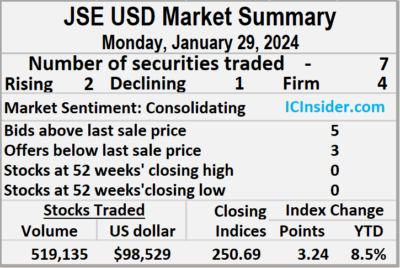

Trading on the Jamaica Stock Exchange US dollar market ended on Monday, with a 23 percent decline in the volume of stocks that were exchanged after 265 percent more US dollars changed hands than Friday, resulting in trading in seven securities, compared to six on the prior trading day with prices of two rising, one declining and four ending unchanged.

The market closed with an exchange of 519,135 shares for US$98,529 compared to 670,997 units at US$26,968 on Friday.

The market closed with an exchange of 519,135 shares for US$98,529 compared to 670,997 units at US$26,968 on Friday.

Trading averaged 74,162 stock units at US$14,076 versus 111,833 shares at US$4,495 on Friday, with a month to date average of 42,458 shares at US$5,106 compared with 40,528 units at US$4,560 on the previous day and December that ended with an average of 28,010 units for US$1,403.

The US Denominated Equities Index climbed 3.24 points to lock up trading at 250.69, with a gain of 8.5 percent for the year to date.

The PE Ratio, a measure used in computing appropriate stock values, averages 10.7. The PE ratio is computed based on the last traded price divided by projected earnings done by ICInsider.com for companies with their financial year ending and or around August 2024.

Investor’s Choice bid-offer indicator shows five stocks ended with bids higher than their last selling prices and three with lower offers.

At the close, First Rock Real Estate USD share ended at 5 US cents with investors swapping 995 units,  Margaritaville rose 1.5 cents to end at 11.5 US cents with 17,321 stocks, crossing the market, Proven Investments ended at 13.5 US cents after investors traded 6,017 shares. Sygnus Credit Investments ended at 8.98 US cents 89 stock units passed through the market and Transjamaican Highway gained 0.01 of a cent to close at 2 US cents after exchanging 418,713 shares.

Margaritaville rose 1.5 cents to end at 11.5 US cents with 17,321 stocks, crossing the market, Proven Investments ended at 13.5 US cents after investors traded 6,017 shares. Sygnus Credit Investments ended at 8.98 US cents 89 stock units passed through the market and Transjamaican Highway gained 0.01 of a cent to close at 2 US cents after exchanging 418,713 shares.

In the preference segment, JMMB US8.5% preference share fell 3 cents to US$1 in trading 75,000 stocks and Sygnus Credit Investments E 8.5% remained at US$11.788 after an exchange of 1,000 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

More gains for JSE USD Market

Tourist arrivals continue to slow

Tourist arrivals to Jamaica are up solidly for the year to November with an increase, of around 20 percent, but the rate of growth has slowed considerably since April with an increase in stopover arrivals of 14 percent compared with 28 percent in March and 44 percent for the first quarter. By July the rate of growth dropped to 12 percent for the month as growth starts returning to more sustainable levels.

Recent data emanating out of Sangster International Airport in Montego Bay shows 403,600 passengers being handled in November, 7.3 percent more than the 376,100 handled in November 2022, with the pace of growth down from 10.3 percent in October and the Kingston Airport processing 123,000 passengers, 6.6 percent fewer than the 131,700 handled in November 2022. Passenger activity in Kingston declined for a third consecutive month with October down 8.9 percent compared with October 2022.

Recent data emanating out of Sangster International Airport in Montego Bay shows 403,600 passengers being handled in November, 7.3 percent more than the 376,100 handled in November 2022, with the pace of growth down from 10.3 percent in October and the Kingston Airport processing 123,000 passengers, 6.6 percent fewer than the 131,700 handled in November 2022. Passenger activity in Kingston declined for a third consecutive month with October down 8.9 percent compared with October 2022.

For the first eleven months of 2023, the Montego Bay Airport processed 20.4 percent more passengers, with 3,918,900 being handled in 2022 moving to 4,716,800 in 2023. Total passenger movements grew by 13.5 percent at the Norman Manley International Airport from 1,402,300 in 2022 to 1,592,000 in the first eleven months of 2023.

