Knutsford Express more than doubled its profit for the first quarter to August, with a jump of 109 percent to $35.7 million, from $17 million in 2014 and revenues that climbed 38.5 percent to $143 million. The increased revenue “was due to growth in passenger travel” the company stated in its report to shareholders.

Knutsford Express more than doubled its profit for the first quarter to August, with a jump of 109 percent to $35.7 million, from $17 million in 2014 and revenues that climbed 38.5 percent to $143 million. The increased revenue “was due to growth in passenger travel” the company stated in its report to shareholders.

Administrative and general operating expenses grew by a much slower 23 percent to $104 million than revenue. Depreciation climbed from $5.4 million to $7.55 million and finance amounts to $3.9 million and is up from $2.3 million in 2014.

Unfortunately the company has not provided information on the composition of administrative and general operating expenses. Based on the last audited financials, the largest cost items are fuel, accounting for around 19 percent of cost, labour for 34 percent and repairs around 10 percent for a total of 43 percent or thereabout.

Earnings per share is 36 cents for the 2015 quarter, putting full year earnings in the $1.60 region.

The company provides a popular coach bus service that plies between Kingston and the North and South coasts of Jamaica. Service was extended to Port Antonio from Ocho Rios earlier in 2015 but will take time to build as more persons become familiar with it. Going forward it is unsure what the opening of the highway to Ocho Rios from Kingston will mean for growth. What is sure it will take less time to cover the route with less operating cost per trip and will allow them to better compete with air travel as the time factor to and from Montego Bay and Kingston will be reduced.

The stock is listed on the junior market of the Jamaica Stock Exchange and has been trading around $6.10, for some time. These results should give the price a lift as the value is very low compared to others on the market, but management needs to improve on the inadequate manner of reporting the results, if not investors will be skeptical about the financial performance and shy away from the stock.

At the end of the quarter, shareholders equity stands at $250 million and liabilities of just $91 million and current assets of $157 million which includes cash and investments of $79 million and other assets of $61 million that rose from $21 million in May this year.

The company paid a dividend of 15 cents per share on September 15.

Knutsford doubles profit

Paramount rolls along with more profits

Paramount office

“Year over year, operating expenses as a percentage of total revenue increased 16.9 percent versus 14.9 percent as the company continued to strengthen its team and streamline operations. Paramount has a positive outlook for the rest of the year as it continues to aggressively pursue growth opportunities,” Hugh Graham, CEO & Managing Director stated in a report to shareholders accompanying the financials.

During the quarter the company generated $44 million in cash from operations and ended up with new cash funds of $69 million after reducing the level of receivables by $20 million, payables grew by $33 and Inventory rose by $15 million, putting cash and equivalent at $164 million at the end of the August.

Some of the products the company handles

Earnings per share for the quarter ended at 28 cents compared with 22 cents, in the August 2014 quarter and 95 cents for the 2015 year that ended in May. IC Insider forecast $1.45 per share for the full year. The stock trades at $6.10 on the Junior market, placing the PE ratio at 4 with much room for growth in the stock price with nearly half of the junior stocks valued at an average of 8.6 times current year’s earnings with all of those above 7.7 times.

The company will be considering a dividend at a directors’ meeting to be held on Thursday, October 29. The last dividend paid, was 15.1 cents per share on December 12, last year and in December 2013, 13.5 cents. With the 2015 full year profit being up by 57 percent over 2014, investors should see an increase to about 23.5 cents per share being paid this time around.

Kremi’s big surge forward

Sharp reduction in cost of sales and a 7 percent increase in revenues that ended at $271 million swelled profit in the August quarter for Caribbean Cream by more than 4,000 percent to $45.5 million and for the six months by 375 percent to $84.7 million from an 11 percent increase in sales to $560 million.

Sharp reduction in cost of sales and a 7 percent increase in revenues that ended at $271 million swelled profit in the August quarter for Caribbean Cream by more than 4,000 percent to $45.5 million and for the six months by 375 percent to $84.7 million from an 11 percent increase in sales to $560 million.

Cost of sales dropped 18 percent from $195.4 million to $161 million for the August quarter due mainly to a fall in the price or raw material input and from $378 million incurred for the half year in 2014, cost dropped to $339.4 million, lifting gross profit by 88 percent for the quarter to $110 million and by 73 percent for the six months versus that of 2014, to $221 million.

