Profit at Jamaican Teas for the 2015 fiscal year to September rose 60 percent to $81 Million from a 17 percent increase in revenues of $1.3 billion and from a 32 percent rise in exports to $370 Million.

Profit at Jamaican Teas for the 2015 fiscal year to September rose 60 percent to $81 Million from a 17 percent increase in revenues of $1.3 billion and from a 32 percent rise in exports to $370 Million.

Export sales exceeded domestic sales from the manufacturing arm that ended at $363 million for a 6 percent increase for the year.

In the final quarter, net profit increased by 520 percent to $12 million from a loss in 2014 and $15.6 million after other comprehensive income. For the full year total comprehensive income amounted to $97 million compared to $46 million in 2014. The company incurred some one-off costs that are not likely to recur in 2016 and should help in contributing to increased profit.

The group operates two supermarkets, one in Kingston and one in Savanna-la-Mar with sales of $520 million for the year compared to $491 Million in 2014. The jointly owned supermarket in Montego have been challenging in a tight but competitive Montego Bay economy.

June marks the end of the tax free status of Jamaican Teas. Accordingly, the company became subject to income tax, effectively at 12.5 percent commencing in the fourth quarter of the 2015 financial year and continuing for another 4 years and nine months.

The company said they completed construction of 29 two bedroom units along with infrastructure work during the fiscal year, with all units being sold, with the majority of sales to be booked in the new fiscal year. The company expects that the net proceeds of sales will be used to pay down loans, pay a dividend to shareholders and finance Phase II of the development of which there are several commitments for.

Outlook|The company is expecting another year of good performance in 2016, in line with this, the 2016 financial year has started off on a favourable note with strong interest shown in units in phase 2 of real estate development. The expected completion of the sale of all units in phase 1 are of real estate development, good export sale orders so far. The electioneering ahead of the general elections could bring increased consumer spending and positive development in the tourism sector with the expectation of a strong tourist arrivals in 2016 could see the company benefitting. Jamaican Teas also holds a portfolio of equities that has increased in value with the 2015 results shows with an increased value of $16 million, that amount would have grown with the growth in the Jamaican Stock market since the year end.

Outlook|The company is expecting another year of good performance in 2016, in line with this, the 2016 financial year has started off on a favourable note with strong interest shown in units in phase 2 of real estate development. The expected completion of the sale of all units in phase 1 are of real estate development, good export sale orders so far. The electioneering ahead of the general elections could bring increased consumer spending and positive development in the tourism sector with the expectation of a strong tourist arrivals in 2016 could see the company benefitting. Jamaican Teas also holds a portfolio of equities that has increased in value with the 2015 results shows with an increased value of $16 million, that amount would have grown with the growth in the Jamaican Stock market since the year end.

The company is primarily involved in the processing of local teas and packaging along with imported teas and for the Jamaican and overseas markets, operates supermarkets, and the rental and development of realty. The company’s shares are listed on the Jamaica Stock Exchange, last traded at $3.85.

Profit up 60% at Jamaican Teas

Point Lisas remains undervalued

Point Lisas is headquartered in Trinidad, is listed on the country’s stock exchange, last traded at $3.90 and is an undervalued stock with earnings per share including gains on property of $1.85 for the nine months to September this year.

Point Lisas is headquartered in Trinidad, is listed on the country’s stock exchange, last traded at $3.90 and is an undervalued stock with earnings per share including gains on property of $1.85 for the nine months to September this year.

Profit before tax of Point Lisas Industrial Port Development (Point Lisas) for the period to September, excluding fair value gains on property, amounts to $20.4 million an increase of 181 percent over $112,000 for the same period for 2014. Gross profit climbed sharply by 29 percent to $51 million in the third quarter from $40 million in 2014 and for the nine months, an increase of 12.66 percent from $134 million to $151 million.

For the September quarter, profit after tax moved from a loss of $14 million to a surplus of $14 million including fair value gains on property of $10.6 million and fair value loss of $4.7 million in the 2014 quarter. For the year to September, fair value gains on property amount to $58 million for 2015 and $91 million in 2014.

