Companies with earnings that are consistently growing are usually the best dividend paying stocks to invest in if income is a prime objective. They will have more room to make increased dividend payments in the future.

Investors looking for the best dividend paying stocks on the Jamaica Stock Exchange should take the above factors into consideration. It is also a good factor to consider when buying stocks that are likely to increase in value over time.

Investors looking for the best dividend paying stocks on the Jamaica Stock Exchange should take the above factors into consideration. It is also a good factor to consider when buying stocks that are likely to increase in value over time.

On the Jamaica Stock Exchange, the Main Market, Carreras is the king of dividend payment with a yield of 11 percent based on the latest stock price of $8 in 2023, followed by Transjamaican Highway and at 7 percent, Scotia Group at 5 percent based on the last dividend paid of 40 cents and annualised, at a then stock price of $34. What is interesting about Scotia is the traditional metric is for the company to pay between 40 to 50 percent of profits.

Scotia historically pays just above 40 percent of profit, but that seems to have been interrupted as a result of the negative impact that flowed from the Covid 9 economic dislocation.  The company reported earnings of $5.54 and that would suggest an annual dividend of $2.20 which would translate to a dividend yield of 6.7 percent with 2024 likely to be higher.

The company reported earnings of $5.54 and that would suggest an annual dividend of $2.20 which would translate to a dividend yield of 6.7 percent with 2024 likely to be higher.

The Junior Market has two stocks with attractive yields Dolphin Cove and MailPac at 7 percent each. The payout for MailPac represent a full years’ profit.

Yields may have dipped in some cases but that does not change the longer term prospects.

Top 5 JSE dividend paying stocks now

13 Junior Market stocks to watch in 2023

To make the 2023 ICTOP15, projected gains have to exceed 280 percent over the next 18 months at a projected PE of 22.5 times earnings. That level of growth is what the lowest on the list, Access Financial is projected to deliver over the period.

To make the 2023 ICTOP15, projected gains have to exceed 280 percent over the next 18 months at a projected PE of 22.5 times earnings. That level of growth is what the lowest on the list, Access Financial is projected to deliver over the period.

So great are the prospects of the Junior Market that IC Insider.com thought it important to highlight these additional companies for investors to see the great potential to make money over the next 18 months. This publication has never before put out such a list to start the year, in addition to the ICTOP15.

While the IC TOP15 2023 listings reflect 15 companies that show the greatest potential to be the top performers up to May 2024, a number of companies have the potential to do exceedingly well over the period but are likely to underperform those in the ICTOP15, even then, the future is not assured and some in the watch list could outperform projections and end in the top performers for the period.

The watch list shows that investors do not have to hit home runs to make decent gains in the stock market, but observation in the local market suggests that many persons may not have the patience to build gains over time.

These may or may not be the best companies in the market based on management, products or services and financial health, but they are undervalued and could deliver above average gains as well as pay attractive dividends in the 2023 to 2024 period.

These may or may not be the best companies in the market based on management, products or services and financial health, but they are undervalued and could deliver above average gains as well as pay attractive dividends in the 2023 to 2024 period.

The market has demonstrated that the ability to increase profits is the most important factor that will drive stock prices and is the primary area for investors to focus on going forward.

CAC2000 Projection EPS $1.

The company has the potential to do exceedingly well, especially with an upsurge in the construction of homes and hotels. But it is not without risk and disappointment from quarter to quarter as projects take time to complete, resulting in jerkiness in earnings. This is definitely a stock to consider from a longer time horizon and not one that can be relied on to deliver instant gains, but it could surprise.

Cargo Handlers

This company is not one that will be on every investor’s list for 2023, don’t let that dissuade you from taking a closer look. One of the smaller Junior Market companies and is highly profitable and holds over $500 million in cash funds and with add to it yearly. The company serves one of the fastest growing regions of Jamaica with the continued expansion of the tourist sector that fuels above average economic activities and the BPO sector that lead to increased imports through the Montego Bay port where its operation is centred. Last year’s earnings per share were 77 cents and ICInsider.com is forecasting $1.10 for the current year, that should be enough to push the price towards $20 or more.

An important factor to consider is the cash that they hold which is available for investment in other entities that could add to improved profits going forward. By the way, don’t ignore the dividends they pay.

Dollar Financial came to the Junior Market in June last year and is now accredited by Bank of Jamaica to operate as a micro financial institution. For the nine months to September 2022, profit before tax amounted to $201 million, 257 percent higher than in 2021. Profit before tax for the quarter ending September 2022 increased a solid 214 percent to $70 million, an indication of what could be coming down the road.

Dollar Financial came to the Junior Market in June last year and is now accredited by Bank of Jamaica to operate as a micro financial institution. For the nine months to September 2022, profit before tax amounted to $201 million, 257 percent higher than in 2021. Profit before tax for the quarter ending September 2022 increased a solid 214 percent to $70 million, an indication of what could be coming down the road.

The increase in profits was fueled by loans receivable of $1.2 billion to September 2022, an increase of $650 million or 125 percent over the September 2021 position. Up to September, secured loans represented 72 percent of total loans and unsecured 28 percent.

The company recently raised $1.17 billion in debt financing and expanded the resources available for lending. These funds plus additional cash from profit to be generated provide more than adequate fuel for strong loan expansion that will result in continued above average profit growth. The company plans to use some of the funds raised to expand to the Bahamas and the Eastern Caribbean and capitalize Ultra Financier Limited, their asset based lender. The company could turn out to be exceptionally profitable if the resources are managed well to prevent heavy loan loss provisioning that could eat away at profits. ICInsider.com projects earnings of 35 cents per share for 2023 and that should be good enough to send the stock flying with gains of more than 200 percent.

Express Catering EPS is projected at 65 cents for 2023/4

The company started to benefit from the rebound in tourism but importantly the first half of the 2022 calendar year saw a decline in visitor arrivals compare to 2019, with the numbers for 2023 set to show a major increase over 2022first quarter numbers. The first quarter should be up over 50 plus percent compared with that of 2022. That will have a major impact on the revenues, with its entire operation within the Sangster International Airport. It is worth noting also that the company will have additional restaurants within the airport during the new fiscal year and this is going to add to revenues and profitability for the company.