Drop in Trinidad & Tobago Stock Exchange

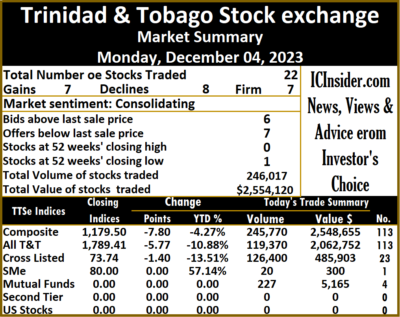

Trading activity dropped on the Trinidad and Tobago Stock Exchange on Monday, resulting in the trading of 22 securities up from 18 on Friday, with seven stocks rising, eight declining and seven remaining unchanged after a 50 percent drop in the volume of stocks traded and a 43 percent plunge in compared to Friday

Investors exchanged 246,017 shares for $2,554,120 down from 487,619 stock units at $4,456,955 on Friday.

Investors exchanged 246,017 shares for $2,554,120 down from 487,619 stock units at $4,456,955 on Friday.

An average of 11,183 stock units were traded at $116,096 compared to 27,090 shares at $247,609 on Friday, with trading month to date averaging 18,341 shares at $175,279 compared with an average trade for November of 19,241 shares at $227,402.

The Composite Index declined 7.80 points to 1,179.50, the All T&T Index lost 5.77 points to wrap up trading at 1,789.41, the SME Index remained unchanged at 80.00 and the Cross-Listed Index dropped 1.40 points to conclude trading at 73.74.

Investor’s Choice bid-offer indicator shows six stocks ended with bids higher than their last selling prices and seven with lower offers.

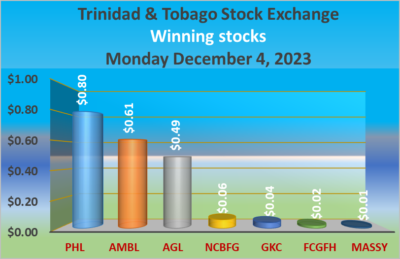

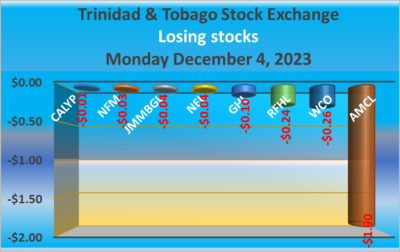

At the close, Agostini’s increased 49 cents in closing at $68.50, with 3,340 units crossing the market, Angostura Holdings ended at $21.50 with a transfer of 13 stocks, Ansa McAl lost $1.90 to end at $54 after 200 shares were exchanged.  Ansa Merchant Bank climbed 61 cents to $43.50 in trading 3,092 stocks, Calypso Macro Investment Fund slipped 1 cent to $22.75 in an exchange of 227 shares, Endeavour Holdings ended at $15, with investors trading 20 stock units. First Citizens Group popped 2 cents to $49.27 with trading in 10,244 units, FirstCaribbean International Bank ended at $7 with traders dealing in 8,759 stocks, GraceKennedy rallied 4 cents to $4.05 after an exchange of 88,315 units. Guardian Holdings fell 10 cents to $18 with investors dealing in 6,124 shares, JMMB Group dipped 4 cents to close at a 52 weeks’ low of $1.30, with 2,966 stock units crossing the exchange, L.J. Williams B share ended at $2.26 in switching ownership of 1,025 stocks. Massy Holdings popped 1 cent to close at $4.45 after a transfer of 60,031 units, National Enterprises skidded 4 cents in closing at $3.50 with stakeholders exchanging 21,279 stocks,

Ansa Merchant Bank climbed 61 cents to $43.50 in trading 3,092 stocks, Calypso Macro Investment Fund slipped 1 cent to $22.75 in an exchange of 227 shares, Endeavour Holdings ended at $15, with investors trading 20 stock units. First Citizens Group popped 2 cents to $49.27 with trading in 10,244 units, FirstCaribbean International Bank ended at $7 with traders dealing in 8,759 stocks, GraceKennedy rallied 4 cents to $4.05 after an exchange of 88,315 units. Guardian Holdings fell 10 cents to $18 with investors dealing in 6,124 shares, JMMB Group dipped 4 cents to close at a 52 weeks’ low of $1.30, with 2,966 stock units crossing the exchange, L.J. Williams B share ended at $2.26 in switching ownership of 1,025 stocks. Massy Holdings popped 1 cent to close at $4.45 after a transfer of 60,031 units, National Enterprises skidded 4 cents in closing at $3.50 with stakeholders exchanging 21,279 stocks,  National Flour Mills declined 3 cents to end at $1.72 after 836 shares passed through the market. NCB Financial gained 6 cents in closing at $2.91 in an exchange of 26,360 stock units, Prestige Holdings advanced 80 cents to $9.50 with investors transferring 239 shares, Republic Financial dipped 24 cents to $120 after an exchange of 4,560 stocks. Scotiabank ended at $70 with shareholders swapping 1,532 units, Trinidad & Tobago NGL remained at $10.50 as investors traded 6,081 stocks, Unilever Caribbean ended at $11.29, with 253 shares changing hands and West Indian Tobacco lost 26 cents to close at $9.25 with an exchange of 521 stocks.

