Caribbean Producers surges in ICTOP 10

Caribbean Producers raced to the top of ICTOP10 listings this week after the company released full year results that showed a loss, but with the final quarter posting a profit of US$2 million before exceptional onetime cost and resulting IC Insider.com upgrading earnings from 65 cents per share to a $1.20 for the current year.

Based on years of underperformance and the knock from the closure of the hotel industry last year, many investors thought this stock was a lost cause. Based on research and understanding of the business sector, this publication had the stock the number three position on the Junior Market Top 10 list at the start of the year, just behind Caribbean Cream.  So far to October, CPJ gained 90 percent and should exceed 100 percent this coming week and Caribbean Cream is up 67 percent ahead of second quarter results due in two weeks. Another TOP 15 stock this year, Caribbean Cement, surged on Friday to close at $120 after trading at a record high of $146.12, just short of IC Insde.com forecast in April this year in the report, captioned “Carib Cement Q1 profit triples” that the stock that last traded at $75 on the Main Market of the Jamaica Stock Exchange is projected to get to $150 in the next twelve months.

So far to October, CPJ gained 90 percent and should exceed 100 percent this coming week and Caribbean Cream is up 67 percent ahead of second quarter results due in two weeks. Another TOP 15 stock this year, Caribbean Cement, surged on Friday to close at $120 after trading at a record high of $146.12, just short of IC Insde.com forecast in April this year in the report, captioned “Carib Cement Q1 profit triples” that the stock that last traded at $75 on the Main Market of the Jamaica Stock Exchange is projected to get to $150 in the next twelve months.

While the Jamaican stock markets continued to bounce around, the past week saw clearer signs of the upward momentum returning, with the Barita Investments APO issue out of the way. Bank of Jamaica’s raise its overnight rate to 1.5 percent from 0.50 percent and the tightening of the financial market continued with CD rates averaging 2.59 percent during the past week.

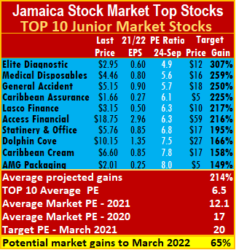

Elsewhere, in the Junior Market, AMG Packaging fell from $2.10 to $1.70, Stationery and Office Supplies rose from $5.76 from $6.49, Access Financial rose from $18.75 to $20, General Accident rose from $5.15 last week to $5.45, Medical Disposables rose from $4.46 to $5.15, Caribbean Assurance fell from $1.80 to $1.66 and Caribbean Cream moved up to $7 from $6.60 last week. In the Main Market, Caribbean Producers rose from $4.65 to $5.50 on Friday.

Elsewhere, in the Junior Market, AMG Packaging fell from $2.10 to $1.70, Stationery and Office Supplies rose from $5.76 from $6.49, Access Financial rose from $18.75 to $20, General Accident rose from $5.15 last week to $5.45, Medical Disposables rose from $4.46 to $5.15, Caribbean Assurance fell from $1.80 to $1.66 and Caribbean Cream moved up to $7 from $6.60 last week. In the Main Market, Caribbean Producers rose from $4.65 to $5.50 on Friday.

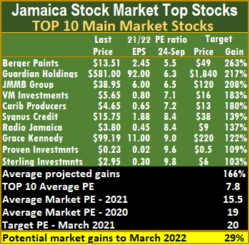

The top three Main Market stocks are Caribbean Producers, Berger Paints, followed by Guardian Holdings, with expected gains of 216 to 336 percent for the three, versus last weeks’ 208 to 263 percent.

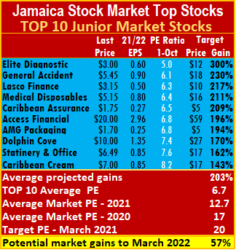

The top three stocks in the Junior Market are Elite Diagnostic, followed by General Accident and Lasco Financial. All three have the potential to gain between 217 and 300 percent, from 250 percent and 307 percent last week.

This past week, the average gains projected for the TOP 10 Junior Market stocks moved from 214 percent to 203 percent and Main Market stocks moved from 166 percent to 180 percent.

This past week, the average gains projected for the TOP 10 Junior Market stocks moved from 214 percent to 203 percent and Main Market stocks moved from 166 percent to 180 percent.