With the stock price hovering around $5 per share this stock is selling slightly less than eight times earnings and shows the potential to do even better than the revenues and the earnings per share projections. With many Junior Market companies selling at PE ratios around 20 one should expect the stock to deliver a 200 percent rise in value over the next 18 months or so.

Fontana stock could gain 150 percent for the period. looking back, for the first quarter to September, revenues rose a healthy 26 percent and profit jumped 43 percent to $87 million. The projection is for revenues to continue to grow around the 26 percent level into 2023, with profit to rise to 80 cents per share for the year and $1.50 in the 2024 fiscal year ending June. With the stock priced around $9 it is nicely positioned for a bounce to provide an excellent return over the next year and a half.

Fontana stock could gain 150 percent for the period. looking back, for the first quarter to September, revenues rose a healthy 26 percent and profit jumped 43 percent to $87 million. The projection is for revenues to continue to grow around the 26 percent level into 2023, with profit to rise to 80 cents per share for the year and $1.50 in the 2024 fiscal year ending June. With the stock priced around $9 it is nicely positioned for a bounce to provide an excellent return over the next year and a half.

The company is adding a new store in Portmore that should come into operation during the first half of 2023 and add revenues and profits to the business, but this may not be significant until the 2024 fiscal year. Expected growth in the local economy and a big bounce in tourism traffic will have a positive impact on stores in the western end of the country and deliver increased revenues and increased profit as a result. For the year to June 2022, profit was up 12 percent to $415 million from a 21 percent rise in revenues to $4.7 billion.

Image Plus Consultants – EPS 30 cents 2023 and $0.35 for 2023-4

The Image Plus stock failed to sparkle on listing in January, rising just 10 percent by the close of its first day on the market in heavy trading of nearly 12.4 million shares, the second heaviest traded Junior Market stock on opening, following an IPO. The price has now fallen below the issue price providing a good entry point for investors but has since bounced just above $2 with the release of nine months’ results to November. (See articles on analyzing the IPO and the nine months’ results.)

Jamaican Teas – earnings could hit 30 cents per share for the current fiscal year. Some input costs have declined following shipping facilities normalizing, resulting in lower shipping costs as well a reduction in some raw material prices worldwide. The forecast includes a sizable contribution from QWI Investments and a contribution from the real estate development that should see sales of its current development being concluded in the current fiscal year.

The group is expanding the product range for the local and export markets which will add to revenues and profits going forward.

The stock has seen increased buying from individual and institutional investors which is an excellent sign as it lends solid support for trading.

Knutsford Express

Knutsford Express – projected EPS of $1 and $1.40 for 2024.

The company suffered, in a meaningful way, from lower revenues when business activities were severely curtailed with the advent of the Covid-19 pandemic in Jamaica which resulted in major disruption in the economy. In the latest fiscal year to May, revenues were back to pre-pandemic levels in dollar terms but profits lagged as increased costs grew faster than revenues, resulting in the 2022 full year results being 38 percent of 2019 but more than twice 2020.

For the August quarter, revenues rose 78 percent to $415 million and profit jumped from $9 million to $84 million. For the half year to November, revenues rose to $813 million from $473 million in 2021 with profit surging from $13 million after tax to $143 million. Third quarter profit rose from just $2 post-tax to $59 million. The Drax Hall Business Centre is contributing fully to profit with all available space occupied with several tenants already open for business and the company looking to generate income in the order of $100 million a year from the complex.

The company is benefiting from the upsurge in visitor arrivals both directly and indirectly from persons working in the industry.

Main Event returns to IC TOP 10.

Main Event – EPS is projected at $1.10 for 2023

There is the potential for the stock price to gain 180 percent over the next 18 months. Profits for the nine months last year jumped 147 percent to $243 million over 2021 as revenues rose from $501 million to just over $1 billion dollars representing 85 percent increase over the previous year. Revenues for the September quarter rose 147 percent to $602 million with profits for the quarter jumping a solid 332 percent to $104 million as profits rose by $95 million over the previous year, suggesting that the results of 2022 will be outstanding and that could carry over well into 2023.

What is worth noting is that revenues for the first quarter were just $203 million and for the April quarter $290 million, well below third quarter numbers. By contrast, revenues were $458 million in the first quarter of 2019 and $438 million in the second quarter, well ahead of those for the 2022 periods, this has a lot of significance for revenue growth in the first half of the 2023 year. The data show that there should be a significant pick up in revenues and profitability in the corresponding 2023 period and a major uptick in revenues for the year and profits. There is a bit of seasonality in earnings and this could have implications in 2023. The final results for 2022 will provide good guidance on this.

The lesson to be drawn from the numbers for the first three quarters of the year is that profit for 2023 will be up substantially up on the ultimate results for 2022. There is a level of uncertainty along with various developments in the local economy that makes it challenging to project with certainty the level of business that Main Event will undertake, this is the major reason why the stock is placed on the watch list. The final numbers could impact the stock price significantly.

Of note, the third quarter revenues are the highest record in the company’s history in the quarter. The company indicates that the increased business was due to added activity in its core business. The entertainment industry has seen a strong return to outdoor events and lifestyle experiences after a two year break.

Medical Disposables EPS is projected at 40 cents for fiscal 2023 and 70 cents for 2024

This company is not one to take at face value as they quietly build the infrastructure on which to deliver increased business going forward. The company is focusing on laying the foundation for growth in consumer products as increased business opportunities in the medical area slow. The dental area that is operated by the newly formed subsidiary has room for expansion outside of the western region and should be able to ride on the parent company’s infrastructure that currently exists in the next year or two.

The company in the meantime has increased expenditure to attract and keep talent within its employ to grow business, this development resulted in increased costs in the current fiscal year and negatively affected growth in profits for the fiscal year to date.

There is the possibility that more shares could be available in the market over the next year or so.