National Flour Mills declined 3 cents to end at $1.72 after 836 shares passed through the market. NCB Financial gained 6 cents in closing at $2.91 in an exchange of 26,360 stock units, Prestige Holdings advanced 80 cents to $9.50 with investors transferring 239 shares, Republic Financial dipped 24 cents to $120 after an exchange of 4,560 stocks. Scotiabank ended at $70 with shareholders swapping 1,532 units, Trinidad & Tobago NGL remained at $10.50 as investors traded 6,081 stocks, Unilever Caribbean ended at $11.29, with 253 shares changing hands and West Indian Tobacco lost 26 cents to close at $9.25 with an exchange of 521 stocks.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

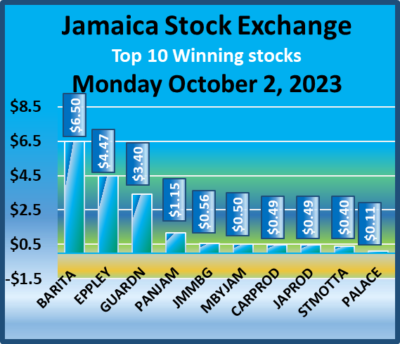

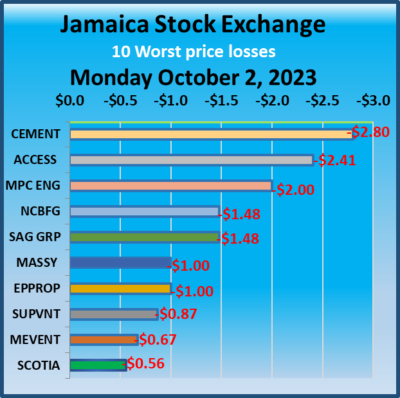

JSE shares tumble to open October

The Markets gave back quite a lot of Friday’s headed gains as trading commenced for October with the Junior Market to the JSE Main Market indices declining sharply but the JSE USD Market Index rose.

At close, the JSE Combined Market Index shed 3,243.01 points to close trading at 338,145.95, the All Jamaican Composite Index dropped 3,568.87 points to finish at 352,223.23, the JSE Main Index fell 2,970.48 points to settle at 324,071.95, the Junior Market Index dived 51.88 points to end trading at 3,907.46 after Fosrich and Fesco dropped back from the late close surge in price on Friday and the JSE USD Market Index shed 2.50 points to settle at 256.33.

At close, the JSE Combined Market Index shed 3,243.01 points to close trading at 338,145.95, the All Jamaican Composite Index dropped 3,568.87 points to finish at 352,223.23, the JSE Main Index fell 2,970.48 points to settle at 324,071.95, the Junior Market Index dived 51.88 points to end trading at 3,907.46 after Fosrich and Fesco dropped back from the late close surge in price on Friday and the JSE USD Market Index shed 2.50 points to settle at 256.33.

At the close, investors traded 25,939,993 shares in all three markets, down sharply from 50,931,729 stock units on Friday. The value of stocks traded on the Junior and Main markets amounted to $118.24 million, down from $256.86 million on Friday. Trading on the JSE USD market ended with investors exchanging 266,503 shares for US$6,378compared with 2,780,944 units at US$60,312 on Friday.

In the preference segment, Productive Business Solutions 10.5% preference share advanced $1 to end at $1,215.

