 1,821.11 points to wrap up trading at 328,795.31. The Junior Market Index popped 20.08 points to culminate at 3,828.57 and the JSE USD Market Index advanced 5.05 points to finish at 249.19.

At the close of trading, 23,484,571 shares were exchanged in all three markets, compared with 29,437,556 units on Thursday, with the value of stocks traded on the Junior and Main markets amounted to $77.55 million, down from $153.98 million on the previous trading day and the JSE USD market closed with an exchange of 262,328 shares for US$19,513 compared to 771,589 units at US$17,159 on Thursday.

Trading in the Main Market was dominated by Wigton Windfarm with 12.52 million shares followed by Radio Jamaica with 3.02 million units, Transjamaican Highway closed with 1.62 million units and Carreras finished trading with 1.02 million units.

In the Junior Market, Stationery and Office Supplies led trading with 641,945 shares followed by Lasco Manufacturing with 308,644 stock units and JFP Ltd with 225,478 units.

In the Junior Market, Stationery and Office Supplies led trading with 641,945 shares followed by Lasco Manufacturing with 308,644 stock units and JFP Ltd with 225,478 units.

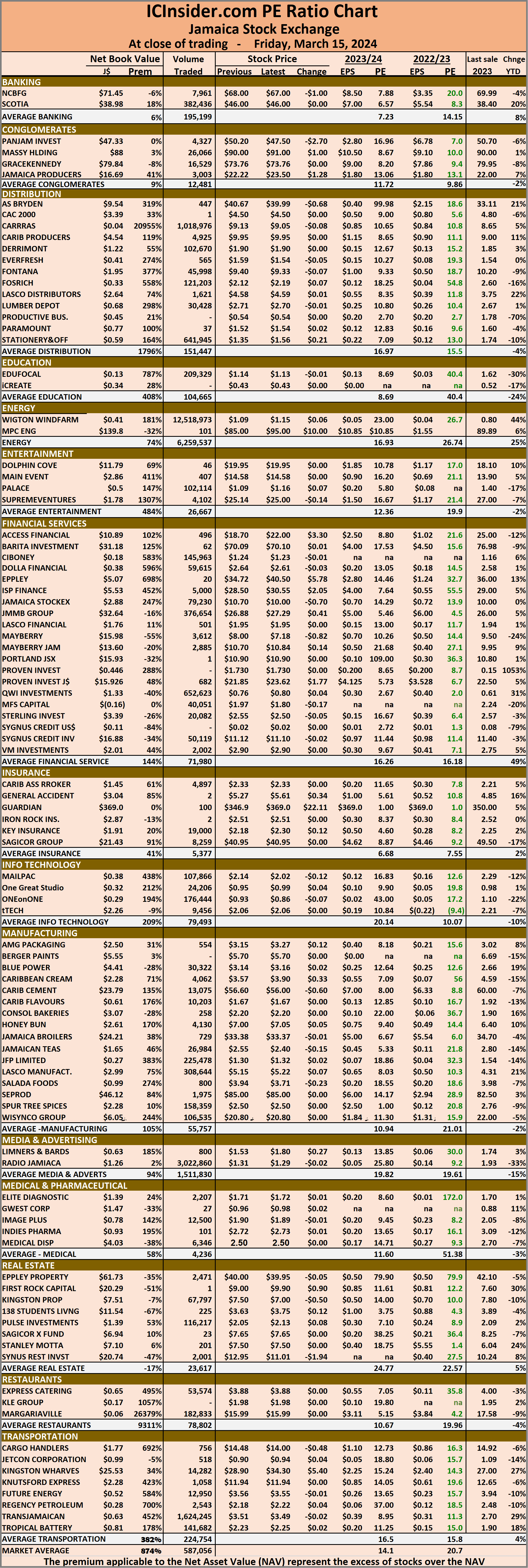

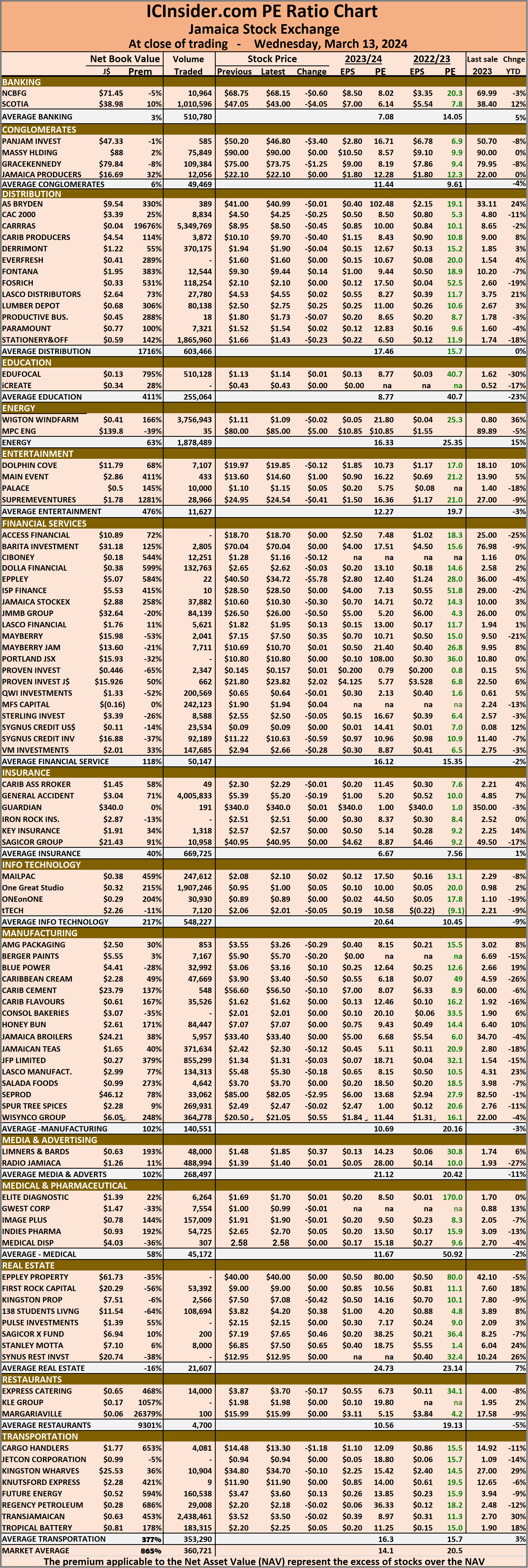

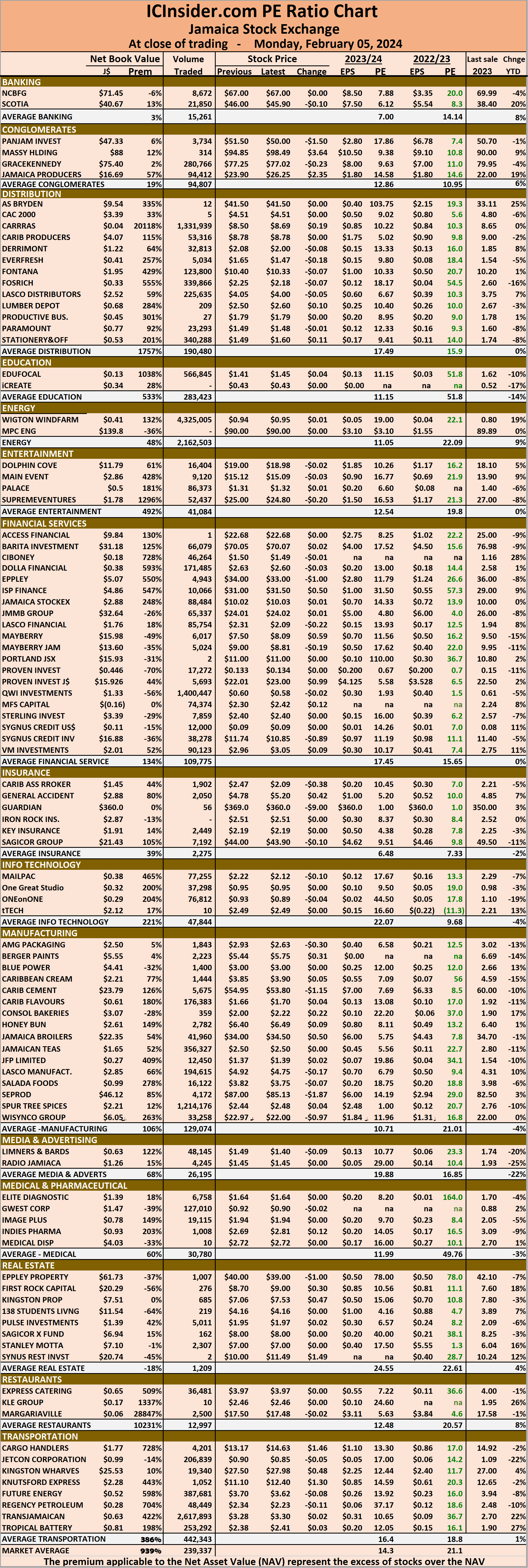

The market’s PE ratio, the most popular measure used to determine the value of stocks, ended at 20.7 on 2022-23 earnings and 14.1 times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily charts provide investors with regularly updated information to help decision-making.

The PE ratio chart covers all ordinary shares on the Jamaica Stock Exchange, grouped by industry, allowing for easy comparisons between the same sector companies and the overall market. The EPS & PE ratios are based on 2023 and 2024 actual or projected earnings, excluding major one off items.

Investors need pertinent information to navigate numerous investment options successfully in the stock market. The ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

The net asset value of each company is reported as a guide for investors to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

The net asset value of each company is reported as a guide for investors to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

Dividends paid or payable and yields for each company are shown in the Main and Junior Markets’ daily report charts, along with the closing volume pertaining to the highest bid and the lowest offer for each company.

Main and USD markets drop Juniors rise

