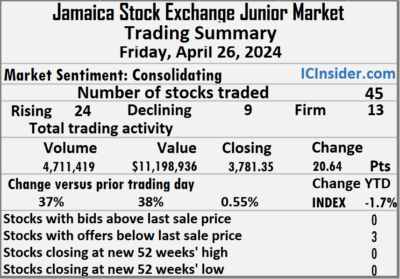

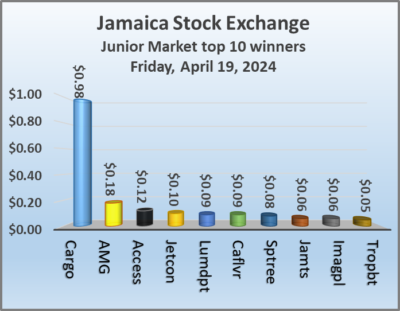

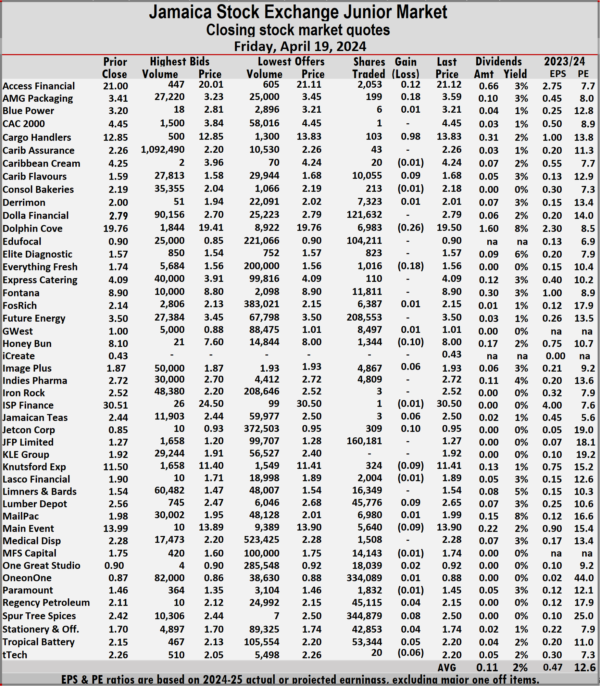

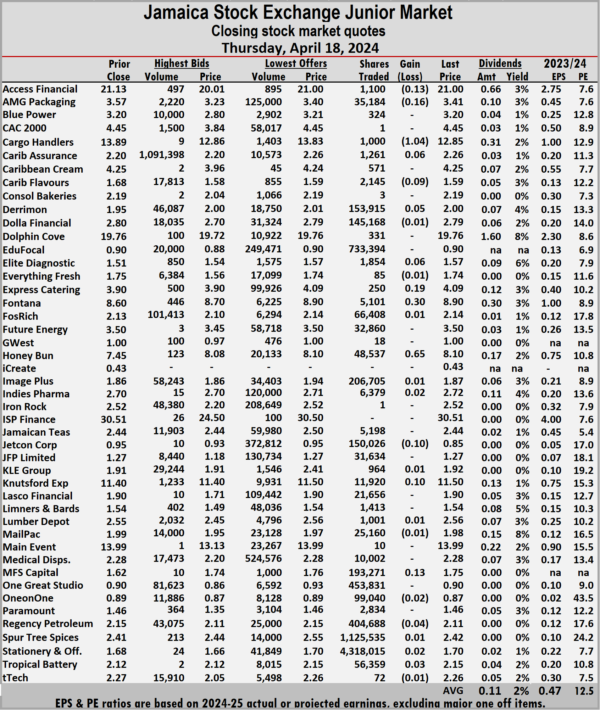

Stocks mostly rose on the Junior Market of the Jamaica Stock Exchange on Friday, after trading in 45 securities compared with 40 on Thursday and ending with prices of 24 rising, 9 declining and 12 closing unchanged following a 37 percent rise in the volume of stocks traded, with 38 percent greater value than Thursday.

At the close of trading, the Junior Market Index rallied 20.64 points to end the day at 3,781.35.

At the close of trading, the Junior Market Index rallied 20.64 points to end the day at 3,781.35.

Trading ended with 4,711,419 shares for $11,198,936 up from 3,441,451 units at $8,137,990 on Thursday.

Trading averaged 104,698 shares at $248,865, up from 86,036 units at $203,450 on Thursday with the month to date, averaging 189,955 units at $422,648 but slightly down from 194,892 stock units at $432,712 on the previous day and March ending with an average of 221,659 units at $464,382.

Fosrich led trading with 859,227 shares for 18.2 percent of total volume followed by ONE on ONE Educational with 662,171 units for 14.1 percent of the day’s trade and Spur Tree Spices with 534,967 units for 11.4 percent market share.

The Junior Market ended trading with an average PE Ratio of 12.9, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

The Junior Market ended trading with an average PE Ratio of 12.9, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows none ended with a bid higher than the last selling price and three with lower offers.