The Junior Market closed the week with an average PE 12.7 based on ICInsider.com’s 2021-22 earnings and currently trades well below the target of 20 and the historical average of 17 for the period to March this year, based on 2020 earnings. The TOP 10 stocks trade at a PE of 6.7, with a 53 percent discount to that market’s PE. The overall Junior Market can gain 57 percent to March next year, based on an average PE of 20 and 34 percent based on an average PE of 17.

The JSE Main Market ended the week with an overall PE of 15.7, a little distance from 19 the market ended at in March, suggesting a 27 percent rise at a PE of 19 and 21 percent at a PE of 20 from now to March 2022. The Main Market TOP 10 trades at a PE of 7.6, with a 49 percent discount to the PE of that market, well off the potential of 20.

ICTOP10 is not intended to be a selection of the best stocks in the market but the most likely to be the biggest winners within fifteen months. ICInsider.com ranks stocks to separate the bigger winners from the rest, allowing investors to focus on potentially huge gains, helping to keep out emotional attachments to stocks that often result in the making of costly mistakes.

ICTOP10 is not intended to be a selection of the best stocks in the market but the most likely to be the biggest winners within fifteen months. ICInsider.com ranks stocks to separate the bigger winners from the rest, allowing investors to focus on potentially huge gains, helping to keep out emotional attachments to stocks that often result in the making of costly mistakes.

IC TOP10 stocks are likely to deliver the best returns up to March 2022 and ranked in order of potential gains, based on possible increases for each company, considering the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in weekly movements in and out of the lists. Revisions to earnings per share are ongoing, based on receipt of new information.

Persons who compiled this report may have an interest in securities commented on in this report.

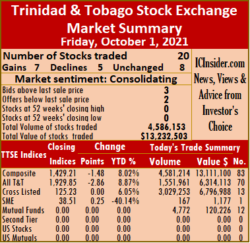

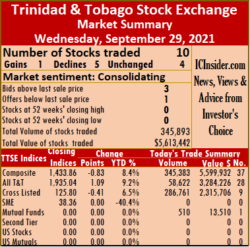

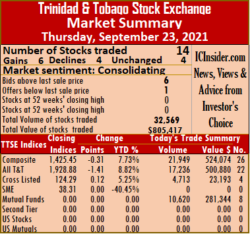

At the close, 20 securities traded compared to 18 on Thursday, with seven rising, five declining and eight remaining unchanged. The Composite Index dipped 1.48 points to 1,429.21, the All T&T Index lost 2.86 points to end at 1,929.85 and the Cross-Listed Index ended at 125.23.

At the close, 20 securities traded compared to 18 on Thursday, with seven rising, five declining and eight remaining unchanged. The Composite Index dipped 1.48 points to 1,429.21, the All T&T Index lost 2.86 points to end at 1,929.85 and the Cross-Listed Index ended at 125.23. Guardian Media remained at $3.01 while trading 1,485,184 stocks, JMMB Group closed at $2.22 in switching ownership of 3,011,424 units, Massy Holding jumped 50 cents in closing at $83, with 2,523 shares clearing the market. National Enterprises fell 9 cents to $3.20, with 1,496 shares crossing the market, National Flour Mills ended at $1.90 after trading 5,000 stock units, Prestige Holdings remained at $7, with 150 stocks crossing the market. Republic Financial Holdings traded 204 units at $135.76, Scotiabank dropped $1.50 in closing at $60.50 after switching ownership of 2,955 stock units, Trinidad & Tobago NGL remained unchanged at $17.40, with 2,500 stocks crossing the exchange. Trinidad Cement rose 4 cents to $4 with the swapping of 10,550 units and West Indian Tobacco gained 1 cent to close at $30.95 with 23,164 shares changing hands.

