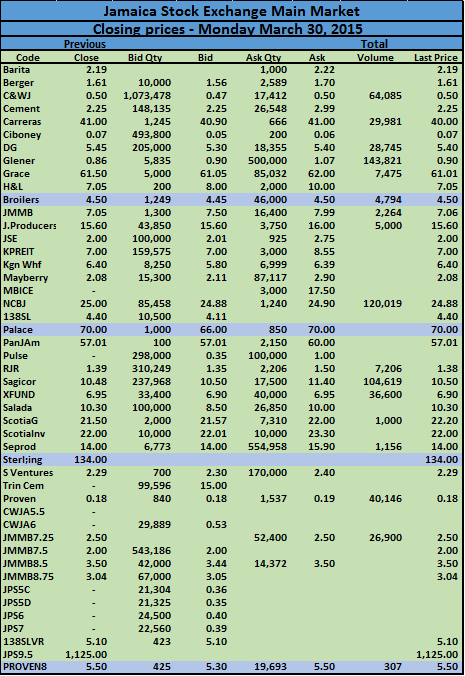

The Jamaica Stock Market started off the week on a positive note, closing at a 34 months high at the end of trading, on Monday. The JSE Market Index gained 848.12 points to 84,246.09,  the JSE All Jamaican Composite index rose 948.24 points to close at 92,909.34 and the JSE combined index climbed 805.21 points at 85,837.84. Monday’s closing All Jamaica Composite Index, is at the highest, since early June 2012.

the JSE All Jamaican Composite index rose 948.24 points to close at 92,909.34 and the JSE combined index climbed 805.21 points at 85,837.84. Monday’s closing All Jamaica Composite Index, is at the highest, since early June 2012.

A 70 cents gain in Scotia Group to close at $22.20 was the main stock that influenced the move in the indices. Jamaica Money Market had earlier traded at $7.99 cents, up 75 cents and would have also positively impacted the indices. Although the indices of the main market moved up strongly, it came out of almost even advanced declined ratio. Only 624,118 units traded in the main and US dollar markets. On a day of low volumes, the leading trades were National Commercial Bank with 120,019 shares and Sagicor Group with 104,619 units.

Near 3 years’ high for JSE on Monday

Pan Jam & Sagicor Financial better buys

I am of the view that a Jamaican investor looking to get in to SGJ would be best served by purchasing either Pan Jam or Sagicor Financial Corporation (SFC) or both.

I am of the view that a Jamaican investor looking to get in to SGJ would be best served by purchasing either Pan Jam or Sagicor Financial Corporation (SFC) or both.

Pan Jam because it is trading at a discount to equity as well as being very heavily invested in Jamaican real estate with excellent levels of occupation and with large minority positions in mostly export oriented companies. The vast bulk of its revenue is derived from SGJ as a result of the 31+% shareholding. Sagicor Group (SJ) has also recently gone in to Central America in addition to their Cayman subsidiary which acts as a hedge against further devaluation of the JA$.

SFC because it trades at a significant discount to equity as well as having most of its asset base (about 66%) outside of Jamaica and most of that in currencies which are fixed against the US$ also therefore acting as a hedge against JA$ devaluation. Further, in my view, the T&T and Barbados markets are discounting almost entirely the value of SJ which allows for better value for a Jamaican investor in SFC.

SJ itself is also trading below equity. In my view, the first attached article supports my argument for purchase of either company to get the benefit of SGJ. The second analysis done by myself in May 2011 using the approach identified in the first article attempts to identify the “true” value of SFC.

At close of trading today (Friday 10/10/2014) the market capitalisation of SJ exceeds that of SFC on a constant currency basis by TT$210,939,023 (J$3,743,302,723). I suspect that it was the recognition of this problem which caused SFC to delist from the JSE.

I am a shareholder in SFC and I live in T&T.