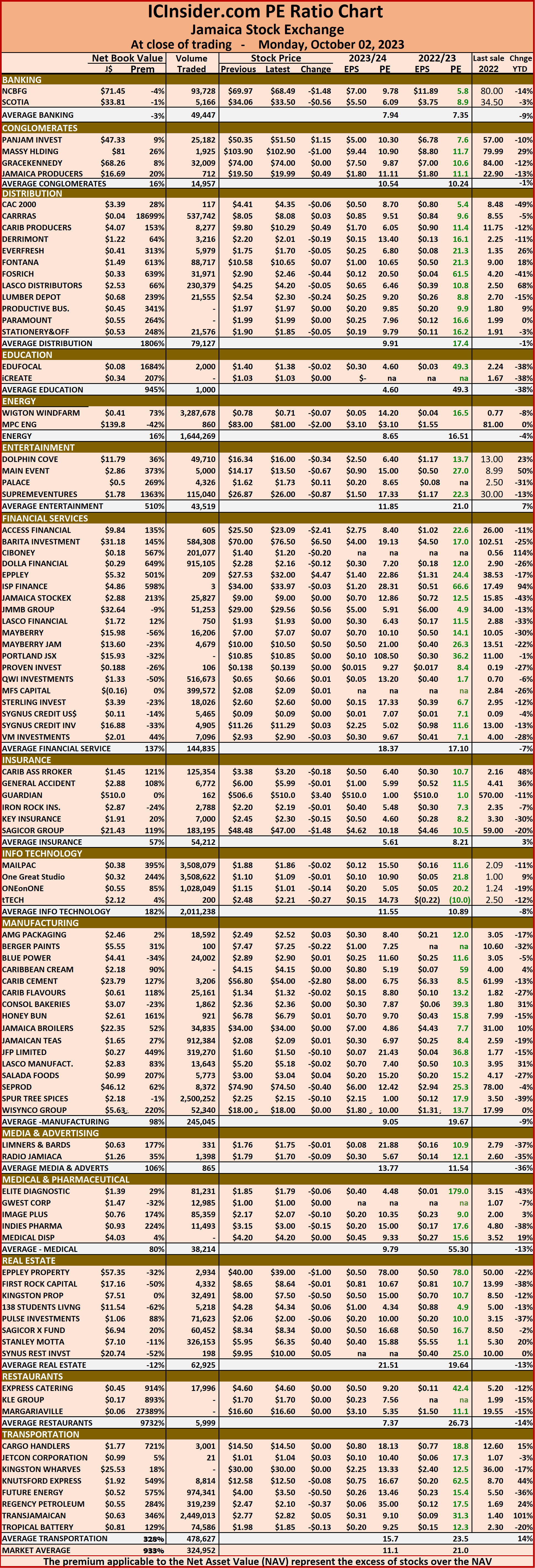

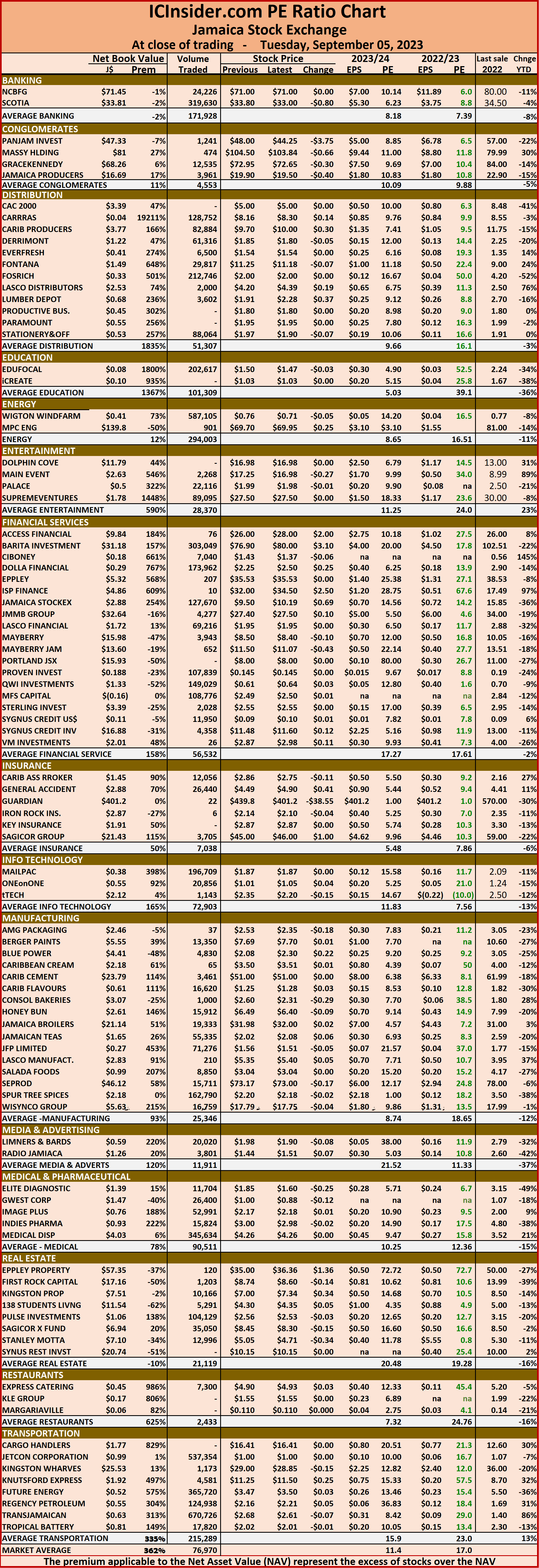

The market’s PE ratio, the most popular measure used to determine the value of stocks ended at 21 on 2022-23 earnings and 11.1 times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