One on One Educational EPS is projected at 20 cents

The stock raced out the blocks on the fifth day of listing in the latter part of last year to hit $2.50 but the price has fallen to a low of $1.10 in December, with investors concerned that they may have lost a major client and the negative impact that may have on profit. The prospectus stated that in August 2021, 63 percent of the Company’s revenue came through Business to Business contracts and 37 percent through the Company’s end user consumers’ business line. Neither the 2022 audited accounts nor the first quarter results show any fall out of business, in fact, revenues almost doubled in the quarter with profit rising to $12 million before tax from a loss of $1.8 million in 2021. The price could be considered appropriate based on results released so far but as more results become available, the current price may appear to be a gift.

Funds raised in the public issue in 2022 net of loan repayment were earmarked for the development of technological infrastructure for expansion. Regardless, the major reasons to invest in this company is not its short-term fortunes or misfortunes but the major potential its operations have to deliver above average growth within Jamaica and overseas.

Spur Tree Spices EPS is projected at 40 cents.

Spur Tree Spices EPS is projected at 40 cents.

The company recorded a 9.4 percent growth in revenues to $672M for the nine-months ended September 2022, from $614 million in 2021. Gross Margin increased from 31 percent in 2021 to 35.4 percent in 2022.

For the September quarter revenues slipped to $233 million from $247 but improved profit margin resulted in a gross profit of $75 million versus $73 million in the prior year. Profit before Taxation fell to $30 million in the quarter from $33 million in 2021, but climbed 30 percent to $119 million for the year to September compared with $91 million in 2021 and was just shy of the $124 million for the full year in 2021.

The company implemented investment projects to expand the Exotic Products factory infrastructure to double production capacity, purchase of building in Port Morant to establish a production facility and upgraded the Spur Tree Spices production capacity.

They also advanced $100 million to purchase a controlling interest in Canco, an ackee canning company, and if combined with Exotic Products could result in a major jump in production and improved efficiency. They also appointed Massy Distributions agents for regional distribution.

This company has a lot of promise but the valuation placed on the stock ran ahead of results as such improved results in 2023 are unlikely to be reflected fully in the stock price and provide above average growth for the stock but it could be good enough to deliver a reasonable gain that investors would be normally pleased with even if it does not put it in the top ranking of stocks. Additionally, it has growth potential going beyond 2023 that could help deliver above average long term growth.

Stationery & Office Supplies recording record 2022 profits.

Stationary and Office Supplies should deliver gains of 250 percent for the period. The company has done exceptionally well in 2022 and is one of the top performing stocks for that year, gaining 140 percent as a result of very strong profit performance during the year that came from an incredible 60 percent increase in revenues that should end close to $1.8 billion for the year and $2.3 billion for 2023. The company generated a profit of $250 million for the nine months to September that should reach $360 million for the full year and just over $550 million in 2023.

ICInsider.com does not expect the performance to be at the same level in 2023 but sees continued attractive growth in earnings that should put it at about $2.20 per share, up from around $1.35 per share in 2022.

The business continues to increase from local and overseas demand. Information is that a deal was struck with a Trinidad company to sell their furniture in that market in addition the possibility exists that they could be getting into other Caribbean countries to add to the organic growth of the business. There is the possibility for acquisitions of small businesses during the year that could benefit from synergies within the company and deliver above average returns from such investments. Investors should not ignore the possibility of a stock split that could provide additional spice to make the performance of the stock an attractive one.

Finally, the company is well managed and financially healthy with limited debt and increasing shareholders’ equity.

Boom coming for Junior Market ICTOP15

The Junior Market ICTOP15 is set for a significant upward climb over the next 15 months as solid economic growth continues and interest rates pull back in 2023. There will be a considerable uptick in Tourism arrivals for the winter season as the sector delivers record performance as it will have fully recovered from the disrupter to the industry in 2020 and deliver record revenues and profits for several companies.

The Junior Market delivered gains for 31 companies in 2022 but underperformed expectations even as the value of shares traded jumped 130 percent to $16.34 billion in 2022 from just $7.1 billion in 2021.

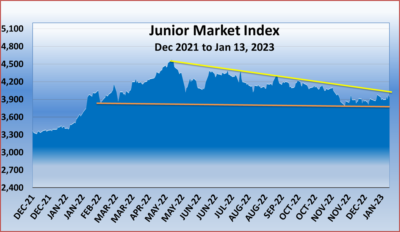

Junior Market Index showing the market in consolidation mode since November ahead of a breakout.

The value of stocks trading in the first 11 months was higher than the previous year, with only December being lower than 2021. Trading slowed in the last three months, helped by new IPOs that pulled funds from the market. Interestingly, the market did not reflect much adverse reaction to the rise in interest rates in 2022.

In the first nine trading days of 2023, the value of stocks traded on the Junior Market rose 15 percent to $172.6 million, up from $149.8 million over the first nine trading days in 2022, and running well ahead of the last month of 2022. That this is unfolding against the drag of higher interest rates sends a powerful message of what lies ahead for the market. Admittedly, there were just 41 listed companies on the exchange at the start of 2022 compared with 47 in 2023, which is a nearly 15 percent increase, and is running well ahead of the last month of 2022. That the increased trading is happening against the drag of higher interest rates sends a powerful message of what lies ahead for the market—the clearest indicator of a booming tourism industry.

The surest sign that prices are heading higher for the Junior Market is that it currently trades around a PE of 13 based on 2022/23 earnings at the end of 2022, with the top 15 stocks representing 32 percent of the market, with PEsfrom 15 to 35, averaging 21, the average based on 2023/4 earnings is a mere 8.6 times.

This is the clearest sign of a boom time in Jamaica’s tourism industry.

Access Financial – EPS projected $2.65 and $4.25 for 2024.

The company suffered a major profit contraction from 2020 to 2022 due to increased loan loss provisions, the write-off of bad loans, and reduced lending. That seems to be behind them, with loans growing again and loan losses reduced.

Profit after Tax of $133 million for the six months ended September 2022, compared to $180 million for the prior period ended September 2021. This performance reflects a 7 percent increase in Operating Revenues in line with a growing loan portfolio. However, this was offset by a 14 percent increase in Operating costs due primarily to increased loan loss and provisions. Loans written off amount to $76 million, up from $58 million in 2021, while provisions fell from $61 million to $54 million.

