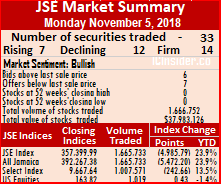

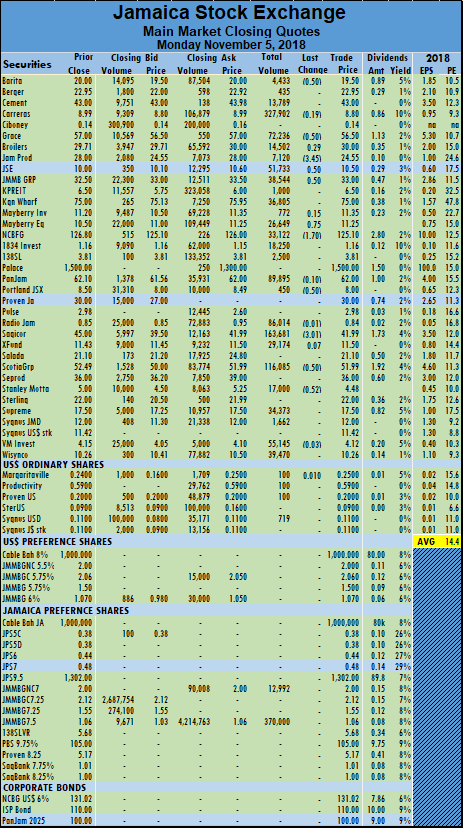

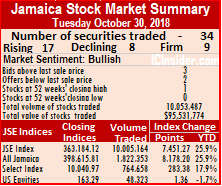

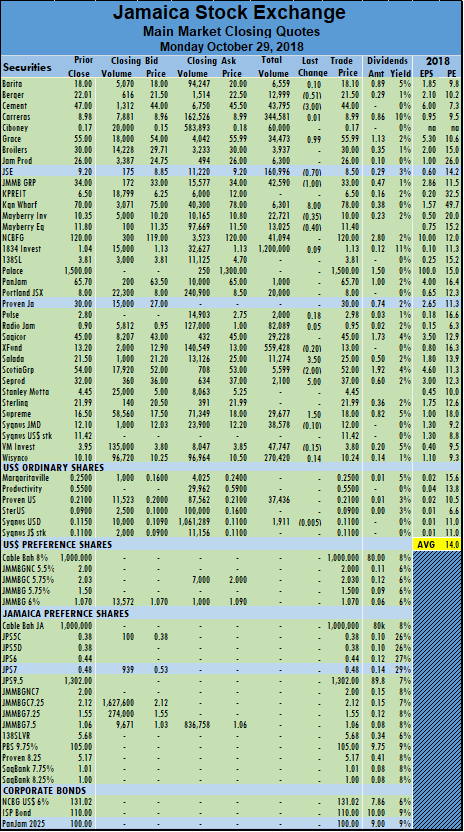

The volume of stocks trading on the Jamaica Stock Exchange slipped further on Tuesday, leading to more stocks falling than rising and resulting in another fall in the market indices.

The volume of stocks trading on the Jamaica Stock Exchange slipped further on Tuesday, leading to more stocks falling than rising and resulting in another fall in the market indices.

At the close of market activity, the prices of 9 securities rose, 12 declined, while 9 remained unchanged, with the All Jamaica Composite Index dropping another 3,094.77 points after falling more than 5,400 points on Monday to close at 389,172.61 and the JSE Index diving 2,819.68 points to close at 354,580.31.

Trading closed with 30 active securities in the main and US dollar markets, on Tuesday compared to 33 on Monday with 2,572,843 units valued at $35,216,901 changing hands compared with 1,665,733 units valued at over $37,959,691 being exchanged, on Monday.

Main market trading closed with Victoria Mutual Investments leading with 1,026,110 units, or 39.9 percent of the day’s volume and Wisynco Group with 1,006,114 units and 39.1 percent of volume traded.

Main market trading closed with Victoria Mutual Investments leading with 1,026,110 units, or 39.9 percent of the day’s volume and Wisynco Group with 1,006,114 units and 39.1 percent of volume traded.

IC bid-offer Indicator|At the end of trading, the Choice bid-offer indicator reading shows just 2 stocks ending with bids higher than the last selling prices and 7 closing with lower offers.

Trading resulted in an average of 95,290 units valued at over $1,304,330 in contrast to 57,439 shares valued at $1,308,955 on Monday. The average volume and value for the month to date amounts to 539,060 valued at $2,116,944, compared to 681,700 valued at $2,378,141. October closed, with an average of 290,851 shares, valued $5,213,901, for each security traded.