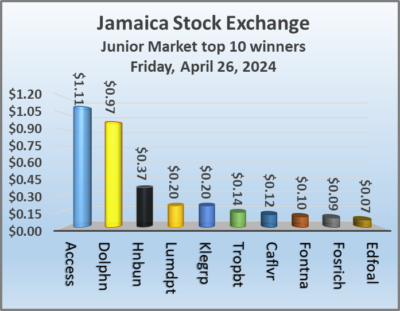

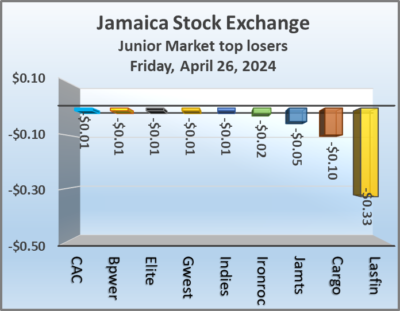

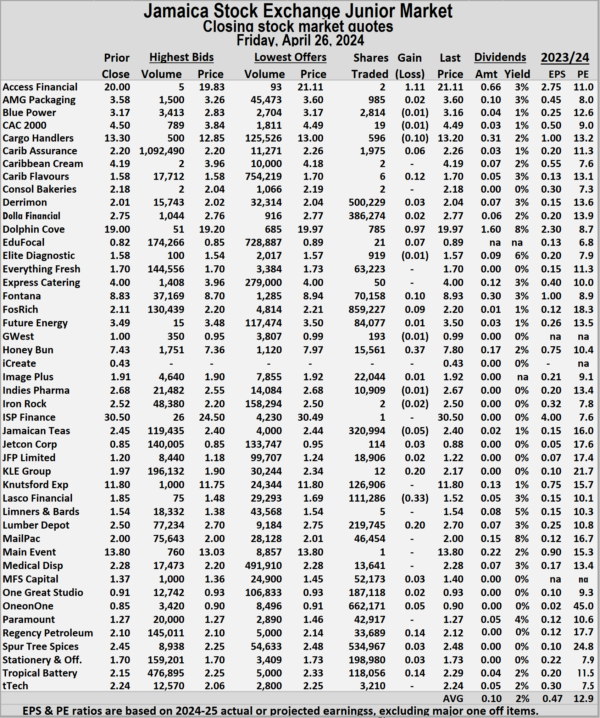

At the close, Access Financial gained $1.11 to end at $21.11, after just two stocks passed through the market, Cargo Handlers dipped 10 cents in closing at $13.20 with traders dealing in 596 units, Caribbean Assurance Brokers rose 6 cents to close at $2.26 with 1,975 shares clearing the market. Caribbean Flavours advanced 12 cents to end at $1.70 with investors swapping a mere 6 stock units, Dolphin Cove popped 97 cents to finish at $19.97 with an exchange of just 785 shares, EduFocal rallied 7 cents and ended at 89 cents, with 21 stocks crossing the market.  Fontana increased 10 cents to $8.93 in an exchange of 70,158 units, Fosrich climbed 9 cents in closing at $2.20 with investors dealing in 859,227 stock units, Honey Bun popped 37 cents to finish at $7.80 in an exchange of 15,561 shares. Jamaican Teas lost 5 cents and ended at $2.40 with investors trading 320,994 stock units, KLE Group increased 20 cents to close at $2.17 after an exchange of 12 stocks, Lasco Financial slipped 33 cents to end at $1.52 with 111,286 units passing through the market. Lumber Depot climbed 20 cents to $2.70 after a transfer of 219,745 shares, ONE on ONE Educational rose 5 cents to finish at 90 cents as investors exchanged 662,171 units and Tropical Battery rallied 14 cents and ended at $2.29 and closed with an exchange of 118,056 stocks.

Fontana increased 10 cents to $8.93 in an exchange of 70,158 units, Fosrich climbed 9 cents in closing at $2.20 with investors dealing in 859,227 stock units, Honey Bun popped 37 cents to finish at $7.80 in an exchange of 15,561 shares. Jamaican Teas lost 5 cents and ended at $2.40 with investors trading 320,994 stock units, KLE Group increased 20 cents to close at $2.17 after an exchange of 12 stocks, Lasco Financial slipped 33 cents to end at $1.52 with 111,286 units passing through the market. Lumber Depot climbed 20 cents to $2.70 after a transfer of 219,745 shares, ONE on ONE Educational rose 5 cents to finish at 90 cents as investors exchanged 662,171 units and Tropical Battery rallied 14 cents and ended at $2.29 and closed with an exchange of 118,056 stocks.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

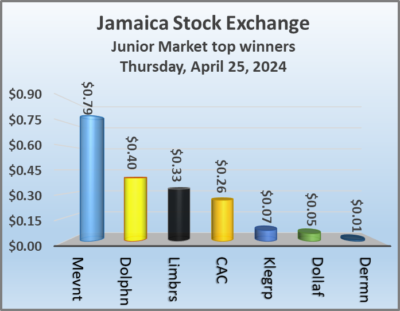

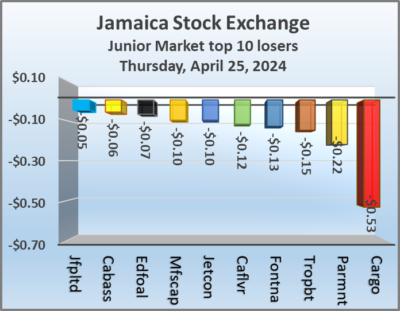

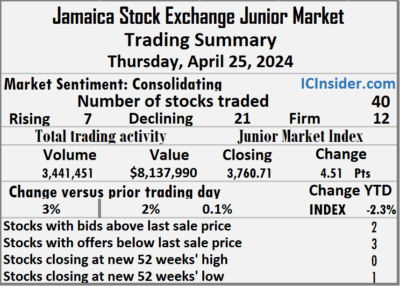

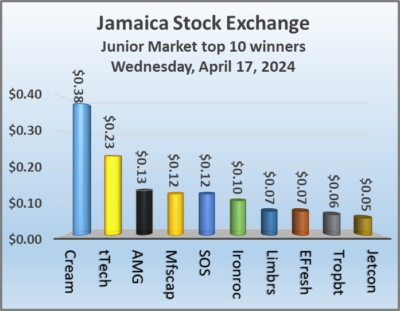

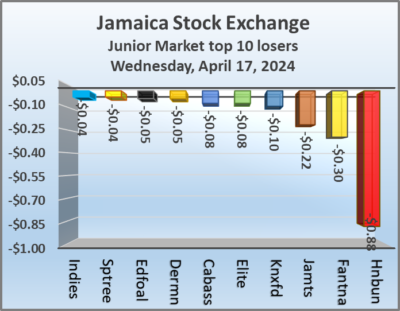

Few Junior Market winners

Winning stocks were hard to come by as trading closed on the Junior Market of the Jamaica Stock Exchange on Thursday, with trading in 40 securities down from 41 on Wednesday and ending with prices of just seven rising, 21 declining and 12 closing unchanged following a moderate rise in the volume and value of stocks that were exchanged on Wednesday.

The market closed with trading of 3,441,451 shares for $8,137,990 up from 3,333,072 units at $7,971,094 on Wednesday.

The market closed with trading of 3,441,451 shares for $8,137,990 up from 3,333,072 units at $7,971,094 on Wednesday.

Trading averaged 86,036 shares at $203,450 compared to 81,294 units at $194,417 on Wednesday, with a month to date average of 194,892 units at $432,712 down from 200,800 stocks at $445,155 on the previous day and March with an average of 221,659 units at $464,382.

Dolla Financial led trading with 1.09 million shares for 31.7 percent of total volume followed by Spur Tree Spices with 789,268 stock units for 22.9 percent of the day’s trade and Fosrich with 589,091 units for 17.1 percent market share.

At the close of trading, the Junior Market Index increased 4.51 points to settle at 3,760.71.

The Junior Market ended trading with an average PE Ratio of 12.3, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and three with lower offers.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and three with lower offers.