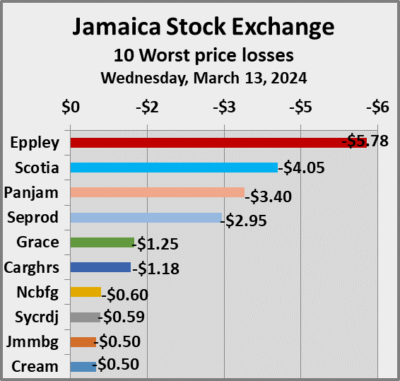

The Main Market and JSE USD stocks plunged on the Jamaica Stock Exchange on Wednesday as the Junior Market closed moderately higher as trading ended with the number of stocks changing hands falling, with the value and volume of stocks traded falling from the previous trading day, resulting in prices of 27 shares rising and 43 declining.

At the close of trading on Wednesday, the JSE Combined Market Index dived 3,639.94 points to 39,676.83, the All Jamaican Composite Index plunged 4,423.34 points to end trading at 366,211.78, the JSE Main Index dropped 3,917.90 points to lock up trading at 326,885.56. The Junior Market Index rallied 3.93 points to conclude trading at 3,780.58 and the JSE USD Market Index dipped 8.85 points to settle at 247.53.

At the close of trading on Wednesday, the JSE Combined Market Index dived 3,639.94 points to 39,676.83, the All Jamaican Composite Index plunged 4,423.34 points to end trading at 366,211.78, the JSE Main Index dropped 3,917.90 points to lock up trading at 326,885.56. The Junior Market Index rallied 3.93 points to conclude trading at 3,780.58 and the JSE USD Market Index dipped 8.85 points to settle at 247.53.

At the close of trading, 27,700,537 shares were exchanged in all three markets, from 42,523,060 units on Tuesday, with the value of stocks traded on the Junior and Main markets amounted to $172.24 million, down from $289.25 million on the previous trading day and the JSE USD market closed with an exchange of 110,543 shares for US$13,237 compared to 2,937,043 units at US$118,791 on Tuesday.

Trading in the Main Market was dominated by Carreras with 5.35 million shares followed by General Accident with 4.01 million units, Wigton Windfarm with 3.76 million units, Transjamaican Highway with 2.44 million shares and Scotia Group with 1.01 million units

In the Junior Market One Great Studio led trading with 1.91 million shares followed by Stationery and Office Supplies with 1.87 million units and JFP Ltd with 855,299 stocks.

The market’s PE ratio, the most popular measure used to determine the value of stocks, ended at 21 on 2022-23 earnings and 14. times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily charts provide investors with regularly updated information to help decision-making.

The market’s PE ratio, the most popular measure used to determine the value of stocks, ended at 21 on 2022-23 earnings and 14. times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily charts provide investors with regularly updated information to help decision-making.

