There is a sharp surge in the earnings of foreign exchange in the first two months of this year and the first week of March for Jamaica over the similar period despite the impact that the Covid pandemic has had on business in the country and, in particular the tourism industry.

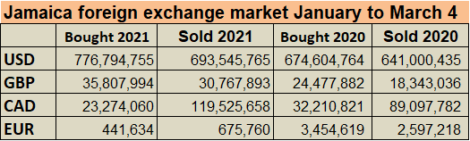

Data out of Bank of Jamaica shows purchasing by Authorized dealers and Cambios for the year to March 4 amounts to $777 million US$103 million more than in 2020, while selling was just $33 million more in 2021 than in 2020. This development is a huge revelation with the tourism sector, a large foreign exchange sector operating around a third of capacity compared to a full capacity for the similar period last year.

Data out of Bank of Jamaica shows purchasing by Authorized dealers and Cambios for the year to March 4 amounts to $777 million US$103 million more than in 2020, while selling was just $33 million more in 2021 than in 2020. This development is a huge revelation with the tourism sector, a large foreign exchange sector operating around a third of capacity compared to a full capacity for the similar period last year.

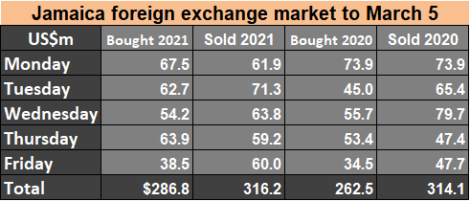

Trading for last week’s Friday resulted in purchases of US$38.5 million and selling of US$60 million against 2020 purchases on the same day of $34.5 million and sales at $47.7 million in all currencies. On Thursday, purchases totalled US$63,861,970 and sales US$59,145,237, well ahead of the same day in 2020.

On Wednesday, purchases amounted to US$54,236,293 and sales US$63,794,632, with the amounts purchased being well ahead of last year’s figure but with sales just $2 million less than last year. Tuesday’s purchases amounted to US$62,667,923, with sales of US$71,359,269, both being much higher than for the similar day in 2020. On Monday, US$67,469,686 were purchased while US$61,868,091 were sold, falling below the 2020 trades.

Last year, trading on the first Monday in March brought in US$73,900,712 while selling amounted to US$73,904,949. Tuesday’s purchases amounted to US$44,971,292 and selling US$65,382,991, while on Wednesday purchases were US$55,679,393 and sales US$79,738,789 and on Thursday, March 5 last year, dealers purchased US$53,369,689 from the system and sold US$47,373,166.

Last year, trading on the first Monday in March brought in US$73,900,712 while selling amounted to US$73,904,949. Tuesday’s purchases amounted to US$44,971,292 and selling US$65,382,991, while on Wednesday purchases were US$55,679,393 and sales US$79,738,789 and on Thursday, March 5 last year, dealers purchased US$53,369,689 from the system and sold US$47,373,166.

Financial institutions have been selling US dollar short as demand weakens and the rate is appreciating. Monday last week saw just US$2.5 million sold in excess of purchases, but National Commercial Bank went short by nearly US$7 million and JMMB Bank by $3 million. Traders went short on Tuesday to the tune of US$15 million with NCB, the major short seller with US$9 million and BNS, FCIB, JMMB Bank, Sagicor and VMBS, making up the bulk of the rest.

NCB is a big player in the FX market.

On Wednesday, net selling amounted to just over US$12 million, with the big net sellers being First Caribbean International Bank, First Global Bank, JMMB Bank, NCB and Sagicor Bank.

On Thursday, there were no overall net sales as purchases exceeded sales, but Scotia Bank, JN Bank and Sagicor Bank sold more than they bought on that day.

One usually reliable and knowledgeable source indicates that from where he sits, “increased inflows are coming from remittances, entities selling US dollars to pay taxes, increased BPO flows and from some exporters”. The high level of short selling is based on demand being soft currently as financial institutions take advantage of the higher rate that the Jamaican dollar sits at. Others are confirming increased flows from the BPO sector that has grown over 2020, increased remittances and exports. Additional flows may be coming from entities or individuals who bought last year in anticipation of the local dollar running away but may have decided to cash in with the price peaking around the $150 million mark.

Others are confirming increased flows from the BPO sector that has grown over 2020, increased remittances and exports. Additional flows may be coming from entities or individuals who bought last year in anticipation of the local dollar running away but may have decided to cash in with the price peaking around the $150 million mark.