The market’s PE ratio, the most popular measure used to determine the value of stocks ended at 21 on 2022-23 earnings and 11.1 times those for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

The PE ratio chart covers all ordinary shares on the Jamaica Stock Exchange, grouped by industry, allowing for easy comparisons between the same sector companies and the overall market. The EPS & PE ratios are based on 2023 and 2024 actual or projected earnings, excluding major one off items.

Investors need pertinent information to successfully navigate numerous investment options in the local stock market. The ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

The net asset value of each company is reported as a guide to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

The net asset value of each company is reported as a guide to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

Dividends paid or payable and yields for each company are shown in the Main and Junior Markets’ daily report charts along with the closing volume pertaining to the highest bid and the lowest offer for each company.

Trading up on JSE USD Market

Trading on the Jamaica Stock Exchange US dollar market ended on Tuesday, with the volume of stocks changing hands rising 128 percent valued 23 percent more than on Monday, resulting in trading in nine securities, similar to Monday and ended with prices of two rising, three declining and four ending unchanged.

Overall, 401,339 shares were traded, for US$48,561 compared to 175,984 units at US$39,421 on Monday.

Overall, 401,339 shares were traded, for US$48,561 compared to 175,984 units at US$39,421 on Monday.

Trading averaged 44,593 units at US$5,396, versus 19,554 shares at US$4,380 on Monday, with a month to date average of 47,869 shares at US$3,999 compared to 48,101 units at US$3,900 on the previous day, down from August with an average of 57,291 units for US$4,251.

The US Denominated Equities Index dropped 3.66 points to undefined 254.00.

The PE Ratio, a measure used in computing appropriate stock values, averages 9.4 The PE ratio is computed based on the last traded price divided by projected earnings done by ICInsider.com for companies with their financial year ending between November 2023 and August 2024.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and one with a lower offer.

At the close, First Rock Real Estate USD share fell 0.2 of a cent to end at 5.8 US cents with shareholders swapping 9,526 shares, Margaritaville rose 3.02 cents to close at 14.02 US cents in an exchange of just one stock unit,  Proven Investments advanced 0.5 of a cent to 14 US cents with an exchange of 325,066 units. Sterling Investments remained at 1.9 US cents with investors dealing in 5,408 stocks, Sygnus Credit Investments ended at 9.07 US cents in switching ownership of 90 stock units, Sygnus Real Estate Finance USD share remained at 10 US cents after 81 units crossed the exchange and Transjamaican Highway dipped 0.07 of a cent to end at 1.62 US cents with traders dealing in 60,714 stocks.

Proven Investments advanced 0.5 of a cent to 14 US cents with an exchange of 325,066 units. Sterling Investments remained at 1.9 US cents with investors dealing in 5,408 stocks, Sygnus Credit Investments ended at 9.07 US cents in switching ownership of 90 stock units, Sygnus Real Estate Finance USD share remained at 10 US cents after 81 units crossed the exchange and Transjamaican Highway dipped 0.07 of a cent to end at 1.62 US cents with traders dealing in 60,714 stocks.

In the preference segment, JMMB Group 6%lost 7.27 cents and ended at US$1 in an exchange of 395 shares and Productive Business Solutions 9.25% preference share ended at US$12 after 58 shares were traded.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Downward trend of murders in Jamaica

Murders in Jamaica have been on the increase since 1962, the year of independence and surged sharply after, averaging just under 1,000 per year between 1996 and 2003, peaking between 2004 to 2010 with an average of 1,545 per annum, followed by a substantially lower average of 1,136 between 2011 and 2016 with the average climbing back to 1,415 since then.

Close analysis suggests that murders in the country may have peaked but that there has been a steady decline since, with more to come. The decline this year is a continuation of the new downward trend.

In 1962, the year of independence for Jamaica, there were 63 murders which jumped by 153 percent over the 351 in 1979 to 889 in the politically charged murderous 1980. Murders have gotten out of control since, with respective governments unable to tackle this chronic problem and bring resolution to it.

In 1962, the year of independence for Jamaica, there were 63 murders which jumped by 153 percent over the 351 in 1979 to 889 in the politically charged murderous 1980. Murders have gotten out of control since, with respective governments unable to tackle this chronic problem and bring resolution to it.