The PE ratio chart covers all ordinary shares on the Jamaica Stock Exchange, grouped by industry, allowing for easy comparisons between the same sector companies and the overall market. The EPS & PE ratios are based on 2023 and 2024 actual or projected earnings, excluding major one off items.

Investors need pertinent information to navigate numerous investment options successfully in the stock market. The ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

The net asset value of each company is reported as a guide for investors to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

The net asset value of each company is reported as a guide for investors to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

Dividends paid or payable and yields for each company are shown in the Main and Junior Markets’ daily report charts, along with the closing volume pertaining to the highest bid and the lowest offer for each company.

All Markets rise on Monday

All three markets of the Jamaica Stock Exchange recorded gains in indices at the close of trading on Monday with the number of stocks changing hands and the value of stocks traded rising over the previous trading day resulting in prices of 35 shares rising and 3 declining.

At the close of trading, the JSE Combined Market Index climbed 3,886.27 points to close at 346,024.78, the All Jamaican Composite Index rose 2,499.80 points to lock up trading at 369,213.68, the JSE Main Index rallied 4,036.96 points to conclude trading at 333,377.53. The Junior Market Index rose 11.44 points to end at 3,810.21 and the JSE USD Market Index popped 1.01 points to conclude trading at 252.02.

At the close of trading, 16,865,715 shares were exchanged in all three markets, up from 17,913,688 units on Friday, with the value of stocks traded on the Junior and Main markets amounted to $79.13 million, up from $65.21 million Friday and the JSE USD market closed with an exchange of 186,772 shares for US$6,867 down from 1,000,615 units at US$122,251 on Friday.

At the close of trading, 16,865,715 shares were exchanged in all three markets, up from 17,913,688 units on Friday, with the value of stocks traded on the Junior and Main markets amounted to $79.13 million, up from $65.21 million Friday and the JSE USD market closed with an exchange of 186,772 shares for US$6,867 down from 1,000,615 units at US$122,251 on Friday.

Main Market trading was dominated by Wigton Windfarm trading with 4.33 million shares followed by Transjamaican Highway with 2.62 million units, QWI Investments ended with 1.40 million stock units and Carreras, 1.33 million stocks.

In the Junior Market, Spur Tree Spices led trading with 1.21 million shares followed by EduFocal with 566,845 stock units and Future Energy with 387,681 units.

At the close of the market, some Main Market stocks that rose were Jamaica Producers rallying $2.35 to close at $26.25, Massy Holdings rising $3.64 to $98.49, Proven Investments increasing 99 cents to $23 and Sygnus Real Estate Finance climbing $1.49 and ended at $11.49.

The major declining Main Market stocks include Caribbean Cement down $1.15 to $53.80, Eppley sinking $1 in closing at $33, Eppley Caribbean Property Fund shedding $1 to end at $39, Pan Jamaica dipping $1.50 to $50, Seprod declining $1.87 to end at $85.13, Sygnus Credit Investments dropping 89 cents in closing at $10.85 and Wisynco Group which skidded 97 cents to close at $22.

The major declining Main Market stocks include Caribbean Cement down $1.15 to $53.80, Eppley sinking $1 in closing at $33, Eppley Caribbean Property Fund shedding $1 to end at $39, Pan Jamaica dipping $1.50 to $50, Seprod declining $1.87 to end at $85.13, Sygnus Credit Investments dropping 89 cents in closing at $10.85 and Wisynco Group which skidded 97 cents to close at $22.

Stocks ending with major gains in the Junior Market are Cargo Handlers up $1.46 to $14.63, ISP Finance increasing 50 cents to $31.50, Knutsford Express advancing $1.30 to $12.40, with the major losing stock being Caribbean Assurance Brokers that sank 38 cents in closing at $2.09.

In the preference segment, Jamaica Public Service 7% rallied $4.19 and ended at $46.09.

The market’s PE ratio, the most popular measure used to determine the value of stocks, ended at 21.1 on 2022-23 earnings and 14.3 times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily charts provide investors with regularly updated information to help decision-making.

The PE ratio chart covers all ordinary shares on the Jamaica Stock Exchange, grouped by industry, allowing for easy comparisons between the same sector companies and the overall market. The EPS & PE ratios are based on 2023 and 2024 actual or projected earnings, excluding major one off items.

Investors need pertinent information to navigate numerous investment options successfully in the stock market. The ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

The net asset value of each company is reported as a guide to quickly assess the value of stocks based on this measure. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

Dividends paid or payable and yields for each company are shown in the Main and Junior Markets’ daily report charts, along with the closing volume pertaining to the highest bid and the lowest offer for each company.

Main & JSE USD Market, Juniors drop

The Junior Market of the Jamaica Stock Exchange gave back just under a half of the gains posted on Thursday but the Main and the JSE USD markets rallied to close out the day higher than the opening, with the volume of stocks traded rising moderately, with trading ending with the value rising over the previous trading day and the market closed with prices of 39 shares gaining and 33 declining.

At the close of the market, the JSE Combined Market Index climbed 1,085.09 points to 336,104.77, the All Jamaican Composite Index rallied 1,200.87 points to 360,257.92, the JSE Main Index rose 1,549.21 points to 323,274.84. The Junior Market Index fell 42.00 points to 3,759.37 and the JSE USD Market Index popped 3.31 points to end at 247.45.

At the close of the market, the JSE Combined Market Index climbed 1,085.09 points to 336,104.77, the All Jamaican Composite Index rallied 1,200.87 points to 360,257.92, the JSE Main Index rose 1,549.21 points to 323,274.84. The Junior Market Index fell 42.00 points to 3,759.37 and the JSE USD Market Index popped 3.31 points to end at 247.45.

At the close of trading, 23,219,570 shares were exchanged in all three markets, moderately more than the 23,131,587 units on Thursday, with the value of stocks traded on the Junior and Main markets amounted to $125.91 million, up from $96.67 million trading on the previous day and the JSE USD market closed with an exchange of 670,997 shares for US$26,968 compared to 119,808 units at US$30,732 on Thursday.

Main Market trading was dominated by Wigton Windfarm with 2.90 million shares followed by Transjamaican Highway with 2.44 million units and Sagicor Select Financial Fund ending with 514,757 units.

In the Junior Market, Mailpac Group led trading with 4.76 million shares followed by Dolla Financial with 1.45 million units, Stationery and Office Supplies ended with 1.36 million stocks, Regency Petroleum closed with 1.27 million shares and One Great Studio with 1.14 million units.