Revenues for the September quarter from loan interest rose from $419 million to $446 million, but net fees and commission income on loans slipped from $107 million to $103 million and net profit ended at $55 million from $90 million in 2021.

Loans and advances now stand at $4.76 billion for September 2022, an increase of 9 percent year over year and 5.5 percent since March 2022, and reflecting an acceleration in the pace of lending, which augurs well for the second half, with the December quarter being the most critical period for growth.

The expected strong move in the stock price is expected in the latter part of 2024 with a big pick up in profits, investors should note that active selling in the stock is declining and if that continues, investors who want to buy into the stock will have to buy at increasing prices.

AMG Packaging back in ICTOP10

AMG Packaging Projection – EPS 50 cents for 2023

The company can deliver a gain of 350 percent in the stock price over the next 17 months. This is expected to flow from improvement in operations due to the installation of new equipment that became operational in the second quarter of 2022, allowing for greater efficiency and increased business opportunity. The company should benefit from cost reduction in some areas as prices of some inputs have declined since the 2022 results were released and should help improve profitability. With continued economic growth and restoration of the tourism industry, demand for boxes will grow and add to revenue with some cost reduction, as profit is expected to rise.

The fiscal year ended August produced a 41 per cent increase in revenues of $996 million over the 2021 outturn of $706 million with the fourth quarter rising 31 percent from $197 million to $257 million. Profit grew from $61 million in 2021 to $107 million for the 2022 fiscal year. Of note, operating profit for the fourth quarter increased 79 percent to $29.5 million, much faster than revenues—confirmation of input cost reduction also reflected in a decrease in its first quarter of the new year.

Caribbean Assurance Brokers – Projection EPS 30 cents for 2022 and 50 cents for 2023

The company earned a 10 percent increase in revenues of $432 million in the nine months to September 2022 compared to $392 million for 2021. For the third quarter, revenues rose 6 percent to $237 million over $224 million in the 2021 quarter.

Net profit amounted to $105 million for the nine months, while profit for the September quarter was flat with that of 2021 at $100 million. Expenses were well contained at $324 million for the nine months compared with $308 million to September 2021, but costs rose sharply from $121 million in the quarter to $136 million.

The growth trajectory suggests continued improvement in revenues going into 2023 that should contribute to a rise in profit. Recent financials show a picture of steady growth and there are no signs that will change in the short term, Investors will therefore need to understand how to play this stock in the short to medium term.

Caribbean Cream – EPS 2023 is 70 cents, and $1.30 for 2024

Caribbean Cream – EPS 2023 is 70 cents, and $1.30 for 2024

The company performed poorly in 2022, but there are signs in the September quarter results that things are on the mend operationally. After reporting good results for 2021 with a profit of $100 million to February, a slight loss was reported for the year to February 2022 as cost far outstripped growth in revenues—a development that the management never fully combatted.

If the company gets its house in order, it could be a stock to be reckoned with in 2023, despite a poor first half year in 2022 with revenues higher but lower profits than in 2021.

Revenues rose 22 percent to $1.25 billion for the half year to September 2022 compared to $1.03 billion in the previous year and by 33 percent for the quarter to $645 million, up from $486 million in 2021. Gross profit came in at $354 million for the half year, slightly down on the $371 million in the previous year, and the quarter raked in $189 million, a 24 percent increase above $153 million in the last year. While recovering some of the increased direct cost, the company is still not fully back to normal in the second quarter but is ahead of the first quarter. They faced increased prices across the board in various areas, with administrative expenses rising 14.5 percent for the half year and 21 percent in the second quarter, which they could not entirely pass on to the general public.

Notably, the second quarter numbers show an improving position over that of the first quarter and one would expect, all things being equal, the performance to carry over into the second half of the year with the final quarter, which covers the Christmas period, being the best and deliver growth in revenues and profits as a result.

The company continues to increase spending on capital expenditure to improve efficiency further. The financials show fixed assets at $1.35 billion from $858 million at the same time in 2021 and is up from $1.1 billion at the end of February 2022 as the company continues to spend to accommodate increased business activities.

Anthony Chang, Managing Director of Consolidated Bakeries

Consolidated Bakeries – EPS forecast 15 cents for 2022 and 55 cents for 2023.

The company reported impressive half year results that suggest a significant improvement in operations from a 35 percent rise in revenues. The third quarter showed continued strong growth in revenues of 21.5 percent. But that was inadequate to cover costs and resulted in a slight loss of $14.5 million in that period as distribution expenses surged $21 million over the previous year, wiping out more than an $11 million increase in gross profit. The company also suffered a reduction in gross margin in the September quarter, thus compounding the negative effect of increased costs. The December quarter usually delivers greater revenues than the September quarter and is expected to be profitable. With all the improvement in 2022, it is 2023 that should see marked improvement with a broader product range and strong growth in tourism and the local economy. In addition, some of the constraints in 2022 have started to dissipate with improved shipping and reduced cost from the Far East, which should help reduce costs in some areas of the company’s operations.

Dolphin Cove.

Dolphin Cove – EPS is projected at $2.30 for 2022 and $3.50 for 2023.

With the bulk of its income coming directly from the tourism industry, 2023 is going to be an excellent year for the company as the industry bounces back to normal levels that should see growth over 2019., the last full year of normalcy, and jump significantly over the first half of 2022 when the sector had 22 percent less stop over arrivals than in the same period for 2019. Visitor arrivals were up over 2019 in the latter part of 2022, suggesting a likely solid 53 percent jump in arrivals in the 2023 first quarter over that for 2022. The second quarter could equate to a 15 percent increase over the 2022 period and will profoundly impact revenues for the company.

The company stated in their third quarter results that they “ended the third quarter of the year with record financial results, with US$3.9 million in revenue, US$1.6 million more year over year and US$600,000 or 17 percent more, when compared to Q3-2019, which was the year before the pandemic. The flow of visitors to our parks has increased through the year – in Q3-2022, we welcomed double the number of guests in our parks than in Q3-2021 and 25 percent more than in Q3-2019. This is the second quarter with better attendance levels than in pre-pandemic times.”