Administrative expenses climbed 37.8 percent to $102 million due mainly to implementation of sanitation measures that had to be implemented while selling and distribution expenses grew from $23.5 million to $25 million for the six months period, compared to that of 2014 and for the quarter, administrative expenses climbed by a more sedate 13.6 percent to $46 million while selling and distribution expenses grew from $12 million to $14 million.

Earnings per share amounted to 22 cents for the half year and 12 cents for the quarter. IC Insider is now forecasting earnings of 65 cents per share for the full year ending February 2016, due to the lower increase in sales in the August quarter than the 15 percent increase in the first quarter. The stock ended at a record close of $2.55 on Tuesday and has gained 240 percent for the year to date. IC Insider expects it to make further gains, as it is priced well below other stocks on the junior market that are selling above 7.6 times this year’s earnings with an average of 8.4.

A lot of the gains in profit came from the decline in raw material input, helping to push gross profit margin from 27 percent to 43 percent. Going forward increased input cost can place pressure on margins unless investment measures plan by Caribbean Cream to lower cost and create a more efficient operation are able to improve revenues and cut cost to compensate for any potential raw material cost increase that may arise. Cost increase in the medium term seems unlikely with downward pressure on input cost, the company has cash that it could be used to build up inventory at low prices if they sense the potential for prices to rise and thus mitigate against sharp price increases for the rest of the fiscal year.

Undervalued Pan Jam few look at

Pan Jamaican Investment Trust is one undervalued company that not many investors seem to be paying much attention at even as many seem to be piling into a few sexy overvalued ones, ignoring the gains being make in the bottom-line of the company. Net profit attributable to owners of Pan Jamaican Investment Trust increased 24 percent for the June 2015 quarter to $853 million, from $688 million in the 2014, second quarter.

Pan Jamaican Investment Trust is one undervalued company that not many investors seem to be paying much attention at even as many seem to be piling into a few sexy overvalued ones, ignoring the gains being make in the bottom-line of the company. Net profit attributable to owners of Pan Jamaican Investment Trust increased 24 percent for the June 2015 quarter to $853 million, from $688 million in the 2014, second quarter.

Pan Jam generated net profit attributable to owners for the six months to June with an increase of 28 percent to $1.4 billion from $1.09 billion for 2014. Profits resulted in earnings per stock unit of $4.07 for the 2015, second quarter and $6.65 for the six months. Earnings for the year should be in the range of $15-17 per share. The stock traded last at $61.71 while the book value is at $105 per share.

Investment income of $158 million in the second quarter is 28 percent higher than last year’s comparable quarter’s income of $123 million. Year to date, investment income declined 25 percent from the 2014 period to $193 million. Investment income fell due a number of factors, “principally as a result of a profitable conclusion to a real-estate related investment in Canada, which more than offset lower foreign exchange gains of $33 million, versus $42 million last year, dividends and interest of $35 million, versus $45 million last year and trading gains of $26 million, versus $32 million last year. Year to date investment income of $193 million is 25 percent behind last year due principally to reduced foreign exchange gains of $31 million, versus $83 million last year, and trading gains of $12 million versus $37 million last year” the company said in a release accompanying the financials.

Rapid True Value owned by Hardware & Lumber an associate of Pan Jam

Share of results of associated and joint venture companies for the quarter, rose 32 percent to $791 million and grew by 35 percent for the six months period to $1,234 million. The results of Sagicor increased by $175 million or 31 percent for the quarter and by $289 million or 33 percent for the half year. The results for Sagicor Group have some non-recurring income that arose from loan loss recovery.

Operating expenses were held fairly tightly with a 12 percent rise in the quarter to $305 million and for the half year only 5 percent to $565 million. Finance costs declined compared to last year, by $25 million to $106 million for the quarter and $74 million to $200 million for the 6 months, resulting from reduced foreign exchange losses on the International Finance Corporation loan and reduced interest on a smaller average principal balance outstanding for the period compared to 2014.

Caribbean Cream profit up 138%

Caribbean Cream profit jumps 138% in Q1-2015-16

That seems to be receding with a big jump in profits for the full year to February when profits climbed to $57 million from $35 million for 2014 and a big leap in the first quarter ending May, jumping 138 percent to $39 million. Growth was only constrained by added cost for cleaning and sanitation which helped push administrative cost to $56 million by $20 million. Loans are down $20 million and brought interest cost down. Inventories fell from $96 million to $61 million, the fall in the world market price for milk powder would have been a major factor behind this, coupled with a greater level of stability of the Jamaica dollar that would suggest there was little benefit from having large amounts of inventories. Trade receivables climbed $20 million, cash moved to $51 million from $17 million in 2014 and could end up around $200 million by the end of fiscal year to February 2016, payables declined from $109 million to $80 million and equity capital has moved to $326 million, lending strength to the company’s improving financial health.