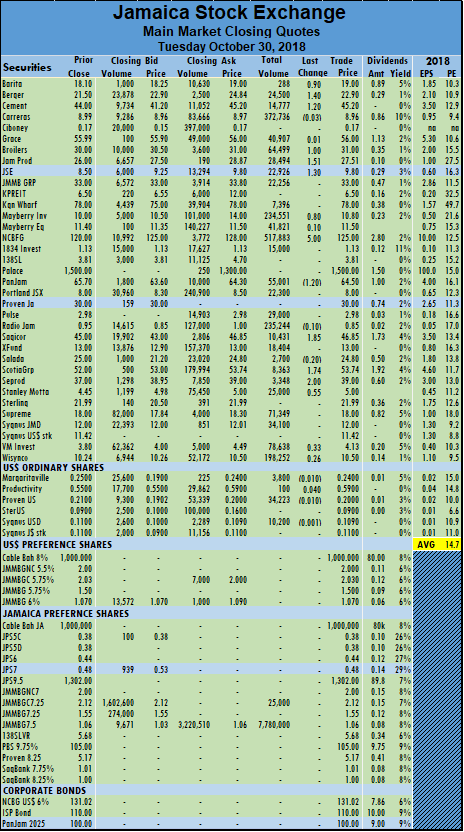

In the main market activity, Caribbean Cement gained $1 to close at $44 in closing trading of 2,602 shares, Grace Kennedy rose 50 cents and ended trading 17,355 shares to close at $57, JMMB Group gained $1 to end at $34,  trading 27,735 shares, Kingston Wharves gained 95 cents to close at $75.95 with 4,281 stock units trading, Mayberry Investments lost $1.35 to settle at $10, in exchanging 20,365 units, Mayberry Jamaica Equities traded 17,367 units but fell 75 cents to close at $10.50, NCB Financial Group climbed $1.90 and ended trading 50,470 shares to close at $127, Proven Investments traded 15,000 shares in the Jamaica market and lost $3 to close at $27, Sagicor Group dropped $2.99 to settle at $39, with 29,976 shares, Scotia Group lost 79 cents to end at $51.20, trading 93,113 units, Sterling lost $1.50 to close at $20.50 trading a mere 140 units and Sygnus Investments traded 68,100 shares after falling $1 to end at $11.

trading 27,735 shares, Kingston Wharves gained 95 cents to close at $75.95 with 4,281 stock units trading, Mayberry Investments lost $1.35 to settle at $10, in exchanging 20,365 units, Mayberry Jamaica Equities traded 17,367 units but fell 75 cents to close at $10.50, NCB Financial Group climbed $1.90 and ended trading 50,470 shares to close at $127, Proven Investments traded 15,000 shares in the Jamaica market and lost $3 to close at $27, Sagicor Group dropped $2.99 to settle at $39, with 29,976 shares, Scotia Group lost 79 cents to end at $51.20, trading 93,113 units, Sterling lost $1.50 to close at $20.50 trading a mere 140 units and Sygnus Investments traded 68,100 shares after falling $1 to end at $11.

Trading in the US dollar market ended with 55,380 units valued at $16,074. At the close of the market,JMMB Group 5.75% percent preference share completed trading of 3,880 and lost 1 cents to end at $2.05, Proven Investments traded 27,500 units at 20 US cents and Sygnus Credit Investments US dollar based ordinary share, traded 24,000 units at 11 US cents. The JSE USD Equities Index closed unchanged at 163.74.

Big fall for JSE on Monday

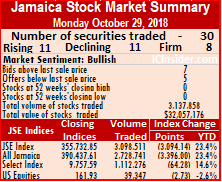

The volume of stocks trading on the Jamaica Stock Exchange declined to very low levels on Monday, leading to more stocks falling than rising and resulting in a big drop in the market indices.

The volume of stocks trading on the Jamaica Stock Exchange declined to very low levels on Monday, leading to more stocks falling than rising and resulting in a big drop in the market indices.

At the close of market activity, the prices of 7 securities rose, 12 declined, while 14 remained unchanged, with the All Jamaica Composite Index dropping 5,472.20 points to 392,267.38 and the JSE Index diving 4,985.79 points to close at 357,399.99. On Friday, the stock exchange released incorrect closing indices which have not been corrected for Friday’s report so far.

Trading closed with 33 active securities in the main and US dollar markets, on Monday compared to 30 on Friday with 1,665,733 units valued at over $37,959,691 changing hands compared with 2,082,014 units valued at $42,778,375 being exchanged, on Friday.

Main market trading closed with JMMB Group 7.5% preference share leading with 370,000 units, or 22 percent of  the day’s volume, Carreras with 327,902 units and 19.7 percent of volume traded and Sagicor group with 163,681 units with 10 percent of the day’s volume.

the day’s volume, Carreras with 327,902 units and 19.7 percent of volume traded and Sagicor group with 163,681 units with 10 percent of the day’s volume.