Elite Diagnostic – EPS is projected at 50 cents for 2023 and $1 for 2024 for the September quarter; revenue increased $47 million from $141 million in the prior year to $188 million. Net profit for the quarter was $5.8 million compared to a loss of $515,000, an improvement of 1,229 percent over the corresponding period in the prior year, but would have been far greater except for increased cost to repair machines and downtime resulting in loss of revenues.

“We continue to record increased revenues in most areas which had significantly declined during the height of the Covid-19 pandemic. However, unforeseen machine downtime during the period under review has negatively impacted our budgetary projections.” The company estimated a shortfall of $25 million in gross revenues due to extensive down time during August and September.

Despite the revenue loss, the latest quarterly results show growth of $176 million over the June quarter, a visible company trend for some years.

The company reported that a branch is slated for Montego Bay in late 2023. The 2023/24 fiscal year could be the breakout for the stock as profits continue to climb upward.

Everything Fresh – EPS is projected at $2.30 for 2022 and $3.50 for 2023

The stock could gain 170 percent in price. The company that sells most of the goods to the tourism sector came off three years of significant losses. Some of which occurred because of the disastrous acquisition by the company. The COVID-19 pandemic impacted the company negatively as the tourism sector was shuttered and only started to come back seriously in 2021 and more so in 2022. This is not the only negative impact the company has overcome in improving the results in 2022. Investors should see even growth over 2019, which was the best period before the pandemic for the sector.

For the nine months to September, revenues jumped 76 percent from $1.079 billion to $1.9 billion and generated a profit of $41 million from a loss of $24 million in 2021. The third quarter recorded revenues of $630 million, a 29 percent increase over $495 million in 2021, and delivered a profit of $9 million from $3.5 million in 2021. Profit for 2022 should end up around 10 cents per share and 35 cents in 2023, with the rebound in the tourism sector giving above average push on revenues. The company benefitted from the bounce in the tourism trade, with much more to come in 2023, as the first quarter will see a big jump in visitor arrivals over 2019 and 2022.

General Accident spreading wings

General Accident Insurance – EPS is projected at 70 cents for 2022 and $1.20 for 2023

For the nine months to September 2022, the company delivered after tax profit of $277 million with the Jamaican operation of General Accident writing premiums of $12 billion and contributing profit before Tax of $297 million. The Trinidad subsidiary registered premiums of $654 million, a 45 percent increase over the $451 million written for the prior year. The Barbados subsidiary wrote premiums of $291 million compared to $214 million for the preceding year. But the company expects the two subsidiaries to be in the black in 2022 and move into profit in 2023.

Investment income for the nine months ended September 2022 was $250 million compared to $148 million in the prior year. Notably, with interest rates trending upwards, there will be increases in consolidated investment income over the short to medium term.

Despite some concerns about the ability to get adequate reinsurance coverage, indications are that General Accident is in a healthy position and is poised to continue to do well and will record increased profits in 2022 and 2023 as operations in Barbados and Trinidad moved from a significant loss in 2021 to profit in 2022. In addition, the stock is an excellent one to hold for long-term investment purposes to benefit from continuous growth and high dividend payments.

Honey Bun – projected EPS of $1 per share for the 2023 fiscal year and $1.85 for 2024

Honey Bun – projected EPS of $1 per share for the 2023 fiscal year and $1.85 for 2024

Profit performance for the financial year to September was disappointing, with revenues surging sharply higher but increased cost eroded the revenue gains. It resulted in a mild reduction in profit for the year.

There are developments in the broader world economy that are set to result in cost reduction in some areas in 2023 that should contain cost increases and thus help deliver increased profit for the year.

For the year to August, revenues rose to $2.95 billion from $2.15 billion in 2021 and delivered a profit of $203 million, down from $219 million after taxation of $51 million and $72 million, respectively, and generated earnings per share of 43 cents versus 46 cents in 2021.

The most recent results ended a four-year run of increased profits, as cost pressure negated an impressive 38 percent surge in sales, but revenue growth pales in comparison to a 59 percent jump in raw material cost for the year, amongst other items reflecting major cost movements.

Gross profit margin fell from 48 percent over the last three years to 40 percent, but a combination of price adjustments and reduction in raw material cost should result in an improvement in the 2023 fiscal year. Raw material accounted for 29 percent of sales in 2021 but surged to 37 percent in the latest year, which will most likely be reversed in 2023. Selling and distribution costs rose 17 percent to $408 million from $348 million in the prior year. Administrative expenses jumped 32 percent to $531 million from $402 million in 2021. Depreciation jumped 25 percent to $91 million from $73 million. Staff costs rose 33 percent to $662 million, of which increased employment accounted for a portion as the number of employed persons climbed 7 percent from 219 to 235.

Lasco Distributors’ EPS is projected at 50 cents for fiscal 2023 and 65 cents for 2024

Increasing revenues by 11 percent to $12.9 billion, improving gross margin that rose more than revenues with a growth of 16 percent and cost containment, delivered a 20 percent increase in after tax profits for the nine months to September 2022. This growth should pick up steam in the second half as revenues and profit after Tax climbed faster in the second quarter of the current fiscal year than in the first by 13.5 percent and 33 percent, respectively. The gross profit margin in the second quarter came in at 17.4 percent versus 16.35 percent in 2021. With the Jamaican economy continuing to record growth above forecast with more to come, Lasco is positioned to take advantage of that.

The company lost its appeal against Pfizer and the legal bills for the defendant will have to be met by Lasco, which may not have been provided for in the half year results. This could weigh down profit in the third quarter, but the effects will be behind them for the 2024 results.

Lasco Financial – EPS is projected at 50 cents for fiscal 2023 and 90 cents for 2024

Revenues rose 12.5 percent to $623 million for the second quarter of 2022 from $554 million in 2021. According to the company, “the increase in income is largely due to the general increase in business transactions. Profit for the three months also exceeds 2021-2022 by $24.7 million, closing at $154 million. Revenues for the six months amount to $1.19 billion, an increase of just 3.7 percent increase over the prior year. For the six months under review, total expenses increased by 5 percent from $857 million to $900 million. The company stated that the administrative expenses increased in line with the expansion of services and growth.”