From a surge in 1980, murders fell back to the 400 level but it gradually started to rise at the start of 1990 and broke the 1,000 mark in 1997 when there were 1,038 murders and remained elevated, hitting 1,471 in 2004 and then 1,674 the following year before hitting a new high of 1,683 in 2009.

In 2011, there were 1,133 murders down from 1,447 in 2010 following the incursion into Western Kingston by the security forces that seemed to have disrupted some of the criminal activities in certain areas in the country.

The accompanying chart shows murders peaking with a downward trajectory even before an 11 percent decline in 2023 to August. The data also shows that the upward trend was broken in 2010, with murders falling back below the red line, although it spiked higher for a few years, that has not really changed the downward drift as can be seen from the black line that is sloping downward after peaking in 2005. Barring some extraordinary developments murders are set to be lower than the 2023 figure and likely to be the in the range of 2018 to 2020 with an average of 1,316 murders.

The chart shows annual murder in Jamaica from 1962 onwards and reflects a scenario where the trend line in the early years put the country with a murder rate around 600 per annum assuming there were no developments to reduce the rate below that level.

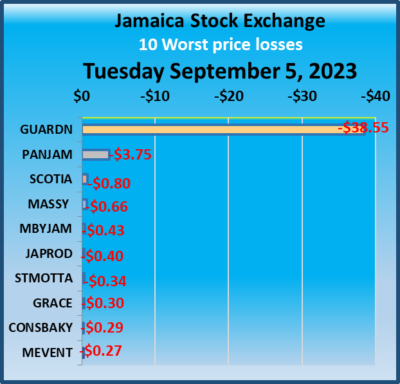

Junior Market gains, Main Market falters

The Junior Market rose for a second day in a row but remained below the close for August while the Main and the JSE USD Market fell on the Jamaica Stock Exchange Tuesday, with the value of stocks traded rising above Monday’s levels accompanied by a fall in the volume of stocks traded.

At the close, the JSE Combined Market Index shed 1,567.18 points to finish trading at 335,914.48, the All Jamaican Composite Index fell 512.67 points to 355,125.22, the JSE Main Index dropped 1,935.10 points to 321,763.77, the Junior Market Index popped 26.05 points to 3,898.55 while the JSE USD Market Index fell 2.20 points to end at 243.25.

At the close, the JSE Combined Market Index shed 1,567.18 points to finish trading at 335,914.48, the All Jamaican Composite Index fell 512.67 points to 355,125.22, the JSE Main Index dropped 1,935.10 points to 321,763.77, the Junior Market Index popped 26.05 points to 3,898.55 while the JSE USD Market Index fell 2.20 points to end at 243.25.

Trading of Preference shares ended, with Jamaica Public Service 7% preference share dropping $12 to $41.

At the close, investors traded 6,987,843 shares in markets, down from 9,618,088 stocks on Monday. The value of stocks traded on the Junior and Main markets was $56.7 million, up from $53.06 million on Monday. Trading on the JSE USD market ended with investors exchanging 195,527 shares for US$19,350 from 193,702 units at US$30,250 on Monday.

The market’s PE ratio, the most popular measure used to determine the value of stocks ended at 17 on 2022-23 earnings and 11.4 times for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

The market’s PE ratio, the most popular measure used to determine the value of stocks ended at 17 on 2022-23 earnings and 11.4 times for 2023-24 at the close of trading. ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

The PE ratio chart covers all ordinary shares on the Jamaica Stock Exchange. It shows companies grouped by industry, allowing for easy comparisons between the same sector companies and the overall market. The EPS & PE ratios are based on 2023 and 2024 actual or projected earnings, excluding major one off items.

Investors need pertinent information to successfully navigate numerous investment options in the local stock market. The ICInsider.com PE ratio chart and the more detailed daily report charts provide investors with regularly updated information to help decision-making.

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

The net asset value of each company is reported as a guide to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

The net asset value of each company is reported as a guide to assess the value of stocks based on this measure quickly. The chart also shows daily changes in stock prices and the percentage year to date price movement based on the last traded prices.

Dividends paid or payable and yields for each company are shown in the Main and Junior Markets’ daily report charts along with the closing volume pertaining to the highest bid and the lowest offer for each company.

Murders drop 10.8% in Jamaica

Murders in Jamaica fell 10.8 percent to the 26th of August this year compared to the similar period last year, with 899 persons murdered to August 26, down from 1,008 last year for the same period last year, data from Jamaica Constabulary Force show.