On Monday, March 8, dealers bought a total of US$43.3 million in all currencies and sold US$59 million, with short selling of US dollars amounting to $20 million and the selling rate for the US dollar ending at J$148.97. The major short-sellers are BNS, US$3 million, Citibank, US$7.6 million, JMMB Bank, US$2.5 million, JN Bank US$US$2.3 million and Victoria Mutual, US$1.8 million.

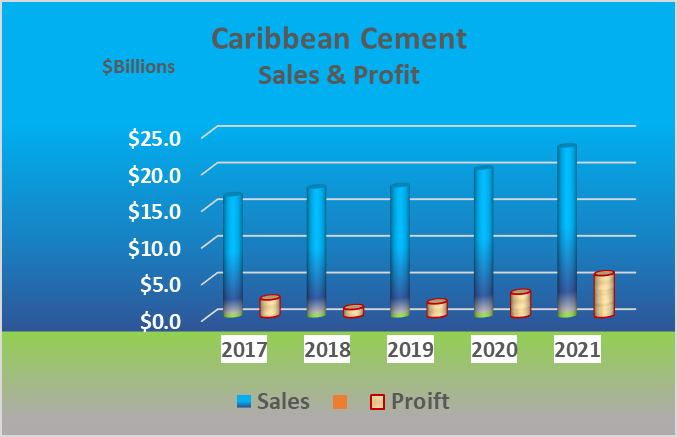

For the year, profit after tax surged 70 percent to $3.2 billion after tax provision of $1.2 billion. The tax charge includes deferred tax amounting to $414 million, down from $664 million in 2019. The results would have been far better but for a billion loss in foreign exchange movement, but interest cost fell from $939 million to $812 million, partially cushioning some exchange losses. Interest cost will fall further in 2021 as the debt load recedes with the strong cash flows allowing for the rapid repayment of the $4.4 billion of long term loans.

For the year, profit after tax surged 70 percent to $3.2 billion after tax provision of $1.2 billion. The tax charge includes deferred tax amounting to $414 million, down from $664 million in 2019. The results would have been far better but for a billion loss in foreign exchange movement, but interest cost fell from $939 million to $812 million, partially cushioning some exchange losses. Interest cost will fall further in 2021 as the debt load recedes with the strong cash flows allowing for the rapid repayment of the $4.4 billion of long term loans. At the end of the year, shareholders’ equity moved to $11.5 billion from $8.3 billion at the end of 2019. The stock is one of the original

At the end of the year, shareholders’ equity moved to $11.5 billion from $8.3 billion at the end of 2019. The stock is one of the original  The evidence can be seen in an exchange rate that was US$1.10 to the Jamaican dollar to nearly $150 to one US dollar now. Interest rates rose from 5.5 percent in 1970 for governments Local Registered Stock, by the dark years in 1990s rates on government paper were as high as 52 percent in 1994. The average

The evidence can be seen in an exchange rate that was US$1.10 to the Jamaican dollar to nearly $150 to one US dollar now. Interest rates rose from 5.5 percent in 1970 for governments Local Registered Stock, by the dark years in 1990s rates on government paper were as high as 52 percent in 1994. The average  Three companies went to the market to raise funds in January and all were successful with the latest

Three companies went to the market to raise funds in January and all were successful with the latest

For the week to Thursday, NCB sold off a net of US$24 million. Dealers bought US$32 million on Thursday and sold US$56.6 million compared to buying US$46.8 million and selling US$51.4 million on Wednesday at an average rate of $142.6258. On Thursday, NCB sold a net of nearly US$20 million.

For the week to Thursday, NCB sold off a net of US$24 million. Dealers bought US$32 million on Thursday and sold US$56.6 million compared to buying US$46.8 million and selling US$51.4 million on Wednesday at an average rate of $142.6258. On Thursday, NCB sold a net of nearly US$20 million.