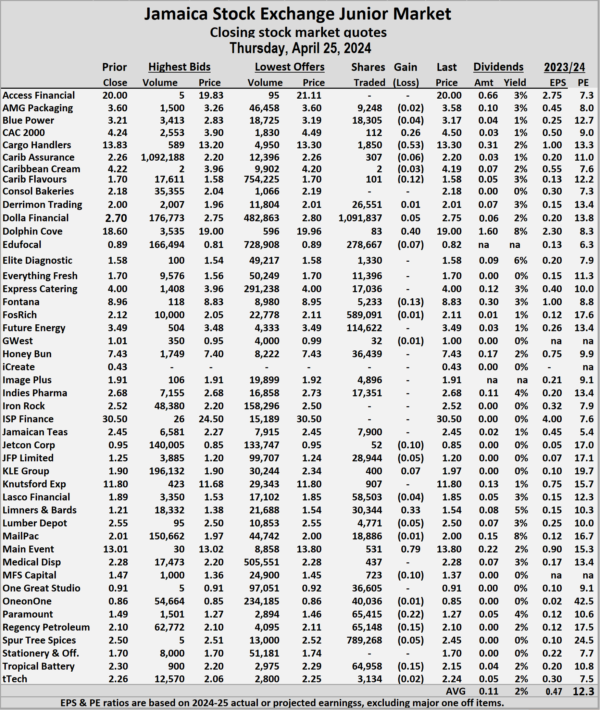

At the close, CAC 2000 added 26 cents to finish at $4.50 after 112 shares were traded, Cargo Handlers dropped by 53 cents to $13.30 with investors trading 1,850 stocks, Caribbean Assurance Brokers fell 6 cents to close at $2.20 after investors ended the trading of 307 stock units. Caribbean Flavours fell 12 cents and ended at $1.58 with a transfer of 101 stocks, Dolla Financial rose 5 cents in closing at $2.75 after trading of 1,091,837 shares, Dolphin Cove rallied 40 cents to end at $19 after 83 stocks passed through the market. EduFocal shed 7 cents in closing at a 52 weeks’ low of 82 cents with investors dealing in 278,667 units, Fontana lost 13 cents to end at $8.83 after an exchange of 5,233 stock units, Jetcon Corporation skidded 10 cents to close at 85 cents with just 52 shares crossing the market.  JFP Ltd sank 5 cents to end at $1.20 with investors trading 28,944 stocks, KLE Group increased 7 cents and ended at $1.97 with an exchange of 400 units, Limners and Bards climbed 33 cents to finish at $1.54 with 30,344 stocks passing through the market. Lumber Depot slipped 5 cents to $2.50 and closed with an exchange of 4,771 shares, Main Event popped 79 cents in closing at $13.80 with traders dealing in 531 stock units, MFS Capital Partners dipped 10 cents and ended at $1.37 in switching ownership of 723 stocks. Paramount Trading sank 22 cents to finish at $1.27 with investors swapping 65,415 units, Spur Tree Spices skidded 5 cents to end at $2.45 in an exchange of 789,268 stocks and Tropical Battery lost 15 cents to close at $2.15 in trading 64,958 units.

JFP Ltd sank 5 cents to end at $1.20 with investors trading 28,944 stocks, KLE Group increased 7 cents and ended at $1.97 with an exchange of 400 units, Limners and Bards climbed 33 cents to finish at $1.54 with 30,344 stocks passing through the market. Lumber Depot slipped 5 cents to $2.50 and closed with an exchange of 4,771 shares, Main Event popped 79 cents in closing at $13.80 with traders dealing in 531 stock units, MFS Capital Partners dipped 10 cents and ended at $1.37 in switching ownership of 723 stocks. Paramount Trading sank 22 cents to finish at $1.27 with investors swapping 65,415 units, Spur Tree Spices skidded 5 cents to end at $2.45 in an exchange of 789,268 stocks and Tropical Battery lost 15 cents to close at $2.15 in trading 64,958 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