At the close of the market, some of the major Main Market stocks that rose are Massy Holdings popped $2 to end at $90, Pan Jamaica rallying $3.90 to $50, Proven Investments advancing $5.05 to $27, Sagicor Group popping $1 to close at $43 as Seprod climbed $2.05 in closing at $85.55.

At the close of the market, some of the major Main Market stocks that rose are Massy Holdings popped $2 to end at $90, Pan Jamaica rallying $3.90 to $50, Proven Investments advancing $5.05 to $27, Sagicor Group popping $1 to close at $43 as Seprod climbed $2.05 in closing at $85.55.

The major declining Main Market stocks include AS Bryden with a loss of 99 cents in ending at $42, Jamaica Producers declining $1.15 to close at $21.66, Scotia Group skidding 96 cents to end at $40.50.

Stocks ending with major gains in the Junior Market are, Caribbean Cream up 34 cents to close at $3.79, Iron Rock Insurance increasing 32 cents and ending at $2.42 and Mailpac Group advancing 25 cents to close at $2.28, the major losing stocks are AMG Packaging dipping 35 cents in closing at $2.60, Dolphin Cove losing 40 cents and ended at $18.60 and Regency Petroleum dropping 23 cents to $2.15.

In the preference segment, Eppley 7.25% preference share shed $1.90 to close at $17, Eppley 7.75% dropped $4.95 to end at $18, 138 Student Living preference share rose $28.84 in closing at $221.12, Productive Business Solutions 10.5% gained $125 and ended at $1200 clearing the market with 170 stocks and recently listed Sygnus Credit Investments c10.5% advanced $2 to $107.

The market’s PE ratio, the most popular measure used to determine the value of stocks, ended at 20.8 on 2022-23 earnings and 14 times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily charts provide investors with regularly updated information to help decision-making.

The PE ratio chart covers all ordinary shares on the Jamaica Stock Exchange, grouped by industry, allowing for easy comparisons between the same sector companies and the overall market. The EPS & PE ratios are based on 2023 and 2024 actual or projected earnings, excluding major one off items.

Investors need pertinent information to navigate numerous investment options successfully in the stock market. The  ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

The net asset value of each company is reported as a guide to quickly assess the value of stocks based on this measure. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

Dividends paid or payable and yields for each company are shown in the Main and Junior Markets’ daily report charts, along with the closing volume pertaining to the highest bid and the lowest offer for each company.

Mostly price gains for ICTOP10

The Main Market of the JSE rose around two percent and Junior Market just under one percent for the week and led the top 10 mostly higher, with 7 Main Market and 4 Junior Market stocks rising with declining stocks recording losses of 4 percent or less, at the same time one stock moved out of the TOP10.

The Main Market ICTOP10 ended with, General Accident declined 11 percent to $4.50. Buying interest picked up during the week for Scotia Group pushing the stock to several 52 weeks’ highs and a rose of 7 percent for the week to a 52 weeks’ closing high of $38.40. This stock has much more juice left that should take it into the $40 range by early 2024. Caribbean Producers rallied 6 percent to $9, while Margaritaville also rose 6 percent and closed at $17 and Pulse Investments rose 5 percent to $2.09 and Key Insurance slipped 4 percent to $2.40.

The Main Market ICTOP10 ended with, General Accident declined 11 percent to $4.50. Buying interest picked up during the week for Scotia Group pushing the stock to several 52 weeks’ highs and a rose of 7 percent for the week to a 52 weeks’ closing high of $38.40. This stock has much more juice left that should take it into the $40 range by early 2024. Caribbean Producers rallied 6 percent to $9, while Margaritaville also rose 6 percent and closed at $17 and Pulse Investments rose 5 percent to $2.09 and Key Insurance slipped 4 percent to $2.40.

The Junior Market ended the week, with AMG Packaging climbing 17 percent to $2.70, buying is not aggressive currently while supplies up to $3.15 is limited, with none on offer until $10. Investors should expect a big bounce in the first quarter profits due by mid-January. The company states that they are exploring the possibility of new equipment and expanded facilities that could shape a future expansion of momentous proportions. Caribbean Cream rose 10 percent to $3.64 and Stationery and Office Supplies gained 9 percent and dropped out of the TOP10 and is replaced by Tropical Battery. There were no notable declines at the end of the week.

There was no new addition to the IC Main Market TOP10.

Indications of where stock prices could be by May 2024 can be seen from stocks with the highest values in the Main and Junior Markets.

The average PE for the JSE Main Market ICTOP 10 stands at 5.3, well below the market average of 13.1. The Main Market ICTOP10 is projected to gain an average of 288 percent by May 2024, based on 2023 forecasted earnings and now provides better values than the Junior Market with the potential to gain 195 percent over the same time frame.

The average PE for the JSE Main Market ICTOP 10 stands at 5.3, well below the market average of 13.1. The Main Market ICTOP10 is projected to gain an average of 288 percent by May 2024, based on 2023 forecasted earnings and now provides better values than the Junior Market with the potential to gain 195 percent over the same time frame.

In the Main Market ICTOP10, 15 of the most highly valued stocks, 31 percent of the Main Market are priced at a PE of 15 to 108, with an average of 29 and 18 excluding the highest PE ratios, and a PE of 24 for the top half and 16 excluding the stocks with overweight values.

The PE of the Junior Market TOP10 sits at 7, just over half of the market, with an average of 13.2. There are 14 stocks, or 29 percent of the market, with PEsfrom 15 to 49, averaging 21, well above the market’s average. The top half of the market has an average PE of 18, possibly the lowest fair value for stocks.

Of great import is that the averages of both markets are now converging around a PE of 20 for close to a third of the market, as the year is coming to a close and with more information available on the full year’s earnings.

ICTOP10 focuses on likely yearly winners, accordingly, the list includes some of the best companies in the market, but this is not always so. ICInsider.com ranks stocks based on projected earnings, allowing investors to focus on the most undervalued stocks and helping to remove emotions in selecting stocks for investments that often result in costly mistakes.

ICTOP10 focuses on likely yearly winners, accordingly, the list includes some of the best companies in the market, but this is not always so. ICInsider.com ranks stocks based on projected earnings, allowing investors to focus on the most undervalued stocks and helping to remove emotions in selecting stocks for investments that often result in costly mistakes.