IC bid-offer Indicator|At the end of trading, the Choice bid-offer indicator reading shows 6 stocks ending with bids higher than the last selling prices and 7 closing with lower offers.

Trading resulted in an average of 57,439 units valued at over $1,308,955, in contrast to 77,112 shares valued at $1,584,384 on Friday. The average volume and value for the month to date amounts to 681,700 valued at $2,378,141, compared to 1,010,856 shares, valued $2,941,894. October closed, with an average of 290,851 shares, valued $5,213,901, for each security traded.

In the main market activity, Barita Investments lost 50 cents and closed trading of 4,433 shares at $19.50, Grace Kennedy lost 50 cents and ended trading 72,236 shares to close at $56.50, Jamaica Broilers traded 14,502 stock units, at $30, after rising 29 cents, Jamaica Producers dropped $3.45 and finished trading of 7,120 units at $24.55, Jamaica Stock Exchange rose 50 cents to close at $10.50, in exchanging 51,733 shares, JMMB Group gained 50 cents to end at $33, trading 38,544 shares, Kingston Wharves lost 95 cents to close at $75 with 2,792 stock units trading, Mayberry Jamaica Equities traded 26,649 units and rose 75 cents to close at $11.25, NCB Financial Group lost $1.70 and ended trading 33,122 shares to close at $125.10. Portland JSX declined by 50 cents and ended at $8, with 450 units changing hands, Sagicor Group dropped $3.01 to settle at $41.99, with 163,681 shares, Scotia Group lost 50 cents to end at $51.99, trading 116,085 units and Stanley Motta traded 17,000 shares after falling 52 cents to end at $4.48.

to end at $33, trading 38,544 shares, Kingston Wharves lost 95 cents to close at $75 with 2,792 stock units trading, Mayberry Jamaica Equities traded 26,649 units and rose 75 cents to close at $11.25, NCB Financial Group lost $1.70 and ended trading 33,122 shares to close at $125.10. Portland JSX declined by 50 cents and ended at $8, with 450 units changing hands, Sagicor Group dropped $3.01 to settle at $41.99, with 163,681 shares, Scotia Group lost 50 cents to end at $51.99, trading 116,085 units and Stanley Motta traded 17,000 shares after falling 52 cents to end at $4.48.

Trading in the US dollar market ended with, Margaritaville rose by 1 cent and ended at 25 cents with 100 shares and Productivity Business completed trading 100 shares at 59 cents, Proven Investments traded 100 units at 20 US cents and Sygnus Credit Investments US dollar based ordinary share traded 719 units at 11 US cents. The JSE USD Equities Index rose 0.43 points at 163.82.

JSE enjoyed modest gains on Friday

Trading on the Jamaica Stock Exchange resulted in more stocks rising than falling leading to a moderate pick up in the market indices as trading levels declined sharply.

Trading on the Jamaica Stock Exchange resulted in more stocks rising than falling leading to a moderate pick up in the market indices as trading levels declined sharply.

At the close of market activity, the prices of 11 securities rose, 9 declined, while 10 remained unchanged, leading the All Jamaica Composite Index to rise 832.12 points to close at 397,739.58 and the JSE Index gained 758.16 points to end at 362,385.78. The closing indices are different than the ones released by the stock exchange that is much lower than the close on Thursday.

Trading closed with 30 active securities in the main and US dollar markets, on Friday compared to 29 on Thursday. Trading closed with 2,082,014 units valued at $42,778,375 compared with 53,515,060 units valued $119,025,805 changing hands, on Thursday.

Main market trading closed with Carreras leading with 440,416 units trading, or 21 percent of the day’s volume, Scotia Group with 392,361 units and 19 percent of volume traded and Radio Jamaica with 259,000 units with  12.4 percent of the day’s volume.

12.4 percent of the day’s volume.

IC bid-offer Indicator|At the end of trading, the Choice bid-offer indicator reading shows 7 stocks ending with bids higher than the last selling prices and 4 closing with lower offers.

Trading resulted in an average of 77,112 units valued at over $1,584,384, in contrast to 1,911,252 shares valued at $4,250,922 on Thursday. The average volume and value for the month to date amounts to 1,010,856 shares, valued $2,941,894. October closed, with an average of 290,851 shares, valued $5,213,901, for each security traded.