Revenues grew by 10 percent for the nine months to September compared to the period to September 2014. Cash flow from operations amounts to $31 million and is up from $13 million in 2014, leading to cash and equivalent of $60 million at the end of the 2015 period. Administrative and other cost declined moderately by $5 million for the quarter and for the nine months.

According to management in their report to shareholders, the increase in revenue was heavily influenced by containerized cargo operations which experienced a 15 percent increase in throughput over the same period in 2014. The data showed a 4 percent increase in imports, an 8 percent increase in exports and a 60 percent increase in trans-shipment cargo. General cargo experienced a 10 percent decline due to an 88 percent decrease in exports, a 1 percent increase in imports and a 4 percent increase in trans-shipment.

Total assets climbed to $2.28 billion in the third quarter 2015, equity capital amounts to $1.97 billion, borrowed funds amount to $125 million, while current assets stood at $121 million and current liabilities at $52 million.

“In the second and third quarters, PLIPDECO provided bunkering services as part of its service and revenue expansion drive. During the fourth quarter, the Corporation intends to continue with infrastructural improvements, information technology upgrades and move steadfastly with the Port upgrade project. The future outcome of these undertakings would further enhance productivity, overall efficiency of Port Operations and ultimately boost profitability,” Ian R. H. Atherly, Chairman of the company said in a release accompanying the financials.

Grace grows Q3 profit 7%

Revenues for Grace Kennedy rose a strong 14.4 percent in the nine months to September, this year, to $59.7 billion from $52.2 billion generated in the corresponding period of 2014. Profit attributable to owners of the group for the third quarter of 2015 was 7 percent higher than for the similar period last year, reaching $754 million.

Revenues for Grace Kennedy rose a strong 14.4 percent in the nine months to September, this year, to $59.7 billion from $52.2 billion generated in the corresponding period of 2014. Profit attributable to owners of the group for the third quarter of 2015 was 7 percent higher than for the similar period last year, reaching $754 million.

Profit declined by $338 million or 14.2 percent for the year to date, compared with the similar period of 2014, moving from $2.38 billion to $2.05 billion.

The earnings per stock unit to September amount to $6.19, down from $7.21 in 2014, for the full year should end around $3.4 billion or $10.30 per share.

“The Group’s performance was in part impacted by the costs associated with the integration of our expanded US Food operations through GraceKennedy Foods (USA), recognition of the total asset tax liability in the first quarter, lower foreign exchange gains and higher finance costs”, Group Chief Executive Officer, Don Wehby and chairman Gordon Shirley said in his report to shareholders.

Group Chief Executive Officer, Don Wehby

“The Money Services segment recorded higher revenues and profits due to higher remittance transactions and increased market share in Jamaica, higher revenues from our cambio operations in Trinidad, and cost containment initiatives implemented by the segment”, Wehby and Shirley stated.

Shareholders’ equity stands at $37.2 billion with book value per share of $112.47. The company will pay a third interim dividend of 90 cents per stock unit on 16th December.

Grace’s shares are listed on the Stock Exchanges of Jamaica and Trinidad and last traded at J$68.11 and TT$3.60 giving it a PE of 6.7 times 2015 earnings leaving room for quite some growth.

Strong Buy Rated growth more to come

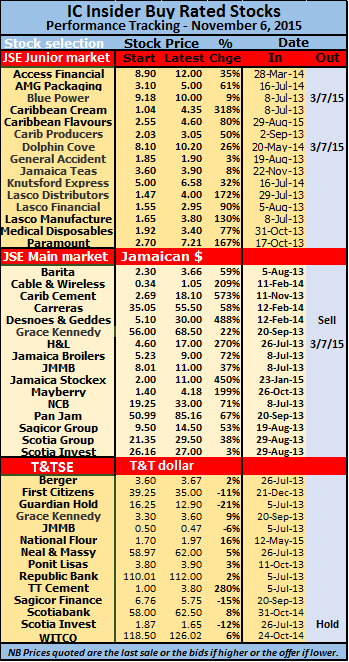

Carib Cement is the IC Insider best performing selection with gains of 573%.