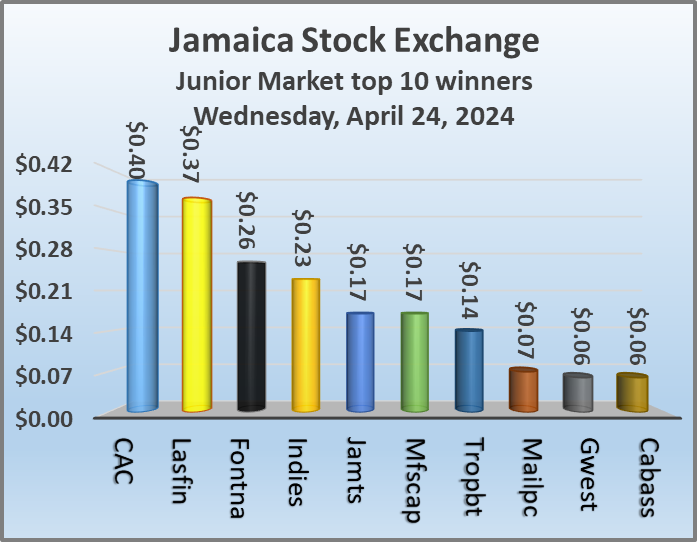

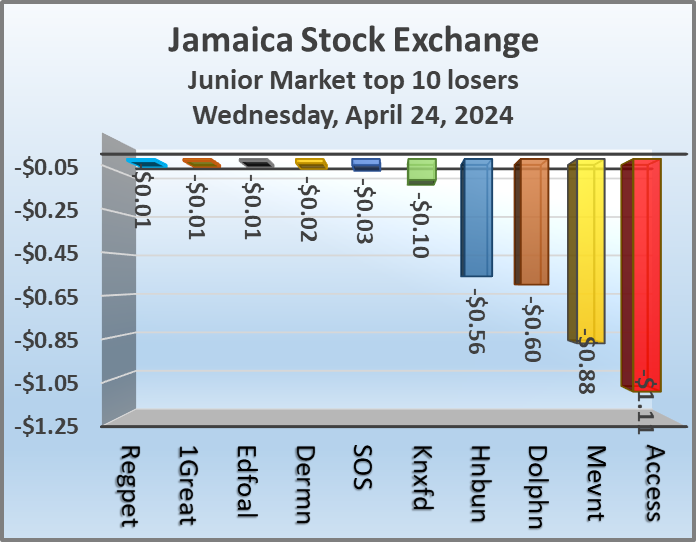

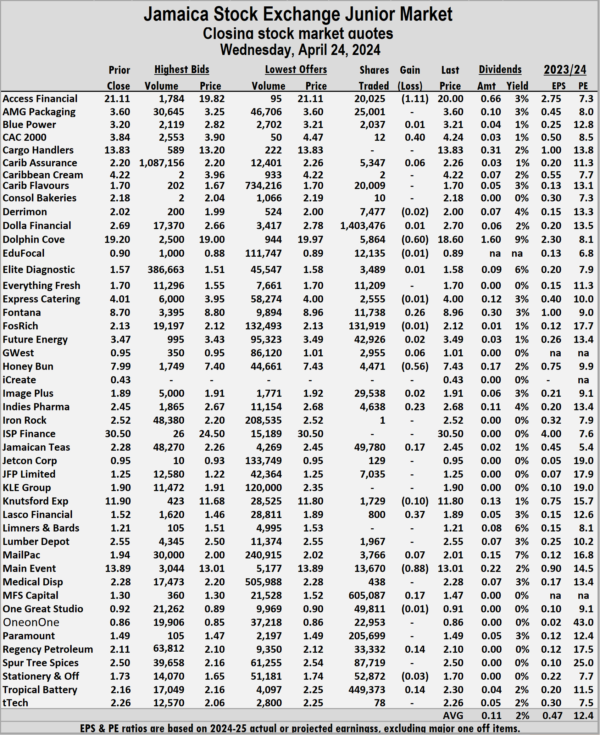

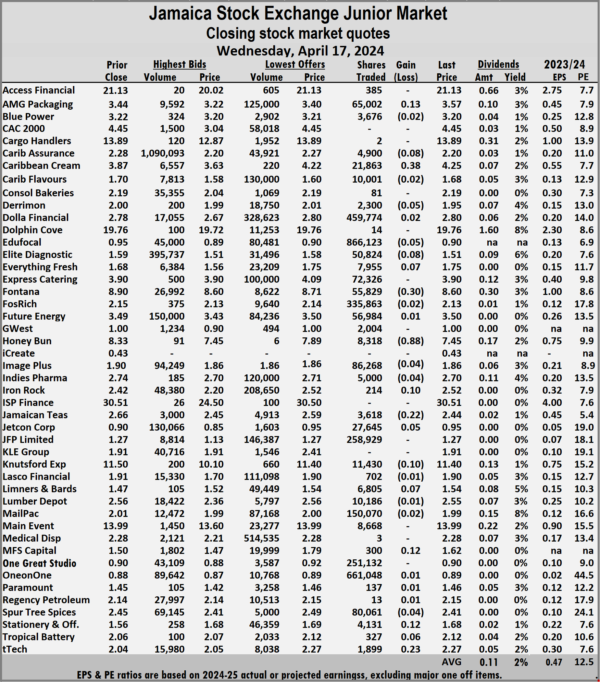

Rising Junior Market stocks beat losers

Rising Junior Market stock edged out those declining at the close of trading on the Jamaica Stock Exchange on Wednesday, with trading in 41 securities compared with 43 on Tuesday and ending with prices of 15 rising, 12 declining and 14 closing unchanged after a 33 percent decline in the volume of stocks traded, with a modest rise in value over that on Tuesday.

The market closed with trading of 3,333,072 shares with a value of $7,971,094 compared with 4,944,789 units at $7,691,275 on Tuesday.

The market closed with trading of 3,333,072 shares with a value of $7,971,094 compared with 4,944,789 units at $7,691,275 on Tuesday.

Trading averaged 81,294 shares at $194,417 compared to 114,995 units at $178,867 on Tuesday with a month to date average of 200,800 units at $445,155 compared to 207,840 stock units at $459,926 on the previous day and March averaging 221,659 units at $464,382.

Dolla Financial led trading with 1.40 million shares for 42.1 percent of total volume followed by MFS Capital Partners with 605,087 units for 18.2 percent of the day’s trade and Tropical Battery with 449,373 units for 13.5 percent market share.

The Junior Market Index increased 11.36 points to end at 3,756.20 at the close of trading.

The Junior Market ended trading with an average PE Ratio of 12.4, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

The Junior Market ended trading with an average PE Ratio of 12.4, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and two with lower offers.

At the close, Access Financial fell $1.11 to finish at $20 after a transfer of 20,025 shares, CAC 2000 popped 40 cents to $4.24 in switching ownership of 12 stocks, Caribbean Assurance Brokers increased 6 cents in closing at $2.26 with investors dealing in 5,347 shares. Dolphin Cove declined 60 cents to close at $18.60 after an exchange of 5,864 stock units, Fontana climbed 26 cents and ended at $8.96 with an exchange of 11,738 shares, GWest Corporation rose 6 cents to end at $1.01 with investors transferring 2,955 units. Honey Bun shed 56 cents in closing at $7.43 with 4,471 stocks passing through the market, Indies Pharma advanced 23 cents to $2.68 after exchanging 4,638 stock units,  Jamaican Teas gained 17 cents to close at $2.45 with 49,780 shares clearing the market. Knutsford Express sank 10 cents to end at $11.80 after investors ended trading 1,729 stock units, Lasco Financial rallied 37 cents to finish at $1.89, with just 800 units changing hands, Mailpac Group rose 7 cents and ended at $2.01 after an exchange of 3,766 stock units. Main Event dropped 88 cents to $13.01, with 13,670 units crossing the market, MFS Capital Partners advanced 17 cents after hitting an intraday 52 weeks’ low of $1.10 but ended at $1.47 with a transfer of 605,087 stocks and Tropical Battery popped 14 cents to close at $2.30 as investors exchanged 449,373 shares.

Jamaican Teas gained 17 cents to close at $2.45 with 49,780 shares clearing the market. Knutsford Express sank 10 cents to end at $11.80 after investors ended trading 1,729 stock units, Lasco Financial rallied 37 cents to finish at $1.89, with just 800 units changing hands, Mailpac Group rose 7 cents and ended at $2.01 after an exchange of 3,766 stock units. Main Event dropped 88 cents to $13.01, with 13,670 units crossing the market, MFS Capital Partners advanced 17 cents after hitting an intraday 52 weeks’ low of $1.10 but ended at $1.47 with a transfer of 605,087 stocks and Tropical Battery popped 14 cents to close at $2.30 as investors exchanged 449,373 shares.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Profits continue to send mixed signals

Early profit results for the first 2024 quarter show some positives, with the Montego Bay-based Knutsford Express reporting b revenue growth and profit for the quarter and the nine months to February, followed by positive results for AMG Packaging and Express Catering, but there were also some disappointing ones.

Knutsford Express

The directors of Knutsford Express stated that “strong and steady demand for our courier services complemented our passenger services have combined in delivering year to date profit of $268 million, up 27.1 percent from $211 million at the end of February 2023. We, therefore, recorded a 20.9 percent growth in our total revenue in this quarter moving to $565 million from $468 million in the comparative period in 2023. Similarly, our nine-month year-to-date revenue has increased by 19.5 percent from $1,281 million in 2023 to $1,530 million in 2024.”

Innovative Energy, formerly Ciboney reported no revenues in the February quarter and a loss of $4.4 million with the year to date, ending with $500,000 in income and a loss of $7.8 million.

AMG Packaging grew profit by 79 percent to $32 million from $18 million in 2023, better than the 72 percent rise in the first quarter. For the six months to February, profit was up by 79 percent to $84 million from $47 million in 2023.

Revenues climbed from US$6 million to US$7 million at Express Catering, up 17.6 percent in the quarter and increased by 23 percent from US$15 million to US$18.7 million, delivering a profit of US$2 million for the year to date and US$1 million for the latest quarter, compared with US$1.9 million for the nine months in 2023 and $1.15 million in the February 2023 quarter. Ian Dear, the company’s CEO confirmed that added cost in the third quarter would have been associated with new restaurants opened close to the quarter as such, some of the cost would not be fully covered by revenues.

The revenue at Margaritaville (Turks) rose just 5 percent to US$5.25 million for the current year, compared to US$4.98 million for the same period last year, with a net profit of US$521,909, earnings per share of 0.773 US cents compared with the similar period of 2023, with a net profit of US$1.18 million which includes non-recurring gains of US$658,000 for EPS of 1.749 US cents.

