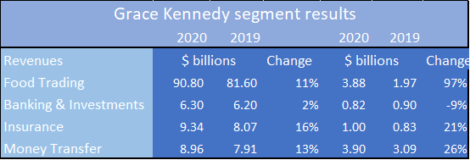

Fresh from a record-breaking profit performance in 2020, Grace Kennedy announced the signing of an agreement to acquire all the shares of Scotia Insurance Eastern Caribbean Limited subject to regulatory approval.

Grace Kennedy HQ in Kingston

Scotia Insurance operates in seven countries in the Eastern Caribbean: Anguilla, Antigua and Barbuda, Dominica, Grenada, St. Kitts and Nevis, St. Lucia and St. Vincent and the Grenadines. Scotia Insurance offers credit protection regionally to customers of Scotiabank on personal loans, residential mortgages, personal lines of credit, personal and small business credit cards.

According to Don Wehby, CEO of Grace Kennedy, “the operation is profitable but not highly profitable”. Grace’s ownership is likely to result in lower operating cost and a vehicle to do business in other countries and for other financial institutions.

In an investors briefing on Monday, Wehby stated that the proposed acquisition is one of ten that the group is looking at currently, at various stages of assessment or negotiation, including some being stress tested and others at the legal stages.

Wehby in answer to a question on the growth rate of 2020 continuing into 2021 confirmed, that it will as the 2020 growth was achieved after years of work to lay the foundation for it to happen.

tTech limited is a Junior Market that seems set to benefit when the acquisition is concluded, the extent of its involvement will depend on the technology in use and whether the acquisition will continue to utilize the current infrastructure or not. tTech is a major Information Technology supplier to Grace.

Grace is listed on the Jamaica Stock Exchange and currently trades at $90.99, the shares are trading on the Trinidad and Tobago Stock Exchange at TT$4.50, in line with the JSE price.

Sterling Investments is a new addition to the Main Market TOP 10, replacing Berger Paints with profit downgraded with earnings per share of $1.30 for 2021. That was inadequate to hold on to the TOP 10 position, but the stock is still on the ICTOP15 list for 2021.

Sterling Investments is a new addition to the Main Market TOP 10, replacing Berger Paints with profit downgraded with earnings per share of $1.30 for 2021. That was inadequate to hold on to the TOP 10 position, but the stock is still on the ICTOP15 list for 2021.

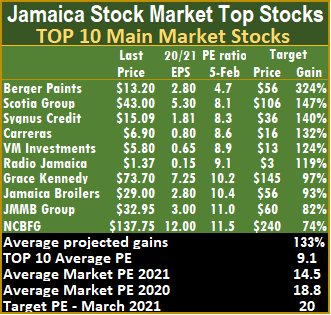

The Main Market has a number in the list that have put out record profits or show signs of strong earnings with the stocks clearly undervalued; these include, JMMB Group, Jamaica Broilers, Sygnus Credit Investments, Grace Kennedy are currently in the TOP10 Main Market listing and Caribbean Cement that is just outside.

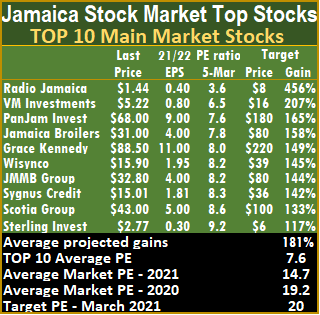

The Main Market has a number in the list that have put out record profits or show signs of strong earnings with the stocks clearly undervalued; these include, JMMB Group, Jamaica Broilers, Sygnus Credit Investments, Grace Kennedy are currently in the TOP10 Main Market listing and Caribbean Cement that is just outside. With expected gains of 165 to 456 percent, the top three Main Market stocks are Radio Jamaica, followed by VM Investments and PanJam Investment.

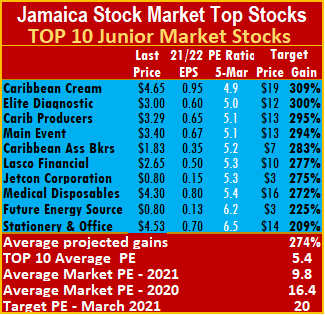

With expected gains of 165 to 456 percent, the top three Main Market stocks are Radio Jamaica, followed by VM Investments and PanJam Investment.  The average projected gain for the Junior Market IC TOP 10 stocks is 274 percent and 181 percent for the JSE Main Market, based on 2021-22 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2022 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.