While Jamaican stocks have jumped sharply those in Trinidad are just marking time which a number of prices retreating as interest rates were pushed up by the central bank on a number of occasions and the country faced falling oil revenues with the fall in world oil prices.

In the Jamaican market, stocks that were selling around 5 times earnings or less at the start of the year, have seen a sharp revaluation of many, with an average now around 9 times earnings based on this year’s estimated earnings. A total of 22 companies or 41 percent of the ordinary listings are selling above the average. Indications suggest that the rally in Jamaica will continue, with expectation for interest rates to decline going into 2016. A sharp 32 percent fall in interest rates from March last year to October this year, is one of the main driver of the market. Company results have been mostly strong with many enjoying large increases over the results of last year as well as over the 2013 period. A fall in the cost of energy and fuel and expanded sales in some cases are major drivers of profit gains this year as well.

It is partly against the above developments, that IC Insider BUY RATED listing of stocks should be viewed. Some of the stocks have been placed on hold based on the gains to date and much higher valuation as a result of this year’s growth.

Four junior market stocks should be held at this moment rather than buys, unless investors are looking at a two to three year’s investment period. Lasco Distributors, Lasco Financial, Lasco Manufacturer and Medical Disposables have reached rich valuations and should be held at this stage of the market. Profit growth for 2017 fiscal year for the Lasco companies should be very strong and will make them attractive buys again, the task is when should these be bought again to take advantage of the strong growth ahead? The problem now is that supply for these stocks is low, currently. Dolphin Cove growth has slowed for this year and remains a hold for now until 2016, the rest of the junior market selections are still attractive buys, with potential gains of 50 to 130 percent for a number of them.

Desnoes and Geddes should be sold now with the price at $30 rather than to await a payout from the proposed buyout proceeds. The Jamaica Stock Exchange share has gained 450 percent since we placed a BUY RATED status on it. The price has room to grow but investors will need to be cautious about buying at current price levels until the release of the September quarterly report in a few days. A hold is placed on the two Scotia shares with both now valued around 10 time 2015 earnings. Carreras is priced close to 10 times this fiscal year’s earnings but high dividend yield well in excess of current Treasury bill rate of 6.2 percent will make the stock an attractive income earner and will continue to drive the price upwards. Mayberry Investments should be a hold at this stage, with reporting earnings not in strong support of the present stock price, the company has the assets that will aid in a large increase in net asset value.

Desnoes and Geddes should be sold now with the price at $30 rather than to await a payout from the proposed buyout proceeds. The Jamaica Stock Exchange share has gained 450 percent since we placed a BUY RATED status on it. The price has room to grow but investors will need to be cautious about buying at current price levels until the release of the September quarterly report in a few days. A hold is placed on the two Scotia shares with both now valued around 10 time 2015 earnings. Carreras is priced close to 10 times this fiscal year’s earnings but high dividend yield well in excess of current Treasury bill rate of 6.2 percent will make the stock an attractive income earner and will continue to drive the price upwards. Mayberry Investments should be a hold at this stage, with reporting earnings not in strong support of the present stock price, the company has the assets that will aid in a large increase in net asset value.In Trinidad, companies are having a tough time growing profits in a meaningful way but there are still a few stocks that are worthwhile holding, with Trinidad Cement being a very compelling buy now selling at a PE of 4 times this year’s earnings. National Flour is undervalued and has room for growth with increased profits in 2015. Most of the rest will have to await 2016 for increased profits and growth.

Strong C&WJ mobile growth

Cable & Wireless HQ

The report went on to state, “In the first half of the current fiscal year, our total number of network sites grew by 10 percent and our mobile networks carried 93 percent more data traffic, with Jamaica data traffic up 241 percent, BTC up 137 percent, Panama up 81 percent and Barbados 73 percent higher.”

In the Caribbean, the company said “we completed Phase 1 of our broadband expansion in Jamaica passing 800 homes in Portland with Phase 2 underway and set to pass an additional 7,300 homes taking our total homes passed to 276,000. We also began installation of a new backbone to upgrade core capacity to multiple 100Gbps links. In Trinidad, we passed an additional 4,800 homes with HFC, taking our total homes passed to 311,000 in Trinidad and we passed an additional 19,000 homes with FTTH in Barbados taking our coverage to over 100,000 homes passed. In the Bahamas, we have completed the design phase of our plans to pass 14,200 homes.”

