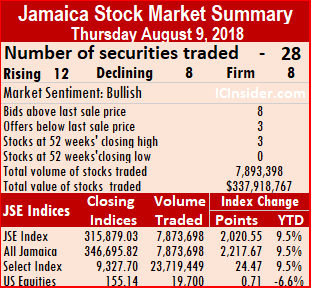

The Jamaica Stock Exchange took another sizable jump to end at a record close on Friday as advancing stocks out-numbered declining stocks in continuation of the market’s record bull run.

The Jamaica Stock Exchange took another sizable jump to end at a record close on Friday as advancing stocks out-numbered declining stocks in continuation of the market’s record bull run.

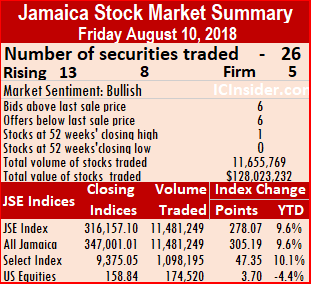

At the close trading, the All Jamaican Composite Index rose 305.19 points to 347,001.01, the first time it closed above 347,000 points and the JSE Index climbed 278.07 points to end at a record close of 316,157.10. The market has gained 9.6 percent for the year to date, the shortage of stocks and low interest rates suggest that the gain for the rest of the year should exceed that of the first 7 months.

Trading in the main market ended with 11,481,249 units valued $123,719,859 compared to 7,873,698 units valued at $335,479,879 on Thursday.

Market activities resulted in 26 securities trading including 2 in the US dollar market compared to 28 securities trading on Thursday. At the end of trading, the prices of 13 stocks rose, 8 declined and 5 traded unchanged, including Caribbean Cement trading at an intraday high of $50 and Salada Foods trading at an all-time high of $17 before pulling back at the close, to a 52 weeks’ high of $16.50.

The day’s volume was led by, Mayberry Jamaican Equities with 9,408,575 units 81.95 percent of the main market volume, followed by Scotia Group with juts 351,092 units and Jamaica Stock Exchange with 281,270 units.

Stocks with major price changes| Berger Paints rose $1 and ended at $21, trading 9,539 stock units, Caribbean Cement fell $1.49 to $42.01 exchanging 76,432 shares, Jamaica Broilers traded 46,334 stock units and dropped $3.40 to end at $22.10, Jamaica Stock Exchange rose 49 cents to close at $8, with 281,270 shares changing hands, JMMB Group rose 50 cents and ended at $30, trading 27,350 shares. Mayberry Investments lost 75 cents to end at $8.25 trading just 8,335 shares, Kingston Wharves finished at $52.25, after rising 25 cents with 3,842 stock units, NCB Financial Group lost 80 cents and ended trading at $104, exchanging 27,159 shares, PanJam Investment jumped $1 to $52 trading 87,500 stock units. Salada Foods jumped $1.50 and ended trading at 52 weeks’ closing high of $16.50, with 35,500 stock units, Scotia Group traded 351,092 units and gained 80 cents to end at $52.80 and Sygnus Credit Investments fell 49 cents in trading 12,010 at $12.

Trading in the US dollar market closed with 174,520 units valued at US$31,642 as  Proven Investments fell 1 cent and closed at 19 US cents trading 3,200 shares and Sygnus Credit Investments fell 0.25 cents in trading 12,010 at 0.0975 US cents. The JSE USD Equities Index rose 3.70 and closed at 154.43

Proven Investments fell 1 cent and closed at 19 US cents trading 3,200 shares and Sygnus Credit Investments fell 0.25 cents in trading 12,010 at 0.0975 US cents. The JSE USD Equities Index rose 3.70 and closed at 154.43

Trading resulted in an average of 478,385 units valued at an average of $5,154,994 for each security traded. In contrast to 302,835 units for an average of $12,903,072 on Thursday. For the month to date an average of 198,469 shares valued at an average of $4,438,731 versus 185,362 shares valued at an average of $5,398,127 on Thursday. July closed with an average of 169,022 units valued at $3,514,756, for each security traded.

IC bid-offer Indicator| At the end of trading, the Choice bid-offer indicator reading shows 6 stocks ended with bids higher than their last selling prices and 6 closing with lower offers.