Guardian Media remained at $3.01 while trading 1,485,184 stocks, JMMB Group closed at $2.22 in switching ownership of 3,011,424 units, Massy Holding jumped 50 cents in closing at $83, with 2,523 shares clearing the market. National Enterprises fell 9 cents to $3.20, with 1,496 shares crossing the market, National Flour Mills ended at $1.90 after trading 5,000 stock units, Prestige Holdings remained at $7, with 150 stocks crossing the market. Republic Financial Holdings traded 204 units at $135.76, Scotiabank dropped $1.50 in closing at $60.50 after switching ownership of 2,955 stock units, Trinidad & Tobago NGL remained unchanged at $17.40, with 2,500 stocks crossing the exchange. Trinidad Cement rose 4 cents to $4 with the swapping of 10,550 units and West Indian Tobacco gained 1 cent to close at $30.95 with 23,164 shares changing hands.

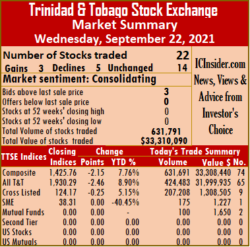

Massy Holdings fell 50 cents to $82.50, with 80 stock units crossing the exchange, National Enterprises traded 525 units at $3.29, National Flour Mills ended at $1.90 with the swapping of 1,046 shares. One Caribbean Media dropped 4 cents to close at $4.26, with 2,500 stock units crossing the market, Prestige Holdings closed at $7, with 1,045 units changing hands, Republic Financial Holdings dipped 66 cents to $135.76 with an exchange of 1,780 stocks. Scotiabank rose $1.75 to end at $62 after trading 7,420 shares, Trinidad & Tobago NGL remained at $17.40, with 8,126 shares crossing the exchange and Unilever Caribbean declined 2 cents to close at $16.20 after 2,077 stocks cleared the market.

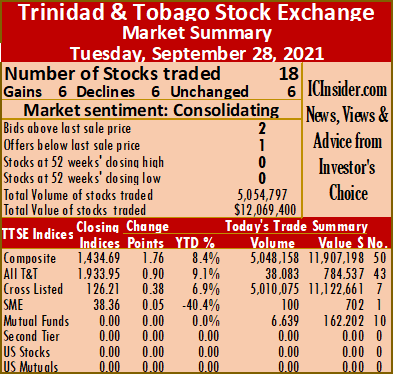

Massy Holdings fell 50 cents to $82.50, with 80 stock units crossing the exchange, National Enterprises traded 525 units at $3.29, National Flour Mills ended at $1.90 with the swapping of 1,046 shares. One Caribbean Media dropped 4 cents to close at $4.26, with 2,500 stock units crossing the market, Prestige Holdings closed at $7, with 1,045 units changing hands, Republic Financial Holdings dipped 66 cents to $135.76 with an exchange of 1,780 stocks. Scotiabank rose $1.75 to end at $62 after trading 7,420 shares, Trinidad & Tobago NGL remained at $17.40, with 8,126 shares crossing the exchange and Unilever Caribbean declined 2 cents to close at $16.20 after 2,077 stocks cleared the market. The Composite Index dipped 0.83 points to 1,433.86, the All T&T Index gained 1.09 points to settle at 1,935.04 and the Cross-Listed Index fell 0.41 points to 125.80.

The Composite Index dipped 0.83 points to 1,433.86, the All T&T Index gained 1.09 points to settle at 1,935.04 and the Cross-Listed Index fell 0.41 points to 125.80. At the close, Agostini’s remained at $24.50 after trading 150 shares, Clico Investment Fund dipped 1 cent to $26.49 in an exchange of 510 units, First Citizens Bank fell 1 cent to $50.55 after finishing trading of 1,150 stocks. GraceKennedy lost 4 cents to end at $6.26, with 25,548 stock units changing hands, Guardian Holdings popped 10 cents to $32.85 after trading 270 stocks, Massy Holdings remained unchanged at $83 in trading 30 stock units. National Enterprises ended at $3.29 after 30 shares crossed the market, NCB Financial Group slipped 5 cents to $8.25, with 261,213 units crossing the exchange, Scotiabank shed 30 cents to close at $60.25 after exchanging 51,200 units and Trinidad & Tobago NGL closed at $17.40, with 5,792 shares changing hands.