IC TOP10 stocks will likely deliver the best returns on or around May 2024 and are ranked in order of potential gains, computed using projected earnings for the current fiscal year. Expected values will change as stock prices fluctuate and result in weekly movements in and out of the lists. Revisions to earnings are ongoing, based on receipt of new information.

Persons who compiled this report may have an interest in securities commented on in this report.

Profit climbs 22% at Stationery & Office Supplies

Profit climbed in 2023 at Stationery and Office Supplies an under the radar company until listing on the Jamaica Stock Exchange transformed it into one of the leading companies peddling office supplies in Jamaica. For the quarter ending September this year, profit after tax climbed 22 percent to $96 million from $79 million last year and for the nine months $294 million up 14 percent from $252.5 million.

Stationary & Office Supplies – Montego Bay office.

The year-to-date figures include a gain on the sale of assets amounting to $7.1 million and $30 million in 2022 as such this year’s ongoing profit performance is greater than the net figures suggest.

Year to date, the operating profit before finance charges and gains or loss on the sale of fixed assets is up a solid 38 percent for the nine months and 12 percent for the quarter.

For the September quarter, revenues inched up from $473 million to $488 million. A fair bit of the slowdown is due to price discounts granted based on originally listed prices following falling input costs. For the year to date, revenues climbed 16 percent to $1.53 billion from $1.32 billion in 2022.

Administrative and general expenses rose 23.5 percent to $138 million from $112 million in the September quarter of 2022 and for the year to date, it climbed 20 percent to $378 million from $314 million. Selling and promotional costs fell to $29 million for the September 2023 quarter from $35.8 million last year, with the year to date figures being almost flat at $97 million in 2023 versus $96 million in 2022. Depreciation charges were slightly down from $8.7 million in the September quarter of last year to $8.4 million this year and year to date the numbers are flat at $26.4 million.

Earnings per share for the third Quarter was 4 cents compared to 3 cents in 2022 and for the nine months end September this year, 13 cents per share, up from 11.33 cents.

ICInsider.com projects 19 cents per share for the year, from revenues of just over $2 billion and 30 cents for 2024. The stock last traded at $1.72, with a PE of 8.9 times current year’s earnings, well below the market average of 12.

Operations produced cash inflows of $356 million, up from $259 million in 2022 and at the end of the period with a surplus of $189 million that brought the total to $320.8 million up from just $99 million at the end of September. The 2023 growth in Cash inflows is after spending $72 million on acquiring property, plant and equipment, $50 million in dividend payments and $40 million used in repaying loans. Some of the amount on hand is earmarked to fund the acquisition of properties to be used for storage to allow for continued expansion of the business.

Operations produced cash inflows of $356 million, up from $259 million in 2022 and at the end of the period with a surplus of $189 million that brought the total to $320.8 million up from just $99 million at the end of September. The 2023 growth in Cash inflows is after spending $72 million on acquiring property, plant and equipment, $50 million in dividend payments and $40 million used in repaying loans. Some of the amount on hand is earmarked to fund the acquisition of properties to be used for storage to allow for continued expansion of the business.

Current assets closed the period at $1 billion, with Receivables rising from $194 million to $317 million and inventories at $349 million compared with $356 million in 2022. Current liabilities rose to $305 million from $148 million in 2022.

Shareholders’ equity stands at $1.35 billion which is up from $884 million from a year ago and borrowed funds used in its operations is only $65 million.

Going forward, the Seek manufacturing division is to get new machines to help meet growing demand as the current facility is said to be at its peak. The distribution of 3M stationery products has been added to the company’s line in the latter months of 2023 and will boost revenues in 2024, with a full year of sales.

Junior Market stocks dominate half year

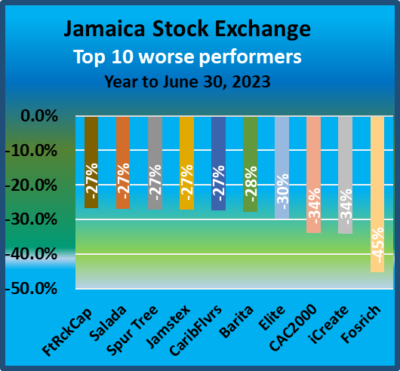

At the midway point in the year, the Jamaica Stock Exchange Main Market is down 7 percent, with the Financial Index down a much larger 15 percent, but the Junior Market is flat, as the JSE delivered 35 price gains for the ordinary shares and 59 losses as Junior Market stocks dominated the top positions for the first half of 2023.

Expectations are that the Junior Market will continue its upward movement in the second half of the year with technical indicators pointing to a big upward push in the market. The market gained 75 percent the last time these indicators flashed a buy signal.

Expectations are that the Junior Market will continue its upward movement in the second half of the year with technical indicators pointing to a big upward push in the market. The market gained 75 percent the last time these indicators flashed a buy signal.

The Main Market remains under some selling pressure and is not signalling a sustained rally in the short term. But June is never the month of recovery for that market following sell in May and go away. July is the month that is historically the period in the past the Main Market usually starts to rally and sometimes as late as August fueled by mid year results that will mostly be in by the middle of August.

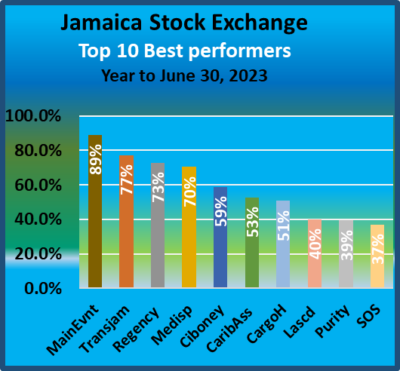

There are only two Main Market stocks in the TOP10 with Transjamaican heads Stocks to Watch coming on top for that market with a 77 percent gain, year to date, with it being the second highest performer for the overall market for the year so far. Ciboney is up 59 percent and the fifth highest performer, and the second best Main market stock, thanks partially to a change in the majority ownership to IEC Energy Company Ltd, with the new directors being Nigel Davy, Jennifer Davy, Klyle Davy, Wycliffe Cameron Conley Salmon Donald Patterson and Wayne Wray.

The top performing stock is Main Event with a rise of 89 percent, with more gains expected with the PE ratio of just 10 times this year’s earnings, while Stationery and Office Supplies doubled after an announcement to consider a stock split at a directors meeting on June 21 ended with a gain of 37 percent for the half year as the price pulled back after the directors announced a recommendation for a 9 for 1 split to be voted on at the company’s AGM on July 25.