New closing high for JSE – Friday

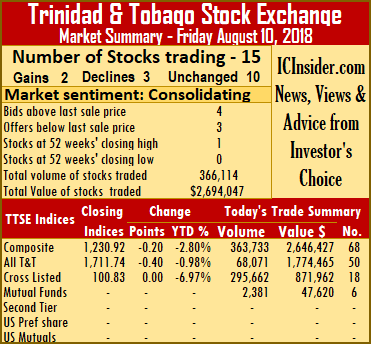

2 TTSE stocks rise 3 fall – Friday

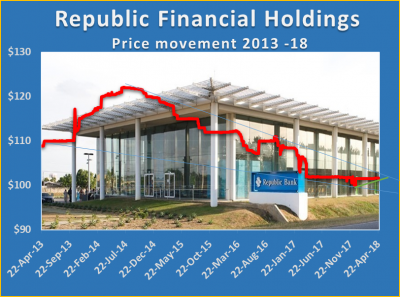

Republic Financial Holdings closes at 52 weeks’ high.

Trading on Trinidad & Tobago Stock Exchange ended on Friday with 366,114 shares valued at $2,694,047 changing hands, compared to 344,130 shares valued at $3,881,434, on Thursday.

Market activity ended with 15 securities changing hands compared to 12 trading on Friday and the market closed with 2 recording gains, 3 losses and 10 ending with prices unchanged. At the close of trading one stock ended at 52 weeks’ closing high.

At the close the Composite Index lost 0.20 points on Friday to 1,230.92, the All T&T Index declined 0.40 points to 1,711.74 and the Cross Listed Index remained unchanged at 100.83 points.

IC bid-offer Indicator| At the close of trading, the Investor’s Choice bid-offer indicator reading shows market sentiment with 4 stocks ending with higher bids than the last selling prices and 3 with lower offers.

Stocks with Gains| First Citizens rose 1 cent and ended at $35.01, after exchanging 1,228 shares and Republic Financial Holdings closed with a gain of 3 cents and completed trading at a 52 weeks’ closing high of $102.95, after exchanging 1,845 shares.

Stocks Losses| One Caribbean Media shares fell 7 cents and completed trading at $12.29, after exchanging 20,831 shares,  Trinidad & Tobago NGL share fell 1 cent and ended at $30, after exchanging 40,150 shares and Trinidad Cement shed 5 cents and completed trading at $2.90, after exchanging 100 shares.

Trinidad & Tobago NGL share fell 1 cent and ended at $30, after exchanging 40,150 shares and Trinidad Cement shed 5 cents and completed trading at $2.90, after exchanging 100 shares.

Firm Trades| Clico Investments settled at $20, with 2,381 stock units changing hands, Grace Kennedy closed at $2.90, trading 253,750 shares, Guardian Holdings concluded trading at $16.50, with 3,000 units, JMMB Group completed trading at $1.75, after exchanging 31,000 shares, Massy Holdings completed trading of 370 shares at $46.90, Point Lisas settled at $3.70, with 223 stock units changing hands, Prestige Holdings concluded trading of 200 units at $10, Sagicor Financial settled at $7.50, with 10,912 stock units changing hands, Scotiabank closed at $65.02, with 15 units and West Indian Tobacco concluded trading at $87.99, with 109 units changing hands.

Prices of securities trading for the day are those at which the last trade took place.

Derrimon buying Woodcats International

Staff at Derrimon Trading.

Derrimon Trading signed an agreement to buy Woodcats International with the transaction set to close within thirty days.

Woodcats was founded in 1999 by Christopher Collings and reached of $450 million in the 2017 financial year. products include: export pallets, warehouse pallets, wooden crates, sawdust, and landscaping mulch with in heat treatment and pallet repair.

Revenues for the Derrimon Trading first quarter March this year, climbed 27 percent to $1.94 billion above the $1.53 billion reported for the 2017 quarter and led to a big hike in profit.

The company reported a strong 45 percent jump in its first quarter results, from $35 million to $52 million or 21 cents per share to March this year, but profit could have been even higher had they not incurred finance cost which jumped 56 percent to $38 million from $25 million in 2017.