At the close, Agostini’s remained at $24.50 after trading 150 shares, Clico Investment Fund dipped 1 cent to $26.49 in an exchange of 510 units, First Citizens Bank fell 1 cent to $50.55 after finishing trading of 1,150 stocks. GraceKennedy lost 4 cents to end at $6.26, with 25,548 stock units changing hands, Guardian Holdings popped 10 cents to $32.85 after trading 270 stocks, Massy Holdings remained unchanged at $83 in trading 30 stock units. National Enterprises ended at $3.29 after 30 shares crossed the market, NCB Financial Group slipped 5 cents to $8.25, with 261,213 units crossing the exchange, Scotiabank shed 30 cents to close at $60.25 after exchanging 51,200 units and Trinidad & Tobago NGL closed at $17.40, with 5,792 shares changing hands. Guardian Holdings ended at $32.75, with 455 stock units crossing the market, Guardian Media popped 1 cent to close at $3.01 in trading 3,397 shares, JMMB Group held at $2.22 trading 5,010,040 stocks. Massy Holdings increased 99 cents in closing at $83 while exchanging two stock units, National Enterprises climbed 4 cents to $3.29, with 55 units clearing the market, National Flour Mills remained at $1.90 after 671 shares crossed the exchange. NCB Financial Group gained 5 cents in ending at $8.30, with 35 stock units changing hands, Scotiabank remained at $60.55, with 1,139 stocks crossing the market, Trinidad & Tobago NGL dropped 10 cents to end at $17.40 after exchanging 5,071 units. Trinidad Cement fell 4 cents to $3.96 with the swapping of 12,670 shares, Unilever Caribbean was unchanged at $16.22 with an exchange of 4,000 stocks and West Indian Tobacco dropped 5 cents in closing at $30.94 trading 210 stock units.

Guardian Holdings ended at $32.75, with 455 stock units crossing the market, Guardian Media popped 1 cent to close at $3.01 in trading 3,397 shares, JMMB Group held at $2.22 trading 5,010,040 stocks. Massy Holdings increased 99 cents in closing at $83 while exchanging two stock units, National Enterprises climbed 4 cents to $3.29, with 55 units clearing the market, National Flour Mills remained at $1.90 after 671 shares crossed the exchange. NCB Financial Group gained 5 cents in ending at $8.30, with 35 stock units changing hands, Scotiabank remained at $60.55, with 1,139 stocks crossing the market, Trinidad & Tobago NGL dropped 10 cents to end at $17.40 after exchanging 5,071 units. Trinidad Cement fell 4 cents to $3.96 with the swapping of 12,670 shares, Unilever Caribbean was unchanged at $16.22 with an exchange of 4,000 stocks and West Indian Tobacco dropped 5 cents in closing at $30.94 trading 210 stock units. Investor’s Choice bid-offer indicator flashed a short-term bullish signal, with seven stocks ending with bids higher than their last selling prices and only two with lower offers.

Investor’s Choice bid-offer indicator flashed a short-term bullish signal, with seven stocks ending with bids higher than their last selling prices and only two with lower offers. At the close, Agostini’s traded 80 shares at $24.55, Clico Investment Fund ended at $26.57 while exchanging 4,153 stocks, First Citizens Bank rose 23 cents to $50.74 after trading ten stock units. GraceKennedy remained at $6.30 with 37,000 units clearing the market, Guardian Holdings closed at $32.75 after exchanging 250 shares, JMMB Group popped 2 cents to $2.22, with an exchange of 20,060 stocks. Massy Holdings inched 1 cent higher to $82.01 in an exchange of 13,849 stock units, NCB Financial Group rose 19 cents to $8.25 after finishing trading of 157,000 units, Republic Financial Holdings dropped $2.08 to $136.42 in trading 2,310 stock units. Scotiabank gained 75 cents to close at $60.55, with 242 stocks crossing the exchange, Trinidad & Tobago NGL popped 75 cents to $17.50 after exchanging 4,129 shares and West Indian Tobacco remained at $30.99 in switching ownership of 1,109 units.

