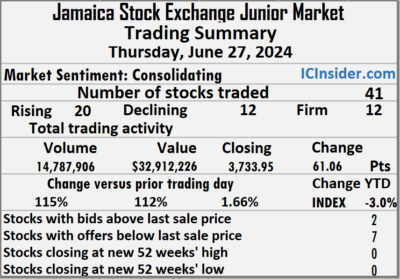

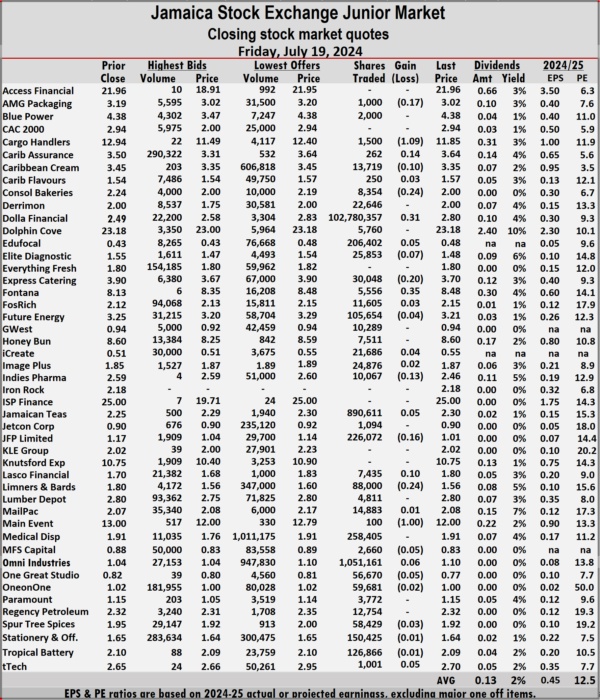

Trading more than doubled at the close of the Junior Market of the Jamaica Stock Exchange Friday, with trading in 41 securities as was the case on Thursday and ending with prices of 20 rising, nine declining and 12 unchanged as the Junior Market Index jumped a solid 61.06 points to 3,733.95. The Investor’s Choice bid-offer indicator is flashing negative signals for Monday’s trading.

The market closed with trading of 14,787,906 shares for $32,912,226 up from 6,869,011 units at $15,510,430 on Thursday.

The market closed with trading of 14,787,906 shares for $32,912,226 up from 6,869,011 units at $15,510,430 on Thursday.

Trading averaged 360,681 shares at $802,737 compared with 167,537 units at $378,303 on Thursday with a month to date, average of 375,434 units at $776,020 compared to 376,281 stock units at $774,486 on the previous day and June with an average of 318,732 units at $696,979.

Jamaican Teas led trading with 4.20 million shares for 28.4 percent of total volume followed by Derrimon Trading with 3.87 million stocks for 26.2 percent of the day’s trade and EduFocal with 1.42 million units for 9.6 percent of the total trade.

The Junior Market ended trading with an average PE Ratio of 12.9, based on last traded prices and earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and seven with lower offers.

Investor’s Choice bid-offer indicator shows two stocks ended with bids higher than their last selling prices and seven with lower offers.

