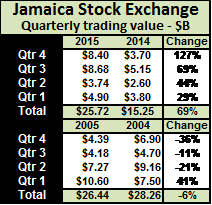

The Jamaica Stocks Exchange stock rocketed from $1.57 to a record $15.50 topping the market as the best performing stock over 52 weeks with gains of 887 percent. The JSE benefitted from a big jump in profits from $8 million in 2014 to $139 million in nine months to September this year, as revenues jumped from $242 million in 2014 to $521 million.

The Jamaica Stocks Exchange stock rocketed from $1.57 to a record $15.50 topping the market as the best performing stock over 52 weeks with gains of 887 percent. The JSE benefitted from a big jump in profits from $8 million in 2014 to $139 million in nine months to September this year, as revenues jumped from $242 million in 2014 to $521 million.

For the quarter, profit amounts to $37 million up from $11 million in 2014, from operating revenues of $157 million versus $89 million in 2014. In addition to operating revenues, the JSE earned $16 million from investment income in the latest quarter, compared to $8 million in the September 2014 quarter and $34 million in the nine months in both years.

Earlier in the year, IC Insider stated, “the stock remains IC Insider BUY RATED and is now available at $3.50 which it last traded at, but won’t remain that way forever and investors should be buying this one for big long-term gains,” since then the stock has shot up to $15.50 for a gain of 933 percent for the year.

For the September quarter, cost rose from $90 million to $109 million due mainly to staff cost jumping b $12 million. For the nine months, cost rose from $273 million to $340 million with staff cost accounting for $20 million of the increase and securities commission fees jumping to $37 million from $10 million in 2014.

For the September quarter, cost rose from $90 million to $109 million due mainly to staff cost jumping b $12 million. For the nine months, cost rose from $273 million to $340 million with staff cost accounting for $20 million of the increase and securities commission fees jumping to $37 million from $10 million in 2014.

The exchange has cash and investments of $448 million with a working capital ratio of 2.4:1 and equity of $624 million, there is no borrowed debt on the books.

Factors that investors should be considering looking forward which will be critical to the fortunes of the stock exchange are the levels of trading that could point them to future income and profit. Up to December 4, this year, the JSE traded $8.4 billion in normal trades compared to $3.7 billion in December 2014, in the September quarter, trading amounted to $8.68 billion up from $3.74 billion in the June 2015 quarter and $5.15 billion in September 2014. The increase in the 4th quarter stock trading activity to date, is just below the 3th quarter level, in addition there will be a full quarterly income from repo business.

In the March quarter 2015, a total of $4.9 billion was involved in trading up from $3.8 billion in March 2014. Both the December and the March quarters in 2015 have a few one off type trades, regardless the trend is pretty clear pointing to the possibility of a strong 2016. The last two quarters suggest that trading levels in dollar terms could be up around 40 percent and it could be more. That would mean a sharp increase in revenues for the exchange in addition the managing of the repo business will provide added income for the entire year compared with two months in the September quarter and 5 months for the year to December.

In the March quarter 2015, a total of $4.9 billion was involved in trading up from $3.8 billion in March 2014. Both the December and the March quarters in 2015 have a few one off type trades, regardless the trend is pretty clear pointing to the possibility of a strong 2016. The last two quarters suggest that trading levels in dollar terms could be up around 40 percent and it could be more. That would mean a sharp increase in revenues for the exchange in addition the managing of the repo business will provide added income for the entire year compared with two months in the September quarter and 5 months for the year to December.

Back in 2004, the market traded $28 billion in regular trading activity when the Jamaican dollar was trading around $62 to the US dollar with trading in 2005 being slightly behind at $26 billion. Trading would need to get to $51-55 billion for a year to match trading levels back in 2004 and 2005.

Profit should close out the year on a high with monetary trading levels set to exceed that of the third quarter and well ahead of the fourth quarter of 2014. IC Insider is forecasting earnings of $1.40 for the 2015 not factoring the trade that could flow from the Heineken buyout of the minority shares in Desnoes and Geddes.

JSE stock up 887% could end higher

Profit break out for Scotia in 2016?

Scotia Group Montego Bay.

Net interest income after impairment losses for the year was $22.9 billion, marginally above 2014 resulting in a reduction in the impairment losses on loans by $241 million or 15.0 percent, this is “due to enhanced adjudication, monitoring and collection efforts. The Group continues to report strong growth in loan volumes during the year, particularly our Residential Mortgages, Consumer, Small Business and Commercial portfolios; however net interest margins continue to decline due to lower market interest rates and the competitive environment”, Scotia stated in their media release accompanying the financials.