At the close, Agostini’s traded 80 shares at $24.55, Clico Investment Fund ended at $26.57 while exchanging 4,153 stocks, First Citizens Bank rose 23 cents to $50.74 after trading ten stock units. GraceKennedy remained at $6.30 with 37,000 units clearing the market, Guardian Holdings closed at $32.75 after exchanging 250 shares, JMMB Group popped 2 cents to $2.22, with an exchange of 20,060 stocks. Massy Holdings inched 1 cent higher to $82.01 in an exchange of 13,849 stock units, NCB Financial Group rose 19 cents to $8.25 after finishing trading of 157,000 units, Republic Financial Holdings dropped $2.08 to $136.42 in trading 2,310 stock units. Scotiabank gained 75 cents to close at $60.55, with 242 stocks crossing the exchange, Trinidad & Tobago NGL popped 75 cents to $17.50 after exchanging 4,129 shares and West Indian Tobacco remained at $30.99 in switching ownership of 1,109 units.

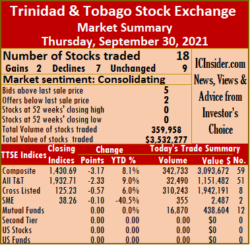

Elsewhere, in the Junior Market, Stationery and Office Supplies pulled back to $5.76 from $6.60 at the end of the prior week. Access Financial fell to $18.75 from $21.49 last week, General Accident fell from $5.54 last week to $5.15, Medical Disposables slipped from $4.94 to $4.46, Caribbean Assurance fell from $1.80 to $1.66 and Caribbean Cream moved up to $6.60, from $6.05 last week.

Elsewhere, in the Junior Market, Stationery and Office Supplies pulled back to $5.76 from $6.60 at the end of the prior week. Access Financial fell to $18.75 from $21.49 last week, General Accident fell from $5.54 last week to $5.15, Medical Disposables slipped from $4.94 to $4.46, Caribbean Assurance fell from $1.80 to $1.66 and Caribbean Cream moved up to $6.60, from $6.05 last week. The top three Main Market stocks are Berger Paints, followed by Guardian Holdings and JMMB Group, with expected gains of 208 to 263 percent for the three, versus last weeks’ 212 to 257 percent.

The top three Main Market stocks are Berger Paints, followed by Guardian Holdings and JMMB Group, with expected gains of 208 to 263 percent for the three, versus last weeks’ 212 to 257 percent. The TOP 10 stocks trade at a PE of 6.5, with a 54 percent discount to that market’s PE. The overall Junior Market can gain 65 percent to March next year, based on an average PE of 20 and 40 percent based on an average PE of 17.

The TOP 10 stocks trade at a PE of 6.5, with a 54 percent discount to that market’s PE. The overall Junior Market can gain 65 percent to March next year, based on an average PE of 20 and 40 percent based on an average PE of 17. ICTOP10 is a selection of stocks that are more likely to be the great winners within fifteen months and not necessarily the best in the market. ICInsider.com ranks stocks to separate the big winners from the rest, allowing investors to focus on potentially huge gains, helping to keep out an emotional attachment to stocks that often result in costly mistakes.

ICTOP10 is a selection of stocks that are more likely to be the great winners within fifteen months and not necessarily the best in the market. ICInsider.com ranks stocks to separate the big winners from the rest, allowing investors to focus on potentially huge gains, helping to keep out an emotional attachment to stocks that often result in costly mistakes. Closing prices are flashing signs of a near term rally, with stocks closing with bids higher than last selling prices outpacing those with lower offers, while some prices are sitting at 52 weeks’ highs.

Closing prices are flashing signs of a near term rally, with stocks closing with bids higher than last selling prices outpacing those with lower offers, while some prices are sitting at 52 weeks’ highs. At the close, Agostini’s rallied 15 cents to $24.55, with 4,835 shares clearing the market, Ansa McAl spiked 79 cents to $57.80 after 2,015 stock units crossed the market, Ansa Merchant Bank rose $1.09 to end at $41.50 while exchanging 124 units. Calypso Macro Investment Fund fell 30 cents to $16.20 with 80 stocks changing hands, Clico Investment Fund remained at $26.57 with the swapping of 10,540 units, First Citizens Bank popped 1 cent to $50.51 in exchanging 1,000 shares. GraceKennedy spiked 5 cents to end at $6.30 with an exchange of 3,128 stock units, Guardian Holdings dropped 20 cents after finishing at $32.75 in trading 1,000 stocks, JMMB Group remained at $2.20 in an exchange of 1,585 units. Massy Holdings shed 1 cent to close at $82 after exchanging 46 stocks, National Flour Mills finished at $1.90 in exchanging 1,000 shares, One Caribbean Media closed at $4.30 after the trading of 260 stock units. Republic Financial Holdings spiked $3.05 to $138.50 in switching ownership of 450 stock units and Trinidad & Tobago NGL lost 26 cents in closing at $16.75, with 6,506 shares changing hands.