Roland Bynoe

Sagicor & JMMB active insider trades

A number of insider trades in JMMB shares occurred in March

A series of listed companies released information to the Jamaica Stock Exchange about each trade that took place in 2015 recently. Connected parties at Jamaica Broilers sold a total of 10,236,510 shares on January 28 and February 12. Sagicor Group had a senior manager purchasing 246,944 shares on March 18 and two senior managers purchased a total of 2,061,715 shares under during the period March 11 and March 16. The trades were done under the Executive Long Term Incentive of the group.

Insiders are buying into Sagicor Group’s vision of the future.

Pan-Jamaican Investment saw a related party purchasing 24,401,900 shares on March 6.

There were only a few sales by insiders for the various companies reporting, with Jamaica Money Market Brokers’ connected party selling 778,362 shares on March 17 and a related party selling 20,219 shares on March 16 and 211,249 on March 11. On February 24 and 25 a related party purchased 5,533,174 of the company’s shares but between March 19 and 24 a related party to a director sold 4,000,000 shares.

Scotia Group had two senior managers disposing of 53,926 shares held under the Employee Share Ownership Plan.

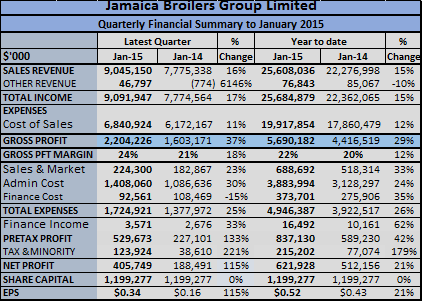

Profit looking up at Broilers

Jamaica Broilers recorded profits of $406 million for the quarter to January 2015, a 115 percent increase against the $188 million in 2014. Results for the third quarter was better than the amount earned in the first two quarters of the fiscal year combined.

Jamaica Broilers recorded profits of $406 million for the quarter to January 2015, a 115 percent increase against the $188 million in 2014. Results for the third quarter was better than the amount earned in the first two quarters of the fiscal year combined.

Profit of $622 million was earned for the nine months, 21 percent above the $512 million for the 2014 period. Earnings per stock amounted 33.8 cents for the quarter, up from 15.7 cents for the corresponding period in 2014 and 51.86 cents per stock unit versus 42.71 cents, for the nine months period. IC Insider is forecasting $1 per share earnings for the year to April and $1.50 for the next fiscal year. If the forecast is met, the stock would be selling at at PE ratio of only 4.

The group should benefit from lower cost of inputs for feed, energy and fuel cost with the decline in the price of oil. Contributing to the gains so far, is the Group’s revenue increase of 15 percent for the quarter to hit $9 billion from the $7.8 billion in the corresponding period last year. Gross profit jumped 38 percent in the quarter to $2.2 billion, $600 million above the $1.60 billion of the corresponding quarter of 2014. For the nine months, gross profit came in at $5.7 billion versus $4.4 billion, an increase of 29 percent. It was the improvement in Gross profit margin that contributed most to the improvements in profit with $370 million for the quarter coming from the increased margin.

“In this quarter, the segment reporting was changed to reflect the new geographical perspective on the Group’s operations, being Jamaica, US and Other which includes Haiti,” the company’s management informed shareholders.

“In this quarter, the segment reporting was changed to reflect the new geographical perspective on the Group’s operations, being Jamaica, US and Other which includes Haiti,” the company’s management informed shareholders.

Management went on to state that “the growth in the US Operations continues. The segment results reflect the improvement in year to date performance; now at $773 million compared to the year to date of $283 million last year-a 173 percent increase. The Operations in Jamaica have performed as anticipated, given the market environment which has resulted in depressed consumer demand and lower disposable incomes. The year to date segment results at $1.297 billion therefore reflects only a 2 percent increase over the $1.270 billion recorded last year. Revenues from the fuel terminal operations at Port Esquivel were booked in this quarter in respect of a short-term contractual arrangement. A long-term agreement is being negotiated and prospects look good due to the current shortage of storage capacity for petroleum products. In this quarter, the segment reporting was changed to reflect the new geographical perspective on the Group’s operations, being Jamaica, US and Other (which includes Haiti). Distribution, selling and administrative costs, quarter -over –quarter, essentially reflect inflation increases along with costs related to organizational strengthening and increased activities in the US Operations.”