The top performing stock is Main Event with a rise of 89 percent, with more gains expected with the PE ratio of just 10 times this year’s earnings, while Stationery and Office Supplies doubled after an announcement to consider a stock split at a directors meeting on June 21 ended with a gain of 37 percent for the half year as the price pulled back after the directors announced a recommendation for a 9 for 1 split to be voted on at the company’s AGM on July 25.

The Junior Market has the majority of stocks, six, in the worst performer grouping, with Fosrich being the worst with a loss of 45 percent as the price corrected sharply from an overbought position last year, followed by iCreate down 34 percent from excessive speculation from a number of announcements the company made last year.

SOS to split stocks into 9 units

Shareholders of Stationery and Office Supplies seem set to enjoy the benefit of splitting existing stock into nine ordinary shares for each they own to take effect and will result in the total number of shares jumping from 250.12 million units to 2.251 billion effective on July 25.

To accommodate the split, shareholders will be asked to vote on a resolution to be tabled at the company’s annual General meeting of July 25 to effect the split and will also be asked to vote to increase the number of shares to 500 billion units, with effect from July 25.

To accommodate the split, shareholders will be asked to vote on a resolution to be tabled at the company’s annual General meeting of July 25 to effect the split and will also be asked to vote to increase the number of shares to 500 billion units, with effect from July 25.

The shares of SOS that hit a record high of $34.98 on Wednesday closed at $33.89 on Thursday on the Junior Market of the Jamaica Stock Exchange.

169% surge in profit at SOS

Stationery and Office Supplies (SOS) enjoyed a blow year in 2022, with earnings hitting a record high, after profits jumped 169 percent before tax to $284 million and $257 million after tax from a 55 percent jump in revenues to $1.75 billion from $1.12 billion in 2021. SOS benefitted from one time income from a Gain on disposal of property, plant and equipment of $30 which was partially offset by unusually large impairment losses of $11.5 million.

Income tax on the year’s profit amounts to $27 million compared with a tax credit of $1 million in 2021. Net profit in 2021 was $107 million but gross profit jumped 59 percent from $574 million in 2021 to $912 million for 2022, as gross profit margin slipped during the year to 47.8 percent from 49 percent in 2021.

Income tax on the year’s profit amounts to $27 million compared with a tax credit of $1 million in 2021. Net profit in 2021 was $107 million but gross profit jumped 59 percent from $574 million in 2021 to $912 million for 2022, as gross profit margin slipped during the year to 47.8 percent from 49 percent in 2021.

Administrative and general expenses rose 25 percent to $399 million from $320 million in 2021. Selling and promotional costs rose 64 percent to $132 million from $80 million in the prior year, Impairment loss on financial assets jumped 698 percent to $11.5 million up from $1.4 million and Depreciation and amortisation costs rose 13.7 percent to $30 million up from $26.4 million. There were cost savings during the year with Loss on foreign exchange falling 85 percent to $1.2 million from $8 million in 2021 and Finance costs dropping 22 percent to $8.7 million from $11 million in 2021 as loans were partially repaid.

Allan McDaniels CEO of SOS

Gross cash flow during the year brought in $336 million, which was used to fund increased working capital needs of $84 million, capital expenditure amounting to $50 million, loan repayment of $49 million and dividend payment of $45 million, leaving $97 million to add to cash funds.

At the end of the year, shareholders’ equity grew to $1.1 billion with long term borrowings at $67 million and short term at $43 million. Current assets ended the period at $737 million inclusive of trade and other receivables of $200 million versus $124 million in the prior year. Cash and bank balances rose to $132 million from $34 million in the previous year and inventories climbed to $369 million up from $296 million in 2021. Current liabilities ended at $181 million and resulted in Net current assets of $556 million.

Earnings per share came out at $1.03 cents for the year up from 43 cents in 2021. IC Insider.com forecasts $2 per share for the current fiscal year, with a PE of 7.3 times the current year’s earnings down from 14.5 based on 2021 results, compared with 11.3 for the market based 2023 earnings at $14.50 the stock traded at on Friday on the Jamaica Stock Exchange Junior Market.

Stationary & Office Supplies – Montego Bay office.

Of note is a 37 percent increase in fourth quarter revenues, which was at a slower pace than the 63 percent increase for the nine months to September and a 45 percent rise in the 4th quarter of 2021, suggesting that the pace for 2023 should be strong, but most likely slower than that of 2022. The pace in 2023 will be helped by a deal struck with a company in Trinidad to cross sell products as well as the possibility that other deals may be struck with others.

SEEK division produced receipts and other ruled books as well as graph paper for the first time in June last year, using machinery that was purchased from the former operators, they will enjoy increased production for the entire year in 2023 compared with approximately six months in 2022 and contributed $43 million to gross profit for 2022.

With improving profits and shrinking supplies outside of the TOP 10 shareholders, who control 91 percent of the issued shares, the stock is setting up for a stock split that cannot be far off and when given will catapult the stock price upwards.

Going forward, with the Jamaican economy recovering and now growing, the stage is being set for SOS to continue to grow at an attractive pace for a while and deliver above average returns for investors in cash dividends and stock price gains.

13 Junior Market stocks to watch in 2023

To make the 2023 ICTOP15, projected gains have to exceed 280 percent over the next 18 months at a projected PE of 22.5 times earnings. That level of growth is what the lowest on the list, Access Financial is projected to deliver over the period.

To make the 2023 ICTOP15, projected gains have to exceed 280 percent over the next 18 months at a projected PE of 22.5 times earnings. That level of growth is what the lowest on the list, Access Financial is projected to deliver over the period.

So great are the prospects of the Junior Market that IC Insider.com thought it important to highlight these additional companies for investors to see the great potential to make money over the next 18 months. This publication has never before put out such a list to start the year, in addition to the ICTOP15.

While the IC TOP15 2023 listings reflect 15 companies that show the greatest potential to be the top performers up to May 2024, a number of companies have the potential to do exceedingly well over the period but are likely to underperform those in the ICTOP15, even then, the future is not assured and some in the watch list could outperform projections and end in the top performers for the period.

The watch list shows that investors do not have to hit home runs to make decent gains in the stock market, but observation in the local market suggests that many persons may not have the patience to build gains over time.