In the main market activity, Caribbean Cement gained up $1.79 trading 1,055 shares to close at $43, Grace Kennedy rose $2 and ended trading with 27,576 shares at $57, Jamaica Broilers traded 19,491 stock units, at $29.71, after  falling 29 cents, Jamaica Producers jumped $3.49 and finished trading 7,040 units at $28, Jamaica Stock Exchange dropped $1.50 to close at $10, in exchanging 207,374 shares, JMMB Group gained 48 cents to $32.50, trading 17,573 shares, Kingston Wharves lost 95 cents to close at $75 with 2,792 stock units trading, Mayberry Jamaica Equities traded 25,925 units but lost $1 to close at $10.50, Scotia Group gained $1.46 to $52.49, trading 392,361 units.

falling 29 cents, Jamaica Producers jumped $3.49 and finished trading 7,040 units at $28, Jamaica Stock Exchange dropped $1.50 to close at $10, in exchanging 207,374 shares, JMMB Group gained 48 cents to $32.50, trading 17,573 shares, Kingston Wharves lost 95 cents to close at $75 with 2,792 stock units trading, Mayberry Jamaica Equities traded 25,925 units but lost $1 to close at $10.50, Scotia Group gained $1.46 to $52.49, trading 392,361 units.

Trading in the US dollar market ended with, JMMB Group 5.75 percent preference share rising 3 cents exchanging 1,700 shares at $2.06, Proven Investments traded 4,360 units changing hands at 20 US cents and Sygnus Credit Investments US dollar based ordinary share traded 11,820 units at 11 US cents. The JSE USD Equities Index rose 0.09 points at 163.39.

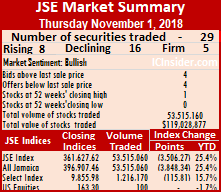

JSE starts November with a big fall

Having risen strongly on the last trading day for October, the Jamaica Stock Exchange slipped back to normal on Thursday with stocks giving back most of the gains of the previous day, in keeping with patterns seen at month ends and openings, going back several years.

Having risen strongly on the last trading day for October, the Jamaica Stock Exchange slipped back to normal on Thursday with stocks giving back most of the gains of the previous day, in keeping with patterns seen at month ends and openings, going back several years.

Trading closed with 29 active securities in the main and US dollar markets, on Thursday compared to 33 on Wednesday. Prices of 8 securities rose, 16 declined, while 5 remained unchanged. At the end of market activity, the All Jamaica Composite Index dropped 3,848.34 points to close at 396,907.46 and the JSE Index dived 3,506.27 points to end at 361,627.62.

Trading closed with 53,515,060 units valued $119,025,805 compared with 36 6,766,220 units valued at $113,213,380 changing hands, on Wednesday.

Main market trading closed with 1834 Investments leading with 50,001,500 units trading, or 93.4 percent of the day’s volume, Mayberry Jamaican Equities with 1,029,435 units and 1.9 percent of volume traded and Ciboney with 764,000 units with 1.4 percent of the day’s volume.

IC bid-offer Indicator|At the end of trading, the Choice bid-offer indicator reading shows 4 stocks ending with bids higher than the last selling prices and 4 closing with lower offers.

Trading resulted in an average of 1,911,252 units valued at over $4,250,922, in contrast to 225,541 shares valued at $3,773,779 on Wednesday. October closed, with an average of 290,851 shares, valued $5,213,901, for each security traded.

In the main market activity, Barita Investments gained $1 to close at $20, with 6,375 shares changing hands, Caribbean Cement gave up $2.79 trading 7,157 shares to close at $41.21, Grace Kennedy lost $1 and ended trading with 45,770 shares at $55, Jamaica Broilers traded 28,064 stock units, at $30 after falling $1, Jamaica Producers dropped $2.99 and finished trading 26,432 units, at $24.51, Jamaica Stock Exchange jumped $1.50 to close at a 52 weeks’ high of $11.50, exchanging 73,099 shares, JMMB Group fell $1.78 and ended at $32.02, trading 127,582 shares, Kingston Wharves gained 95 cents and finished at $75.95 with 24,474 stock units trading, NCB Financial Group added 80 cents and ended trading 160,771 shares to close at $126.80, PanJam Investment closed with a loss of $2.01 to end at $61.99, trading 14,135 stock units, Sagicor Group settled at $45 after falling $1.85, with 7,156 shares traded, Sagicor Real Estate Fund lost 57 cents to settle at $11.43, exchanging 239,704 shares, Salada Foods ended trading just 258 stock units and dropped $3.70 to end at $21.10, Scotia Group fell $1.97 to $51.03, trading 122,623 units and Supreme Ventures dropped $2.26 to close at $17.54 with 197,166 shares changing hands.

Kingston Wharves gained 95 cents and finished at $75.95 with 24,474 stock units trading, NCB Financial Group added 80 cents and ended trading 160,771 shares to close at $126.80, PanJam Investment closed with a loss of $2.01 to end at $61.99, trading 14,135 stock units, Sagicor Group settled at $45 after falling $1.85, with 7,156 shares traded, Sagicor Real Estate Fund lost 57 cents to settle at $11.43, exchanging 239,704 shares, Salada Foods ended trading just 258 stock units and dropped $3.70 to end at $21.10, Scotia Group fell $1.97 to $51.03, trading 122,623 units and Supreme Ventures dropped $2.26 to close at $17.54 with 197,166 shares changing hands.