Derrimon stock traded 236,050 as high as $25 on Friday on the Jamaican Stock Exchange but ended at a record close of $24 to be up 243 percent for the year. The company is expected to approve a stock split of 10 to 1 at their upcoming annual general meeting slated for August 22.

JSE end at a new close – Thursday

The Jamaica Stock Exchange took another sizable jump to end at a record close on Thursday as advancing stocks out-numbered declining stocks in continuation of the market’s record bull run.

The Jamaica Stock Exchange took another sizable jump to end at a record close on Thursday as advancing stocks out-numbered declining stocks in continuation of the market’s record bull run.

At the close trading, the All Jamaican Composite Index jumped 2,217.67 points to 346,695.82 and the JSE Index climbed 2,020.55 points to end at a record close at 315,879.03.

Trading in the main market ended with 7,873,698 units valued at $335,479,879 compared to 3,458,733 units valued at $66,593,492 on Wednesday.

Market activities resulted in 28 securities trading including 2 in the US dollar market compared to 27 securities trading on Wednesday. At the end of trading, the prices of 12 stocks rose, 8 declined and 8 traded unchanged, including Grace Kennedy trading at an intraday high of $58 and Mayberry Investments trading at an all-time high of $9 before pulling back at the close.

The day’s volume was led by, Grace Kennedy with 5,253,678 units accounting for 66.72 percent of the main market volume,  followed by Carreras with 899,233 units or just 11.42 percent of the day’s volume and JMMB Group 7.50% preference share with 500,000 units and 6.35 percent of the day’s volume.

followed by Carreras with 899,233 units or just 11.42 percent of the day’s volume and JMMB Group 7.50% preference share with 500,000 units and 6.35 percent of the day’s volume.

Major price changes| Grace Kennedy jumped $1.01 to finish at a record high of $58.05, JMMB Group rose 40 cents ended at $29.50, trading 13,087 shares. Mayberry Investments climbed $1.60 to end a record closing high of $9 trading just 1,000 shares, Kingston Wharves finished at $52, after falling 50 cents with 3,842 stock units NCB Financial Group gained 60 cents and ended trading at $104.80, trading 27,159 shares, Sagicor Real Estate Fund rose 50 cents and settled at $14.50 exchanging 3,300 shares, Sterling Investments gained 40 cents to $14.50 after 68,200 shares traded, Scotia Group traded 351,092 units and gained $1.30 to end at $52.80 and Seprod added 99 cents to finish trading at $34, with an exchange of just 750 shares.

Trading in the US dollar market closed with 5,754 units valued at US$5,330 as JMMB Group 6% preference share  completed trading of 16,500 stock units and rose 1 cent to end at $1.05, Proven Investments fell 1 cent and closed at 19 US cents trading 3,200 shares. The JSE USD Equities Index closed unchanged at 154.43

completed trading of 16,500 stock units and rose 1 cent to end at $1.05, Proven Investments fell 1 cent and closed at 19 US cents trading 3,200 shares. The JSE USD Equities Index closed unchanged at 154.43

Trading resulted in an average of 302,835 units valued at an average of $12,903,072 for each security traded. In contrast to 138,349 units for an average of $2,663,740 on Wednesday. For the month to date an average of 185,362 shares valued at an average of $5,398,127 versus 157,082 shares valued at an average of $2,241,849 on Wednesday. July closed with an average of 169,022 units valued at $3,514,756, for each security traded.

IC bid-offer Indicator| At the end of trading, the Choice bid-offer indicator reading shows 8 stocks ended with bids higher than their last selling prices and 3 closing with lower offers.

Junior Market bounces – Thursday

The Junior Market move higher at the close of trading on Thursday rising 39.96 points to close at 3,125.61 as the number of declining and advancing stocks were equal but with a bounce in volume.

The Junior Market move higher at the close of trading on Thursday rising 39.96 points to close at 3,125.61 as the number of declining and advancing stocks were equal but with a bounce in volume.

The market closed with, 17,879,196 units valued at $94,384,927 compared to 6,775,011 units valued at $40,419,386. on Wednesday. Lasco Financial accounted for bulk of the trade with 16.75 million units.