These may or may not be the best companies in the market based on management, products or services and financial health, but they are undervalued and could deliver above average gains as well as pay attractive dividends in the 2023 to 2024 period.

These may or may not be the best companies in the market based on management, products or services and financial health, but they are undervalued and could deliver above average gains as well as pay attractive dividends in the 2023 to 2024 period.

The market has demonstrated that the ability to increase profits is the most important factor that will drive stock prices and is the primary area for investors to focus on going forward.

CAC2000 Projection EPS $1.

The company has the potential to do exceedingly well, especially with an upsurge in the construction of homes and hotels. But it is not without risk and disappointment from quarter to quarter as projects take time to complete, resulting in jerkiness in earnings. This is definitely a stock to consider from a longer time horizon and not one that can be relied on to deliver instant gains, but it could surprise.

Cargo Handlers

This company is not one that will be on every investor’s list for 2023, don’t let that dissuade you from taking a closer look. One of the smaller Junior Market companies and is highly profitable and holds over $500 million in cash funds and with add to it yearly. The company serves one of the fastest growing regions of Jamaica with the continued expansion of the tourist sector that fuels above average economic activities and the BPO sector that lead to increased imports through the Montego Bay port where its operation is centred. Last year’s earnings per share were 77 cents and ICInsider.com is forecasting $1.10 for the current year, that should be enough to push the price towards $20 or more.

An important factor to consider is the cash that they hold which is available for investment in other entities that could add to improved profits going forward. By the way, don’t ignore the dividends they pay.

Dollar Financial came to the Junior Market in June last year and is now accredited by Bank of Jamaica to operate as a micro financial institution. For the nine months to September 2022, profit before tax amounted to $201 million, 257 percent higher than in 2021. Profit before tax for the quarter ending September 2022 increased a solid 214 percent to $70 million, an indication of what could be coming down the road.

Dollar Financial came to the Junior Market in June last year and is now accredited by Bank of Jamaica to operate as a micro financial institution. For the nine months to September 2022, profit before tax amounted to $201 million, 257 percent higher than in 2021. Profit before tax for the quarter ending September 2022 increased a solid 214 percent to $70 million, an indication of what could be coming down the road.

The increase in profits was fueled by loans receivable of $1.2 billion to September 2022, an increase of $650 million or 125 percent over the September 2021 position. Up to September, secured loans represented 72 percent of total loans and unsecured 28 percent.

The company recently raised $1.17 billion in debt financing and expanded the resources available for lending. These funds plus additional cash from profit to be generated provide more than adequate fuel for strong loan expansion that will result in continued above average profit growth. The company plans to use some of the funds raised to expand to the Bahamas and the Eastern Caribbean and capitalize Ultra Financier Limited, their asset based lender. The company could turn out to be exceptionally profitable if the resources are managed well to prevent heavy loan loss provisioning that could eat away at profits. ICInsider.com projects earnings of 35 cents per share for 2023 and that should be good enough to send the stock flying with gains of more than 200 percent.

Express Catering EPS is projected at 65 cents for 2023/4

The company started to benefit from the rebound in tourism but importantly the first half of the 2022 calendar year saw a decline in visitor arrivals compare to 2019, with the numbers for 2023 set to show a major increase over 2022first quarter numbers. The first quarter should be up over 50 plus percent compared with that of 2022. That will have a major impact on the revenues, with its entire operation within the Sangster International Airport. It is worth noting also that the company will have additional restaurants within the airport during the new fiscal year and this is going to add to revenues and profitability for the company.

With the stock price hovering around $5 per share this stock is selling slightly less than eight times earnings and shows the potential to do even better than the revenues and the earnings per share projections. With many Junior Market companies selling at PE ratios around 20 one should expect the stock to deliver a 200 percent rise in value over the next 18 months or so.

Fontana stock could gain 150 percent for the period. looking back, for the first quarter to September, revenues rose a healthy 26 percent and profit jumped 43 percent to $87 million. The projection is for revenues to continue to grow around the 26 percent level into 2023, with profit to rise to 80 cents per share for the year and $1.50 in the 2024 fiscal year ending June. With the stock priced around $9 it is nicely positioned for a bounce to provide an excellent return over the next year and a half.

Fontana stock could gain 150 percent for the period. looking back, for the first quarter to September, revenues rose a healthy 26 percent and profit jumped 43 percent to $87 million. The projection is for revenues to continue to grow around the 26 percent level into 2023, with profit to rise to 80 cents per share for the year and $1.50 in the 2024 fiscal year ending June. With the stock priced around $9 it is nicely positioned for a bounce to provide an excellent return over the next year and a half.

The company is adding a new store in Portmore that should come into operation during the first half of 2023 and add revenues and profits to the business, but this may not be significant until the 2024 fiscal year. Expected growth in the local economy and a big bounce in tourism traffic will have a positive impact on stores in the western end of the country and deliver increased revenues and increased profit as a result. For the year to June 2022, profit was up 12 percent to $415 million from a 21 percent rise in revenues to $4.7 billion.

Image Plus Consultants – EPS 30 cents 2023 and $0.35 for 2023-4

The Image Plus stock failed to sparkle on listing in January, rising just 10 percent by the close of its first day on the market in heavy trading of nearly 12.4 million shares, the second heaviest traded Junior Market stock on opening, following an IPO. The price has now fallen below the issue price providing a good entry point for investors but has since bounced just above $2 with the release of nine months’ results to November. (See articles on analyzing the IPO and the nine months’ results.)

Jamaican Teas – earnings could hit 30 cents per share for the current fiscal year. Some input costs have declined following shipping facilities normalizing, resulting in lower shipping costs as well a reduction in some raw material prices worldwide. The forecast includes a sizable contribution from QWI Investments and a contribution from the real estate development that should see sales of its current development being concluded in the current fiscal year.

The group is expanding the product range for the local and export markets which will add to revenues and profits going forward.

The stock has seen increased buying from individual and institutional investors which is an excellent sign as it lends solid support for trading.

Knutsford Express

Knutsford Express – projected EPS of $1 and $1.40 for 2024.

The company suffered, in a meaningful way, from lower revenues when business activities were severely curtailed with the advent of the Covid-19 pandemic in Jamaica which resulted in major disruption in the economy. In the latest fiscal year to May, revenues were back to pre-pandemic levels in dollar terms but profits lagged as increased costs grew faster than revenues, resulting in the 2022 full year results being 38 percent of 2019 but more than twice 2020.

