The Orchid property being developed that should add to Jamaican Teas’ profits in 2015 & 2016.

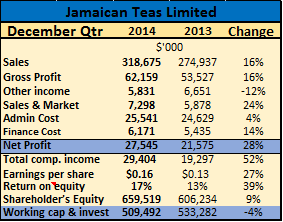

Sales were helped by 91 percent jump in exports, moving from $55 million to $103 million. The increase in exports, relate mainly to supplies to the US market and is partially due to the appointment of a new Distributor for the North East USA and expect that this will result in further improvement in sales. Revenues for the group, in the prior year, included $21.75 million in Real Estate sales. Excluding these sales, revenues would be up 26 percent for the quarter. Group sales also benefited from the launch of four new products during the period. Sales for Supermarkets are up 9 percent compared to the comparative quarter, in 2013, however, profits are flat. The jointly owned Supermarket in Montego Bay showed a reduction in losses which was helped by certain actions taken to reduce cost in 2014.

Gross profit margin increased to 24.3 percent from 24 percent in 2013, while gross profit increased 16 percent to $62 million but cost rose in other areas, with marketing climbing 24 percent to $7.3 million, administration by only 4 percent to $25.5 million and finance used to generate revenues in the period, is up 14 percent to $6.2 Million.

Property Development| The group has completed construction of more than 50 percent of units in phase 1 of the development in Yallahs, St Thomas. Approximately a half of the units in the first phase have been sold, delivery to the purchasers should start in April. The group should enjoy increased profits from this development which should start reflecting in the June quarter.

Property Development| The group has completed construction of more than 50 percent of units in phase 1 of the development in Yallahs, St Thomas. Approximately a half of the units in the first phase have been sold, delivery to the purchasers should start in April. The group should enjoy increased profits from this development which should start reflecting in the June quarter.Borrowed funds stand at $320 million including long term debt of $228 million and equity capital at $660 million.

Barring any unforeseen developments, 2015 could produce the best financial performance far. The stock which is now at $2.55 seems to have much room for growth.