Paramount more than doubles dividend

Paramount Trading will be paying a final dividend of 39 cents on November 23, 2015 to shareholders on record as at November 12.The ex-dividend date is November 10, 2015.

Paramount Trading will be paying a final dividend of 39 cents on November 23, 2015 to shareholders on record as at November 12.The ex-dividend date is November 10, 2015.

The company made profit of 95 cents per share for the fiscal year to May 2015 and 61 cents in 2014. The 2015 payment represents 41 percent of profit and equates to a dividend yield of 14.89 percent based on the price of $2.62 at the start of the year. For the quarter ending August earnings grew 27 percent to 28 cent per share versus 22 cents in the same period in 2014.

Paramount Trading paid a dividend of 15.1 cents per share payable on December 12 last year.

the company’s shares are listed on the junior market of the Jamaica Stock Exchange and last traded at $7.10.

TCL older owners screwed as profit rise

Trinidad Cement achieved a 135 percent jump in profit after tax due to shareholders for the quarter to September, but the data showed that the most of the minority shareholders have suffered a massive dilution in their earnings.

Trinidad Cement achieved a 135 percent jump in profit after tax due to shareholders for the quarter to September, but the data showed that the most of the minority shareholders have suffered a massive dilution in their earnings.

The company reports $74 million for the 2015 third quarter, compared with $30 million for the same period last year, year to date profit after tax leapt 558 percent to $395 million above the $60 million reported for similar period for 2014. All shareholders get 16 cents per share for the September quarter for each share they hold, the year to date results show them entitled to $1.18 or 7.65 times the September quarters’ earnings. The year to date profit is 6.8 times the prior year’s nine months figure, a difference of 12.5 percent.

The company through a rights issue increased the share capital which diluted the earnings per share. Instead of increased earnings after the company’s debt was restructured, leading to lower debt servicing cost, the majority of shareholders will see lower earnings per share going forward even as the company prevented some shareholders from participating in the issue and withheld pertinent information from most shareholders. As a result the earning per share for 2016 is likely to be no more than 70 cents compared to 96 cents in 2015 from continuing operations, even as profit is likely to rise.

Earnings per share from continuing operations amount to 15.5 cents for the quarter and $1.186 for the nine months. Full year earnings should end up around $1.40 but this includes approximately 44 cents relating to the one off restructuring credit, thus reducing the ongoing earnings to 96 cents per share.

Caribbean Cement factory- majority controlled by TCL

“This performance was largely driven by higher domestic sales volumes, and lower fuel and electricity costs at CCCL and ACCL” Wilfred Espinet Group Chairman and Nigel Edwards, a Director of the company told shareholders in a statement accompanying the interim financials. The company enjoyed a $206 million credit which is reflected mainly in the year to date results for 2015 as a result of restructuring the heavy debt in had incurred previously.

Finance cost for third quarter was $12.5 million lower than third quarter 2014 and ended at $35 million due both to the reduced interest rates from the new loans and a reduction of the principal loan balance from US$245 million to US$200 million. For the year to date finance cost fell to $145 million compared to $214 million in 2014.

Cash flow from operations amounts to $65 million I the quarter and $677 million of the nine months leading to cash at the end of the period at $302 million. The working capital moved to $340 million with current assets of $978 million and current liabilities of $633 million at the end of September. Non-current liabilities stand at $1.4 billion and equity at $1 billion.

The company shares are listed on the Trinidad and Tobago Stock Exchange (TTSE), it manufactures and distributes cement in the eastern Caribbean and Jamaica. The stock last traded at $3.50 on the TTSE on Friday October 30.

Q4 Profit jumps 215% at AMG

AMG Packaging enjoyed a great year to August, with 74 percent jump in profits to $79 million over 2014 and 86 percent before expenses incurred for the new toilet tissue operation. For the last quarter of the fiscal year things were even better with a 215 percent jump to $27 million.

