Profit popped 45 percent higher in 2022 at Derrimon Trading Company to $580 million for shareholders, following a mere 3.8 percent rise in revenues to $18.4 billion from $17.74 billion in 2021 and following a fall in cost of sales to $13.78 billion from $14.34 billion in 2021 resulting in gross profit rising a solid 36 percent to $4.6 billion from just $3.4 billion, with profit margin climbing to 25.2 percent from just 19.2 percent in 2021.

Sales revenue fell in the final quarter compared with 2021, with $4.6 billion generated in the December 2022 quarter, down from $5.6 billion in 2021, as segment data shows the wholesale and retail segment suffering a $1.8 billion decline for the year to $8.4 billion. “We took deliberate strategic steps to focus more on our retail business that has greater margins and improves cash flows,” Derrick Cotterell, Managing Director, advised ICInsder.com in response to a question about the reasons for the lower sales in the December quarter. He continued to indicate that “going forward, there will be more focus on brands with a higher margin and less on bulk products.” He said it does not mean they are getting out of the bilk products.

Sales revenue fell in the final quarter compared with 2021, with $4.6 billion generated in the December 2022 quarter, down from $5.6 billion in 2021, as segment data shows the wholesale and retail segment suffering a $1.8 billion decline for the year to $8.4 billion. “We took deliberate strategic steps to focus more on our retail business that has greater margins and improves cash flows,” Derrick Cotterell, Managing Director, advised ICInsder.com in response to a question about the reasons for the lower sales in the December quarter. He continued to indicate that “going forward, there will be more focus on brands with a higher margin and less on bulk products.” He said it does not mean they are getting out of the bilk products.

Other operating income includes rental, $82 million from a gain on acquiring a subsidiary, management fees and dividend. Debt recovery generated $237 million in 2022, up from $104 million in 2021.

Operating and administrative expenses rose 28.7 percent to $2.995 billion in 2022 from $2.33 billion in the previous year. Sales and distribution expenses increased by a hefty 71 percent to $689 million from $402 million in 2021. The shift in focusing on retail business is also based on increased borrowing costs, with interest rates having risen sharply in the country and forcing attention on improving cash flows to keep borrowings down and, by extension, interest cost. Finance costs more than doubled to $464 million from $231 million in 2021.

Going forward, the group will benefit from opening a supermarket in May Pen in the last quarter, which Cotterell says is doing very well.

Going forward, the group will benefit from opening a supermarket in May Pen in the last quarter, which Cotterell says is doing very well.

Gross cash flow brought in $1.25 billion, which was used to fund increased working capital of $720 million, capital expenditure amounted to $1.47 billion that was partially financed by loans inflows net of repayment of $600 million.

At the end of December, shareholders’ equity stood at $6.1 billion, with long term borrowings at $4.7 billion and short term at $476 million. Current assets ended the period at $7.3 billion inclusive of trade and other receivables of $2.2 billion, cash and bank balances of $900 million. Current liabilities ended at $4.3 billion and net current assets at $2.9 billion.

Earnings per share came out at 12.8 cents for the year, up from 9.4 cents in 2021. IC Insider.com forecasts 16 cents per share for 2023, with a PE of 14 times the current year’s earnings based on the price of $2.10, the stock traded at on the Jamaica Stock Exchange Junior Market.

The company did not pay a dividend during the year and ended with a net asset value at the end of the year at $1.22, with the stock selling at 1.73 book value.

Profit bolted 45% at Derrimon in 2023

Barita acquires 20% of Derrimon Trading

Barita Investments now owns 20% of the issued shares of Derrimon Trading Company following the closing of the Derrimon additional public offer of shares, Barita disclosed in a release to the Jamaica Stock Exchange.

Barita headquarters.