The revenue at Margaritaville (Turks) rose just 5 percent to US$5.25 million for the current year, compared to US$4.98 million for the same period last year, with a net profit of US$521,909, earnings per share of 0.773 US cents compared with the similar period of 2023, with a net profit of US$1.18 million which includes non-recurring gains of US$658,000 for EPS of 1.749 US cents.

For the third quarter, revenues fell to US$1.9 million from US$2.2 million in 2023, delivering a profit of US$222,174 versus US$725,000 in 2023 including one time income of US$340,000.

Sygnus Real Estate Finance fell by 43 percent in the February quarter from $67 million in 2023 to $44 million in 2024. For six months revenues reached $88 million down 38 percent from $142 million in the prior year. The company incurred a loss of $187 million in the 2024 second quarter 45 percent worse than the $129 million and for the six months, a loss of $320 million was incurred marginally more than $302 million in 2023.

Paramount Trading is expanding into Chlorine and bleach processing.

Paramount Trading reported reduced revenues and profit for the third quarter and the nine months. Revenues in the February quarter declined 8.5 percent from $438 million in 2023 to $401 million in 2024. For the nine months, revenues fell 23 percent from $1.63 billion down to $1.266 billion with profits coming in at 40 percent lower at $18 million for the quarter from $30 million in 2023 and 44 percent to $100 million for the nine months of February this year from $179 million in the previous year.

One On One Educational Services reported revenues of $57 million in the February quarter down 12 percent from $73 million in 2023 and fell 27 percent to $111 million for the six months to February from $153 million in 2023.

A loss of $20 million million was incurred in the February quarter down from a profit of $6 million in 2023 and a loss of $41 million for the six months, down from a profit of $17 million in 2023 for the 6 months.

Trading plunged as the Junior Market index jumps

Trading plunged on the Junior Market of the Jamaica Stock Exchange on Friday, with an 81 percent drop in the volume of stocks traded, with a 77 percent lower value than Thursday following trading in 44 securities as was the case on Thursday, with prices of 19 rising, 12 declining and 13 closing unchanged.

Trading closed with an exchange of 1,594,451 shares for $3,409,014 down sharply from 8,355,224 stock units at $15,074,942 on Thursday.

Trading closed with an exchange of 1,594,451 shares for $3,409,014 down sharply from 8,355,224 stock units at $15,074,942 on Thursday.

Trading averaged 36,238 shares at $77,478, compared with 189,891 units at $342,612 on Thursday with the month to date, averaging 217,407 units at $486,040 compared to 231,540 stock units at $517,914 on the previous day and March with an average of 221,659 units at $464,382.

Spur Tree Spices led trading with 344,879 shares for 21.6 percent of total volume followed by ONE on ONE Educational with 334,089 units for 21 percent of the day’s trade and Future Energy with 208,553 units for 13.1 percent market share.

At the close of trading, the Junior Market Index jumped 35.75 points, ending at 3,794.14.

The Junior Market ended trading with an average PE Ratio of 12.6, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows none ended with a bid higher than the last selling price and two with lower offers.

Investor’s Choice bid-offer indicator shows none ended with a bid higher than the last selling price and two with lower offers.

At the close, Access Financial popped 12 cents to end at $21.12 after a transfer of 2,053 shares, AMG Packaging gained 18 cents to close at $3.59 with 199 units crossing the market, Cargo Handlers rose 98 cents in closing at $13.83 in an exchange of 103 stocks. Caribbean Flavours rallied 9 cents and ended at $1.68 with investors swapping 10,055 stock units, Dolphin Cove dropped 26 cents to close at $19.50 with a transfer of 6,983 shares, Everything Fresh fell 18 cents to finish at $1.56 with investors trading 1,016 stock units. Honey Bun shed 10 cents to end at $8 after an exchange of 1,344 units, Image Plus popped 6 cents to end at $1.93 with 4,867 stock units clearing the market, Jamaican Teas rose 6 cents to $2.50 in trading 3 shares.  Jetcon Corporation increased 10 cents to end at 95 cents and closed after an exchange of 309 stocks, Knutsford Express sank 9 cents in closing at $11.41 after an exchange of 324 units. Lumber Depot popped 9 cents higher and ended at $2.65 with investors trading 45,776 stocks, Main Event dipped 9 cents to finish at $13.90 after an exchange of 5,640 shares. Spur Tree Spices advanced 8 cents to close at $2.50 in trading 344,879 stock units, Tropical Battery increased 5 cents to end at $2.20 with investors transferring 53,344 stocks and tTech shed 6 cents to close at $2.20 after trading 20 units.

Jetcon Corporation increased 10 cents to end at 95 cents and closed after an exchange of 309 stocks, Knutsford Express sank 9 cents in closing at $11.41 after an exchange of 324 units. Lumber Depot popped 9 cents higher and ended at $2.65 with investors trading 45,776 stocks, Main Event dipped 9 cents to finish at $13.90 after an exchange of 5,640 shares. Spur Tree Spices advanced 8 cents to close at $2.50 in trading 344,879 stock units, Tropical Battery increased 5 cents to end at $2.20 with investors transferring 53,344 stocks and tTech shed 6 cents to close at $2.20 after trading 20 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

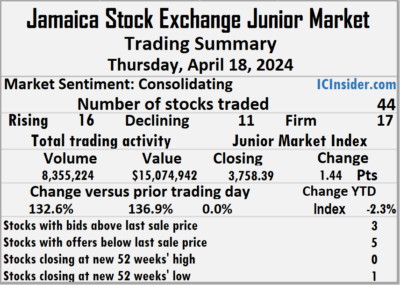

Winning stocks barely moved Junior Market

Trading climbed on the Junior Market of the Jamaica Stock Exchange on Thursday, with a 133 percent rise in the volume of stocks traded, and a 137 percent rise in value over Wednesday with trading in 44 securities compared with 42 on Wednesday and ending with prices of 16 rising, 11 declining and 17 closing unchanged.

The market closed with trading of 8,355,224 shares for $15,074,942 up from just 3,592,810 units at $6,363,318 on Wednesday.

The market closed with trading of 8,355,224 shares for $15,074,942 up from just 3,592,810 units at $6,363,318 on Wednesday.

Trading averaged 189,891 shares at $342,612, compared with 85,543 units at $151,508 on Wednesday with the month to date, averaging 231,540 units at $517,914 compared with 235,064 stock units at $532,747 on the previous day and March with an average of 221,659 units at $464,382.

Stationery and Office Supplies led trading with 4.32 million shares for 51.7 percent of total volume followed by Spur Tree Spices with 1.13 million stocks for 13.5 percent of the day’s trade and EduFocal with 733,394 units for 8.8 percent market share as the stock traded at a 52 weeks’ intraday low of 85 cents and a closing low of 90 cents.

At the close of trading, the Junior Market Index popped 1.44 points to 3,758.39.