Borrowed funds increased to $6.9 billion and cash funds also increased to $1.76 billion, while equity stands at $11.3 billion.

NCB ends at $28 in Trinidad Thursday

NCB closed up by $1.50 at $25 on Wednesday

A total of 60,000 shares were traded in Trinidad on Thursday. At the close the bid on the stock was TT$1.55 for 42,395 shares with no stock on the offer for sale

In Jamaica 184,000 unit of the stock traded between $24.10 and $25 with the majority at $25. There are only three offers on the board for 275 units at $25.50, 103,873 at $30 and 503 shares at $33.

NCB demand flows from good 2014 results with earnings of $4.73 cents per share and a hike in its dividend payments as well as robust first quarter results to December and the high level of undervaluation of the stock.

Loans grew by $8.7 billion, or 6 percent to $157 billion at the end of December last year from the similar period in 2013. Net profit of $2.1 billion, a decrease of 15 percent, or $368 million from the $2.5 billion earned in 2013 but the booking of the tax on assets was done in full in the December 2014 quarter instead of being spread over the entire year. This added $670 million to cost compared to 2013 resulting in the net profit getting a hit of roughly $400 million.

NCB reported that “gain on foreign currency and investment activities, up by $861 million. This was due to higher levels of foreign exchange income and gains from the sale of debt securities in the December 2014 quarter. Net fee and commission income, increased by $465 million or 22 percent, mainly due to Payment Services fees, related to card usage and transaction volumes, credit related fees from the growth in loans and greater corporate finance and unit trust fees, booked in the current period, net interest income, increasing by 2 percent, or $151 million, primarily due to growth in net loans and advances and investment securities portfolios.”

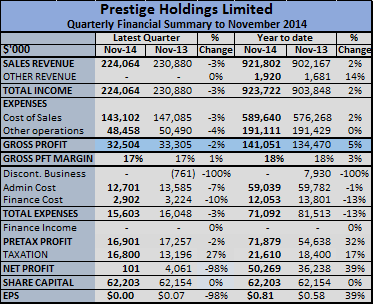

Profit up at Prestige

Prestige Holdings with its KFC, Subway, TGI Fridays and Pizza Hut franchises reported improved results for the first twelve months of the fiscal year ending November 2014, but from revenues that were virtually flat.

Prestige Holdings with its KFC, Subway, TGI Fridays and Pizza Hut franchises reported improved results for the first twelve months of the fiscal year ending November 2014, but from revenues that were virtually flat.

Cost containment below that of 2013 also helped with the improvement in the profit out turn. Group revenue increased by 2 percent for the year to TT$922 million but declined 3 percent in the last quarter to $224 million. Profit after tax increased by 39 percent for the year to $50 million but declined by 98 percent to $101,000 in the November quarter. In 2013, the company wrote off its investment in TGI Friday operations in Barbados and was hit with an $8.7 million one off charge to profit, as a result.

The company faces cost and service quality problems in Trinidad where it has its main operation due to labour shortage in that country. Looking ahead the company has 110 restaurants outlets with one in Jamaica, room for expansion may be limited in the medium term thus negating the attractiveness of the stock as an attractive investment at this stage.

The company faces cost and service quality problems in Trinidad where it has its main operation due to labour shortage in that country. Looking ahead the company has 110 restaurants outlets with one in Jamaica, room for expansion may be limited in the medium term thus negating the attractiveness of the stock as an attractive investment at this stage.