Trading ended with 22 securities changing hands, compared to 22 on Wednesday, with just 6 advancing, 6 falling and 10 remaining unchanged. General Accident traded at a 52 weeks’ high of $3.90 but closed lower at $3.40.

IC bid-offer Indicator|At the end of trading, the Investor’s Choice bid-offer indicator reading had 7 stocks ending with bids higher than their last selling prices, 2 closed with lower offers.

Trading closed with an average of 812,691 units for an average of $4,290,224 in contrast to 307,955 units for an average of $1,837,245 on Wednesday. The average volume and value for the month to date amounts to 245,494 units valued at $1,311,926, compared to 105,288 units valued at $575,717 previous trading day. Trading in July, averaged 154,060 units valued at $655,146 for each security traded.

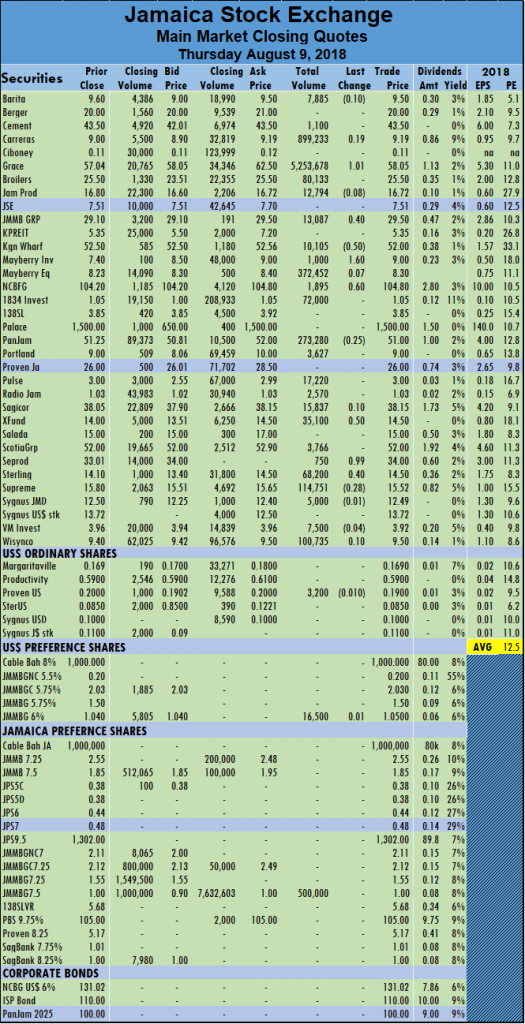

At the close of trading, Access Financial closed at $36, trading 4,041 shares, AMG Packaging ended 10 cents higher at $2, exchanging 1,200 stock units, Blue Power concluded trading at $40, with 200 units, Caribbean Producers finished trading 100,000 units but lost 27 cents at $6.50, Derrimon Trading concluded trading 15,000 shares at $23. Elite Diagnostic settled at $2.75, trading 6,000 units, Eppley ended trading 78 cents higher at $9.96, with 15,030 shares, Everything Fresh traded 96,968 shares and lost 7 cents to end at $1.91. Express Catering traded with a loss of 10 cents at $8, with 41,451 shares changing hands, FosRich Group finished trading 41,146 shares and rose 40 cents to $2.97, with shares. General Accident closed with a loss of 46 cents at $3.40, trading 27,032 stock units, Honey Bun concluded trading and rose 6 cents to $4.31, with 7,000 shares, Iron Rock finished trading at $3.15, with 50,052 shares, Jamaican Teas ended trading 5 cents higher at $4.05, with 25,091 stock units changing hands. Jetcon Corporation traded 18,720 units at $4, Lasco Distributors concluded trading 412,642 stock units, at $4, Lasco Financial finished 10 cents higher at $5.40, with 16,753,104 units, Lasco Manufacturing settled at $3.93, exchanging 40,000 shares. Main Event ended trading at $6.85, with 2,006 shares changing hands, Medical Disposables traded with a loss of 20 cents at $6, with 50,000 shares and Stationery and Office closed with a loss of 1 cent at $8.03, trading 72,513 units. In the junior market preference segment, Eppley 9.5% finished at $5.98, with 100,000 shares.