Commenting on the investment, Jason Chambers, Director of Barita and Chief Investment Officer of Barita’s parent company, Cornerstone, said: “The Board of Directors of Barita and the leadership team of Cornerstone are very satisfied with this investment as Derrimon embodies several of the characteristics we typically look for in assessing investment opportunities. DTL has built up an enviable track record of growth and value creation, and the management has demonstrated their ability to achieve scale both organically and through the successful integration of several accretive acquisitions. Barita has, over the course of the last two-plus years, established significant capacity to expand its portfolio of investments into sectors that are viable alternatives to traditional ones that are now fully priced in our view and therefore not likely to generate alpha for our shareholders in the medium to long term. This minority acquisition should be seen as a by-product of our increased investing capacity as we prudently seek to unearth both value and growth-oriented investment opportunities within the context of the current global investment landscape.”

Chambers continued, “We also note the diversification factor that this investment adds to our portfolio as it provides exposure to the real sector via a company which has recently begun an international expansion.

Mayberry tried trading 420m Derrimon Trading shares but the transaction was disqualified.

At Cornerstone and Barita, our goal is to positively impact the lives of our stakeholders through the tireless pursuit of opportunities that provide solid risk-adjusted returns throughout their investment horizons. We believe this investment is aligned with that ethos and we look forward to collaborating with the team at DTL to the mutual benefit of our collective stakeholder groups.”

Paula Barclay, General Manager of Barita, in commenting on the Company’s investment in Derrimon, stated: “At Barita, we continuously seek out unique strategic opportunities to build shareholder value while balancing the interests of our clients, team members, and other key stakeholders. We are confident that our association with a company like Derrimon will only contribute positively to our overall future performance. Consummating this investment took significant effort from the team at Barita and I would like to take this opportunity to extend my gratitude to them for their hard work.”

Barita Investments is a publicly-traded Securities Dealer listed on the Jamaica Stock Exchange and majority-owned by Cornerstone Financial Holdings.

Derrimon Trading is listed on the Junior Market of the Jamaica Stock Exchange and distributes dry and frozen bulk commodities. It also operates retail outlets and Supermarkets.

The shares of Barita are trading at $81.14 and Derimon at $2.56 on early Friday morning after the release.

Investors gobble up new issues

The Jamaican economic and financial environment has undergone much change over the past five decades or so. Since the early 1970s, the country lost its way and endured years of negative economic and in cases social development.

The evidence can be seen in an exchange rate that was US$1.10 to the Jamaican dollar to nearly $150 to one US dollar now. Interest rates rose from 5.5 percent in 1970 for governments Local Registered Stock, by the dark years in 1990s rates on government paper were as high as 52 percent in 1994. The average Treasury bill rates, between 1992 and 1994 was 39.5 percent. That was the challenge that the banks and businesses face in that period that led to the collapse of the businesses and the destruction of the financial sector.

The above set the stage for the state of the capital market in Jamaica now. In 1986, National Commercial Bank as it was then named went to the market, with the issue pulling in $249 million or US$45 million and attracted over 30,000 shareholders in a heavily oversubscribed issue. The total amount attracted seems to be the largest public issue ever in the local market.

That was then, now interest rates have hit levels that are the lowest on record, with Treasury bill rates now less than one percent and there are now more than 200,000 investors owning shares compared to around 40,000 after the NCB issue, making for a larger pool of investors to draw on to take up new issues.

Three companies went to the market to raise funds in January and all were successful with the latest Derrimon Trading Company invitation for subscription of 1,498,698,931 Ordinary Shares with the option to upsize was oversubscribed with taking up an additional 301,301,069 shares. The company will issue 1.8 million Shares and take in J$4.08 billion in gross proceeds.

Three companies went to the market to raise funds in January and all were successful with the latest Derrimon Trading Company invitation for subscription of 1,498,698,931 Ordinary Shares with the option to upsize was oversubscribed with taking up an additional 301,301,069 shares. The company will issue 1.8 million Shares and take in J$4.08 billion in gross proceeds.

The allocation of the issue will result in existing shareholders and Derrimon team members receiving 51.63 percent of their application. Key Investors will get all of their applications, Lead Broker’s Clients 83.72 percent and Non-Reserved Share Applicants (General Public) 39.15 percent.

Proven Investments upsized of the Additional Public Offer (APO) of ordinary shares to a maximum of 134,124,037 units with applications totalling 154,231,234 shares, for an oversubscription of US$4.3 million. Proven states that 4,148 applications were received, totalling just over US$34.5 million.