For the August quarter, revenues rose 78 percent to $415 million and profit jumped from $9 million to $84 million. For the half year to November, revenues rose to $813 million from $473 million in 2021 with profit surging from $13 million after tax to $143 million. Third quarter profit rose from just $2 post-tax to $59 million. The Drax Hall Business Centre is contributing fully to profit with all available space occupied with several tenants already open for business and the company looking to generate income in the order of $100 million a year from the complex.

The company is benefiting from the upsurge in visitor arrivals both directly and indirectly from persons working in the industry.

Main Event returns to IC TOP 10.

Main Event – EPS is projected at $1.10 for 2023

There is the potential for the stock price to gain 180 percent over the next 18 months. Profits for the nine months last year jumped 147 percent to $243 million over 2021 as revenues rose from $501 million to just over $1 billion dollars representing 85 percent increase over the previous year. Revenues for the September quarter rose 147 percent to $602 million with profits for the quarter jumping a solid 332 percent to $104 million as profits rose by $95 million over the previous year, suggesting that the results of 2022 will be outstanding and that could carry over well into 2023.

What is worth noting is that revenues for the first quarter were just $203 million and for the April quarter $290 million, well below third quarter numbers. By contrast, revenues were $458 million in the first quarter of 2019 and $438 million in the second quarter, well ahead of those for the 2022 periods, this has a lot of significance for revenue growth in the first half of the 2023 year. The data show that there should be a significant pick up in revenues and profitability in the corresponding 2023 period and a major uptick in revenues for the year and profits. There is a bit of seasonality in earnings and this could have implications in 2023. The final results for 2022 will provide good guidance on this.

The lesson to be drawn from the numbers for the first three quarters of the year is that profit for 2023 will be up substantially up on the ultimate results for 2022. There is a level of uncertainty along with various developments in the local economy that makes it challenging to project with certainty the level of business that Main Event will undertake, this is the major reason why the stock is placed on the watch list. The final numbers could impact the stock price significantly.

Of note, the third quarter revenues are the highest record in the company’s history in the quarter. The company indicates that the increased business was due to added activity in its core business. The entertainment industry has seen a strong return to outdoor events and lifestyle experiences after a two year break.

Medical Disposables EPS is projected at 40 cents for fiscal 2023 and 70 cents for 2024

This company is not one to take at face value as they quietly build the infrastructure on which to deliver increased business going forward. The company is focusing on laying the foundation for growth in consumer products as increased business opportunities in the medical area slow. The dental area that is operated by the newly formed subsidiary has room for expansion outside of the western region and should be able to ride on the parent company’s infrastructure that currently exists in the next year or two.

The company in the meantime has increased expenditure to attract and keep talent within its employ to grow business, this development resulted in increased costs in the current fiscal year and negatively affected growth in profits for the fiscal year to date.

There is the possibility that more shares could be available in the market over the next year or so.

One on One Educational EPS is projected at 20 cents

The stock raced out the blocks on the fifth day of listing in the latter part of last year to hit $2.50 but the price has fallen to a low of $1.10 in December, with investors concerned that they may have lost a major client and the negative impact that may have on profit. The prospectus stated that in August 2021, 63 percent of the Company’s revenue came through Business to Business contracts and 37 percent through the Company’s end user consumers’ business line. Neither the 2022 audited accounts nor the first quarter results show any fall out of business, in fact, revenues almost doubled in the quarter with profit rising to $12 million before tax from a loss of $1.8 million in 2021. The price could be considered appropriate based on results released so far but as more results become available, the current price may appear to be a gift.

Funds raised in the public issue in 2022 net of loan repayment were earmarked for the development of technological infrastructure for expansion. Regardless, the major reasons to invest in this company is not its short-term fortunes or misfortunes but the major potential its operations have to deliver above average growth within Jamaica and overseas.

Spur Tree Spices EPS is projected at 40 cents.

Spur Tree Spices EPS is projected at 40 cents.

The company recorded a 9.4 percent growth in revenues to $672M for the nine-months ended September 2022, from $614 million in 2021. Gross Margin increased from 31 percent in 2021 to 35.4 percent in 2022.

For the September quarter revenues slipped to $233 million from $247 but improved profit margin resulted in a gross profit of $75 million versus $73 million in the prior year. Profit before Taxation fell to $30 million in the quarter from $33 million in 2021, but climbed 30 percent to $119 million for the year to September compared with $91 million in 2021 and was just shy of the $124 million for the full year in 2021.

The company implemented investment projects to expand the Exotic Products factory infrastructure to double production capacity, purchase of building in Port Morant to establish a production facility and upgraded the Spur Tree Spices production capacity.

They also advanced $100 million to purchase a controlling interest in Canco, an ackee canning company, and if combined with Exotic Products could result in a major jump in production and improved efficiency. They also appointed Massy Distributions agents for regional distribution.

This company has a lot of promise but the valuation placed on the stock ran ahead of results as such improved results in 2023 are unlikely to be reflected fully in the stock price and provide above average growth for the stock but it could be good enough to deliver a reasonable gain that investors would be normally pleased with even if it does not put it in the top ranking of stocks. Additionally, it has growth potential going beyond 2023 that could help deliver above average long term growth.

Stationery & Office Supplies recording record 2022 profits.

Stationary and Office Supplies should deliver gains of 250 percent for the period. The company has done exceptionally well in 2022 and is one of the top performing stocks for that year, gaining 140 percent as a result of very strong profit performance during the year that came from an incredible 60 percent increase in revenues that should end close to $1.8 billion for the year and $2.3 billion for 2023. The company generated a profit of $250 million for the nine months to September that should reach $360 million for the full year and just over $550 million in 2023.

ICInsider.com does not expect the performance to be at the same level in 2023 but sees continued attractive growth in earnings that should put it at about $2.20 per share, up from around $1.35 per share in 2022.

The business continues to increase from local and overseas demand. Information is that a deal was struck with a Trinidad company to sell their furniture in that market in addition the possibility exists that they could be getting into other Caribbean countries to add to the organic growth of the business. There is the possibility for acquisitions of small businesses during the year that could benefit from synergies within the company and deliver above average returns from such investments. Investors should not ignore the possibility of a stock split that could provide additional spice to make the performance of the stock an attractive one.

Finally, the company is well managed and financially healthy with limited debt and increasing shareholders’ equity.