General Accident closed with a loss of 46 cents at $3.40, trading 27,032 stock units, Honey Bun concluded trading and rose 6 cents to $4.31, with 7,000 shares, Iron Rock finished trading at $3.15, with 50,052 shares, Jamaican Teas ended trading 5 cents higher at $4.05, with 25,091 stock units changing hands. Jetcon Corporation traded 18,720 units at $4, Lasco Distributors concluded trading 412,642 stock units, at $4, Lasco Financial finished 10 cents higher at $5.40, with 16,753,104 units, Lasco Manufacturing settled at $3.93, exchanging 40,000 shares. Main Event ended trading at $6.85, with 2,006 shares changing hands, Medical Disposables traded with a loss of 20 cents at $6, with 50,000 shares and Stationery and Office closed with a loss of 1 cent at $8.03, trading 72,513 units. In the junior market preference segment, Eppley 9.5% finished at $5.98, with 100,000 shares.

Prices of securities trading for the day are those at which the last trade took place.

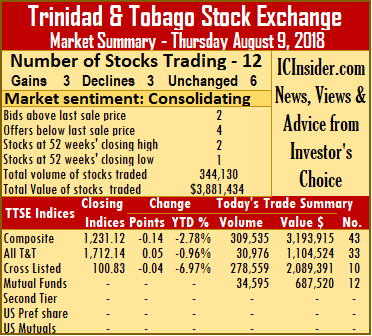

3 TTSE stocks each rise & fall – Thursday

Republic Bank traded at a 52 weeks’ high of $102.92.

Trading on Trinidad & Tobago Stock Exchange ended on Thursday with 344,130 shares valued at $3,881,434 changing hands, compared to 214,080 shares valued at $2,940,696, on Wednesday.

Market activity ended with 12 securities changing hands compared to 17 trading on Thursday, and the market closed with 3 recording gains, 3 losses and 6 ending with prices unchanged. At the close of trading two stocks ended at 52 weeks’ closing highs and one at a low.

At the close the Composite Index lost 0.14 points on Thursday to 1,231.12, the All T&T Index added 0.05 points to 1,712.14 and the Cross Listed Index lost 0.04 points to 100.83.

IC bid-offer Indicator| At the close of trading, the Investor’s Choice bid-offer indicator reading shows market sentiment with 2 stocks ending with higher bids than the last selling prices and 4 with lower offers.

Stocks with Gains| Republic Financial Holdings concluded trading of 474 shares and gained 4 cents and ended at a 52 weeks’ high of at $102.92, Scotiabank added 1 cent in completing trading at $65.02, after exchanging 5,800 units and Trinidad & Tobago NGL increased 27 cents and settled at a 52 weeks’ high of $30.01, after exchanging 8,879 shares.

Stocks Losses| First Citizens closed with a loss of 1 cent at $35, after exchanging 1,516 shares,

National Enterprises shed 50 cents and ended at a 52 weeks’ low of $9, with 2,310 stock units changing hands and West Indian Tobacco lost 1 cent and completed trading at $87.99, with 2,497 units.

Firm Trades| Ansa Merchant settled at $40, after exchanging 1,000 shares, Clico Investments ended at $20, with 34,595 stock units changing hands, First Caribbean International Bank completed trading 200 units at $8.49, National Flour ended trading 2,500 units at $1.79, One Caribbean Media concluded market activity at $12.36, after exchanging 6,000 shares and Sagicor Financial ended at $7.50, with 278,359 stock units changing hands.

Prices of securities trading for the day are those at which the last trade took place.

Profit jumps 58% at Proven

Investors in shares of PROVEN Investments pushed the price to a year’s low of 12 US cents last month but data now available suggest that they made a big mistake, as the stock now trades back at 20 US cents and profit that suffered from foreign exchange losses in the second half of 2018 fiscal year is now back up.

Investors in shares of PROVEN Investments pushed the price to a year’s low of 12 US cents last month but data now available suggest that they made a big mistake, as the stock now trades back at 20 US cents and profit that suffered from foreign exchange losses in the second half of 2018 fiscal year is now back up.