The average projected gain for the Junior Market IC TOP 10 stocks is 274 percent and 181 percent for the JSE Main Market, based on 2021-22 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2022 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information. Coming into the TOP10 are Fesco, the latest IPO that is expected to come to market shortly, with the prospectus having been released but temporarily withdrawn to correct some errors. JMMB Group and Sygnus Credit Investments are now in the TOP10 Main market listing.

Coming into the TOP10 are Fesco, the latest IPO that is expected to come to market shortly, with the prospectus having been released but temporarily withdrawn to correct some errors. JMMB Group and Sygnus Credit Investments are now in the TOP10 Main market listing.

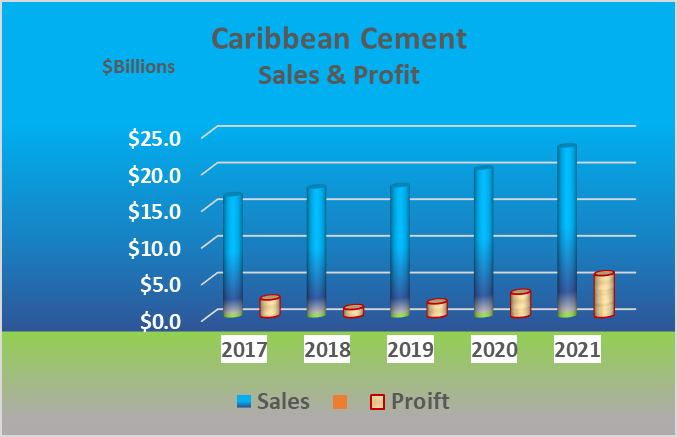

This week’s focus: Grace Kennedy had outstanding results for 2020 with much more to come in 2021; expect the price to move sharply over the next few weeks. Caribbean Cement reported a 70 percent rise in profit for 2020 and is projected to earn $6.70 for 2021, the stock is an ideal candidate to move higher in the weeks ahead.

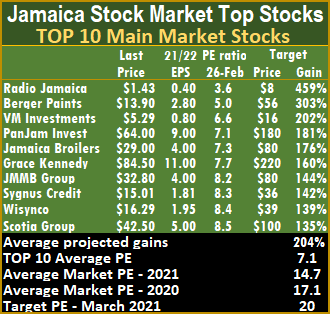

This week’s focus: Grace Kennedy had outstanding results for 2020 with much more to come in 2021; expect the price to move sharply over the next few weeks. Caribbean Cement reported a 70 percent rise in profit for 2020 and is projected to earn $6.70 for 2021, the stock is an ideal candidate to move higher in the weeks ahead. The local stock market’s targeted average PE ratio is 20 based on profits of companies reporting full year’s results, up to the second quarter of 2021. The Junior and Main markets are currently trading well below the market average, a clear indication of strong gains ahead. The JSE Main Market ended the week, with an overall PE of 14.7 and the Junior Market 9.8 based on ICInsider.com’s projected 2021-22 earnings. The PE ratio for the Junior Market Top 10 stocks average a mere 5.2 at just 53 percent of the market average. The Main Market TOP 10 stocks trade at a PE of 7.1 or 48 percent of the PE of that market.

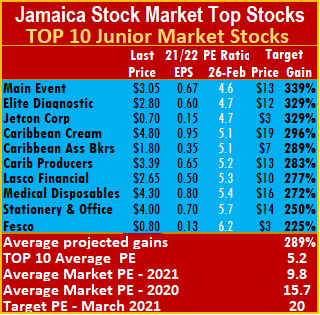

The local stock market’s targeted average PE ratio is 20 based on profits of companies reporting full year’s results, up to the second quarter of 2021. The Junior and Main markets are currently trading well below the market average, a clear indication of strong gains ahead. The JSE Main Market ended the week, with an overall PE of 14.7 and the Junior Market 9.8 based on ICInsider.com’s projected 2021-22 earnings. The PE ratio for the Junior Market Top 10 stocks average a mere 5.2 at just 53 percent of the market average. The Main Market TOP 10 stocks trade at a PE of 7.1 or 48 percent of the PE of that market. The average projected gain for the Junior Market IC TOP 10 stocks is 289 percent and 204 percent for the JSE Main Market, based on 2021-22 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.

