Tropical Battery reported stunning first quarter results to December, with profits surging 198 percent from just $19 million in 2020 to $56.7 million as revenues jumped 46.8 percent to $662 million and encouraging investors to react positively to the surprising numbers right out of the block by driving the price up 18 percent for the day of the release and 37 percent for the year to date.

Earnings per share climbed from 1.5 cents to 4.4 cents for the quarter.ICInsider.com forecast is for profit of $280 million, with earnings per share of 22 cents, for the year to September, more than five times 2021 full year earnings, with potential for the price to deliver gains of 153 percent.

Earnings per share climbed from 1.5 cents to 4.4 cents for the quarter.ICInsider.com forecast is for profit of $280 million, with earnings per share of 22 cents, for the year to September, more than five times 2021 full year earnings, with potential for the price to deliver gains of 153 percent.

Battery Sales jumped 52 percent from $389 million in the 2020 December quarter to $591 million while Tyre Sales rose from $6.5 million to $8 million and Accessories contributed $67 million compared to $60 million in 2020, just 11 percent more.

The big push in sales was facilitated by a recovery in the local economy but importantly, increased inventory levels that doubled from $434 million at the end of December 2021 to $873 million which is up from $609 million at the end of September last year, would have played a big role in increasing revenues. The increase in sales “was achieved through an increase in balanced inventory arrivals and a tremendous effort on the part of our sales team to surpass targets by bringing in new customers,” the company managing director and deputy managing director advised in their interim report to shareholders.

Other Income slipped 14 percent to $2.6 million and interest Income dropped 39 percent to $3.6 million.

Improvement in profit margin remained at 30 percent for both quarters and resulted in gross profit rising 44 percent to $196 million from $136 million in 2020 as cost of sales rose just ahead of the increase in revenues.

Administrative expenses rose 10 percent to $114 million in the quarter from $104 million in 2020. Depreciation charges jumped 79 percent to $16 million. Finance costs rose 13 percent, to $15 million from $13.5 million in 2020.

Tropical Battery line of products

The operation generated gross cash flow of $73 million but ended up with negative inflows of $30 million after increase in working capital and addition to fixed assets and ended with cash funds of $144 million. At the end of the quarter, current assets rose to $1.6 billion from $1.09 billion in 2020 while current liabilities moved from $343 million at the end of December 2020 to $679 million, leaving net current assets at $933 million. Payables rose to $564 million from $223 million at the end of 2020, at the same time shareholders’ equity stands at $883 billion with borrowings at $568 million.

“With our more-than-adequate levels of inventory, we see a bright year ahead. We are also currently expanding our top-selling retail store, located on Grove Road, just off Half Way Tree Road in Kingston, which will allow us to increase sales at this location even further, and achieve higher profitability, given that retail margins are better than our wholesale margins while offering greater comfort and convenience for our team members and customers with a substantial increase in square footage. We plan to increase our retail presence island-wide in the coming quarters. The company rolled out new products in the quarter and plan to launch more in the March quarter”, the company stated in a report to shareholders, jointly signed by Alexander Melville, Managing Director and Daniel Melville Deputy Managing Director.

The stock traded at $1.74 on the Junior Market of the Jamaica Stock Exchange with a PE ratio of just 8 times 2022 earnings compared to an average of over 19 for the market and sits at the top of ICTOP10 Junior Market listing.

The growth in the

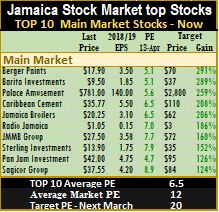

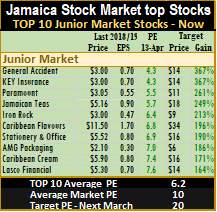

The growth in the At the end of April last year, the average PE for the Junior Market was 13 and 16.5 for the Main Market. At the end of June it was 13 and 17 respectively and September 12 and 15.5 times.

At the end of April last year, the average PE for the Junior Market was 13 and 16.5 for the Main Market. At the end of June it was 13 and 17 respectively and September 12 and 15.5 times. Persons interested in investing in stocks should open an account at a brokerage company so they can start investing when they decide to take the plunge.

Persons interested in investing in stocks should open an account at a brokerage company so they can start investing when they decide to take the plunge.

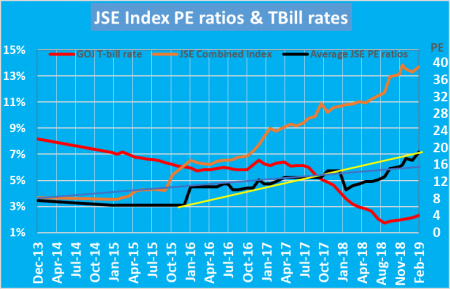

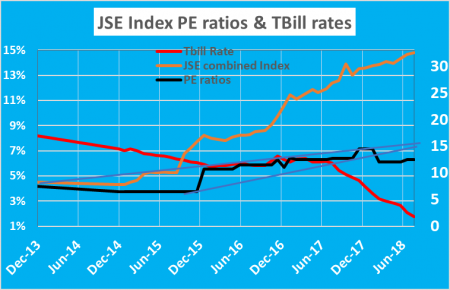

The stock market combined index climbed from 82,934.95 points at the end of 2013 to 324,801.52 on Friday, for increase of 292 percent but the average PE ratio has moved from 7.3 by just under 100 percent to peak at an average of 14.5 times last year December.

The stock market combined index climbed from 82,934.95 points at the end of 2013 to 324,801.52 on Friday, for increase of 292 percent but the average PE ratio has moved from 7.3 by just under 100 percent to peak at an average of 14.5 times last year December. The other factor is that interest rates have fallen faster in 2018 than for some time, investors seem to need more time to digest the rapid change in rates and determine how long it likely to remain at very low levels.

The other factor is that interest rates have fallen faster in 2018 than for some time, investors seem to need more time to digest the rapid change in rates and determine how long it likely to remain at very low levels.

In 2018, there will also be greater emphasis on building out exports by targeting new markets in Central America and the Greater CARICOM region,” the Managing Director reported.

In 2018, there will also be greater emphasis on building out exports by targeting new markets in Central America and the Greater CARICOM region,” the Managing Director reported.

The question of the week comes from one of IC Insider.com’s readers. “ I’m trying to understand more about investing and would like to know about buying stocks at the IPO price, selling when they go up and then buying when the prices settles lower? Does it make sense to do so?

The question of the week comes from one of IC Insider.com’s readers. “ I’m trying to understand more about investing and would like to know about buying stocks at the IPO price, selling when they go up and then buying when the prices settles lower? Does it make sense to do so?

reported in the interim results are wrong and in effect understated as the number of shares used in the computation is overstated. Instead of earnings per share of 25 cents for the half year it is 27.7 cents and for the 2016 period 26.8 cents and not 21 cent. The earnings for the 2016 April quarter, is 17.2 cents and for the full 2016 fiscal year 23.5 cents.

reported in the interim results are wrong and in effect understated as the number of shares used in the computation is overstated. Instead of earnings per share of 25 cents for the half year it is 27.7 cents and for the 2016 period 26.8 cents and not 21 cent. The earnings for the 2016 April quarter, is 17.2 cents and for the full 2016 fiscal year 23.5 cents.