The investment bank just released first quarter results to June showing profit attributable to shareholders jumping 58.43 percent to US$1.79 million from the US$1.13 million in the same period last year. Annualized return on average equity translate to 8.56 percent and is consistent with Proven target set when they went public. The sharp jump in earnings resulted from net revenue for the quarter rising a 17.4 percent to US$8.5 million compared to US$7.25 million earned in the June 2017 quarter. According to the CEO Christopher Williams, “this was mainly due to a more efficient carry trade strategy and significant improvement in foreign exchange gains.”

Earnings per share for the quarter amounted to 0.29 US cent versus 0.20 US cents in 2017. An interim dividend of 0.25 US cent per share will be paid to shareholders on September 10.

According to the report released with the financials “spread income was the major contributor to revenue during the period, with a 16.97 percent improvement compared with the same period last year as net interest income totalled US$5.28 million. This increase reflects success in the carry trade strategy as the company was able to concurrently increase interest income while reducing interest expense by 18.30 percent.

Net foreign exchange gains totalled US$1.20 million, compared to just US$200,000 in the same period last year. While foreign exchange grew fees and commission income declined from $1.2 million to $894,000 due to change in reporting some fee income with some income now being booked over the period that they cover rather than at the time of billing, the impact for the full year should not reflect a major difference, IC Insider.com was informed.

Proven invests in a number of privately held entities except for Access Finance. The investment strategy seems to be working with most entities delivering increased returns in the quarter.

Christopher Williams, Proven Investments CEO.

According to the release Proven Wealth net income totalled US$0.93 million for the quarter, representing more than a six -times increase compared to the same period last year. The firm continues its strategy to offer investment products to clients in reducing the previous reliance on repurchase agreements. Total Assets of the company as at June 2018 stood at US$120.5 million.

Proven Fund Managers continues to be one of the top players in the Asset and Pension Fund Management and Administration business. Profitability increased by almost 68 percent compared to the same period last year, with net profit of US$220,000 compared to US$130,000 million for 2017.

Access Financial Services appears to be maturing contributing nearly 21 percent increase in net profits attributable to PIL of US$790,000 or 44 percent of the group’s profit for the quarter. But according to Williams, profit at Access is growing around $10 million on a monthly basis and is expected to continue for the rest of the fiscal year barring unforeseen negative development. IC Insider.com gathers that they may be more acquisition in the period ahead for this subsidiary in a new market. Access seems to have absorbed the acquisitions last year that led to a hike in doubtful loan provisioning being above normal in the 2018 fiscal year. The loan portfolio was US$24.4 million up 22 percent over the balance at June 2017.

BOSLIL Bank headquartered in St Lucia is Proven Investments’ most recent acquisition and currently 75 percent owned by the group. BOSLIL contribution to group profits was just below Access at US$610,000 million. Total Assets of the bank stood at US$271 million and seems set to increase as the group has signed an agreement to acquire yet another banking entity that will fall under the arm of Boslil.

PROVEN REIT is involved in residential real estate development with two new developments scheduled to commence construction and are expected to be completed and sold over the next twelve to eighteen months. But the current fiscal year is not likely to benefit from these is they are successfully executed.

Operating expenses increased by 11.5 percent to US$5.6 million compared to US$4.9 million in 2017 but the expenses include US$236,000 in preference dividends that will not repeat as the company retires the preference shares on which dividend was paid while there was just over $400,000 provision made relating to the impact of IFRS 9. Excluding these two items profit for the quarter would have been much greater than reported.

Access Financial contributed much to Proven profit in the quarter.

At the end of June total assets amounted to US$575 million down slightly from US$599 million at June 2017 and liabilities fell from US$509 million in 2017 to US$470 million. Shareholders’ Equity grew to US$82 million from US$71 million as at June 2017 mainly from increased in the share capital following the rights issue last year.

The group has not been able to put the new capital fully to work as they awaited regulatory approval for the plan acquisition of a brokerage company in Cayman Island which has now been granted with the acquisition said by Proven to close at the end of the month. That may not be the only acquisition for Proven this fiscal year as the group seek to grow its overseas business and take advantage of the many investment opportunities management sees within the region.