The average projected gain for the Junior Market IC TOP 10 stocks is 289 percent and 204 percent for the JSE Main Market, based on 2021-22 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information. For the year, profit after tax surged 70 percent to $3.2 billion after tax provision of $1.2 billion. The tax charge includes deferred tax amounting to $414 million, down from $664 million in 2019. The results would have been far better but for a billion loss in foreign exchange movement, but interest cost fell from $939 million to $812 million, partially cushioning some exchange losses. Interest cost will fall further in 2021 as the debt load recedes with the strong cash flows allowing for the rapid repayment of the $4.4 billion of long term loans.

For the year, profit after tax surged 70 percent to $3.2 billion after tax provision of $1.2 billion. The tax charge includes deferred tax amounting to $414 million, down from $664 million in 2019. The results would have been far better but for a billion loss in foreign exchange movement, but interest cost fell from $939 million to $812 million, partially cushioning some exchange losses. Interest cost will fall further in 2021 as the debt load recedes with the strong cash flows allowing for the rapid repayment of the $4.4 billion of long term loans. At the end of the year, shareholders’ equity moved to $11.5 billion from $8.3 billion at the end of 2019. The stock is one of the original

At the end of the year, shareholders’ equity moved to $11.5 billion from $8.3 billion at the end of 2019. The stock is one of the original

The group earned 6.26 per share for the year versus $4.51 in 2019 and the stock price closed on Friday with a last traded price of $84.50 for a PE ratio of 13, well below the market average of 20. ICInsider.com projects 2021 earnings of $11 per share and see the stock heading close to $200 for the year and receives the coveted

The group earned 6.26 per share for the year versus $4.51 in 2019 and the stock price closed on Friday with a last traded price of $84.50 for a PE ratio of 13, well below the market average of 20. ICInsider.com projects 2021 earnings of $11 per share and see the stock heading close to $200 for the year and receives the coveted

Caribbean Cream – EPS 95 cents Current PE 5.

Caribbean Cream – EPS 95 cents Current PE 5.

Jetcon Corporation – EPS 15 cents Current PE 5

Jetcon Corporation – EPS 15 cents Current PE 5

The performance was even more stunning, with pretax profit jumping a very strong 43.4 percent for the quarter and 36.7 percent for the nine months to $1.3 billion as the company profit became subject to full taxation as of October 12 in 2020.

The performance was even more stunning, with pretax profit jumping a very strong 43.4 percent for the quarter and 36.7 percent for the nine months to $1.3 billion as the company profit became subject to full taxation as of October 12 in 2020.

Lasco Distributors earnings were also adjusted down, with the release of the nine months results showing earnings per share of 21 cents and 7 cents for the December quarter, putting the full-year numbers at 30 cents per share.

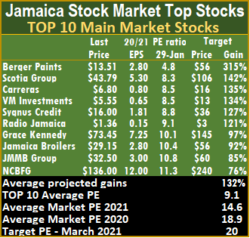

Lasco Distributors earnings were also adjusted down, with the release of the nine months results showing earnings per share of 21 cents and 7 cents for the December quarter, putting the full-year numbers at 30 cents per share. The current TOP 10 report is based on earnings for 2020/21 as there are substantial gains ahead, for many stocks in the listings.

The current TOP 10 report is based on earnings for 2020/21 as there are substantial gains ahead, for many stocks in the listings. Main Market TOP 10 stocks trade at a PE of 9.1 or 48 percent of the PE of that market.

Main Market TOP 10 stocks trade at a PE of 9.1 or 48 percent of the PE of that market. While the Junior Market had a new addition, the Main Market TOP10 continued with the same stocks as the week before but Grace Kennedy price rose from $68 to $73.45 with the stock moving from 5th spot to 7th.

