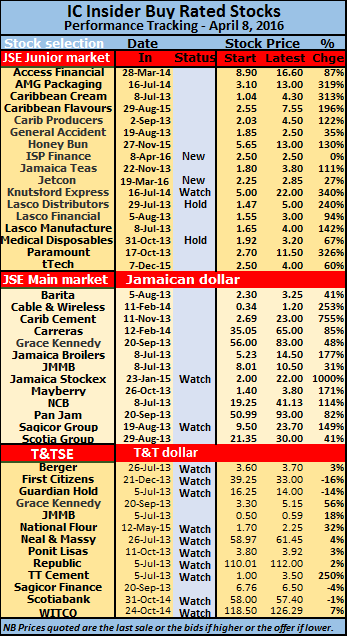

I$P hits a new high on Friday.

The original audited report had the average number of shares issued at 126.5 million instead of 88.44 million which the amended report now shows.

The company reported profit of $40.24 million after tax from increased revenues of $30 million to reach $241 million in 2016. Other operating expenses jumped sharply from $36.6 million to $64.8 million. Individual items did not move much during the two years. In 2015 a refund of insurance premium amounting to $12.3 million was offset against expenses, reducing expenses from $49 million to $37 million, while 2016 figures had a few items of cost not reflected in the 2015 results. These include directors’ fees, bond issue cost and consultancy fees of $6 million. ISP also benefited from loan loss recovery, leading to lower loan loss provisioning at year end, from $19 million 2015 to just $10 million in 2016. Some debt was, however, fully written off, management informed IC Isider.com, reducing the overall provision to $53.7 million from $63 million at the end of 2015.

The company is gearing to grow. Last year apart from restructuring it finances that led to a public share issue, the company floated a bond issue that raised over $140 million net, which will be used to supplement cash flow from earnings. Discussion with the company’s management team led by Dennis Smith, reveal, that the $60 million growth in loans in the December quarter mostly remains on the books while the plan is for a 30 to 40 percent expansion in the current year. If that level of growth is achieved it would take net loans to more than $400 million by year end and raise revenues in a full year to more than $400 million and raise profit sharply from the current levels.

The company started off serving the security guard sectors but is targeting new areas within the business sector for expansion as well as areas outside of the corporate area.

Management appears to be gathering information as to the feasibility of a stock split and that seems to be a logical move, with just 105 million shares now issued and prospects for a rapid increase in profits going forward. Management would neither deny nor confirm if that is on the cards.

IC Insider.com is forecasting earnings in the current year to be in the order of $1.40-$1.75, with continued strong increase into 2018. The stock closed on the Junior Market of the Jamaica Stock Exchange at and 52 weeks high of $15.50 on Friday, resulting in gains of 675 percent, since it was listed at the end of March 2016.

With the potential to grow rapidly, the stock remains BUY RATED even with the price now at the level reached on Friday.

Jamaica Stock Exchange Junior Market”. The company in fact issued 26 million bonus shares in 2013 while the public offering was for 20,000,000 ordinary shares, only 4,867,338 new shares were offered by the company while 15,132,662 shares existing shares were sold to the public in the IPO by shareholders. At the time the IPO, 95,132,662 ordinary shares were already issued, the average number of shares should be approximately 60 million rather than 46.8 million used to compute the 2014 EPS, which would have worked out around 83 cents.

Jamaica Stock Exchange Junior Market”. The company in fact issued 26 million bonus shares in 2013 while the public offering was for 20,000,000 ordinary shares, only 4,867,338 new shares were offered by the company while 15,132,662 shares existing shares were sold to the public in the IPO by shareholders. At the time the IPO, 95,132,662 ordinary shares were already issued, the average number of shares should be approximately 60 million rather than 46.8 million used to compute the 2014 EPS, which would have worked out around 83 cents.