Increases occurred in Hanover with 28 persons, an increase of 104 percent, with 55 murders. St. Ann has a rise of 29 percent from 41 murders last year to 53 this year. Clarendon rose 11 percent to 72 and Kingston Eastern 6 percent more than the 38 experienced in 2022, while Kingston Western popped 6 percent higher to 52.

Increases occurred in Hanover with 28 persons, an increase of 104 percent, with 55 murders. St. Ann has a rise of 29 percent from 41 murders last year to 53 this year. Clarendon rose 11 percent to 72 and Kingston Eastern 6 percent more than the 38 experienced in 2022, while Kingston Western popped 6 percent higher to 52.

St Catherine North had the most significant reduction of 33 percent, with 33 fewer deaths by force, compared with a total of 101 in 2022, while Westmoreland saw a decrease of 19 percent, but it continues to be a hot spot with 79 murders and that was picked up by Hanover up by 28 deaths from 27 in 2022, while St James remains a considerable problem area with a mere 4.4 per fall from 137 to 131.

Biden appoints Jamaican to economic council

Dr C Kirabo Jackson

President Biden announced his intent to appoint Dr C. Kirabo Jackson to be a Member of the Council of Economic Advisers. Jackson an American-born Jamaican whose father Dr. Clement Jackson was head of the Planning Institute of Jamaica in the 1980s is the Abraham Harris Professor of Education and Social Policy at Northwestern University. He is also a Professor of Economics, a Fellow at the Institute for Policy Research, and a Faculty Research Fellow at the National Bureau of Economic Research. Jackson also attended Hillel in Kingston, Jamaica in his early formative years.

Currently, Jackson serves as the Editor-In-Chief of the American Economic Journal: Economic Policy. He was previously Co-Editor for the American Economic Journal: Economic Policy and the Journal of Human Resources. Jackson earned his Bachelor’s in Ethics, Politics, and Economics from Yale University and obtained his Ph.D. in Economics from Harvard University. His research interests include labour economics, public finance, and applied econometrics, with a focus on the economics of education. His research has explored the role of teachers in the K-12 system, the causal impact of public-school spending on students, methods to measure impacts on students’ socio-emotional skills, and other education-related subjects.

His work has been published in the highest-impact economics journals, including the Quarterly Journal of Economics, the Journal of Political Economy, the Review of Economic Studies, the American Economic Review: Insights, the Review of Economics and Statistics, the American Economic Journal: Economic Policy, and the American Economic Journal: Applied Economics. His research findings have garnered attention from numerous media outlets, including the New York Times, the Wall Street Journal, the Washington Post, Bloomberg, and others.

In 2020, Jackson was elected to the National Academy of Education and received the David N. Kershaw Award from the Association for Public Policy Analysis and Management in recognition of his contributions to the field of public policy analysis and management. In 2022, Jackson was elected to the American Academy of Arts and Sciences, an honour that celebrates excellence and leadership across various disciplines and practices.

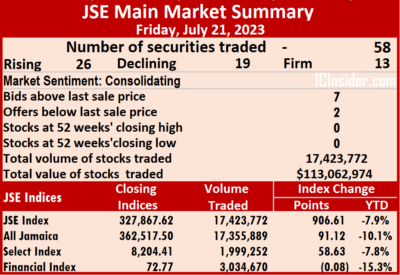

More gains for JSE Main Market

The Jamaica Stock Exchange Main Market closed higher for a second consecutive day on Friday, with the volume of stocks changing hands climbing 42 percent and the value 41 percent lower than on Thursday, with 58 securities trading compared with 52 on Thursday, with 26 rising, 19 declining and 13 ending unchanged.

A total of 17,423,772 shares were exchanged for $113,062,974 versus 12,158,165 units at $187,080,964 on Thursday.

A total of 17,423,772 shares were exchanged for $113,062,974 versus 12,158,165 units at $187,080,964 on Thursday.

Trading averaged 300,410 shares at $1,949,362 compared with 233,811 units at $3,597,711 on Thursday and month to date, an average of 308,048 stocks at $2,115,819, compared with 308,619 units at $2,128,260 on the previous day. Trading in June closed with an average of 366,795 units at $6,952,581, including trading in bonds.

Transjamaican Highway led trading with 5.75 million shares for 33.3 percent of total volume, followed by JMMB Group 7.35% – 2028 with 2.57 million units for 14.9 percent of the day’s trade, Sagicor Select Financial Fund ended with 2.53 million units for 14.6 percent market share, QWI Investments controlled 1.46 million units for 8.4 percent of the market and Wigton Windfarm with 1.40 million units for 8.1 percent of total volume.