At the close of trading, the Junior Market Index popped 1.44 points to 3,758.39.

The Junior Market ended trading with an average PE Ratio of 12.5, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and five with lower offers.

At the close, Access Financial dipped 13 cents to close at $21 after an exchange of 1,100 stock units, AMG Packaging lost 16 cents to end at $3.41, with 35,184 shares crossing the market, Cargo Handlers dropped $1.04 to finish at $12.85 with investors swapping 1,000 units. Caribbean Flavours sank 9 cents and ended at $1.59 after 2,145 stocks crossed the market,  Express Catering rose 19 cents to end at $4.09 with investors transferring 250 units, Fontana climbed 30 cents in closing at $8.90 in an exchange of 5,101 shares. Honey Bun popped 65 cents to $8.10 with investors trading 48,537 stocks, Jetcon Corporation declined 10 cents to end at 85 cents in switching ownership of 150,026 stock units, Knutsford Express advanced 10 cents in closing at $11.50 after 11,920 shares passed through the exchange and MFS Capital Partners rallied 13 cents to close at $1.75 in trading 193,271 stocks.

Express Catering rose 19 cents to end at $4.09 with investors transferring 250 units, Fontana climbed 30 cents in closing at $8.90 in an exchange of 5,101 shares. Honey Bun popped 65 cents to $8.10 with investors trading 48,537 stocks, Jetcon Corporation declined 10 cents to end at 85 cents in switching ownership of 150,026 stock units, Knutsford Express advanced 10 cents in closing at $11.50 after 11,920 shares passed through the exchange and MFS Capital Partners rallied 13 cents to close at $1.75 in trading 193,271 stocks.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Profit bolts 79% at AMG

Profit continued to surge at AMG Packaging in the February quarter, up 79 percent to $32 million from $18 million in 2023, the performance is better than the 72 percent rise in the first quarter. For the six months to February, profit was also up 79 percent to $84 million from $47 million in 2023.

Sale revenues rose by just one percent for the quarter, to $250 million from $247 million and popped 4 percent for the year to date, to $522 million from $501 million in 2023.

Sale revenues rose by just one percent for the quarter, to $250 million from $247 million and popped 4 percent for the year to date, to $522 million from $501 million in 2023.

Two main features are at play resulting in improved performance. The company installed new multi-coloured machinery in early 2023 that measures and determine the cut for boxes which has helped in cutting operating costs as it is far more efficient than the original ones. Secondly, the price of paper declined in 2023 from 2022 and has carried over into the current year, the result is that raw material costs declined to 41 percent of revenues in the second quarter from 53 percent in 2023.

Historically, profit was stuck for years between $37 million and $62 million from 2017 to 2021 . In 2022 profit jumped to $105 million following a revenues surge of 41 percent over 2021 but fell back to $89 million in 2023 with some one-off cost, helping in pushing the profit down, otherwise it would have exceeded that of 2022. ICInsider.com projects profit to come in around $225 million for this fiscal year ending in August.

Manufacturing costs declined by 12 percent in the February quarter to $154 million from $175 million and by 9 percent year to date, to $325 million from $356 million. Gross profit margin rose a significant 36 percent in the quarter to $96 million from $72 million and climbed even more for the half year to 39 percent to $197 million from $145 million in 2024.

Administrative expenses rose 18 percent to $33 million in the quarter and increased 19 percent in the six months to $66 million. Depreciation charges increased by 26 percent to $13.5 million in the quarter, and the half year to $26 million. Finance cost declined in the quarter, to $1.8 million from $2 million in 2024 and from $4.2 million to $3.6 million for the six months.

The operations generated $130 million in Gross cash flow, after paying dividends of $51 million and increased working capital needs, net flows were negative and pulled down the cash on hand from of $297 million in 2023 to $252 million.

Current assets ended the period at $651 million and include trade and other receivables of $143 million, up from $123 million in 2023, and cash and bank balances of $252 million, representing an increase over $144 million in 2023. Inventories rose a bit from $240 million to $255 million. Current liabilities at the half way marker amount to $152 million. Net current assets ended the period at $500 million.

At the end of February, shareholders’ equity amounts to $1.29 billion with long term borrowings of just at $66 million and short term at $19 million.

Earnings per share for the quarter amounts to 6 cents and 14 cents for the half year. IC Insider.com computation projects earnings around 45 cents per share for the current fiscal year, with a PE of 8 times the current year’s earnings based on the price of $3.59 the stock traded at on the Jamaica Stock Exchange Junior Market. Net asset value ended the period at $2.53 with the stock selling at a premium of 41 percent to book value.

Junior stocks drift lower

Stocks drifted lower in trading on the Junior Market of the Jamaica Stock Exchange on Wednesday, following a 16 percent rise in the volume of stocks traded, with an 8 percent higher value than Tuesday with trading in 42 securities the same as on Tuesday and ending with prices of 15 rising, 17 declining and 10 closing unchanged.

Trading netted 3,592,810 shares for $6,363,318 compared with 3,102,805 units at $5,901,970 on Tuesday.

Trading netted 3,592,810 shares for $6,363,318 compared with 3,102,805 units at $5,901,970 on Tuesday.

Trading averaged 85,543 shares at $151,508 compared with 73,876 units at $140,523 on Tuesday. Trading for the month to date averages 235,064 units at $532,747 compared to 248,202 stock units at $566,245 on the previous day and March with an average of 221,659 units at $464,382.

On a day of low trading volume, EduFocal led with 866,123 shares for 24.1 percent of total volume followed by ONE on ONE Educational with 661,048 units for 18.4 percent of the day’s trade and Dolla Financial with 459,774 units for 12.8 percent market share.

At the close of trading, the Junior Market Index declined 24.08 points to close at 3,756.95.

The Junior Market ended trading with an average PE Ratio of 12.5, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and four with lower offers.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and four with lower offers.

At the close of the market, AMG Packaging popped 13 cents to finish at $3.57 as 65,002 stock units passed through the market, Caribbean Assurance Brokers shed 8 cents in closing at $2.20 with investors exchanging 4,900 shares, Caribbean Cream increased 38 cents to end at $4.25 with 21,863 stocks clearing the market. Derrimon Trading lost 5 cents in closing at $1.95 in an exchange of 2,300 units, EduFocal dropped 5 cents to close at 90 cents with investors swapping 866,123 stocks, Elite Diagnostic sank 8 cents and ended at $1.51 with an exchange of 50,824 units. Everything Fresh climbed 7 cents to $1.75 with 7,955 shares crossing the market, Fontana skidded 30 cents to end at $8.60 as investors exchanged 55,829 stock units, Honey Bun fell 88 cents in closing at $7.45 with a transfer of 8,318 shares.  Iron Rock Insurance rose 10 cents to close at $2.52 with 214 units passing through the exchange, Jamaican Teas slipped 22 cents to finish at $2.44 in trading 3,618 stocks, Jetcon Corporation rallied 5 cents and ended at 95 cents, with 27,645 stock units changing hands. Knutsford Express declined 10 cents to $11.40 with investors transferring 11,430 shares, Limners and Bards advanced 7 cents to close at $1.54 after 6,805 units were traded, MFS Capital Partners gained 12 cents and ended at $1.62 in switching ownership of 300 stocks. Stationery and Office Supplies popped 12 cents in closing at $1.68 with trading in 4,131 stock units, Tropical Battery advanced 6 cents to finish at $2.12 with investors dealing in 327 shares and tTech rose 23 cents to end at $2.27 with 1,899 stocks crossing the market.