AMG Packaging report big gains in profit for 2015

A sharp $4.5 million fall in fuel cost and repairs and maintenance respectively, a 50 percent cut in selling and distribution expenses amounting to $7 million, and lesser declines in wages, electricity along with an increase in revenues helped to improve gross profit, margins and the results for the year.

Gross cash flow generated from operations came in at $92 million, up from $58 million in 2014. Going forward its unclear what impact the new operations will have, barring any major losses IC Insider is forecasting $1.05 per share after tax for 2016, the first year of reduced taxation will be payable. The company paid dividends of $18.4 million during the fiscal year and in the prior year $20.5 million.

Looks like a greater stability in raw material cost and attention paid to cost in a number of areas, paid rich dividend in the past four quarters and in particular the final quarter. Cost of sales fell from $491 million in 2014 to $484 million and gross profit jumped to $149.4 million from $116 million, an increase of 28.6 percent. Revenues rose moderately by 3 percent for the quarter to $172 million and 4 percent increase for the full year to hit $633 million. While the growth in revenues may not appear electric closer look indicates a growth of around 7 percent on a quarter over quarter basis for the last 4 quarters.

Administrative expenses rose from $48.5 million to $51.4 million in 2015 and finance cost declined form $10 million to $8.7 million.

Borrowings grew to $151.6 million while cash funds rose $64 million from $22 million in 2014. The balance sheet shows $59 million deposited to purchase equipment for the new tissue operation. Current assets stood at $335 million and current liabilities at $60 million. Equity capital grew to $377 million from $316 million.

AMG Packaging is in the business of manufacturing paper based boxes for the packaging and its shares are listed on the junior market of the Jamaica Stock Exchange and last traded at $4.80 with a gain of 82 percent for the year to date.

Lasco Distributors blow out profits

Lasco Distributors with responsibility to distribute “I Cool” drink.

The Gross profit for the period was S1.1 billion, an increase of $299 million or 36 percent over the prior year. The Gross Profit margin for the quarter was $628 million, or 32 percent over the same period last year. Gross profit margin for the august 2015 quarter is 17.26 percent versus 17.5 percent in 2014 and year to date 16.2 percent in 2015 and 16.28 percent in 2014.

The huge gain came from increased revenues of 34 percent for the quarter, amounting to $6.95 billion and 36 percent for the six months of $3.64 billion.

“This growth was driven mainly by contributions from our iCool and Unilever lines of business, both of which have been doing very well”, Peter Chin, Managing Director reported to shareholders in the directors’ report accompanying the financial data.

An interesting element of the results is the 10 percent growth in revenue over the June quarter a continuation of the quarter over quarter growth evident from late in 2014 with an average of 8 percent for the last three quarters.

Earnings per stock for the six months amount to 11 cents and 7 cents for the quarter. IC Insider projects profit of 34 cents for the current year and 50 cents for the year to March 2017.

Cost were held well below the growth in revenues with Operating Expenses in the latest quarter rising to $396 million from $377 in 2014 and for the six months this year the company incurred $779 million versus $658 million in 2014 for a rise of 18 percent.

Cash flow from operations increased by 94 percent to $391 million from $202 million for the similar period to September 2014 swelling Cash and Equivalents at the end of the Period to $904,043 compared with $191,277.

The company’s shares are listed on the junior market of the Jamaica Stock Exchange. Its principal activity is the distribution of pharmaceutical and consumable items, ii distributes all of Lasco Manufacturing’s products locally.

The stock may be considered fully priced currently with a PE of 10 being one of the higher priced junior market stocks, but with strong growth expected and lower interest rates to come, investors with a long term time horizon may want to accumulate from now, bearing in mind the limited supply available.