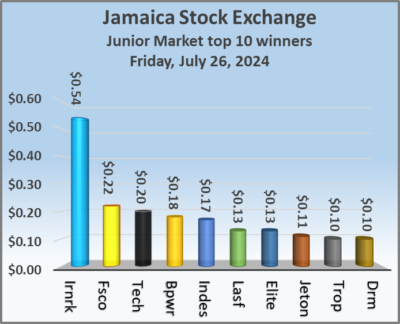

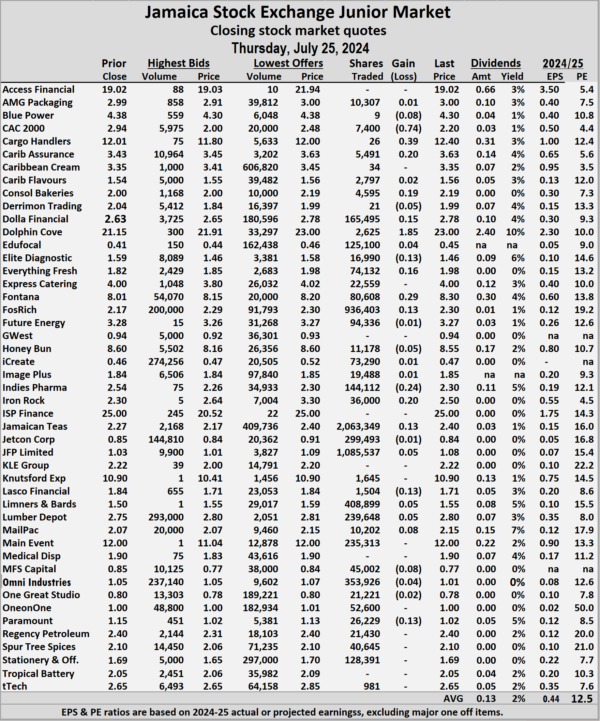

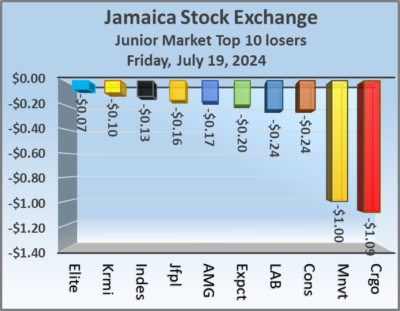

At the close, AMG Packaging dropped 10 cents in closing at $2.90 with an exchange of 3,022 stock units, Blue Power gained 18 cents to close at $4.48, with 8,000 shares passing through the market, Derrimon Trading popped 10 cents to finish at $2.09 with investors trading 3,867,566 units. Dolla Financial fell 13 cents and ended at $2.65 after closing with 284,821 stocks being traded, Elite Diagnostic climbed 13 cents to close at $1.59 with traders dealing in 21,360 shares, Fontana dipped 10 cents to end at $8.20 with an exchange of 566,164 stocks.  Future Energy rose 22 cents to $3.49 in trading 517,728 units, Indies Pharma gained 17 cents and ended at $2.47 in switching ownership of 328,267 stock units, Iron Rock Insurance rallied 54 cents to end at $3.04, with just 28 shares changing hands. Jetcon Corporation advanced 11 cents in closing at 95 cents, with 370,872 units crossing the exchange, Lasco Financial popped 13 cents to finish at $1.84 in trading 500 stocks, MFS Capital Partners gained 8 cents to close at 85 cents after 121,561 stock units passed through the market. Tropical Battery rose 10 cents to $2.15 in an exchange of 61,526 shares and tTech climbed 20 cents in closing at $2.85, with a mere 3 stock units crossing the market.

Future Energy rose 22 cents to $3.49 in trading 517,728 units, Indies Pharma gained 17 cents and ended at $2.47 in switching ownership of 328,267 stock units, Iron Rock Insurance rallied 54 cents to end at $3.04, with just 28 shares changing hands. Jetcon Corporation advanced 11 cents in closing at 95 cents, with 370,872 units crossing the exchange, Lasco Financial popped 13 cents to finish at $1.84 in trading 500 stocks, MFS Capital Partners gained 8 cents to close at 85 cents after 121,561 stock units passed through the market. Tropical Battery rose 10 cents to $2.15 in an exchange of 61,526 shares and tTech climbed 20 cents in closing at $2.85, with a mere 3 stock units crossing the market.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Nice gains for Junior Market

Rising stocks moved the Junior Market of the Jamaica Stock Exchange higher at the close on Thursday, after trading in 41 securities compared with 40 on Wednesday and ended with prices of 19 rising, 13 declining and nine ending unchanged with a 167 percent rise in the volume and 264 percent jump in the value of stocks traded, over Wednesday.

Trading closed with an exchange of 6,869,011 shares for $15,510,430 compared with 2,576,485 units at $4,262,470 on Wednesday.