Iron Rock Insurance rose 10 cents to close at $2.52 with 214 units passing through the exchange, Jamaican Teas slipped 22 cents to finish at $2.44 in trading 3,618 stocks, Jetcon Corporation rallied 5 cents and ended at 95 cents, with 27,645 stock units changing hands. Knutsford Express declined 10 cents to $11.40 with investors transferring 11,430 shares, Limners and Bards advanced 7 cents to close at $1.54 after 6,805 units were traded, MFS Capital Partners gained 12 cents and ended at $1.62 in switching ownership of 300 stocks. Stationery and Office Supplies popped 12 cents in closing at $1.68 with trading in 4,131 stock units, Tropical Battery advanced 6 cents to finish at $2.12 with investors dealing in 327 shares and tTech rose 23 cents to end at $2.27 with 1,899 stocks crossing the market.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Trading slips on the Junior Market

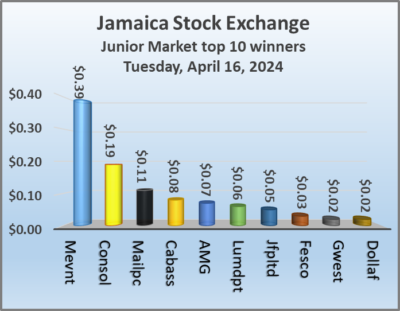

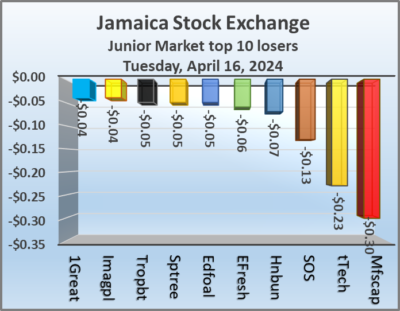

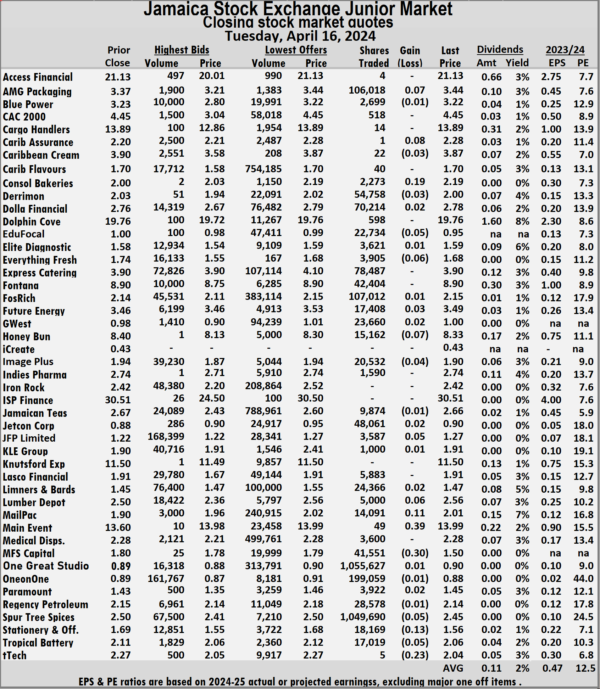

Trading closed on the Junior Market of the Jamaica Stock Exchange Tuesday, with a 35 percent decline in the volume of stocks traded with 44 percent lower value than on Monday and ended with trading in 42 securities down from 45 on Monday and closing with prices of 16 rising, 16 declining and 10 closing unchanged.

The market closed with trading in 3,102,805 shares for $5,901,970 down from 4,798,812 units at $10,594,590 on Monday.

The market closed with trading in 3,102,805 shares for $5,901,970 down from 4,798,812 units at $10,594,590 on Monday.

Trading averaged 73,876 shares at $140,523 compared to 106,640 units at $235,435 on Monday with a month to date, average of 248,202 units at $566,245 compared to 264,995 stock units at $607,255 on the previous day and March with an average of 221,659 units at $464,382.

One Great Studio led trading with 1.06 million shares for 34 percent of total volume followed by Spur Tree Spices with 1.05 million units for 33.8 percent of the day’s trade and ONE on ONE Educational with 199,059 units for 6.4 percent market share.

At the close of trading, the Junior Market Index slipped 2.92 points to finish at 3,781.03.

The Junior Market ended trading with an average PE Ratio of 12.7, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

The Junior Market ended trading with an average PE Ratio of 12.7, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and three with lower offers.

At the close, AMG Packaging advanced 7 cents to $3.44 in switching ownership of 106,018 shares, Caribbean Assurance Brokers popped 8 cents to finish at $2.28 with investors swapping just one share, Consolidated Bakeries increased 19 cents and ended at $2.19, with 2,273 shares crossing the market. EduFocal declined 5 cents to close at 95 cents with traders dealing in 22,734 stock units, Everything Fresh shed 6 cents to end at $1.68 with 3,905 shares clearing the market, Honey Bun fell 7 cents in closing at $8.33 with a transfer of 15,162 stock units.  JFP Ltd popped 5 cents to $1.27 with investors dealing in 3,587 units, Lumber Depot rose 6 cents to end at $2.56 in an exchange of 5,000 stocks, Mailpac Group rallied 11 cents in closing at $2.01 as 14,091 units passed through the market. Main Event gained 39 cents and ended at $13.99 with an exchange of 49 shares, MFS Capital Partners slipped 30 cents to finish at $1.50, with 41,551 stocks crossing the market, Spur Tree Spices lost 5 cents to close at $2.45 after a transfer of 1,049,690 stock units. Stationery and Office Supplies skidded 13 cents to $1.56 as investors exchanged 18,169 shares, Tropical Battery sank 5 cents in closing at $2.06, with 17,019 stocks changing hands and tTech dipped 23 cents to finish at $2.04 in an exchange of 5 units.

