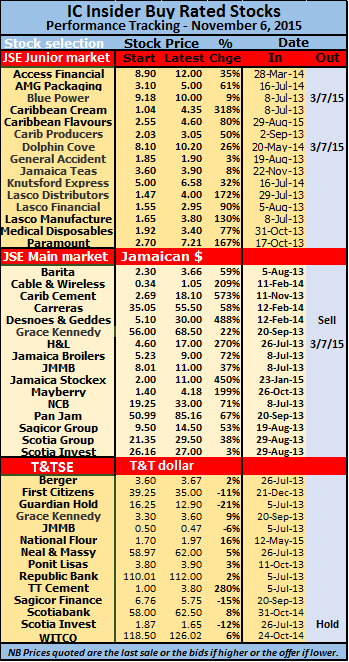

Carib Cement is the IC Insider best performing selection with gains of 573%.

While Jamaican stocks have jumped sharply those in Trinidad are just marking time which a number of prices retreating as interest rates were pushed up by the central bank on a number of occasions and the country faced falling oil revenues with the fall in world oil prices.

In the Jamaican market, stocks that were selling around 5 times earnings or less at the start of the year, have seen a sharp revaluation of many, with an average now around 9 times earnings based on this year’s estimated earnings. A total of 22 companies or 41 percent of the ordinary listings are selling above the average. Indications suggest that the rally in Jamaica will continue, with expectation for interest rates to decline going into 2016. A sharp 32 percent fall in interest rates from March last year to October this year, is one of the main driver of the market. Company results have been mostly strong with many enjoying large increases over the results of last year as well as over the 2013 period. A fall in the cost of energy and fuel and expanded sales in some cases are major drivers of profit gains this year as well.

It is partly against the above developments, that IC Insider BUY RATED listing of stocks should be viewed. Some of the stocks have been placed on hold based on the gains to date and much higher valuation as a result of this year’s growth.

Four junior market stocks should be held at this moment rather than buys, unless investors are looking at a two to three year’s investment period. Lasco Distributors, Lasco Financial, Lasco Manufacturer and Medical Disposables have reached rich valuations and should be held at this stage of the market. Profit growth for 2017 fiscal year for the Lasco companies should be very strong and will make them attractive buys again, the task is when should these be bought again to take advantage of the strong growth ahead? The problem now is that supply for these stocks is low, currently. Dolphin Cove growth has slowed for this year and remains a hold for now until 2016, the rest of the junior market selections are still attractive buys, with potential gains of 50 to 130 percent for a number of them.

Desnoes and Geddes should be sold now with the price at $30 rather than to await a payout from the proposed buyout proceeds. The Jamaica Stock Exchange share has gained 450 percent since we placed a BUY RATED status on it. The price has room to grow but investors will need to be cautious about buying at current price levels until the release of the September quarterly report in a few days. A hold is placed on the two Scotia shares with both now valued around 10 time 2015 earnings. Carreras is priced close to 10 times this fiscal year’s earnings but high dividend yield well in excess of current Treasury bill rate of 6.2 percent will make the stock an attractive income earner and will continue to drive the price upwards. Mayberry Investments should be a hold at this stage, with reporting earnings not in strong support of the present stock price, the company has the assets that will aid in a large increase in net asset value.

Desnoes and Geddes should be sold now with the price at $30 rather than to await a payout from the proposed buyout proceeds. The Jamaica Stock Exchange share has gained 450 percent since we placed a BUY RATED status on it. The price has room to grow but investors will need to be cautious about buying at current price levels until the release of the September quarterly report in a few days. A hold is placed on the two Scotia shares with both now valued around 10 time 2015 earnings. Carreras is priced close to 10 times this fiscal year’s earnings but high dividend yield well in excess of current Treasury bill rate of 6.2 percent will make the stock an attractive income earner and will continue to drive the price upwards. Mayberry Investments should be a hold at this stage, with reporting earnings not in strong support of the present stock price, the company has the assets that will aid in a large increase in net asset value.In Trinidad, companies are having a tough time growing profits in a meaningful way but there are still a few stocks that are worthwhile holding, with Trinidad Cement being a very compelling buy now selling at a PE of 4 times this year’s earnings. National Flour is undervalued and has room for growth with increased profits in 2015. Most of the rest will have to await 2016 for increased profits and growth.