For the quarter, revenues climbed 15 percent to $289.2 million from $251.5 million in May 2014 and was better than for the February quarter of $273 million. The growth in revenues is better than the 11 percent garnered in the February quarter. Lower operating expenses of $178 million versus $183 million in 2014 drove gross profit up 61 percent with profit margin jumping to 38 percent from 27 percent in 2014 and was helped by a 13 percent price increase ahead of the February quarter. Marketing costs remain static at $11 million while interest cost fell from $5.8 million to $4.6 million.Earnings came in at 10 cents per share, well over the 4 cents reported in 2014 and not very far from the full year earnings of 15 cents. Earnings for fiscal year ending 2016 should hit 75 cents per share as cost savings and marketing measures take effect. The price of milk powder, a major input into the production of ice cream, fell 25 percent since the end of the May quarter to the end of August on the US market and looks like it headed lower, will result in major cost savings. The company enjoys 5 years tax free holiday commencing in 2013 when it listed on the junior market of the Jamaica Stock exchange and after that is entitled to 5 years of taxation at half the regular tax rate.

The stock traded at $1.67 on Friday on the junior market of the Jamaica Stock Exchange but was as high as $2.50 coming from a low of 61 cents earlier in the year. The next set of results due early October, will most likely give the stock another shot in the arm.

Lasco Financial’s Q1 Profit up 14%

Lasco Financial Services (LFSL) reported profit of $10 million for the March 2015 quarter, down from $41 million made in 2014 but revved things up to a 14 increase in June quarter to $54 million as revenues climbed 8 percent to $192 million and well over the $148 million generated in the March quarter.

Lasco Financial Services (LFSL) reported profit of $10 million for the March 2015 quarter, down from $41 million made in 2014 but revved things up to a 14 increase in June quarter to $54 million as revenues climbed 8 percent to $192 million and well over the $148 million generated in the March quarter.

For the March quarter revenue that compared with the 2014 quarter expenses grew by $28 million due mainly to increase spend on marketing and selling expenses. Jacinth Hall-Tracey, Managing director indicated that the period suffered from squeezed margins in March quarter on foreign exchange trading and foreign exchange losses in the quarter, resulting from the revaluation of the Jamaican dollar and greater stability of the exchange rate. Loan disbursements slowed as credit rating data used in assessing potential clients resulted in lower loan approvals.

Total expenses for the first quarter increased by 5.5 percent to $137 million compared to the corresponding period. This is primarily due to a 36 percent increase in administrative expenses and 16 percent decrease in selling and promotion expenses. “The net increase is reflecting the expansion of our network, staff cost and software support to manage operational efficiencies and to build customer relationships. LFSL continues to review its marketing tactics which gave rise to a reduction in selling and promotion expenses”, Hall-Tracey said. She went on to say “During the quarter, our growth initiatives included the launch of our motorcycle loan product and the opening of our new cambio branch in Port Antonio”. The opening of the new branch would have added to administrative cost against which revenues would not cover.

The company has cash of $563 million and is generating over $200 million per year. If the company can find the formula to ramp up good quality lending successfully, the profit outlook can be transformed considerably with high profit margins for lending. “We are working on a number of initiatives that will help in the transition from lower income in foreign exchange activity” Hall-Tracey said in response to questions posed after the company released the Full year results to March. The area of credit approval is one that they is being revisited as the use of credit rating information is stymying lending. But Hall-Tracey expects profit for this year that ends March 2016 to be higher than for the year just ended, subject to taxes on profit which the company will start bearing at fifty percent of the official tax rate of 25 percent.

The company has cash of $563 million and is generating over $200 million per year. If the company can find the formula to ramp up good quality lending successfully, the profit outlook can be transformed considerably with high profit margins for lending. “We are working on a number of initiatives that will help in the transition from lower income in foreign exchange activity” Hall-Tracey said in response to questions posed after the company released the Full year results to March. The area of credit approval is one that they is being revisited as the use of credit rating information is stymying lending. But Hall-Tracey expects profit for this year that ends March 2016 to be higher than for the year just ended, subject to taxes on profit which the company will start bearing at fifty percent of the official tax rate of 25 percent.

The equity capital of Lasco is $868 million and is well below that of its two siblings who have equity in equity of more than $2.4 billion each, as such the possibility for strong growth is probably more present here than with the bigger entities over time.