Trading in the US dollar market ended with Margaritaville being the only stock trading to end with a mere 100 units changing hands at 24 US cents. The JSE USD Equities Index remained unchanged at 163.30.

JSE up 27% with net gains in October

The Jamaica Stock Exchange hit several new highs in October but closed the month with a net gain of 7,478.51 points on the All Jamaica and 6,813.78 points on the JSE index leading to gains of 26.6 percent for the first 10 months of the year.

The Jamaica Stock Exchange hit several new highs in October but closed the month with a net gain of 7,478.51 points on the All Jamaica and 6,813.78 points on the JSE index leading to gains of 26.6 percent for the first 10 months of the year.

Trading closed with 33 active securities in the main and US dollar markets, on Wednesday compared to 34 on Tuesday.

The market ended with the prices of 12 securities rising, 9 declining while 12 remained unchanged leading to the All Jamaica Composite Index climbing 2,139.99 points to close at 400,755.80 and the JSE Index rising 1,949.77 points to close at 365,133.89.

Trading closed with 6,766,220 units valued at $113,213,380 trading, compared with 10,005,164 units valued at $94,380,140 changing hands, on Tuesday.

Main market trading closed with Supreme Ventures leading with 3,066,003 units trading, or 45.3 percent of the day’s volume and Wisynco Group with 2,131,159 units and 31.5 percent of volume traded and Carreras closed with 381,353 units with 5.6 percent of the day’s volume.

IC bid-offer Indicator|At the end of trading, the Choice bid-offer indicator reading shows 3 stocks ending with bids higher than the last selling prices and 2 closing with lower offers.

Trading resulted in an average of 225,541 units valued at over $3,773,779, in contrast to 333,505 shares valued at $3,146,005 on Tuesday. The average volume and value for the month to date amounts to 290,851 shares, valued $5,213,901and previously, 293,971 shares, valued $5,289,432. September closed, with an average of 1,022,243 shares, valued $15,752,876, for each security traded.

In the main market activity, Caribbean Cement fell $1.20 trading 11,024 shares to close at $44, JMMB Group added 80 cents and ended at $33.80, trading 9,658 shares, Kingston Wharves lost $3 and finished at $75, with 771 stock units trading, Mayberry Investments gained 45 cents, settling at $11.25, trading 5,500 units, NCB Financial Group  added $1 and ended trading 108,157 shares to close at $126, PanJam Investment closed with a loss of 50 cents to end at $64, trading 36,716 stock units, Portland JSX rose 50 cents and ended at $8.50, with 500 units. Sagicor Real Estate Fund lost $1 to settle at $12, exchanging 26,431 shares, Scotia Group fell 74 cents to settle at $53 in trading 142,970 units, Seprod dropped $3, in finishing trading at $36, with 7,900 shares changing hands. Supreme Ventures jumped $1.80 to close at $19.80, with 3,066,003 shares changing hands.

added $1 and ended trading 108,157 shares to close at $126, PanJam Investment closed with a loss of 50 cents to end at $64, trading 36,716 stock units, Portland JSX rose 50 cents and ended at $8.50, with 500 units. Sagicor Real Estate Fund lost $1 to settle at $12, exchanging 26,431 shares, Scotia Group fell 74 cents to settle at $53 in trading 142,970 units, Seprod dropped $3, in finishing trading at $36, with 7,900 shares changing hands. Supreme Ventures jumped $1.80 to close at $19.80, with 3,066,003 shares changing hands.

Trading in the US dollar market ended with 36,650 units valued at $23,839 changing hands, with JMMB Group 5.75 percent preference share traded 10,920 shares at $2.03, Margaritaville closed with 125 units trading at 24 US cents and Sygnus Credit Investments US dollar based ordinary share, traded 16,979 units and rose 0.10 to end at 11 US cents after. The JSE USD Equities Index advanced by 0.01 point to close at 163.30.

Carib Cement hit by exchange loss

Caribbean Cement traded at $45.200 on Tuesday.

Sale revenues at Caribbean Cement rose 6.7 percent for the quarter, to $4.46 billion from $4.18 billion in 2017 and rose 7.9 percent for the year to date, to $13.2 billion from $12.25 billion in 2017.

A $464 million foreign exchange loss hit the results for the September quarter pulling the strong 44 percent increase in operating profit to $1.2 billion from $836 million, into lower net profit of $305 million than $748 million for the prior year’s period. For the nine months to September, profit fell 28 percent to $1.3 billion from $1.8 million in 2017.