JFP Ltd popped 5 cents to $1.27 with investors dealing in 3,587 units, Lumber Depot rose 6 cents to end at $2.56 in an exchange of 5,000 stocks, Mailpac Group rallied 11 cents in closing at $2.01 as 14,091 units passed through the market. Main Event gained 39 cents and ended at $13.99 with an exchange of 49 shares, MFS Capital Partners slipped 30 cents to finish at $1.50, with 41,551 stocks crossing the market, Spur Tree Spices lost 5 cents to close at $2.45 after a transfer of 1,049,690 stock units. Stationery and Office Supplies skidded 13 cents to $1.56 as investors exchanged 18,169 shares, Tropical Battery sank 5 cents in closing at $2.06, with 17,019 stocks changing hands and tTech dipped 23 cents to finish at $2.04 in an exchange of 5 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

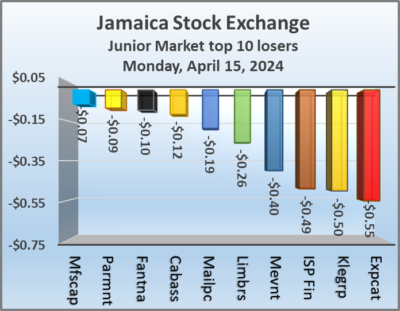

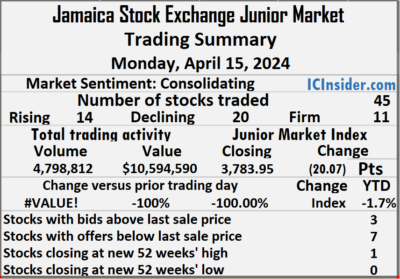

More decline for Junior Market

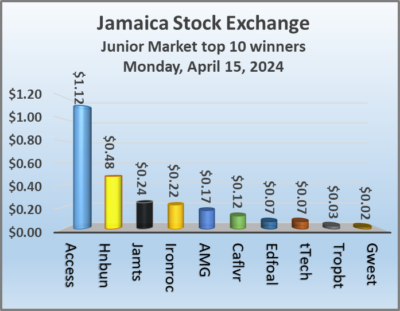

Trading closed on the Junior Market of the Jamaica Stock Exchange Monday, with a 52 percent rise in the volume of stocks traded, with 82 percent more value than Friday, with trading in 45 securities compared with 44 on Friday and ending with prices of 14 rising, 20 declining and 11 closing unchanged as Honey Bun closed at a new 52 weeks’ high and EduFocal traded at an intraday 52 weeks’ low of 90 cents.

The market closed trading of 4,798,812 shares for $10,594,590 compared with 3,153,277 units at $5,829,829 on Friday.

The market closed trading of 4,798,812 shares for $10,594,590 compared with 3,153,277 units at $5,829,829 on Friday.

Trading averaged 106,640 shares at $235,435, compared with 71,665 units at $132,496 on Friday with the month to date, averaging 264,995 units at $607,255 compared to 283,220 stock units at $650,048 on the previous day and March with an average of 221,659 units at $464,382.

Spur Tree Spices led trading with 1.47 million shares for 30.6 percent of total volume followed by EduFocal with 536,957 units for 11.2 percent of the day’s trade and Stationery and Office Supplies with 517,761 units for 10.8 percent market share.

At the close of trading, the Junior Market Index declined 20.07 points to lock up trading at 3,783.95, with indications that it could fall further on Tuesday.

The Junior Market ended trading with an average PE Ratio of 12.8, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and seven with lower offers.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and seven with lower offers.

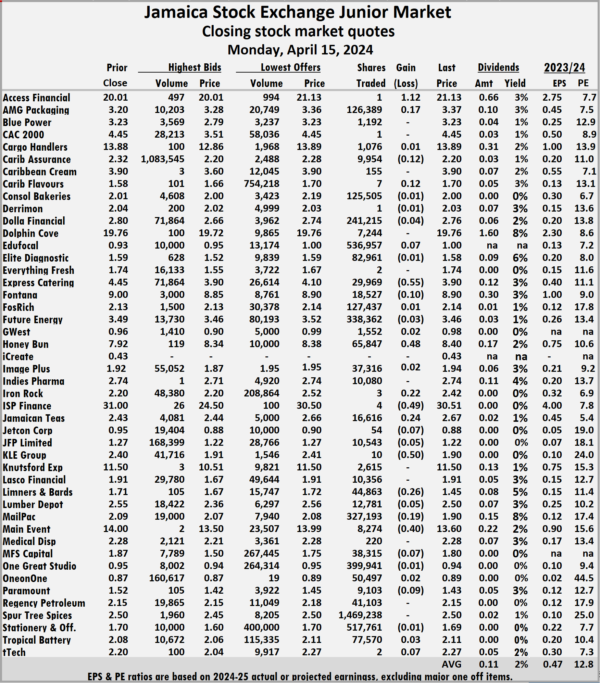

At the close, Access Financial increased $1.12 and ended at $21.13 with investors trading just one share, AMG Packaging climbed 17 cents to $3.37, with 126,389 units crossing the exchange, following the release of b six months results with profit up 79 percent, Caribbean Assurance Brokers dipped 12 cents to end at $2.20, in switching ownership of 9,954 shares. Caribbean Flavours popped 12 cents in closing at $1.70 with an exchange of 7 stock units, EduFocal rallied 7 cents to finish at $1 with traders dealing in 536,957 shares, but only after hitting an intraday 52 weeks’ low of 90 cents, Express Catering fell 55 cents to close at $3.90 after a transfer of 29,969 units, following release of increased earnings for the nine months. But with a slightly lower profit in the third quarter, Fontana shed 10 cents to $8.90 as investors exchanged 18,527 stocks, Honey Bun rose 48 cents to finish at a new 52 weeks’ high of $8.40 after 65,847 stock units passed through the market, Iron Rock Insurance gained 22 cents and ended at $2.42, with 3 shares changing hands.  ISP Finance dropped 49 cents to close at $30.51 with investors swapping 4 stocks, Jamaican Teas advanced 24 cents to end at $2.67 with a transfer of 16,616 units, Jetcon Corporation lost 7 cents in closing at 88 cents, with 54 stock units crossing the market. KLE Group skidded 50 cents to $1.90 with investors transferring 10 shares, Limners and Bards sank 26 cents to close at $1.45 with 44,863 units clearing the market, Mailpac Group declined 19 cents in closing at $1.90 after trading 327,193 stocks. Main Event slipped 40 cents and ended at $13.60, with 8,274 stock units crossing the market, MFS Capital Partners sank 7 cents to finish at $1.80 with an exchange of 38,315 shares and tTech rose 7 cents to end at $2.27 in trading 2 units.

ISP Finance dropped 49 cents to close at $30.51 with investors swapping 4 stocks, Jamaican Teas advanced 24 cents to end at $2.67 with a transfer of 16,616 units, Jetcon Corporation lost 7 cents in closing at 88 cents, with 54 stock units crossing the market. KLE Group skidded 50 cents to $1.90 with investors transferring 10 shares, Limners and Bards sank 26 cents to close at $1.45 with 44,863 units clearing the market, Mailpac Group declined 19 cents in closing at $1.90 after trading 327,193 stocks. Main Event slipped 40 cents and ended at $13.60, with 8,274 stock units crossing the market, MFS Capital Partners sank 7 cents to finish at $1.80 with an exchange of 38,315 shares and tTech rose 7 cents to end at $2.27 in trading 2 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.