At the close, Agostini’s rallied 15 cents to $24.55, with 4,835 shares clearing the market, Ansa McAl spiked 79 cents to $57.80 after 2,015 stock units crossed the market, Ansa Merchant Bank rose $1.09 to end at $41.50 while exchanging 124 units. Calypso Macro Investment Fund fell 30 cents to $16.20 with 80 stocks changing hands, Clico Investment Fund remained at $26.57 with the swapping of 10,540 units, First Citizens Bank popped 1 cent to $50.51 in exchanging 1,000 shares. GraceKennedy spiked 5 cents to end at $6.30 with an exchange of 3,128 stock units, Guardian Holdings dropped 20 cents after finishing at $32.75 in trading 1,000 stocks, JMMB Group remained at $2.20 in an exchange of 1,585 units. Massy Holdings shed 1 cent to close at $82 after exchanging 46 stocks, National Flour Mills finished at $1.90 in exchanging 1,000 shares, One Caribbean Media closed at $4.30 after the trading of 260 stock units. Republic Financial Holdings spiked $3.05 to $138.50 in switching ownership of 450 stock units and Trinidad & Tobago NGL lost 26 cents in closing at $16.75, with 6,506 shares changing hands. Guardian Media rallied 36 cents to $3, with 155 stock units changing hands, JMMB Group dropped 2 cents to $2.20 after exchanging 500 shares, L.J Williams B share remained at $1.50 in switching ownership of 50 stocks. Massy Holdings shed 9 cents to $82.01 with 371,891 stock units clearing the market, National Enterprises ended at $3.25 after trading 976 units, National Flour Mills remained at $1.90 with an exchange of 5,948 shares. NCB Financial Group declined 11 cents to $8.06, with 8,000 stocks crossing the market, One Caribbean Media closed to $135.45 after trading 424 units. Scotiabank fell $1.20 to $59.80 with the swapping of 4,066 shares, Trinidad & Tobago NGL remained at $17.01 after exchanging 8,000 stocks, Trinidad Cement traded 550 shares at $4 and West Indian Tobacco closed at $30.99 in trading 10,730 stocks.

Guardian Media rallied 36 cents to $3, with 155 stock units changing hands, JMMB Group dropped 2 cents to $2.20 after exchanging 500 shares, L.J Williams B share remained at $1.50 in switching ownership of 50 stocks. Massy Holdings shed 9 cents to $82.01 with 371,891 stock units clearing the market, National Enterprises ended at $3.25 after trading 976 units, National Flour Mills remained at $1.90 with an exchange of 5,948 shares. NCB Financial Group declined 11 cents to $8.06, with 8,000 stocks crossing the market, One Caribbean Media closed to $135.45 after trading 424 units. Scotiabank fell $1.20 to $59.80 with the swapping of 4,066 shares, Trinidad & Tobago NGL remained at $17.01 after exchanging 8,000 stocks, Trinidad Cement traded 550 shares at $4 and West Indian Tobacco closed at $30.99 in trading 10,730 stocks.

Shocking 4 years of Cargo Handlers errors

The number of shares issued by publicly listed companies is very important information for investors to know, but investors would not think so when examining interim financial statements in Jamaica and Trinidad and Tobago of some of the companies.

There have been so many occasions one has to search high and low to find it if at all it is reported in the interim numbers. This is such a simple matter and the stock exchanges in the region could cure it easily, by making it one of the items that must be included in quarterly reports. It should be included as a part of the statement of movement in Shareholders’ equity.

There have been so many occasions one has to search high and low to find it if at all it is reported in the interim numbers. This is such a simple matter and the stock exchanges in the region could cure it easily, by making it one of the items that must be included in quarterly reports. It should be included as a part of the statement of movement in Shareholders’ equity.