Energy cost climbed by $233 million in the quarter and $342 million year to date but other operating cost declined, with the repurchase of the mill and kiln, previously leased from Trinidad Cement with only $213 million was incurred in the third quarter versus $1.1 million in 2017. For the nine months $1.57 million was incurred compared to $3.3 billion. On-the-other-hand finance cost excluding foreign exchange loss rose to $227 million up sharply from just $11 million in 2017 in the quarter and $299 million versus $4 million year to date. Depreciation and amortisation cost rose to $342 million from $132 million in 2017 and for the nine months to $808 million from $400 million in 2017. The net effect is that the company enjoyed a savings of $500 million per quarter or $2 billion per annum as a result of the buy of the lease, but virtually none of this, benefited shareholders.

Earnings per share came out at 39 cents for the quarter and $1.54 for the nine months and should end the fiscal year ending to around $3.50, as the company reverses the foreign exchange loss in the December quarter and picks up some gains, as well as increased revenues resulting from a price increase of just over 4 percent, effective on October 22.

Carib Cement could earn $5.30 in 2019.

But IC Insider.com is forecasting a jump in earnings for 2019 around $5.30 per shares, as the plant upgrades is completed and commissioned, allowing for the elimination of costly imports that negatively impacted cost in 2018 and will see them moving back into exports.

Gross cash flow brought in $849 million but growth in receivables, inventories, addition to fixed assets, loan repayment and increased payables resulted in negative total flows thus reducing the cash on hand to $468 million. For the nine months the operations brought in $2.6 billion but working capital needs and capital transactions saw cash funds reduced from $1.67 billion to $468 million.

The sharp changes in funds is due to the repurchase of equipment that was previously leased that drove fixed assets to $23 billion from $7.7 million in 2017 and borrowing to $12 billion.

Shareholders’ equity stood at $10.26 billion with borrowings at just $12 billion and net current assets ended the period was negative $1 billion.

The stock traded at $45.20 on the Jamaica Stock Exchange with a PE ratio of 13 times 2018 earnings and sits around the centre of the market valuation. the price could double in 2019. Net asset value is $12 with the stock selling at almost 4 times book value.

Going forward, the company results should be helped from the improvement in the Jamaican economy and growth that is likely to flow from the construction sector including buildings and roads and bridges as well as from increased exports. There is also focus on cost reduction with the high energy cost being the next centre of attention.

JSE makes big recovery on Tuesday

The Jamaica Stock Exchange closed a big gain on Tuesday as trading levels rose much higher than on Monday, from 34 active securities in the main and US dollar market compared to 31 on Monday.

The Jamaica Stock Exchange closed a big gain on Tuesday as trading levels rose much higher than on Monday, from 34 active securities in the main and US dollar market compared to 31 on Monday.

The market ended with the prices of 17 securities rising, 7 declining while 10 remained unchanged leading to the All Jamaica Composite Index surging 8,178.20 points to close at 398,615.81 and the JSE Index jumping 7,451.27 points to close at 363,184.12.

Trading closed with 10,005,164 units valued at $94,380,140 trading, compared with just 3,098,511 units valued at $31,049,457 changing hands, on Monday.

Main market trading closed with JMMB Group 7.50% preference share leading with 7,780,000 units trading, or 78 percent of the day’s volume and NCB Financial with 517,883 units and 5 percent of volume traded and Carreras closed with 372,736 units with 3.7 percent of the day’s volume.

IC bid-offer Indicator| At the end of trading, the Choice bid-offer indicator reading shows 3 stocks ending with bids higher than the last selling prices and 2 closing with lower offers.

Trading resulted in an average of 333,505 units valued at over $3,146,005, in contrast to 110,661 shares valued at $1,108,909 on Monday. The average volume and value for the month to date amounts to 293,971 shares, valued  $5,289,432 and previously, 291,988 shares, valued $5,142,412. September closed, with an average of 1,022,243 shares, valued $15,752,876, for each security traded.

$5,289,432 and previously, 291,988 shares, valued $5,142,412. September closed, with an average of 1,022,243 shares, valued $15,752,876, for each security traded.

In the main market activity, Barita Investments rose 90 cents and closed at $19 while trading 288 shares, Berger Paints climbed $1.40 to $22.90, in exchanging 24,500 stock units, Caribbean Cement rose $1.20 trading 14,777 shares to close at $45.20, Jamaica Broilers gained $1 trading 64,499 stock units to close at $31, Jamaica Producers jumped $1.651 and finished trading 28,494 units at $27.51, Jamaica Stock Exchange climbed $1.30 to close at a 52 weeks’ high of $9.80, trading 22,926 shares, Mayberry Investments gained 80 cents and settled at $10.80, trading 234,551 units, Mayberry Jamaican Equities lost 40 cents and settled at $11.40, in exchanging 13,025 units, NCB Financial Group added $5 and ended trading 517,883 shares to close at $125, PanJam Investment closed with a rise of $1.20 to end at $64.50, trading 55,001 stock units, Sagicor Group climbed $1.85 and settled at  $46.85, exchanging 10,431 shares, Scotia Group rose $1.74 in trading 8,363 units to close at $53.74, Seprod jumped $2, in finishing trading at $39, with 3,348 shares, Stanley Motta rose 55 cents trading 25,000 shares to close at $5, Victoria Mutual Investments rose 33 cents and concluded trading of 78,638 stock units at $4.13 and Wisynco Group rose 26 cents and finished at $10.50, with 198,252 units changing hands.