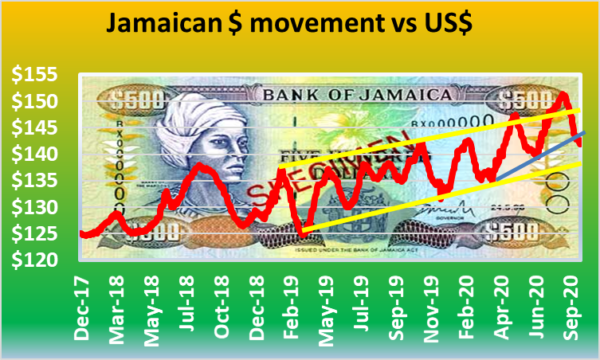

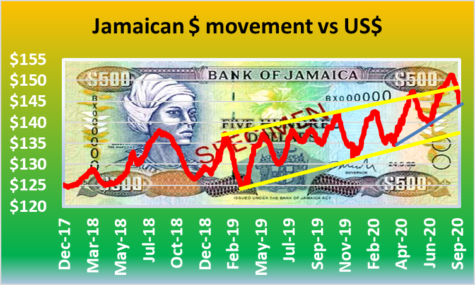

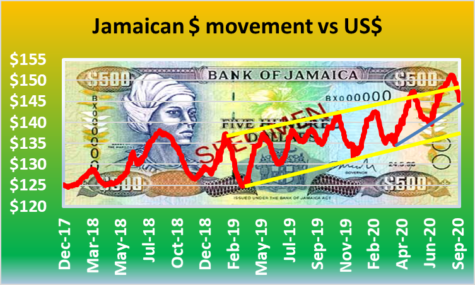

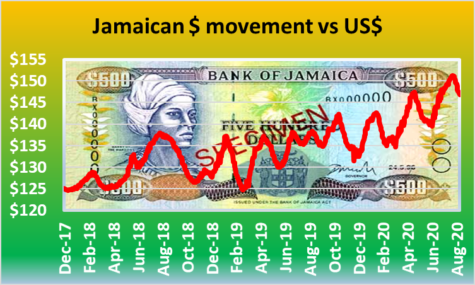

Since August when the rate hit a low of $151.27 against the US dollar, the local dollar has rebounded 4.5 percent. A number of developments have occurred to help the local currency. Unbeknown to many is an issue of $5 billion government bond with a duration of more than 30 years that pulled liquidity out of the market to purchase them at an average rate of just over 7 percent, there was also another issue at the beginning of September for J$3 billion bonds resulting in an average rate of 2.91 percent for the instrument that has a two and a half years life. In addition, the reopening of the tourism sector would be adding some badly needed US dollars to the system.

Since August when the rate hit a low of $151.27 against the US dollar, the local dollar has rebounded 4.5 percent. A number of developments have occurred to help the local currency. Unbeknown to many is an issue of $5 billion government bond with a duration of more than 30 years that pulled liquidity out of the market to purchase them at an average rate of just over 7 percent, there was also another issue at the beginning of September for J$3 billion bonds resulting in an average rate of 2.91 percent for the instrument that has a two and a half years life. In addition, the reopening of the tourism sector would be adding some badly needed US dollars to the system. The Jamaican dollar hit a low of $151.27 against the US dollar in August and has rebounded since to trade at $145.3 on Wednesday with one technical indicator showing that it could appreciate further.

The Jamaican dollar hit a low of $151.27 against the US dollar in August and has rebounded since to trade at $145.3 on Wednesday with one technical indicator showing that it could appreciate further. In Wednesday’s trading, dealers sold $64.8 million at $145.306 having bought US$55.8 million at an average rate of $144.43. In trading, Scotia Bank bought US$8.5 million more than they sold. First Global, JMMB Bank, National Commercial Bank and Victoria Mutual Building Society sold far more US dollars than the bought.

In Wednesday’s trading, dealers sold $64.8 million at $145.306 having bought US$55.8 million at an average rate of $144.43. In trading, Scotia Bank bought US$8.5 million more than they sold. First Global, JMMB Bank, National Commercial Bank and Victoria Mutual Building Society sold far more US dollars than the bought. On Monday, dealers sold US$36.5 million at an average of $146.89, while dealers bought just US$23.2 million, at an average rate of $144.02.

On Monday, dealers sold US$36.5 million at an average of $146.89, while dealers bought just US$23.2 million, at an average rate of $144.02. National Commercial Bank bought US$32,148,142.99 at an average rate of J$129.83 and sold US$73,145,676 at J$130.16 each. The trade by the country’s largest commercial bank accounted for 48 percent of the total of US$67.5 million purchased and 70 percent of the US$104.3 million sold. After NCB, the next biggest trades were by Bank of Nova Scotia, in buying US$10.3 million, at an average of $132.60 and selling $7 million at $133.54.

National Commercial Bank bought US$32,148,142.99 at an average rate of J$129.83 and sold US$73,145,676 at J$130.16 each. The trade by the country’s largest commercial bank accounted for 48 percent of the total of US$67.5 million purchased and 70 percent of the US$104.3 million sold. After NCB, the next biggest trades were by Bank of Nova Scotia, in buying US$10.3 million, at an average of $132.60 and selling $7 million at $133.54. The Bank of Jamaica’s website shows their inflation target for the 2019 to 2020 fiscal year ranging from four to 6 percent and they expect that such high levels of inflation should be achieved by 2020/21.

The Bank of Jamaica’s website shows their inflation target for the 2019 to 2020 fiscal year ranging from four to 6 percent and they expect that such high levels of inflation should be achieved by 2020/21.