Trading closed with an exchange of 6,869,011 shares for $15,510,430 compared with 2,576,485 units at $4,262,470 on Wednesday.

Trading averaged 167,537 shares at $378,303 up from 64,412 units at $106,562 on Wednesday. Trading for the month to date, averages 376,281 stock units at $774,486 compared with 388,998 shares at $798,622 on the previous day as well as June that ended with an average of 318,732 units at $696,979.

Jamaican Teas led trading with 2.06 million shares for 30 percent of total volume followed by JFP Ltd with 1.09 million units for 15.8 percent of the day’s trade and Fosrich with 936,403 units for 13.6 percent market share.

At the close of trading, the Junior Market Index increased 21.67 points to end the day at 3,672.89.

The Junior Market ended with an average PE Ratio of 12.4, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows five stocks ended with bids higher than their last selling prices and four with lower offers.

Investor’s Choice bid-offer indicator shows five stocks ended with bids higher than their last selling prices and four with lower offers.

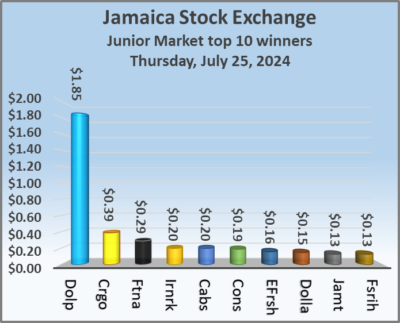

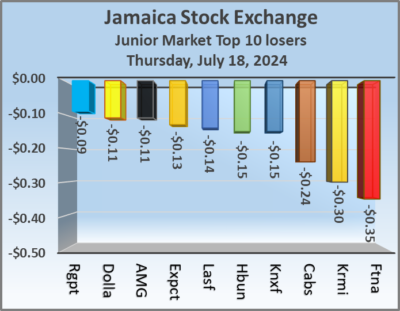

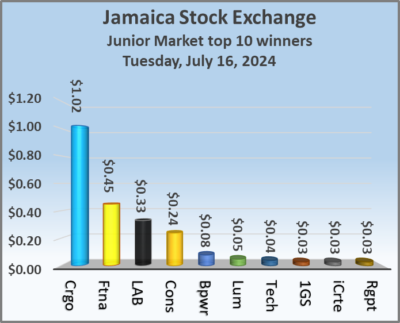

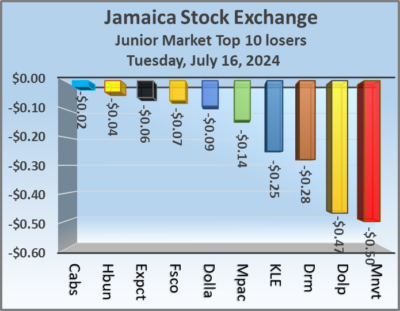

At the close of the market, Blue Power slipped 8 cents and ended at $4.30 with investors trading 9 stock units, CAC 2000 declined 74 cents to close at a 52 weeks’ low of $2.20 with 7,400 shares clearing the market, Cargo Handlers rallied 39 cents to $12.40 after an exchange of 26 units. Caribbean Assurance Brokers popped 20 cents in closing at $3.63, with 5,491 stocks crossing the market, Consolidated Bakeries rallied 19 cents to finish at $2.19 after trading 4,595 units, Derrimon Trading lost 5 cents to end at $1.99 in an exchange of 21 stocks. Dolla Financial increased 15 cents to $2.78 with investors trading 165,495 shares, Dolphin Cove climbed $1.85 and ended at $23, with 2,625 stock units crossing the market, Elite Diagnostic dropped 13 cents to close at $1.46 after an exchange of 16,990 shares.  Everything Fresh rose 16 cents to end at $1.98 after 74,132 stocks passed through the market, Fontana gained 29 cents in closing at $8.30 with an exchange of 80,608 units, Fosrich popped 13 cents to finish at $2.30, with 936,403 stock units changing hands. Honey Bun fell 5 cents and ended at $8.55 with traders dealing in 11,178 shares, Indies Pharma slipped 24 cents to $2.30 in an exchange of 144,112 stock units, Iron Rock Insurance gained 20 cents to close at $2.50 with investors dealing in 36,000 units. Jamaican Teas rose 13 cents to finish at $2.40 with a transfer of 2,063,349 stocks, JFP Ltd advanced 5 cents in closing at $1.08 and closed after 1,085,537 units changed hands, Lasco Financial sank 13 cents to end at $1.71 in trading 1,504 shares. Limners and Bards climbed 5 cents to $1.55 with 408,899 stock units crossing the exchange, Lumber Depot increased 5 cents to end at $2.80 in switching ownership of 239,648 stocks,