$46.85, exchanging 10,431 shares, Scotia Group rose $1.74 in trading 8,363 units to close at $53.74, Seprod jumped $2, in finishing trading at $39, with 3,348 shares, Stanley Motta rose 55 cents trading 25,000 shares to close at $5, Victoria Mutual Investments rose 33 cents and concluded trading of 78,638 stock units at $4.13 and Wisynco Group rose 26 cents and finished at $10.50, with 198,252 units changing hands.

Trading in the US dollar market ended with 48,323 units valued at $8,927 changing hands, with Margaritaville falling 1 cent and closing with 3,800 units trading at 24 US cents, Productive Business Solution gained 4 cents to close at 59 US cents trading just 100 units, Proven Investments fell 1 cent trading 34,223 shares to close at 20 US cents and Sygnus Credit Investments US dollar based ordinary share, traded 10,200 units to end at 10.9 US cents after slipping 0.1 cent The JSE USD Equities Index advanced by 1.36 points to close at 163.29.

JSE falls with modest trading on Monday

The Jamaica Stock Exchange closed on Monday with more decline following Friday’s big decline as trading volume decline to very low level.

The Jamaica Stock Exchange closed on Monday with more decline following Friday’s big decline as trading volume decline to very low level.

The market ended with the prices of 11 securities rising, 11 declining while 9 remained unchanged leading to the All Jamaica Composite Index diving 3,396.00 points to 390,437.61 and the JSE Index dropping 3,094.14 points to close at 355,732.85.

Trading closed with 31 active securities in the main and US dollar market compared to 29 on Friday but with higher volume and value as 3,098,511 units valued at $31,049,457 traded, compared with 4,241,799 units valued at $75,795,522 changing hands, on Friday.

Main market trading closed with 1834 Investments with the leading volume of 1,200,000 units trading, or 39 percent of the day’s volume, Sagicor Real Estate Fund with 559,428 units and 18 percent of volume traded and Carreras closed with 344,581 units accounting for 11 percent of the day’s volume.

IC bid-offer Indicator| At the end of trading, the Choice bid-offer indicator reading shows 7 stocks ending with bids higher than the last selling prices and 5 closing with lower offers.

Trading resulted in an average of 110,661 units valued at over $1,108,909, in contrast to 151,493 shares valued at $2,706,983 on Friday. The average volume and value for the month to date amounts to 291,988 shares, valued $5,142,412 and previously 300,895 shares, valued $5,350,785. September closed, with an average of 1,022,243 shares valued $15,752,876, for each security traded.

In the main market activity, Berger Paints lost 51 cents and ended at $21.50, exchanging 12,999 stock units, Caribbean Cement dipped $3 to finish trading with 43,795 shares at $44, Grace Kennedy gained 99 cents, trading 34,473 shares to close at $55.99, Jamaica Stock Exchange lost 70 cents to close at $8.50, trading 160,996 shares, JMMB Group lost $1 and ended at $33, exchanging 42,590 shares, Kingston Wharves jumped $8 and finished at $78 trading 6,301  stock units, Mayberry Investments lost 35 cents and settled at $10 in trading 22,721 units, Mayberry Jamaican Equities lost 40 cents and settled at $11.40, in exchanging 13,025 units, Salada Foods jumped $3.50 ended trading 11,274 stock units to close at $25, Scotia Group declined $2 in trading 5,599 units to close at $52, Seprod jumped $5, finishing trading at $37, with 2,100 shares and Supreme Ventures rose $1.50 to end at $18, in an exchange of 29,677 shares.

stock units, Mayberry Investments lost 35 cents and settled at $10 in trading 22,721 units, Mayberry Jamaican Equities lost 40 cents and settled at $11.40, in exchanging 13,025 units, Salada Foods jumped $3.50 ended trading 11,274 stock units to close at $25, Scotia Group declined $2 in trading 5,599 units to close at $52, Seprod jumped $5, finishing trading at $37, with 2,100 shares and Supreme Ventures rose $1.50 to end at $18, in an exchange of 29,677 shares.

Trading in the US dollar market ended with 39,347 units changing hands with Proven Investments trading 37,436 to close at 21 US cents and Sygnus Credit Investments US dollar based ordinary share traded 1,911 units but lost 0.5 cent to end at 11 US cents. The JSE USD Equities Index lost 2.73 points to close at 161.93.