The All Jamaican Composite Index rallied 91.12 points to 362,517.50, the JSE Main Index rose 906.61 points to 327,867.62 and the JSE Financial Index dipped 0.08 points to 72.77.

The All Jamaican Composite Index rallied 91.12 points to 362,517.50, the JSE Main Index rose 906.61 points to 327,867.62 and the JSE Financial Index dipped 0.08 points to 72.77.

The PE Ratio, a formula used to compute appropriate stock values, averages 13.1 for the Main Market. The JSE Main and USD Market PE ratios are calculated based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending up to August 2024.

Investor’s Choice bid-offer indicator shows seven stocks ended with bids higher than their last selling prices and two with lower offers.

At the close, Barita Investments rallied $1.50 and ended at $76 after trading 57,195 shares, First Rock Real Estate fell $1.45 in closing at $9, with 3,400 stock units clearing the market, Guardian Holdings climbed $4 to $455 as investors exchanged 849 units, Jamaica Broilers gained 47 cents to end at $35 with a transfer of 22,072 stocks. Jamaica Stock Exchange dipped $1.21 to close at $10.22 in an exchange of 36,696 stock units, JMMB Group dropped 30 cents in closing at $28.90 in trading 28,280 stocks, Kingston Wharves popped 31 cents and ended at $29.80 after an exchange of 21,223 shares, Margaritaville advanced 40 cents to $15 after an exchange of 54 units.  Massy Holdings declined 50 cents to end at $98.50, with 5,272 stock units crossing the market, Mayberry Jamaican Equities rose 40 cents to close at $11.90 and closed after 2,505 stocks changed hands, NCB Financial increased $2.49 to end at $74.99 in switching ownership of 709,089 units, 138 Student Living advanced 65 cents to close at $4.65 with an exchange of 111,931 shares. Pan Jamaica shed $1.35 in closing at $49 with stakeholders exchanging 50,625 shares, Proven Investments increased $1.25 to $23.25 in an exchange of 1,228 stocks, Scotia Group rose 70 cents to $33.75, with 204,253 units crossing the market, Seprod climbed $2.10 to $74.10 with investors transferring 3,139 stock units. Supreme Ventures rallied 49 cents to close at $27.49 after a transfer of 208,004 stock units, Sygnus Credit Investments lost 83 cents to end at $11.17 with shareholders swapping 146,619 units, Victoria Mutual Investments gained 37 cents in closing at $3.37, with 56,404 stocks changing hands and Wisynco Group popped 30 cents to end at $18 with 50,440 shares crossing the exchange.

Massy Holdings declined 50 cents to end at $98.50, with 5,272 stock units crossing the market, Mayberry Jamaican Equities rose 40 cents to close at $11.90 and closed after 2,505 stocks changed hands, NCB Financial increased $2.49 to end at $74.99 in switching ownership of 709,089 units, 138 Student Living advanced 65 cents to close at $4.65 with an exchange of 111,931 shares. Pan Jamaica shed $1.35 in closing at $49 with stakeholders exchanging 50,625 shares, Proven Investments increased $1.25 to $23.25 in an exchange of 1,228 stocks, Scotia Group rose 70 cents to $33.75, with 204,253 units crossing the market, Seprod climbed $2.10 to $74.10 with investors transferring 3,139 stock units. Supreme Ventures rallied 49 cents to close at $27.49 after a transfer of 208,004 stock units, Sygnus Credit Investments lost 83 cents to end at $11.17 with shareholders swapping 146,619 units, Victoria Mutual Investments gained 37 cents in closing at $3.37, with 56,404 stocks changing hands and Wisynco Group popped 30 cents to end at $18 with 50,440 shares crossing the exchange.

In the preference segment, Eppley 7.50% preference share rallied 91 cents in closing at $6.12, as 3,056 units passed through the market, Jamaica Public Service 7% dipped $1 to $70 while exchanging 1,022 stocks. JMMB Group 7.25% due 2024 preference share fell 30 cents and ended at $1.70 with investors transferring 208,689 shares and 138 Student Living preference share rose $13.39 to close at $102.63 in trading one stock unit.

In the preference segment, Eppley 7.50% preference share rallied 91 cents in closing at $6.12, as 3,056 units passed through the market, Jamaica Public Service 7% dipped $1 to $70 while exchanging 1,022 stocks. JMMB Group 7.25% due 2024 preference share fell 30 cents and ended at $1.70 with investors transferring 208,689 shares and 138 Student Living preference share rose $13.39 to close at $102.63 in trading one stock unit.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.