Jackie Sharp – CEO Scotia Group

Total assets increased year over year by $25.9 billion or 6.4 percent to $433 billion as at October 2015 due primarily to increases of $8.8 billion or 6 percent in Loans to $154.5 billion, increase in investment and pledged assets and $9.2 billion in other assets

The group reported earnings per share of $3.19 for the year and $1.26 for the last quarter and seems poised to generate earnings around $4 for the 2016 fiscal year.

tTech offer seems a buy

tTech a company most investors would hardly have heard about, will be going to the capital market this month, to raise approximately $50,263,900, by the issuing for subscription 25,652,000 ordinary shares to the general public and special persons related to the company at $2.50 each.

tTech a company most investors would hardly have heard about, will be going to the capital market this month, to raise approximately $50,263,900, by the issuing for subscription 25,652,000 ordinary shares to the general public and special persons related to the company at $2.50 each.

In reality only 16.4 million are allocated for the general public, a relatively small number. The Company that was formed in 2006 currently provides outsourced IT solutions to businesses currently in Jamaica. IC Insider’s preliminary assessment indicates earnings per share around 40 cents before taxation for a PE of 6.3 and would make the stock a buy.

The purpose of the offer is to provide working capital support to its operations and in order to allow the Company to augment its productive capacity and thereby to take advantage of new business opportunities as well as benefit from listing on the stock exchange and improve staff compensation by allowing them to buy the shares that are bound to increase sharply in price after listing.

The Company estimates that the expenses in the Invitation will not exceed $10 million. Subscription opens at 9 am on December 16th, 2015 and closes at 4:30 p.m. on the December 18th, 2015, subject to the right of the Company to shorten or extend the time for closing. If the Invitation is fully subscribed and is successful in raising $50,263,900, the Company will make an application to the JSE for the Shares to be admitted to the Junior Market. The company has been profitable with revenues growing at an attractive rate. The Company has adopted a dividend policy of paying 25 percent of profits each year.

All completed Application Forms must be delivered to NCB Capital Markets.

IC Insider will have a fuller report at a later date.

Caribbean Flavour(ing) future profits

“With the price of the stock, trading at $2.55 for a PE of just over 3 and 2.3 based on IC Insider’s forecast, (is) indicative of much upside potential,” was how Caribbean Flavours was assessed back in August this year, as the stock was elevated to the BUY RATED ranking after the company released its full year results to June.

“With the price of the stock, trading at $2.55 for a PE of just over 3 and 2.3 based on IC Insider’s forecast, (is) indicative of much upside potential,” was how Caribbean Flavours was assessed back in August this year, as the stock was elevated to the BUY RATED ranking after the company released its full year results to June.

In the June posting, IC Insider stated, “The company seems poised to hit earnings of 65 cents per share, for the June 2015 financial year, making it attractive for some short-term gains, with the current price of $2.09, at a PE ratio of 3 times earnings.”

Focusing on the end results of Caribbean Flavours & Fragrances for the year to June 2015 with increased profit of 22 percent over 2014 would lead one to look elsewhere, but that would be a big error. For while the nine months to March showed profit down marginally to $39 million from $40 million, profit for the March quarter was up 20 percent over March 2014 quarter, the June quarter increased by 143 percent to $18.77 million from just $7.6 million for June 2014.

The company followed up the improved results for the March and June quarters, with another quarter of strong performance to September, with a 51.3 percent increase in net profit to $20.36 million over the $13.46 million recorded for the similar period in 2014. The improved profit flowed from sales for the quarter jumping 38.20 percent to $87.46 million, compared to the $63.29 million recorded for the same period in 2014.

Caribbean Flavours’ produce with ingredients – the stock closed at a new high.

“The gross profit showed an increase of 28.91 percent moving from $25.487 million to $32.856 million as per our first quarter’s performance. The Company will continue to refine and improve our purchasing strategy in order to extract the necessary efficiencies and improve our cost of sales and gross profit.

The company continues to manage its administrative and general expenses within budget and compared to the 2014 quarter, there was only a 4.4 percent increase,” the report went on to state.

The future looks much brighter than the past year, for the company that manufactures and distributes flavours mainly for the beverage, baking and confectionery industries and also sells food colouring and fragrances. In responding to questions posed at the annual general meeting held on Wednesday 25 of November, directors indicated that the strong performance enjoyed in the September quarter continues into the December quarter.