Everything Fresh rose 16 cents to end at $1.98 after 74,132 stocks passed through the market, Fontana gained 29 cents in closing at $8.30 with an exchange of 80,608 units, Fosrich popped 13 cents to finish at $2.30, with 936,403 stock units changing hands. Honey Bun fell 5 cents and ended at $8.55 with traders dealing in 11,178 shares, Indies Pharma slipped 24 cents to $2.30 in an exchange of 144,112 stock units, Iron Rock Insurance gained 20 cents to close at $2.50 with investors dealing in 36,000 units. Jamaican Teas rose 13 cents to finish at $2.40 with a transfer of 2,063,349 stocks, JFP Ltd advanced 5 cents in closing at $1.08 and closed after 1,085,537 units changed hands, Lasco Financial sank 13 cents to end at $1.71 in trading 1,504 shares. Limners and Bards climbed 5 cents to $1.55 with 408,899 stock units crossing the exchange, Lumber Depot increased 5 cents to end at $2.80 in switching ownership of 239,648 stocks,  Mailpac Group rallied 8 cents in closing at $2.15 as investors exchanged 10,202 shares. MFS Capital Partners skidded 8 cents and ended at a 52 weeks’ low of 77 cents after a transfer of 45,002 units and Paramount Trading shed 13 cents to finish at $1.02 with investors swapping 26,229 stocks.

Mailpac Group rallied 8 cents in closing at $2.15 as investors exchanged 10,202 shares. MFS Capital Partners skidded 8 cents and ended at a 52 weeks’ low of 77 cents after a transfer of 45,002 units and Paramount Trading shed 13 cents to finish at $1.02 with investors swapping 26,229 stocks.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

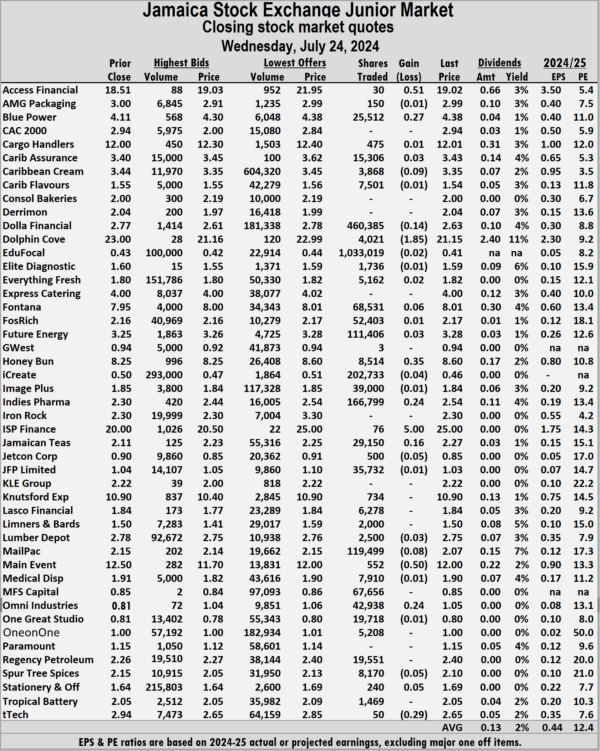

Junior Market popped higher Wednesday

Trading activity fell sharply at the close of the Junior Market of the Jamaica Stock Exchange on Wednesday, with a 74 percent drop in the volume of stocks traded, with an 83 percent lower value than on Tuesday with trading in 40 securities compared with 41 on Tuesday and ending with prices of 15 rising, 18 declining and seven closing unchanged.