Applicants in General Pool and existing shareholders applicants in the pool will receive a full allotment, but Key Investors Applicants in this pool will receive 70.75 of the subscription amount.

Sygnus Credit Investments APO of ordinary shares was upsized to 240,887,900 Shares, reflecting a 54 percent upsize to the maximum allowed. The issue pulled around US31 million for the company.

Derrimon expands with APO funds

Derrimon Trading is spreading its wings, to New York, with the recently announced agreement to acquire control of the Brooklyn-based operations of FoodSaver New York, Inc. a wholesale food distributor and Good Food For Less, LLC, a speciality supermarket.

The acquisition will be done through a New York based, Derrimon subsidiary, Marnock LLC, which will acquire the Brooklyn-based operations as a going concern. “The overall consideration upon completion is expected to be valued between USD$8.9 million and USD$9.1 million,” Derrimon states. The amount translates to J$1.3 billion.

The acquisition will be done through a New York based, Derrimon subsidiary, Marnock LLC, which will acquire the Brooklyn-based operations as a going concern. “The overall consideration upon completion is expected to be valued between USD$8.9 million and USD$9.1 million,” Derrimon states. The amount translates to J$1.3 billion.

The purchase will be funded from proceeds of a current additional public offer, to raise around J$3.5 billion and a 20 percent minority interest in Marnock.

Derrimon expects the deal to be completed in the first quarter of this year. According to the prospectus, the businesses being acquired generated revenues of J$5.1 billion with 6% or J$311 million being converted into net income.”

Derrimon Trading reported flat revenues of $9.62 billion for the nine months to September over $9.53 billion reported for the similar period in 2019, with Gross Profit of $1.84 billion, increasing by $182 million and Profit before Tax of $316 million, up 25 percent or $61 million over 2019. ICInsider.com forecast is 16 cents per share for 2021, with the current PE Ratio at 15 times earnings and suggesting the stocks is fairly priced on the basis that the existing business remains substantially intact along with the new business being acquired. The company has just two years left of the tax concession for listing on the Junior Market.

Caribbean Flavours a Derrimon’s subsidiary

The company is offering if fully subscribed the gross proceeds will be approximately J$3.50 billion, of which approximately J$205.25 million is expected to be used to pay transaction costs. The net proceeds from the invitation are expected to be J$3.29 billion. If the option to upsize is fully exercised the maximum proceeds is J$4.22 billion and result in the total shares in issue at 4.2 billion based on the initial share offer.

The shares are priced at $2.20 for existing shareholders and $2.40 for the public. Derrimon has grown by using a high level of borrowed funds, which is a highly risky way for funding expansion. $1.1 billion of the APO proceeds will be used to fund the New York businesses’ acquisition. $1.2 billion will be used in reducing existing loans, with $500 million to be used in the expansion of a retail location in Clarendon and working capital.

There are positives and negatives with the acquisition and capital raise. The successful raising of fresh capital will better balance the company’s leveraging that was out of line with safe levels. The amount slated for debt reduction will save around $90 billion per year before taxation and will help to improve the profitability of the group. The group can reduce some areas of cost with the larger size and will have greater opportunities for cross-country sales, thus expanding sales and profit. Overseeing managing a new business overseas is often more difficult than it may appear at the start.

The current share offer closes on January 26 and the stock last traded at $2.38 on the Junior Market of the Jamaica Stock Exchange.

Medical Disposables out Jetcon in – Top 5

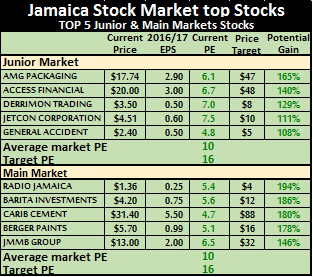

Medical Disposables fell out of the Top 5 junior market selection during the past week, based on price movement, with the bid at $4.95 and Jetcon Corporation with the price at $4.51 returns, making it back into the top list by just inching ahead of General Accident.