While the Junior Market had a new addition, the Main Market TOP10 continued with the same stocks as the week before but Grace Kennedy price rose from $68 to $73.45 with the stock moving from 5th spot to 7th.

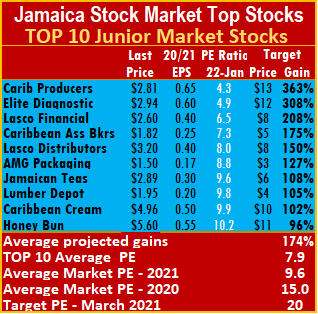

In this regard, based on 2020 release of results, interim financials are expected this week, from Access Financial, Barita Investments, Iron Rock Insurance, NCB Financial, the Lasco group of companies and Jamaican Teas.

In this regard, based on 2020 release of results, interim financials are expected this week, from Access Financial, Barita Investments, Iron Rock Insurance, NCB Financial, the Lasco group of companies and Jamaican Teas. The local stock market’s targeted average PE ratio is 20 based on profits of companies reporting full year’s results, from now to the second quarter in 2021. The Junior and Main markets are currently trading well below the market average, indicating strong gains ahead. The JSE Main Market ended the week, with an overall PE of 18.9 and the Junior Market 14.8, based on ICInsider.com’s projected 2020-21 earnings. The PE ratio for the Junior Market Top 10 stocks average a mere 7.8 at just 53 percent of the market average. The Main Market TOP 10 stocks trade at a PE of 9.1 or 48 percent of the PE of that market.

The local stock market’s targeted average PE ratio is 20 based on profits of companies reporting full year’s results, from now to the second quarter in 2021. The Junior and Main markets are currently trading well below the market average, indicating strong gains ahead. The JSE Main Market ended the week, with an overall PE of 18.9 and the Junior Market 14.8, based on ICInsider.com’s projected 2020-21 earnings. The PE ratio for the Junior Market Top 10 stocks average a mere 7.8 at just 53 percent of the market average. The Main Market TOP 10 stocks trade at a PE of 9.1 or 48 percent of the PE of that market. IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.

IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.

initially reported by the company to just $29 million with the stock selling off to a low of 95 cents but bounced a bit thereafter.

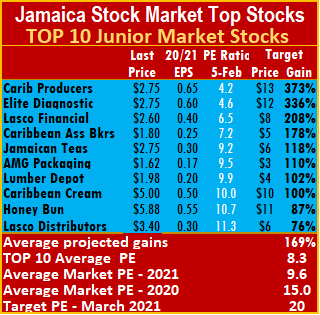

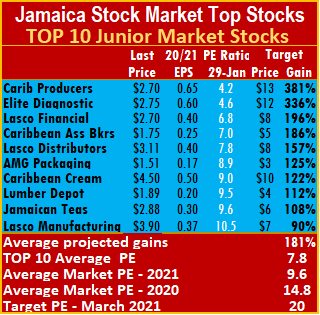

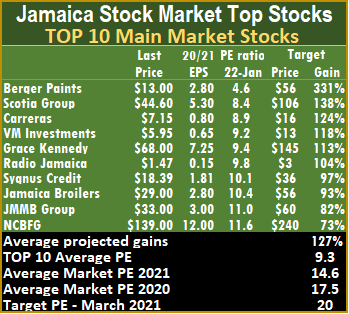

initially reported by the company to just $29 million with the stock selling off to a low of 95 cents but bounced a bit thereafter. The top three stocks in the Junior Market with the potential to gain between 208 to 363 percent are Caribbean Producers followed by Elite Diagnostic and Lasco Financial. With expected gains of 124 to 331 percent, the top three Main Market stocks are, Berger Paints followed by Scotia Group and Carreras.

The top three stocks in the Junior Market with the potential to gain between 208 to 363 percent are Caribbean Producers followed by Elite Diagnostic and Lasco Financial. With expected gains of 124 to 331 percent, the top three Main Market stocks are, Berger Paints followed by Scotia Group and Carreras. The average projected gain for the Junior Market IC TOP 10 stocks is 174 percent and 127 percent for the JSE Main Market, based on 2020-21 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.

The average projected gain for the Junior Market IC TOP 10 stocks is 174 percent and 127 percent for the JSE Main Market, based on 2020-21 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.