Take the matter of segment reporting. Some companies report it quarterly and some only annually. Most correctly report the current period and the comparative previous year’s period. Why can’t the JSE insist on some minimum standards for the benefit of investors so they get information consistently? Limners and Bards is the latest company to provide a quarterly report with no segment results yet they report it in the audited report albeit just one year forcing investors to have to go back to the previous year’s report for the comparison. Seems if that is the approach they should just report the current year’s figures and let investors go back to the previous year’s reports for profit and balance sheet information.

Take the matter of segment reporting. Some companies report it quarterly and some only annually. Most correctly report the current period and the comparative previous year’s period. Why can’t the JSE insist on some minimum standards for the benefit of investors so they get information consistently? Limners and Bards is the latest company to provide a quarterly report with no segment results yet they report it in the audited report albeit just one year forcing investors to have to go back to the previous year’s report for the comparison. Seems if that is the approach they should just report the current year’s figures and let investors go back to the previous year’s reports for profit and balance sheet information.

Communication with investors is a subjective matter but there are some simple matters that it just takes some thinking or consulting to get right.

Communication with investors is a subjective matter but there are some simple matters that it just takes some thinking or consulting to get right.

The latest shocking reporting is that of Cargo Handlers that shows the number of shares issued as a part of the statement of shareholders’ equity. The oddity is the company reporting only 37.466 million issued shares since 2018 when it increased to more than 374 million units. The Jamaica Stock Exchange website shows them as having 416.25 million shares issued and the audited accounts show that the change took place in 2018 the numbers moving from 37.485 to 374.653 million shares. One wonders why no one discovered this glaring error when the list of top 10 shareholders show four of them having more shares than what they list as issued. The error goes back to 2018 for all of the quarterly reports.

This is such a glaring error and neither the Stock Exchange, the Financial Services Commission the directors of the company or its accounting staff have found out.

Our reporting standards are not up to scratch and some persons in the financial system love to talk about best practices globally.

The vast majority of listed companies report profit results with direct and indirect costs and gross profit. But others do not. The group shockingly includes GraceKennedy, 138 Student Living, Knutsford Express. It is full time that companies lift the standard of reporting so that investors can get pertinent information to use in their investment decision making. In response to a question put to Don Wehby about the bulking of all cost on the profit statement suggest that they are in compliance with accounting standards, but that is such a lame and shocking excuse from a company of such standing in the country. Seprod produces it, Jamaica Broilers does it and several other listed companies so why not Grace. Are grace directors suggesting that their shareholders are lesser persons than those of other companies? The case of 138 Student Living is shocking when one considers that the Chairman, Ian Parsard is also Group Senior Vice President – Finance & Corporate Planning at Jamaica Broilers.

AMG Packaging is in a class by itself when it comes to poor communication. The company has embarked on a major capital project, but the directors appear to be of the view that minority shareholders are best kept in as much darkness as possible about it. The audited accounts for 2020 are silent on any commitment to the project.

The latest quarterly the only capital spend, is shown as work in progress on the balance sheet in the amount of $57 million, with no comments on the progress, the total commitment and when it is expected to be complete and be in use. Worse there are no comments on its use. It is noted that the purpose has moved from a warehouse to a factory between 2018 and now.

In the 2018 annual report, the Chairman stated that “the Company recently took an option to purchase an adjoining property. If the transaction is completed, the additional space will be used to alleviate some of the space constraints in the existing facility, making operations more efficient.”

In the 2019 annual report “The Company completed the acquisition on the property at 12 Retirement Crescent which will allow us to expand our operations and to better serve our customers.” The company also stated that they “obtained funding from Proven Wealth Limited to assist with the development of 12 Retirement Crescent. The KSAC is in the process of reviewing the architectural drawings for 12 Retirement.”

The 2020 annual report states, “the company plans on utilizing the strong cash and cash equivalents position into developing 12 Retirement Crescent. The pandemic had caused the development of 12 Retirement Crescent to delay from 2020 to 2021. A contractor has been chosen and the building of an additional 11,370 square feet is set to begin in February 2021.”

In the results to February this year, the only comment made about the development is “that the new steel frame warehouse purchased from China arrived and construction commenced. The financial statement shows WIP at $49 million, with a zero balance in the November quarter.”