“We have hardly scratched the surface of the potential market” Derrick Cotterell indicated, “we have moved into the Dominican Republic and Canada where there is much potential for growth and with renewed efforts and products the locally Jamaican market as well”. Cotterell stated that they have increased research into new products such as fragrances and this has opened up new opportunities for them. Trinidad, Cuba and Haiti are countries with potential for growth, they indicated but Haiti is said to be a difficult market to break into but they have contacts there that should make it possible. In addition to the focus on research and developments for new products and new customers the company said they were able to source some of its raw material more cheaply than before.

According to the company’s board, in their comments on the 2015 annual results “the economic environment has allowed the company to grow its revenues and profits by securing new markets for fragrances and increasing the volume of sales of flavours to existing and new customers in foreign markets. Based on the outlook for the coming year, it is expected that the company will continue to improve its profits whilst increasing its market share in the domestic and overseas markets”.

IC Insider projects profits for 2016 at $99 million or $1.10 per share with increased sales and improving profit margins and $1.50 for the 2017 fiscal year. Company is free of interest bearing debt and has net current assets of $221 million including cashfunds of $103 million.

Huge profit turn at Honey Bun – BUY RATED

![]() Honey Bun turned around a loss of $17 million in the September 2014 quarter into a profit of $4 million in 2015 and a profit of only $23 million into a one of $68 million for the 2015 fiscal year or earnings per share of 72 cents.

Honey Bun turned around a loss of $17 million in the September 2014 quarter into a profit of $4 million in 2015 and a profit of only $23 million into a one of $68 million for the 2015 fiscal year or earnings per share of 72 cents.

The performance and IC Insider’s forecast for the next two years, (See EPS forecast below) have elevated the status of the stock to BUY RATED.

The change came from a 22 percent rise in revenue in the quarter to $215 million from $169 million in 2014 and from a 19 percent growth in revenues for the full year, to $887 million from $747 million in 2014. The profit in the September quarter is a major achievement for the company it being the first time since 2012 when a small profit of $550,000 was realized that the company is reporting a profit.

“The company services lots of schools and so the summer months are normally reduced due to the holiday season for July and August. We will always have this challenge but we have somewhat overcome a significant portion of it by way of the development of new products that are not directly geared for schools and by targeting other markets also.

One Honey Bun’s Products

Helping the growth in profits was an improvement in gross profit and gross profit margin with the latter being 42.8 percent up from 41 percent in 2014 and from a 9.5 percent increase in administrative and other expenses, selling & distribution costs of $307 million from $280 million.

Investments, cash and equivalents rose to $92 million, net current assets stood at $102 million, borrowed funds fell from $73 million in 2014 to $51 million while equity rose to $368 million.

The company’s shares are listed on the junior market of the Jamaica Stock Exchange and last traded at $5.50, with the price being up 164 percent since 2015, and now sports a PE of 7.6 times 2015 earnings. IC Insider is forecasting earnings per share (EPS) of $1.15 for the 2016 fiscal year which gives it a PE of 4.8 and EPS of $1.70 for 2017.

The company advised that the Board of Directors will meet on Monday, December 7 to consider the declaration of a dividend. An interim dividend of 12 cents per stock, amounting to $11.3 million was paid in May this year.

Eppley’s stock scarce & undervalued

Eppley’s profit after tax increased 5 percent for the first nine months of the year to $41.7 million compared to $39.7 million in 2014. For the September quarter, profit jumped sharply by 91 percent to $19.3 million versus $10 million in 2014.

Earnings per share of $52.47 was achieved for the nine months and $24.17 for the quarter. A dividend of $9 per share will be paid on November 30 to ordinary shareholders on record at November 20.

Earnings per share of $52.47 was achieved for the nine months and $24.17 for the quarter. A dividend of $9 per share will be paid on November 30 to ordinary shareholders on record at November 20.

Revenues grew 93 percent for the quarter to $63 million and 60 percent for the nine months period, to $171 million. Net interest income increased from 39.56 percent in the nine months to 43.9 percent in the quarter. Operating expenses climbed 16 percent for the quarter and 15 percent for the nine months.

As of September, Eppley had a $1.38 billion portfolio consisting mainly of loans, leases and receivables. The average income yield of the portfolio was 14 percent, the company stated.

Equity capital at the end of the quarter stood at $341 million and borrowing at $1 billion with average cost of debt being 10 percent. We ended the quarter with $237 million of cash and short-term investments, the company also stated.

Eppley provides loan and insurance premium financing. At the end of the quarter, the stock that is listed on the junior market of the Jamaica Stock Exchange last traded at $380 much lower than the net asset value was $429 per share.