The company has done well from the money remittance and cambio operations but it is in the lending that the future growth prospects seems to rest. Hence the connection between Mayberry Investments with the know-how having been exposed at Access Financial. The company has adequate free capital to increase lending with only $147 million in loans at March. Earnings per share of 0.45 cents for the quarter should end around 20 cents for the year to March 2016. The stock last traded at $1.80, investors need to keep an eye for the possibility that Mayberry Investments could increase their holdings in the company.

Profit jumps 45% at Lasco Distributors

Lasco Distributors” hot new “I Cool” drink.

“The main contributing factors to the increase revenues were the increase in volumes of iCool beverages and additional revenue from the distribution of the full range of Unilever Products”, Peter M. Chin, Managing Director reported to shareholders in the directors’ report accompanying the financial data.

“Increase logistics costs for the period and the continued aggressive selling and marketing activities resulting in the gross profit margin being lower by 1.4 percentage points than the prior year. The aggressive efforts to drive demand for our newly launched iCool brand of beverages has been successful as the company achieved a significant increase in volumes’, Chin went on to say.

Cost of sales rose 41 percent to $1.75 billion faster than revenue growth but still allowed for the strong increase in profit. Gross profit margin came out at 16.9 percent down from 18.25 percent in 2014 and declined to 17.94 percent for the 12 months to March 2015 from 19.37 percent in 2014. Administrative, selling and other expenses rose 22 percent to $441 million during the June quarter, from $361 million in 2014.

Cost of sales rose 41 percent to $1.75 billion faster than revenue growth but still allowed for the strong increase in profit. Gross profit margin came out at 16.9 percent down from 18.25 percent in 2014 and declined to 17.94 percent for the 12 months to March 2015 from 19.37 percent in 2014. Administrative, selling and other expenses rose 22 percent to $441 million during the June quarter, from $361 million in 2014.“For the reporting period Current Assets increased by 24.5 percent or $951 million. The major contributory factor was Trade and Other Receivables category which increased by 48.1 percent or $776 million, this was a result of the increased Credit Sales and Principal activities. Inventories increased by 33.6 percent or $436.7 million due to new products to market and new business agreements, Trade and Other Payables increased by 34.4 percent or $615 million over the corresponding period,” Peter M. Chin, reported.

Earnings per share ended at 4 cents, and IC Insider is forecasting 35 cents per share for the full year which would be well ahead of the 16 cents earned for the 2015 fiscal year.

While the stock is trading at $1.90 or 5.5 times current year’s earnings, making the stock attractive especially as profits are likely enjoy a big uptick in 2017 as well with more products to distribute. Investors need to bear in mind that profits become taxable at 12.5 percent starting in the second half of this fiscal year, for five years.

ICooled profits hike at Lasco Manufacturing

Lasco Manufacturing’s bottling line.

Gross profit margin for the quarter climbed to 33 percent from 29 percent in 2014 but gross profit jumped 50.50 percent well above the growth in revenues, a positive development for continued strong growth in profit going forward.

Operating Expenses climbed 29 percent to $185 while finance cost rose from $32 million to $42 million as a result of construction phase of the factory completed, resulting in the interest on the funds used in construction being expensed as opposed to being capitalised during the construction phase.

With new factory facilities completed and in use, depreciation ended at $67 million for the fiscal year up from $27 million in 2014 but is set to jump in 2016 with only a fraction of the annual charge being booked to March 2015. With more monies to be transferred to fixed assets for the year to March 2016 depreciation cost should climb. At the end of March, net book value of property, plant and equipment amounts to $3.4 billion and includes assets under construction of $1.34 billion. The cost of assets under construction will be depreciated once the property is complete and in use. The estimated additional cost of completion of the facility was $373 million at March, since then more than $150 million was added to fixed assets.

Lasco’s new I Cool drink distributed locally by Lasco Distributors, produced by Lasco Manufacturing.

At the end of the June quarter, Inventories stood at $736 million and is up from $433 million and Receivables jumped to $1.26 billion from $846 million at the end of June 2014. Borrowing stands at $1.86 million against equity capital of $5.8 billion.

IC Insider projects profit at $1.6 billion for the year or 40 cents per share for the year to March 2016, that should jump to around 60 cents for 2017. While the company becomes taxable this year capital allowances plus tax will be a 12.5 percent will result in little or no taxes being paid on profit for the year.

The company is listed on the junior market of the Jamaica Stock Exchange and last traded at $1.90 for a PE of just less than 5 based on IC Insider’s projected earnings. The stock should deliver a healthy increase in price during the fiscal year and the next as the expanded product lines and the new factory deliver increased revenues at reduced cost.