In going forward, investors need to pay attention to the impact of foreign exchange trading and movement in the rate of exchange and the impact on profits positively or negatively, so the strong gains enjoyed in the quarter may not repeat in the rest of the year. The preference dividend and the provision for IFRS provisioning should not repeat and are likely to reduce cost going forward. Access continues to grow profit on a quarterly basis as the company increase loans granted and securities trading can add or subtract from profits depending how well the investment portfolio is managed.

With the continued focus on acquisition, the future could be brighter for the group, in addition IC Insider.com is forecasting a rise in the PE ratio from an average of 12.5 now to a higher level by year end.

The stock that was in the IC TOP 10 and slipped out this past week traded at 19 US cents on Thursday on the JSE US dollar market and sits just outside the Top list.

Honey Bun profit up modestly in Q3

![]() Sales for the three months ended June 2018, rose 15 percent to $332 million over the 2017 out turn of $289 million at Honey Bun, but profit before tax was just $9 million, 5 percent higher than the $8.6 million earned in the corresponding prior year period.

Sales for the three months ended June 2018, rose 15 percent to $332 million over the 2017 out turn of $289 million at Honey Bun, but profit before tax was just $9 million, 5 percent higher than the $8.6 million earned in the corresponding prior year period.

Profit after tax rose to $9.7 million up from $7.55 million as a provision of $1 million in taxes in 2017 turned into $695,000 in 2018. Management stated in their release to shareholders that “this has been as a result of continued investment in production capacity and restructuring of distribution.”

Year to date, sales for the nine months, were $1 billion up 4 percent over the corresponding 2017 period’s income of $969 million, leading to profit before tax of $80 million, 17 percent lower than in the previous year. After taxation of $8.3 million for the nine months, profit declined to $72 million from $84.7 million in 2017, after taxation for $12 million.

Earnings per share for the quarter amounts to just 2 cents and for the nine months period year to date amounted to 15 cents. Honey Bun’s last quarter is not the most robust for the fiscal year so not much improvement is expected when the year ends in September.

Even as the net profit was disappointing, there were some good signs. Gross margin increased to 44.1 percent from 42.4 percent in 2017 for the June quarter and from 43.2 percent to 45.2 percent for the nine months. Gross profit rose 19 percent to $146 million for the quarter but was up 8 percent for the year to date period to $455 million.

Marketing and Distribution cost rose 32 percent in the quarter to $61 million and 37 percent to $164 million while Administrative Expenses rose 14 percent for the quarter to $63 million and was flat at $166 million for the nine months. Depreciation moved up by 9 percent to $12.3 million for the quarter and 11 percent to $36 million for the year to date.

“The Company’s asset base has grown as a result of the investment in the expanded facilities. This investment will allow the company to take advantage of the strong market demand for our products.

One Honey Bun’s Products.

In April of this year Honey Bun launched its new Buccaneer Jamaica pocket size rum cakes in 3 flavors at the Jamaica Expo. We have entered two new markets with further interest from other buyers in existing markets,” Michelle Chong Chief Executive Officer, informed shareholders.

Operations brought in $113 million in cash for the nine months of which $93 million was used as payment for fixed assets and $18.6 million in dividends resulting in $84 million in cash at the end of the period.

Shareholders’ Equity grew to $600 million at the end of June, current assets fell to $212 million and current liabilities fell to $84 million from $117 million in 2017. Fixed assets rose to $441 million from $368 million in 2017 and borrowed funds stood at just $31 million.

Seprod could ditch Duckenfield sugar

Seprod could ditch loss making Duckenfield sugar operations.

Duckenfield sugar factory in St Thomas faces closure, unless the government steps in to alleviate the problems. IC Insider.com understands a major part of the issue is a cess placed on locally produced sugar that cost the industry almost a billion per year.

The industry that is struggling to be viable is not in a position to bear the cost of the cess. Duckenfield has racked up a huge amount of losses since it was taken over by Seprod.

Seprod who operates the St Thomas based Duckenfield factory, stated in a release accompanying their six months results as they bemoan the impact that continuous losses at the factory has on the results of the group.

The report singed by the Chief executive, Richard Pandohie and Vice Chairman, Peter John Thwaites states, “Unfortunately, the Group would have had much better results had it not been for the $220 million loss in the sugar operation for the period. Management has exhausted almost all options to make these operations achieve even a breakeven status and we are committed to, in very short order, eliminating these nine years of erosion in shareholders’ value.”