Revenue growth pushes down C&W loss

Cable & Wireless HQ

The company posted losses of $485 million after exceptional expenses in the September quarter, or 11 percent less than the $548 million loss for the six months in 2014.

EBITDA earnings grew to $1.2 billion compared to $971 million a year ago and for the half year $2.58 billion versus $1.78 billion, an increase of 45 percent.

“Each line of business showed improved results leading to growth in total revenues and EBITDA. Our mobile business was again the leading performer with our pre-paid subscriber base growing by 23 percent and our post-paid subscriber base growing by 6 percent when compared to the prior year first half,” stated Garfield Sinclair who heads C&WJ, in the financial report.

During the quarter, revenues grew 9 percent to $5.63 billion. This growth was filliped by mobile subscriber base and revenues up 22 percent and 16 percent respectively; and broadband subscribers and revenue up 8 percent and 11 percent respectively. Revenues for the half year grew 10 percent to $11 billion as revenues for the September quarter exceeded that of the June quarter by $179 million or 3.3 percent.

Interest cost declined in the quarter to $934 million from $1 billion last year and should fall in the coming quarters as the interest rates reset downwards in November, to 7.2 percent from 7.787 percent with the fall in local Treasury bill rates. For the half-year interest cost amounts $2 billion. Staff costs are down by $300 million in the six months period from that of 2014 to be at $1.246 billion but out payments and direct cost rose $226 million with the September quarter by $149 million over the June quarter.

The company generated operating cash flow of $520 million compared with negative cash flows of $133 million in six months to September 2014.

The financials does not show any indication of a merger between the local operations of Flow and C&W but the latter wrote large amounts of assets and made staff redundant but no mention is made in the report as to how the two entities will be operating going forward. There are questions to be answered here.

The company’s shares are listed on the Jamaica Stock Exchange last traded at $1.45.

Profit up 60% at Jamaican Teas

Profit at Jamaican Teas for the 2015 fiscal year to September rose 60 percent to $81 Million from a 17 percent increase in revenues of $1.3 billion and from a 32 percent rise in exports to $370 Million.

Profit at Jamaican Teas for the 2015 fiscal year to September rose 60 percent to $81 Million from a 17 percent increase in revenues of $1.3 billion and from a 32 percent rise in exports to $370 Million.

Export sales exceeded domestic sales from the manufacturing arm that ended at $363 million for a 6 percent increase for the year.

In the final quarter, net profit increased by 520 percent to $12 million from a loss in 2014 and $15.6 million after other comprehensive income. For the full year total comprehensive income amounted to $97 million compared to $46 million in 2014. The company incurred some one-off costs that are not likely to recur in 2016 and should help in contributing to increased profit.

The group operates two supermarkets, one in Kingston and one in Savanna-la-Mar with sales of $520 million for the year compared to $491 Million in 2014. The jointly owned supermarket in Montego have been challenging in a tight but competitive Montego Bay economy.

June marks the end of the tax free status of Jamaican Teas. Accordingly, the company became subject to income tax, effectively at 12.5 percent commencing in the fourth quarter of the 2015 financial year and continuing for another 4 years and nine months.

The company said they completed construction of 29 two bedroom units along with infrastructure work during the fiscal year, with all units being sold, with the majority of sales to be booked in the new fiscal year. The company expects that the net proceeds of sales will be used to pay down loans, pay a dividend to shareholders and finance Phase II of the development of which there are several commitments for.

Outlook|The company is expecting another year of good performance in 2016, in line with this, the 2016 financial year has started off on a favourable note with strong interest shown in units in phase 2 of real estate development. The expected completion of the sale of all units in phase 1 are of real estate development, good export sale orders so far. The electioneering ahead of the general elections could bring increased consumer spending and positive development in the tourism sector with the expectation of a strong tourist arrivals in 2016 could see the company benefitting. Jamaican Teas also holds a portfolio of equities that has increased in value with the 2015 results shows with an increased value of $16 million, that amount would have grown with the growth in the Jamaican Stock market since the year end.

Outlook|The company is expecting another year of good performance in 2016, in line with this, the 2016 financial year has started off on a favourable note with strong interest shown in units in phase 2 of real estate development. The expected completion of the sale of all units in phase 1 are of real estate development, good export sale orders so far. The electioneering ahead of the general elections could bring increased consumer spending and positive development in the tourism sector with the expectation of a strong tourist arrivals in 2016 could see the company benefitting. Jamaican Teas also holds a portfolio of equities that has increased in value with the 2015 results shows with an increased value of $16 million, that amount would have grown with the growth in the Jamaican Stock market since the year end.