Profit after Tax for the six months rose 17 percent to $157 million, over $134 million generated in 2021, while the quarter ended at $74 million, 26 percent above the $59 million in 2021.

With the December quarter being one of their biggest for revenues and profit, they should enjoy a bounce in the final quarter of 2022. Although not cast in stone, performance for the current fiscal year is well indicated from the results to date; as such, the next fiscal year is all important.

Lasco Manufacturing – EPS is projected at 60 cents for fiscal 2023 and 80 cents for 2024

After languishing in the doldrums for three years, the company reminded investors that they are not dead and are roaring back to deliver decent growth in revenues and profit for the current fiscal year and into the next. ICI nsider.com expects that the stock that traded as high as $6 in 2021 will surpass this level sooner than later and deliver a handsome gain.

Profit growth accelerated 23 percent for the three months to September to $469 million from $380 million in 2021 and from a rise of 13 percent in the six months to September 2021 from $782 million to $883 million in 2022. Gross profit margin fell in the first quarter to 34 percent but rebounded to 37 percent in the second quarter, bringing the year to date margin to 36 percent compared to 37 percent the previous year, suggesting importantly, the company has now restored the margins to 2020 levels.

Revenues also accelerated 22.6 percent in the second quarter to $2.87 billion from $2.33 billion in 2021, from a growth of 17.5 percent for the six months to $5.47 billion from $4.66 billion. Gross profit rose 18.4 percent to $1.07 billion in the quarter from $870 million in 2021 and climbed 15.3 percent to $1.97 billion for the six months compared to $1.71 billion in 2021.

Operating expenses rose 18.5 percent to $378 million in the 2022 September quarter versus $319 million in the comparable quarter in 2021 and 10.75 percent to $690 million for the six months to September 2022 versus $623 million last year.

Paramount Trading logo

Paramount Trading – EPS projected at 35 cents for fiscal 2023 and 50 cents for 2024

The stock can deliver gains of 465 percent over the next 18 months, making it an attractive, undervalued candidate for acquisition with a view of picking up handsome gains.

A classic turnaround case that pushed the stock up 59 percent in 2022, with more to come in 2023 as profit continues to grow.

The company was poorly impacted by the closure of businesses in the country with the advent of the Covid-19 pandemic, resulting in reduced revenues and profit for the 2021 fiscal year. But it enjoyed a 19 percent bounce in revenues in 2022, with profit jumping to $174 million. It followed that up with a 61 percent increase in revenues for the August quarter, with profit growing to $85 million in 2022 from $19 million. Second quarter results show continued improvement in profit from revenues that climbed 50 percent in the November quarter to $601 million and 55 percent for the half year to $1.2 billion ahead of the 2021 period. Profit surged 126 percent to November quarter to $65 million and 212 percent for the half year to $149 million.

The latest two quarterly numbers send a positive message about the likely outcome for the 2023 performance and beyond.

Tropical Battery – EPS projected at 30 cents for fiscal 2023

The total recovery of the tourism industry is set to propel growth in the wider economy above normal levels in 2023, thus providing increased spending that should boost sales and profit for Tropical. The company had an outstanding 2022 fiscal year, with profits soaring 127 percent over 2021 from a 31 percent rise in revenues over 2021 to $2.63 billion from $1.997 billion in 2021. In addition, the company is raising capital to fund an acquisition that should add to income and profit.

ICInsider.com projects earnings of 30 cents per share for 2023, with the price moving towards a $5 to $6 region during the year.

Check out ICInsider.com Stocks to Watch list.

Watch interest rates steer stocks forward

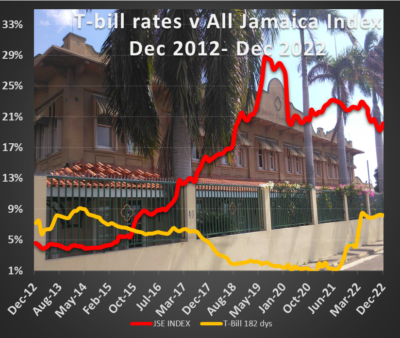

It does not take much to determine the future of the stock market, the direction of interest rates tells it all, well, almost, but profits cannot be ignored. The accompanying chart suggests that the Bank of Jamaica’s recent hikes in interest rates won’t last much longer, a fact that stock market investors need to ponder early in 2023.

While the Bank of Jamaica only recently pushed their Overnight rate to 7 percent, Interest rates on Treasury bills may have peaked as far back as April 2022, with the 182 days’ Treasury bill rate averaging 8.46 percent in the April auction and moderated slightly downwards since, an indication that the market determined rates were at or close to the peak.

Bank of Jamaica moved their overnight interest rates charged to banks from 0.50 percent in September 2021 to 7 percent in November last year, a measure implemented mainly to tame inflation. Inflation has cooled sharply from the high in 2021 and is on the way down. The foreign exchange market buoyancy resulted in some appreciation of the Jamaican dollar, while the NIR seems to have risen to record levels for an end of year close.

Bank of Jamaica moved their overnight interest rates charged to banks from 0.50 percent in September 2021 to 7 percent in November last year, a measure implemented mainly to tame inflation. Inflation has cooled sharply from the high in 2021 and is on the way down. The foreign exchange market buoyancy resulted in some appreciation of the Jamaican dollar, while the NIR seems to have risen to record levels for an end of year close.

The attached chart shows investors tending to react belatedly in response to interest rate movements. Profit ultimately is the primary long term driver of stock values. If interest rates are falling and so are profits, stock prices are unlikely to increase in the short run, the reverse is true. It is, therefore, not surprising that many companies listed on the Junior Market that enjoyed a substantial increase in profits registered good gains in stock prices in 2022, with seven gaining between 100 percent and 312 percent and 8 gaining 50 to 99 percent even as the Junior Market index rose only 16.3 percent for the year, while 21 Main Market stocks gained between 2 and 82 percent for the year, following a 10.2 percent decline in the JSE Main Index and 8 percent for the All Jamaica Composite Index. In all, 22 stocks gained more than the market average. Although not spectacular, the movement in the market was vastly better than the increase in Treasury bill interest rates, which jumped 89 percent above the 4.33 percent rate at the end of December 2021.