Lasco Manufacturing has been a BUY RATED stock for some time and remains with that status.

Knutsford’s sales up 38% cost 44%

Knutsford Express’ audited report for 2015 shows a big 38 percent surge in profit to $69 million over the $50 million in 2014, from revenues of $454 million, 38 percent more than the $329 million generated in 2014. With that level of revenue increase profit should have grown much faster than it did, and should have been closer to doubling.

New routes added could have been a factor as passenger traffic takes time to build up, more importantly, increased cost in a number of areas seems more the culprit. Expenses for 2015 are up 41 percent but excluding $4.58 million of IPO cost included in 2014, the increase would have been 43.5 percent. The overall increase comes against the fact that fuel rose only 12 percent to $70 million and accounted for 19 percent of cost, down from 24 percent in 2014. Excluding fuel, all other costs are up 50 percent over 2014 and 54 percent, excluding the IPO cost, well over the revenue increase of 38 percent.

Staff and labour cost jumped 72 percent to $126 million and now accounts for 34 percent of cost up from 28 percent.

Telephone cost rose 68 percent to $7.9 million. Rent grew 61 percent to $7.8 million, travelling was up 160 percent to $6 million, advertising and promotion grew only 30 percent to $12.4 million and is one of the items that grew more slowly than revenues.

Knutsford’s New Kingston depot

Some items of cost such as repairs and maintenance actually fell while others such as electricity and office supplies rose more moderately than those above.

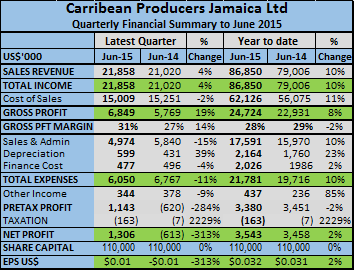

Caribbean Producers BUY RATED again

Caribbean Producers reported profit of US$3.54 million or 32 US cents per share for the year to June 2015, versus $3.46 million or 31 cents in 2014, according to the company’s audited financial statements. Sales brought in $86.85 million during the year compared with $79 million in 2014, a gain of 10 percent and for the quarter sales were up just 4 percent over 2014 to $21.86 million from $21 million in 2014 while profit came in at $1.3 million compared with a loss of $613,000 in 2014.

Caribbean Producers reported profit of US$3.54 million or 32 US cents per share for the year to June 2015, versus $3.46 million or 31 cents in 2014, according to the company’s audited financial statements. Sales brought in $86.85 million during the year compared with $79 million in 2014, a gain of 10 percent and for the quarter sales were up just 4 percent over 2014 to $21.86 million from $21 million in 2014 while profit came in at $1.3 million compared with a loss of $613,000 in 2014.

Profit for the latest quarter is 23 percent higher than the $922,000 earned in the March quarter, a period that is usually the highest earner. Earnings per share ended at 32 cents for the year or close to J$3.75.

Gross profit margin jumped in the June quarter to 31 percent and well over the 27 percent enjoyed in the 2014 quarter and higher than the 28 percent for the full year. Gross profit climbed as well by 19 percent to $6.8 million for the quarter much faster than the growth in revenues and was up by 8 percent for the year a bit less than revenue growth. Selling and administrative expenses fell in the quarter, by 15 percent but was up 10 percent for the year.

Profits seem to be moving in the right direction with cost falling in some areas and profit margin improving. At the current price of J$2.50 the stock is undervalued as it should be moving into the J$3 region with these results. The group has been seeing improvement in the St Lucian operations and that could be improved upon in 2016 fiscal year.  Caribbean Producers made a profit of $447,000 in the September 2013 quarter but made on $2,500 profit in 2014, the results for this year’s September quarter should be better as 2014 had certain cost associated with new products and the holding of prices for certain items sold to the hotel sector during that period.

Caribbean Producers made a profit of $447,000 in the September 2013 quarter but made on $2,500 profit in 2014, the results for this year’s September quarter should be better as 2014 had certain cost associated with new products and the holding of prices for certain items sold to the hotel sector during that period.

The bother continues to be the heavy debt, at $24.76 million which is down from $25.2 million in 2014, while equity is up to $19 million from $16 million in 2014 thus improving the debt to equity ratio quite a bit. The probability exists that there should be an improvement in 2016 as well, as profit continue to perform, thus building up equity.

IC Insider is restoring it BUY RATED stamp on this one.