At the end of the fiscal year, Prestige had equity of $231 million and borrowing of $123 million and cash funds of $57 million. The stock sells for a PE of 12 times 2014 earnings and is likely to have limited upside potential, especially with interest rates on the rise in Trinidad.

5 months of deflation for Jamaica

Jamaica is enjoying a respite in upward price movements since October last year with the price of oil on the world market having collapsed from US$100 per barrel to hover around US$50. The country had a 0.1 percent inflation in October, but declined in each of the following months, with the latest data showing February 2015 with a 0.7 percent decline in the All Jamaica ‘All Divisions’ Consumer Price Index. This followed the fall of 0.5 percent in January. Year-to-date inflation to February 2015, is -1.1 percent and since November last year the decline is 2 percent.

Jamaica is enjoying a respite in upward price movements since October last year with the price of oil on the world market having collapsed from US$100 per barrel to hover around US$50. The country had a 0.1 percent inflation in October, but declined in each of the following months, with the latest data showing February 2015 with a 0.7 percent decline in the All Jamaica ‘All Divisions’ Consumer Price Index. This followed the fall of 0.5 percent in January. Year-to-date inflation to February 2015, is -1.1 percent and since November last year the decline is 2 percent.

The Statistical Institute of Jamaica (Statin) indicated that the “main contributor to the decline, was a 3.6 percent decrease in the index for the division ‘Housing, Water, Electricity, Gas and Other Fuels’ resulting from lower rates for electricity and water. The reduction was tempered by an upward movement in the wages for carpenters, masons, plumbers, painters and electricians during the month. Also contributing to the decline was a 0.6 percent fall in ‘Food and Non-Alcoholic Beverages’, the heaviest weighted division. All other divisions recorded movements of below 0.5 percent.”

Increase were experienced by certain categories with ‘Alcoholic Beverages and Tobacco’ increasing by 0.3 percent, ‘Clothing and Footwear’ 0.2 percent, ‘Furnishings, Household Equipment and Routine Household Maintenance’ 0.3 percent ‘Health’ 0.4 percent, ‘Transport’ 0.1 percent, ‘Recreation and Culture’ 0.3 percent and ‘Miscellaneous Goods and Services’ 0.2 percent. ‘Communication’, ‘Education’ and ‘Restaurants and Accommodation Services’ recorded negligible movement for the period under review, Statin stated.

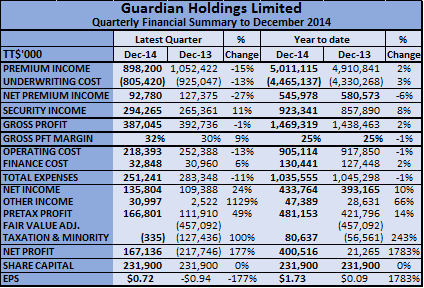

Profit up at Guardian Holdings

Profit climbed for Guardian Holdings for 2014, resulting in a profit after tax attributable to shareholders of $401 million, an increase from only $20 million in 2013.

Profit climbed for Guardian Holdings for 2014, resulting in a profit after tax attributable to shareholders of $401 million, an increase from only $20 million in 2013.

Based on the improved results the company announced an increase in its dividend. The 2013 profit was negatively affected by a write down of $457 million in the assets of Pointe Simon development. Consequently, earnings per share for 2014 are $1.73 as compared to 20 cents in 2013. Profit before the 2013 write down of Pointe Simon asset, increased by 14 percent to $481 million. Net income before operating expenses was flat at $1.469 billion. Operating cost fell slightly to $905 million and finance cost rose moderately to $130 million. Net Income from Insurance Underwriting Activities fell from $581 million in 2013 to $546 million in 2014.

For the December quarter, profit before tax rose 49 percent from lower underwriting profit, higher investment and other income and a 13 percent reduction in operating cost.

“The drop in net Income from Insurance Underwriting Activities is as a result of adverse claims experience in our health and general insurance business as well as actuarial strengthening of reserves in some lines. It should be noted that neither of these factors is structural and we expect that they would have no material impact on performance going forward as they resulted from normal statistical volatility in our business the group’s” management said in a statement accompanying the results.