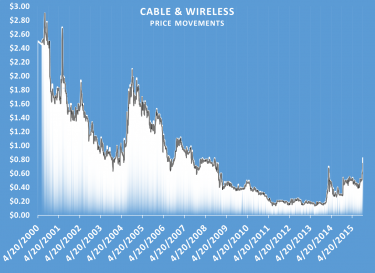

C&W shares may fetch over $3 in a takeover

Cable & Wireless with the old Lime brand logo

Cable and Wireless shares had become scarce in recent weeks, with one investor IC Insider sources indicated, was seeking 7 million shares to buy, earlier last week at 60 cents each. From as far back as the 8th of October, there were only 4 million units on offer between 55 cents and $1.21. By Thursday the supply dropped even more with trading taking place as high as 67 cents. At 12.30 on October 22, there were 453,964 shares on offer at 67 cents, with 5,000 units sold out of this amount by the close of the market. A total of 305,850 units were on offer at 70 cents, with the next at 90 cents, with 5,000 units. At 99 cents there were 233,730 units, at $1 one block of 877,723 units with the next lot of 10,000 at $1.71, the next 130,169 shares at $2 and 1.66 million units at $3.75. That not a lot for a stock that usually trade in millions of units.

Only 5,850 shares traded on Friday at 82 cents and demand swelled to more than 5 million units at the close to buy at 82 cents. Supply disappeared with only 4 offers listed, ranging for 10,000 units each at $1.20, $1.21 and $1.70 and then 2.66 million units at $3.75.

The question on investors’ minds, is where will the price settle? One broker indicated that it will trade at $1 on Monday if there is supply. With the imbalance between supply and demand, a higher price than that seems imminent. Some Investors are wondering why some buying on the buyout news of the parent when there is uncertainty if the Jamaican shareholders will be bought out as well if the deal goes through. Some are looking at the Diageo transaction with Desnoes & Geddes and speculating that the same could happen here.

IC Insider.com has the stock as BUY RATED from February 2014 on the basis of a turnaround in the financial fortunes of the company. Based on what’s happening locally the current price can be justified as the company is now in a position to be reporting profits, with rising revenues and falling cost. If the deal with CWC goes through, (that does not seem likely at the stated price) and the minority shareholders in C&W were to be bought out, IC Insider went to work to see how high the price could be, in a takeover.

C&W had major improvement in earnings in the June quarter, with EBITDA rising a very strong 82 percent. Net results saw a sharp fall to a loss of just $303 million, from a loss of $712 million in 2014 as revenues grew 13 percent to $5.45 billion, aided by a 17 percent growth in mobile subscribers and 27 percent increased mobile revenues. Operating expenses were static at $4 billion but finance cost rose to $1.1 billion from $962 million in 2014, depreciation was down and amortization up. Revenues should climbed close to $6 billion in the September quarter and is likely to result in a profit around $200 million before any allowance for tax.

C&W had major improvement in earnings in the June quarter, with EBITDA rising a very strong 82 percent. Net results saw a sharp fall to a loss of just $303 million, from a loss of $712 million in 2014 as revenues grew 13 percent to $5.45 billion, aided by a 17 percent growth in mobile subscribers and 27 percent increased mobile revenues. Operating expenses were static at $4 billion but finance cost rose to $1.1 billion from $962 million in 2014, depreciation was down and amortization up. Revenues should climbed close to $6 billion in the September quarter and is likely to result in a profit around $200 million before any allowance for tax.In March 2015, CWC completed the purchase of Columbus International, a fibre-based telecommunications and technology services provider operating in the Caribbean, Central America and the Andean region, for a consideration comprising US$708 million in cash and 1,558 million CWC shares. This resulted in an increase in share capital of US$78 million and the formation of a merger reserve of US$1,209 million. The total consideration, $2 billion for the CWC acquisition resulted in a multiple of 7.8 times EBITDA.

The proposed price of US$5.5 billion being proposed for CWC with EBITDA of US$840 for the combined entities at March, would be 6.55 times EBITDA. Applying this ratio, puts C&W value based on EBITDA for the current fiscal year around $3.30 each. CWC communications paid much higher multiple for Columbus only a year ago which would make it difficult for CWC management to justify to their shareholders a deal that reduced the value of the group with the full benefit of the merger of the Flow operation not yet visible. The proposed buyout price would, however, be more than the market value of CWC, worth 2.6 billion pounds, or about $4 billion, based on its market capitalization on Thursday. John Malone the major owner of Liberty Global already has a 13 percent stake in CWC.