Investors can look forward to a fall in rates in 2023 as inflation moderates substantially and falls within BOJ’s 4-6 percent target during 2023. That development will likely be more impactful for Junior Market stocks that will enjoy a higher profit increase than those in the Main Market.

Jamaica Stock Exchange poised for solid gains in 2023

The Jamaican stocks are poised to record a solid performance in 2023 as interest rates commence their decent later in the year and profits of several companies enjoy significant gains. Inflation has passed its peak from 2021 and trended down in 2022 towards the 7 percent level and is set to fall further. The economy is growing as the critical important tourism sector enjoys a sharp recovery while certain input costs have normalized.

Investors should focus on the likely performance of individual companies rather than on the market. Even as interest rates rose sharply last year, it did not prevent the majority of stocks in the Junior Market from rising and nearly half those in the Main Market, as profit growth out weight pressure from rising interest rates. Careful looking at economic developments for 2023 points to another year when there will be significant gains for several companies as profits of many will rise and BOJ cut interest rates as inflation subsides and foreign exchange inflows jump.

Dolphin Cove stock projected to a big 2023 winner.

A key investment observation reveals that good stocks deliver optimal returns over an extended period. They do not usually make huge moves over a short period that is clearly the case with ICTOP15 stocks that may deliver good gains over more than a one year period. Investors need to take this approach to benefit fully from the attractive bargains that currently exist in the Jamaica Stock Market, with uncertainty as to the exact timing of the market takeoff.

The past year ably demonstrated the need to focus on companies, not the markets. The Junior Market managed to record gains of 16.3 percent for the year, but it turned out to be lower than the 29.7 percent gain in 2021. The main market declined at the end of the year as investors forsook the financial institutions in the market and essentially pushed the market down due to rising interest rates.

2022 started off quite brightly for the Jamaica stock market, especially Junior stocks that were up 27 percent by May, but increasing interest rates placed a damper on the performance of stocks, even then, 31 stocks in the Junior Market rose, with 21 gaining 11 percent to a high of 312 percent and 15 stocks gaining over 50 percent, while 7 gained 100 percent or more.

Caribbean Producers to be a big 2023 winner

While the main market index fell 10 percent for the year, the market ended the year with gains in 22 stocks, with gains between two and 82 percent compared with 25 losers that fell from 3 percent to 40 percent. Increased profits were the primary reason for the gains in both markets.

In some cases, some stocks that did spectacularly well in the early part of the year pulled back markedly after Treasury bill rates surged to 8.5 percent in April and remained at that level to the end of the year.

The 80:20 rule of investing shows an average of only 20 percent of stocks that end in the TOP10 in a year repeat in the following one, while around 40 percent of the 10 worst performers end up in the TOP10 in the following year that is supported by data going back 40 years in the local market. The clear message is that investors should not get carried away with an outstanding winner and miss out on other opportunities.

The ICTOP15 are chosen based on the best information available, but there are many other factors to be aware of in 2023 that could swing in favour of or against the selections. Shipping rates that were very high for some time in 2022 are almost back to normal and will result in lower input costs for many listed companies.

Everything Fresh to enjoy gains from tourism in 2023.

Interest rates have been hiked appreciably to contain inflation and foreign exchange demand. With inflation subsiding, interest rates could start a downward trek in the first half of the year and probably before the first quarter ends, when this happens it will be a positive sign for stocks. Worldwide, many prices are declining. Locally, tourism has bounced back strongly but could jump around 50 percent up to April and have significant implications for the broader economy and several listed companies. Bear in mind that the revenues and profits of companies will be affected in different ways and it will be challenging for forecasts to be always close to the mark. 2023 will be a year to key keen eyes on ongoing developments that could affect companies and their operations.

Two key features of the stock market in 2023 will be the strong rebound in tourism traffic in the first half of the year compared with 2022, this development will contribute to above average GDP growth in the first half but will also result in a significant jump in revenues and profits for a number of companies, Caribbean Producers, Dolphin Cove, Everything Fresh and Express Catering that are heavily involved in trading in that sector.

NCB Financial could move from worst performer to TOP10 2023 performer

For the first quarter of 2022 visitor arrivals to Jamaica averaged approximately 72 percent compared to 2019 and 97 percent in the April to June period but in September and October the numbers climbed approximately 12 percent over that for 2019 when this level of recovery is factored into the equation for 2023 visitor arrivals in the first half of the year quit drum by 30 percent or more.

Banks benefited from increased interest rates in 2022 and will continue to do so in 2023 and should see some reversal in losses recorded last year as other comprehensive income. Other companies that would benefit but to a lesser degree are companies such as Wisynco and Jamaica Broilers in addition ICInsider.com expect interest rates to decline during the course of the year and that should provide added stimulus to the market.

A lot of potential gains were not factored into stock prices in 2022 many attractive ones are cheap, investors only task is to make the right choices to pick up gains in 2023 that could be much more exciting than normal.

The Junior Market has 15 stocks representing 32 percent of the market, with PEs from 15 to 35, averaging 21 compared with the above average of the market. The top half of the market has an average PE of 18 and shows the extent of potential gains that lie ahead for the TOP 10 stocks. The situation in the Main Market is similar, with the 20 highest valued stocks priced at a PE of 15 to 110, with an average of 33.5 and 24 excluding the highest valued ones and 22 for the top half excluding the highest valued stock.

Some of the above gains will not be fully reflected until May 2023 as stocks move primarily in response to the release of results. Companies with earlier year ends will discount most of the earnings before those with later periods.

Main Market stocks did poorly as a group in 2022, but they should enjoy a better year in 2023 with interest rates falling during the year and investors are presented with many choices of undervalued stocks. Regardless, Junior Markets stocks are points to outperform those of the more mature companies in the Main Market.