Our portfolio of financial service companies diversified across lines of insurance and geographies together with our diversified investment portfolio has withstood operating volatility and provided strong overall performance, generating a Return on Equity of 13.7 percent.

Looking forward, investment income should benefit from interest rates that are on the increase in Trinidad and should be up in the USA before long. Operating cost should decline for the year based on the out turn for the December quarter that should carry over into 2015. The company states that it has moved away from investment type insurance to the traditional type cover and that the shift will generate higher margins for them.

Looking forward, investment income should benefit from interest rates that are on the increase in Trinidad and should be up in the USA before long. Operating cost should decline for the year based on the out turn for the December quarter that should carry over into 2015. The company states that it has moved away from investment type insurance to the traditional type cover and that the shift will generate higher margins for them.

“Confident in the fact that our negative legacy issues which have plagued us over recent years have been resolved, and given our solid business franchises and significant market positions throughout the region, your board of directors, after many years of flat dividend payment, has decided to increase the total dividend per share by 9.6 percent to fifty-seven (57) cents. Consequently, further to the interim dividend of seventeen (17) cents, the final dividend will be forty (40) cents and will be paid to shareholders on record on March 25, 2015” Management concluded.

The stock at $13.50 on the Trinidad Stock exchange is undervalued and ought to be priced higher. IC Insider’s Buy Rating remains in place with earnings likely to reach $2.50 per share in 2015.

Witco 2014 profit up 19%

West Indian Tobacco reported profit before taxation of TT$655 million, after earning TT$219 million in the final quarter ending December, last year, and an increase of 18 percent over the 2013.

West Indian Tobacco reported profit before taxation of TT$655 million, after earning TT$219 million in the final quarter ending December, last year, and an increase of 18 percent over the 2013.

Profit after taxation for the year amounted to TT$489 million, 19 percent increase over 2013. Revenues increased from $1.185 billion to $1.25 billion.

Cost of sales improved in the 2014 quarter raising gross profit to $784 million versus $701 million. Other costs of operation declined for the year with distribution cost declining from $18 million to $13 million and administrative expenses reaching $89 million in 2014 compared with $95 million in 2013. Other operating expenses fell to $27 million from $33 million.

The company earned $5.81 per share for the year to December and paid out $5.51 in dividend. A price adjustment, made in the latter part of 2014 is set to help push dollar sales and move profits up for 2015. IC Insider is projecting earnings of $6.50 per share for 2015. The stock trades at $125.03 on the Trinidad and Tobago Stock Exchange.

FCIB profit up but

First Caribbean International Bank’s profit rose in the first quarter ending in February, but this was mainly due to reduction in loans loss provisioning than an improvement in revenues. Loans declined and so did interest earned on loans.

First Caribbean International Bank’s profit rose in the first quarter ending in February, but this was mainly due to reduction in loans loss provisioning than an improvement in revenues. Loans declined and so did interest earned on loans.

Loans fell to US$5.996 billion down from $6.28 billion in January 2014 and $6.14 billion at the end of October last year. The bank, operating across the Caribbean region, reported interest income of US$108.7 million for the latest quarter. In 2014, interest income was $116.6 million. Other operating income of $41.8 million was earned in 2015 versus $42.5 million in 2014. The bank enjoyed a better loan loss experience with a charge of $15.7 million, in the latest quarter compared to $30.6 million in 2014. Operating expenses declined to $85 million from $89 in 2014. The bank profit after tax amounted to $26.6 million versus $15.4 million for 2014.

The bank needs to increase quality loans if it is to have enjoy sustainable growth going forward, this is a difficult challenge for a bank operating across an economically distressed region. At a price of TT$5.03 the stocks trades around 10 times current year’s earnings and that is lower than the other banking stocks on the Trinidad Stock Exchange.