For the six months ended June 2018, Seprod generated revenues of $10.44 billion, an increase of J$2.07 billion or 25 percent over the corresponding period in 2017. Net profit increased 29 percent for the period to $598 million in the 2017 period. The 2018 results are bolstered by the transfer of the former Jamaican dairy operations of Nestle within the Group effective January, this year.

Sugar cane under production in Jamaica

These operations, located in Bog Walk, St. Catherine, produce Supligen and Betty products, as well as co-manufacture products for international customers. In 2017, these operations were operated by Seprod under a management services contract and were not included in the Group’s results. The directors’ report stated that, “had these operations been included in the Group’s results in 2017, the increase in revenues for the six months ended 30 June 2018 would have been $1.20 billion or 13 percent and the increase in net profit would have been $77 million or 15 percent.”

For the June quarter, revenues rose 33 percent to $5.48 billion with gross profit rising sharply to 36 percent from 24 percent in 2017, with gross profit hitting $1.96 billion and profit after tax coming in at $325 million attributable to Seprod shareholders, 37 percent ahead of the 2017 out turn.

TTSE stock prices steady again – Wednesday

Trading on Trinidad & Tobago Stock Exchange ended on Wednesday with 214,080 shares valued at $2,940,696 changing hands, compared to 93,130 shares valued at $2,269,792, on Tuesday but closed without any price change.

Trading on Trinidad & Tobago Stock Exchange ended on Wednesday with 214,080 shares valued at $2,940,696 changing hands, compared to 93,130 shares valued at $2,269,792, on Tuesday but closed without any price change.

Market activity ended with 17 securities trading and based on the last traded price none recording a change at the close, while 12 traded on Wednesday.

At the close the Composite Index lost 2.22 points on Wednesday to 1,231.26, the All T&T Index dropped 6.72 points to 1,712.09 and the Cross Listed Index rose 0.33 points to 100.87.

IC bid-offer Indicator| At the close of trading, the Investor’s Choice bid-offer indicator reading shows market sentiment with 4 stocks ending with higher bids than the last selling prices and 6 with lower offers.

At the close of the market, Angostura Holdings completed trading of 100 shares to close at $15.75, Ansa McAl settled at $57, exchanging 445 units, Calypso Macro Index Fund traded 3,250 units at $15.95, Clico Investments completed trading at $20, with 3,596 stock units changing hands, First Caribbean International Bank settled at $8.49, exchanging 72,500 units, First Citizens concluded market activity at $35.01, after exchanging 1,982 shares, Grace Kennedy completed trading at $2.80, with 10,463 stock units changing hands, Guardian Holdings settled at $16.60, with 2,787 units, Massy Holdings ended at $46.90, after exchanging 7,330 shares, National Enterprises completed trading of 5,600 stock units at $9.50, One Caribbean Media ended at $12.36, after exchanging 9,512 shares, Point Lisas completed trading at $3.70, with 100 stock units changing hands, Republic Financial Holdings closed at $102.88, after exchanging 1,030 shares, Sagicor Financial completed trading at $7.50, with 69,959 stock units changing hands, Scotiabank settled at $65.01, with 3,534 units, Trinidad & Tobago NGL ended at $29.74, after exchanging 21,780 shares and Unilever Caribbean completed trading 112 stock units at $27.

Grace Kennedy completed trading at $2.80, with 10,463 stock units changing hands, Guardian Holdings settled at $16.60, with 2,787 units, Massy Holdings ended at $46.90, after exchanging 7,330 shares, National Enterprises completed trading of 5,600 stock units at $9.50, One Caribbean Media ended at $12.36, after exchanging 9,512 shares, Point Lisas completed trading at $3.70, with 100 stock units changing hands, Republic Financial Holdings closed at $102.88, after exchanging 1,030 shares, Sagicor Financial completed trading at $7.50, with 69,959 stock units changing hands, Scotiabank settled at $65.01, with 3,534 units, Trinidad & Tobago NGL ended at $29.74, after exchanging 21,780 shares and Unilever Caribbean completed trading 112 stock units at $27.

Prices of securities trading for the day are those at which the last trade took place.