Carib Cement chops $2B from lease cost

Jamaica Caribbean Cement Company slashed the cost formerly associated with leasing of Kiln 5 and Mill 5, from Trinidad Cement after acquiring direct ownership of the assets by $2 million per annum.

Data disclosed by Jamaica’s sole cement producer in their nine months interim report showed that excluding foreign exchange gains or loss that there was a $500 million savings in the overall cost associated with the two items formerly leased.

The equipment lease ended in April 2018 when both parties agreed to the ending of the arrangement leading the Jamaican company agreeing to purchase same. The interim figures show finance cost excluding foreign exchange loss rose to $227 million up sharply from just $11 million in 2017, in the quarter and $299 million versus $4 million year to date. Depreciation and amortisation cost rose to $342 million from $132 million in 2017 and for the nine months to $808 million from $400 million in 2017. The net effect is that the company enjoyed a savings of $500 million for the quarter or $2 billion per year.

A $464 million foreign exchange loss hit the results for the September quarter pulling the strong increase in operating profit of 44 percent to $1.2 billion from $836 million into lower net profit of $305 million than the $748 million generated for the prior year’s period. For the nine months to September, profit fell percent to $1.3 billion from $1.8 million in 2017.

All Jamaica drops 8,000 points – Friday

NCB Financial dropped $8 on Friday.

The Jamaica Stock Exchange closed on Friday with big losses in heavily capitalized companies with NCB Financial leading with a fall of $8 and Grace Kennedy falling $4 that pulled the market down 2 percent with the 5th largest points decline in the market’s history and the second big fall in October.

The market ended with the prices of 8 securities rising, 15 declining while 6 remained unchanged leading to the All Jamaica Composite Index diving 8,031.01 points to 393,833.61 and the JSE Index dropping 7,317.16 points to close at 358,826.99.

Trading closed with 29 active securities in the main and US dollar market compared to 30 on Thursday but with higher volume and value as 4,241,799 units valued at $75,795,522 traded, compared with 8,202,147 units valued at $132,503,743 changing hands, on Thursday.

Main market trading closed with JMMB Group 7.5% preference share leading with 1,652,103 units trading, or 39 percent of the day’s volume and Jamaica Broilers with 713,975 units and 16.8 percent of volume traded. Jamaica Stock Exchange leading with 448,893 units and 10.6 percent of the day’s volume, followed by

IC bid-offer Indicator| At the end of trading, the Choice bid-offer indicator reading shows 5 stocks ending with bids higher than the last selling prices and 2 closing with lower offers, an indication that falling prices are likely to be dominant on Friday.

Trading resulted in an average of 151,493 units valued at over $2,706,983, in contrast to 292,934 shares valued at $4,732,277 on Thursday. The average volume and value for the month to date amounts to 300,895 shares, valued $5,350,785 and previously 308,613 shares, valued $5,494,805. September closed, with an average of 1,022,243 shares valued $15,752,876, for each security traded.

In the main market activity, Grace Kennedy dropped $4, trading 120,588 shares to close at $55, Jamaica Broilers added $2 in trading 713,975 stock units, and closed at $30, Jamaica Producers lost $1 to close at $26 with 17,624 units changing hands, Jamaica Stock Exchange climbed 95 cents to close at a 52 weeks’ high of $9.20, with 448,893 shares, JMMB Group lost 80 cents and ended at $34, exchanging 60,884 shares., NCB Financial Group dropped  $8 to $120, trading 207,683 shares, PanJam Investment closed at $65.70, after declining $1.30 in trading 1,890 stock units, Portland JSX lost 50 cents in ending at $8 with 136,300 units, Sagicor Group dropped $2 to end at $45, trading 49,349 shares, Sagicor Real Estate Fund dropped $1.70 to $13.20, with 13,594 shares changing hands. Scotia Group climbed $2.50 in trading 33,416 units to close at $54, Supreme Ventures rose 25 cents to end at $16.50, in an exchange of 10,000 shares and Wisynco Group finished at $10.10, in trading 138,251 units after posting a loss of 20 cents.

$8 to $120, trading 207,683 shares, PanJam Investment closed at $65.70, after declining $1.30 in trading 1,890 stock units, Portland JSX lost 50 cents in ending at $8 with 136,300 units, Sagicor Group dropped $2 to end at $45, trading 49,349 shares, Sagicor Real Estate Fund dropped $1.70 to $13.20, with 13,594 shares changing hands. Scotia Group climbed $2.50 in trading 33,416 units to close at $54, Supreme Ventures rose 25 cents to end at $16.50, in an exchange of 10,000 shares and Wisynco Group finished at $10.10, in trading 138,251 units after posting a loss of 20 cents.

Trading in the US dollar market closed with Proven Investments trading 2,152 to close at 21 US cents. The JSE USD Equities Index rose 2.97 points to close at 164.66.