Jamaica’s economy looking great for 2023

The Jamaican economy could grow by more than 6 percent in 2022, with continued growth in tourism and the Alcoa Alumina plant back in production in late August and could lift the December quarter growth above the 5.9 percent that Statin reported for the September quarter. The strong second half year growth should carry over into 2023, coming from an average increase of 5.73 percent for the period up to September and will be boosted by the expected continued strong resurgence of the tourism sector in 2023, barring unforeseen adverse developments, along with the impact of production from the reopening of the Jamalco Alumina plant that will add quite a bit to growth going into the first half of 2023.

Mining to contribute to GDP gains in 2023

Inflation is still not entirely under control yet, but it peaked in 2021, with the average for 2022 running close to the upper end of the central bank’s target of 4 to 6 percent. Developments that should help decrease the rate include world oil prices that have fallen substantially from the over $US120 experienced after the Ukraine war started and are now around US$80 a barrel. Prices of some other commodities are reduced and others could follow as a push of interest rates by several developed countries is set to tighten economic activities and trim demand. A tighter labour market, locally, could put upward pressure on wages and prices, but the tighter monetary policy from last year could hold prices down for a while.

Growth is not only expected from the above two areas. Assuming fair weather conditions, Agriculture, the star performer in the economy for several years, should continue its contribution in 2023. The sector will be helped by growth in tourism that feeds off the industry. The BPO sector seems poised to continue to add to growth as well as the construction sector, with continued growth in housing, road construction and the need for factories and warehousing space. There may well be a lull in the sector with the two south coast roads coming to completion in 2023: the Harbour View to Portland leg and the May Pen to Williamsfield leg of Highway 2000. The Montego Bay perimeter road should take over but may not fill the gap. This may not happen until the Montego Bay to Ocho Rios dualisation commences and is well on the way.

Why is tourism so important? Data shows that for the first quarter in 2022, stopover arrivals were 28 percent below arrivals for 2019, with the June quarter off by 3.3 percent, but September to November increased an average of 12 percent, which means that the first quarter in 2023 could see a 50 percent increase over 2019 and much more over 2022 in the first half on 2022.

Tourist arrivals into Jamaica are now running at record levels since August 2022. Data shows the country enjoying four consecutive months of arrivals exceeding similar months in 2019, the previous best period. Airport passenger movements through the Sangster Airport are up an average of 12 percent for the September to November period.

Growth in tourism is expected to be big in 2023

If the recent trend continues, it would mean that stopover arrivals should be in the order of 3 million next year, up from 2,680,920 in 2019 and would exceed those in 2022 by a solid 20 percent, with the winter months enjoying much higher levels of growth as shown above.

The strong rebound in tourism traffic in the first half of the year, compared with 2022, will contribute to above average GDP growth in the first half but will also result in a significant jump in revenues and profits for some companies and the government. This will have significant implications for the foreign exchange market with significantly increased flows, especially in the year’s first half. This development could also impact interest rates as BOJ may no longer have to lend much support to the local currency using high interest rates.

ICinsider.com don’t see interest moving higher and most likely will start to decline before midyear, with inflation within reach of the BOJ target of 4-6 percent in 2022 and with interest rates seeming to peak at 8.46 percent from April 2022 and remaining at the 8 percent level since based on 182 days Treasury bills.

Jamaica’s labour market has tightened and could pressure inflation in 2023.

Unemployment at 6.6 percent in July is expected to fall in 2023 towards the 5 percent region as more workers will be needed to man the economic expansion. This could mean wage increases could rise above normal to retain or attract new workers.

But all the above is good news for the private sector overall, that should see increasing demand for goods and services.

The banking sector showed loans growing at an annual pace of 12 percent up to September 2022, data from the Bank of Jamaica shows up to $1,096 billion, but increased loan rates may be negatively affecting some areas. With what could be a year of reducing interest rates engineered by BOJ, there could be even faster loan growth in 2023 than in 2022.

Remittances in 2022 appear they will fall short of the US$3.5 billion generated in 2021 and could come in at just over $3.4 billion for the year, reaching $2.84 billion to October. It may again slip marginally in 2023 since the big surge that took it from $2.4 billion in 2019 to the $3.5 billion level.

Net International Reserves. Jamaica’s Net International Reserves are in a healthy position with a jump of $75 million to $3.85 billion in November, data released by the Bank of Jamaica shows, an improvement over October at $3.77 billion. This year’s November balance is at the highest monthly balance for 2022 but is down US$150 million from the end of December last year with a net of $4 billion. Data from the Bank of Jamaica shows a US$100 million growth to Mid December 2022 that would push the net to around US$3.95, just shy of US$4 billion. Daily trades in the forex market after mid-December suggest a continued buildup of the reserves that should push it over the US$4 billion mark by the end of 2022, with the exchange rate for the Jamaica dollar appreciating 152 to the US dollar at the end of the year.

Road construction could slow growth in the sector in 2023

With the significant rebound in tourism, a resurgence in the Alumina sector and relatively stable remittances and BPO sectors, the country should enjoy record foreign exchange inflows in 2023.

Developments on the foreign exchange front could result in greater stability in the exchange rate for the local dollar. Investors should not be too surprised if there is some revaluation, especially in the first half.

The entertainment and transportation sectors seem poised to get a shot in the arm and benefit from the rebound in tourism, increased employment in the country and the general buoyancy in the wider economy.

The present government will be in power for three years at the end of August, but the last public opinion polls indicate a huge lead over the opposition party; with such a lead, the government is in the driver’s seat as to when elections will be called. But the opposition party could start revving up their machinery, so there could be a fair bit of noise to contend with. Local government elections are due in 2023 and barring some significant negative development these elections appear as if they will proceed as planned. If the opposition does well in these elections, it could result in the political heat being turned up a notch or two. If they don’t things will quiet down as the odds favour the government going the full term.

The above are positive developments but investors cannot ignore the impact that the war in Ukraine has had and could have going forward as well as concerns about the covid19 problems in China and how that could affect the world economies.

Reports to follow – Interest rates and the stock market. Outlook for stocks in 2023. Top 15 stocks. Stocks to watch in 2023.