The company is primarily involved in the processing of local teas and packaging along with imported teas and for the Jamaican and overseas markets, operates supermarkets, and the rental and development of realty. The company’s shares are listed on the Jamaica Stock Exchange, last traded at $3.85.

Point Lisas remains undervalued

Point Lisas is headquartered in Trinidad, is listed on the country’s stock exchange, last traded at $3.90 and is an undervalued stock with earnings per share including gains on property of $1.85 for the nine months to September this year.

Point Lisas is headquartered in Trinidad, is listed on the country’s stock exchange, last traded at $3.90 and is an undervalued stock with earnings per share including gains on property of $1.85 for the nine months to September this year.

Profit before tax of Point Lisas Industrial Port Development (Point Lisas) for the period to September, excluding fair value gains on property, amounts to $20.4 million an increase of 181 percent over $112,000 for the same period for 2014. Gross profit climbed sharply by 29 percent to $51 million in the third quarter from $40 million in 2014 and for the nine months, an increase of 12.66 percent from $134 million to $151 million.

For the September quarter, profit after tax moved from a loss of $14 million to a surplus of $14 million including fair value gains on property of $10.6 million and fair value loss of $4.7 million in the 2014 quarter. For the year to September, fair value gains on property amount to $58 million for 2015 and $91 million in 2014.

Revenues grew by 10 percent for the nine months to September compared to the period to September 2014. Cash flow from operations amounts to $31 million and is up from $13 million in 2014, leading to cash and equivalent of $60 million at the end of the 2015 period. Administrative and other cost declined moderately by $5 million for the quarter and for the nine months.

According to management in their report to shareholders, the increase in revenue was heavily influenced by containerized cargo operations which experienced a 15 percent increase in throughput over the same period in 2014. The data showed a 4 percent increase in imports, an 8 percent increase in exports and a 60 percent increase in trans-shipment cargo. General cargo experienced a 10 percent decline due to an 88 percent decrease in exports, a 1 percent increase in imports and a 4 percent increase in trans-shipment.

Total assets climbed to $2.28 billion in the third quarter 2015, equity capital amounts to $1.97 billion, borrowed funds amount to $125 million, while current assets stood at $121 million and current liabilities at $52 million.

“In the second and third quarters, PLIPDECO provided bunkering services as part of its service and revenue expansion drive. During the fourth quarter, the Corporation intends to continue with infrastructural improvements, information technology upgrades and move steadfastly with the Port upgrade project. The future outcome of these undertakings would further enhance productivity, overall efficiency of Port Operations and ultimately boost profitability,” Ian R. H. Atherly, Chairman of the company said in a release accompanying the financials.

Grace grows Q3 profit 7%

Revenues for Grace Kennedy rose a strong 14.4 percent in the nine months to September, this year, to $59.7 billion from $52.2 billion generated in the corresponding period of 2014. Profit attributable to owners of the group for the third quarter of 2015 was 7 percent higher than for the similar period last year, reaching $754 million.

Revenues for Grace Kennedy rose a strong 14.4 percent in the nine months to September, this year, to $59.7 billion from $52.2 billion generated in the corresponding period of 2014. Profit attributable to owners of the group for the third quarter of 2015 was 7 percent higher than for the similar period last year, reaching $754 million.

Profit declined by $338 million or 14.2 percent for the year to date, compared with the similar period of 2014, moving from $2.38 billion to $2.05 billion.

The earnings per stock unit to September amount to $6.19, down from $7.21 in 2014, for the full year should end around $3.4 billion or $10.30 per share.

“The Group’s performance was in part impacted by the costs associated with the integration of our expanded US Food operations through GraceKennedy Foods (USA), recognition of the total asset tax liability in the first quarter, lower foreign exchange gains and higher finance costs”, Group Chief Executive Officer, Don Wehby and chairman Gordon Shirley said in his report to shareholders.

Group Chief Executive Officer, Don Wehby

“The Money Services segment recorded higher revenues and profits due to higher remittance transactions and increased market share in Jamaica, higher revenues from our cambio operations in Trinidad, and cost containment initiatives implemented by the segment”, Wehby and Shirley stated.

Shareholders’ equity stands at $37.2 billion with book value per share of $112.47. The company will pay a third interim dividend of 90 cents per stock unit on 16th December.

Grace’s shares are listed on the Stock Exchanges of Jamaica and Trinidad and last traded at J$68.11 and TT$3.60 giving it a PE of 6.7 times 2015 earnings leaving room for quite some growth.