Medical Disposables fell out of the Top 5 junior market selection during the past week, based on price movement, with the bid at $4.95 and Jetcon Corporation with the price at $4.51 returns, making it back into the top list by just inching ahead of General Accident.

The insurance company enjoyed strong buying during the past week and could slip out in the coming week. Medical Disposables still has more room for growth with the company expanding its product range. Derrimon Trading moved up to third spot after the stock traded at $4 during the week but pulled back to $3.50 by the close. Knocking at the Top 5 position in the junior market are tTech now that the price slipped to $5.30, Caribbean Flavours and Caribbean Cream with Paramount Trading just below.

Stocks in the main market all remained in the Top 5 but positions have changed, the top attraction for the week is JMMB Group that climbed to $13 and sits just and now sits at number 5 spot having entered at the top spot last week. With the news of the group obtaining a banking license, the way may be clear for the price to surge a bit more in the coming week and most likely push it out of the top 5. Stocks peeping in at the Top 5 in the main market are Grace Kennedy, National Commercial Bank and Sterling Investments.

Stocks in the main market all remained in the Top 5 but positions have changed, the top attraction for the week is JMMB Group that climbed to $13 and sits just and now sits at number 5 spot having entered at the top spot last week. With the news of the group obtaining a banking license, the way may be clear for the price to surge a bit more in the coming week and most likely push it out of the top 5. Stocks peeping in at the Top 5 in the main market are Grace Kennedy, National Commercial Bank and Sterling Investments.

With the junior market trading at new records this past week, the attractive gains that were evident a few weeks ago are receding in the junior market with IC Insider data showing just 7 junior market stocks that could double by early 2017. That is in contrast to the main market that shows 15 stocks that could double or more than double. All that is reflected in the fact that the junior market is up 33 percent year to date, while the main market is up just 9 percent.

Lasco & Kremi push juniors to new record close

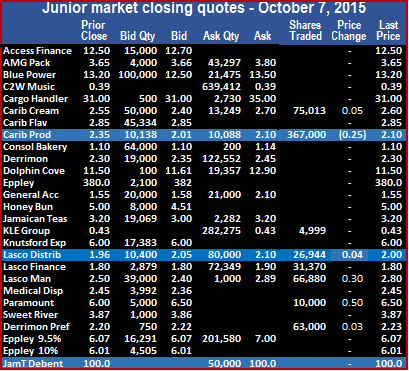

Caribbean Cream ended at a new closing all-time high on Wednesday of $2.60.

At the close 3 securities ended with no bids to buy, while 10 had no stocks being offered for sale. A total of 7 stocks closed with bids higher than the last traded prices and none closed with a lower offer.

In trading, Caribbean Cream traded to end at a new all-time closing high of $2.60 with 75,013 shares changing hands, after gaining 5 cents. Investors were responding to a sharp increase in profit of $46 million versus $1.3 million in the prior year for the August quarter.

Caribbean Producers lost 25 cents in trading 367,000 shares at $2.10, KLE Group ended with 4,999 units changing hands at 43 cents, Lasco Distributors with 26,944 units trading, ended 4 cent up to $2. Lasco Financial had 31,370 shares changing hands to end at $1.80, Lasco Manufacturing traded 66,880 shares to end at a new high of $2.80 after gaining 30 cents for a new all-time high. Paramount Trading gained 50 cents while 10,000 units changed hands at a new high of $6.50 and Derrimon Trading Company 11.75% preference share ended with 63,000 units changing hands at $2.23.

Caribbean Producers lost 25 cents in trading 367,000 shares at $2.10, KLE Group ended with 4,999 units changing hands at 43 cents, Lasco Distributors with 26,944 units trading, ended 4 cent up to $2. Lasco Financial had 31,370 shares changing hands to end at $1.80, Lasco Manufacturing traded 66,880 shares to end at a new high of $2.80 after gaining 30 cents for a new all-time high. Paramount Trading gained 50 cents while 10,000 units changed hands at a new high of $6.50 and Derrimon Trading Company 11.75% preference share ended with 63,000 units changing hands at $2.23.