The market ended with 2,576,485 shares trading at $4,262,470 down from 9,854,162 units at $24,889,108 on Tuesday.

The market ended with 2,576,485 shares trading at $4,262,470 down from 9,854,162 units at $24,889,108 on Tuesday.

Trading averaged 64,412 shares at $106,562, down from 240,345 stocks at $607,051 on Tuesday with trading for the month to date, averaging 388,998 units at $798,622 versus 409,509 stock units at $842,354 on the previous day compared to June with an average of 318,732 units at $696,979.

EduFocal led trading with 1.03 million shares for 40.1 percent of total volume followed by Dolla Financial with 460,385 units for 17.9 percent of the day’s trade and iCreate with 202,733 units for 7.9 percent market share.

At the close of trading, the Junior Market Index advanced 10.46 points to conclude trading at 3,651.22.

The Junior Market ended trading with an average PE Ratio of 12.4, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows 10 stocks ended with bids higher than their last selling prices and four with lower offers.

Investor’s Choice bid-offer indicator shows 10 stocks ended with bids higher than their last selling prices and four with lower offers.

At the close, Access Financial rose 51 cents in closing at $19.02 with an exchange of 30 stocks, Blue Power rallied 27 cents to $4.38 and closed after an exchange of 25,512 units, Caribbean Cream declined 9 cents to finish at $3.35 with traders dealing in 3,868 shares. Dolla Financial sank 14 cents and ended at $2.63 with 460,385 stocks clearing the market, Dolphin Cove dropped $1.85 to close at $21.15 with a transfer of 4,021 shares, Fontana popped 6 cents to end at $8.01, with 68,531 units crossing the exchange. Honey Bun gained 35 cents to end at $8.60 in trading 8,514 stocks, Indies Pharma increased 24 cents to end at $2.54, with 166,799 stock units crossing the market, ISP Finance climbed $5 in closing at $25 after a transfer of 76 shares. Jamaican Teas rose 16 cents t0 $2.27 after 29,150 units passed through the market,  Jetcon Corporation fell 5 cents to close at 85 cents in switching ownership of 500 stocks, Mailpac Group skidded 8 cents to finish at $2.07 after an exchange of 119,499 stock units. Main Event sank 50 cents to close at $12, with 552 shares crossing the market, Regency Petroleum popped 14 cents to finish at $2.40 with investors swapping 19,551 units, Spur Tree Spices slipped 5 cents and ended at $2.10 in an exchange of 8,170 stock units. Stationery and Office Supplies advanced 5 cents to close at $1.69 after investors ended trading 240 stock units and tTech lost 29 cents to end at $2.65 as investors exchanged 50 shares.

Jetcon Corporation fell 5 cents to close at 85 cents in switching ownership of 500 stocks, Mailpac Group skidded 8 cents to finish at $2.07 after an exchange of 119,499 stock units. Main Event sank 50 cents to close at $12, with 552 shares crossing the market, Regency Petroleum popped 14 cents to finish at $2.40 with investors swapping 19,551 units, Spur Tree Spices slipped 5 cents and ended at $2.10 in an exchange of 8,170 stock units. Stationery and Office Supplies advanced 5 cents to close at $1.69 after investors ended trading 240 stock units and tTech lost 29 cents to end at $2.65 as investors exchanged 50 shares.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

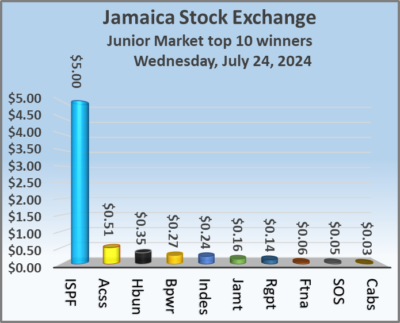

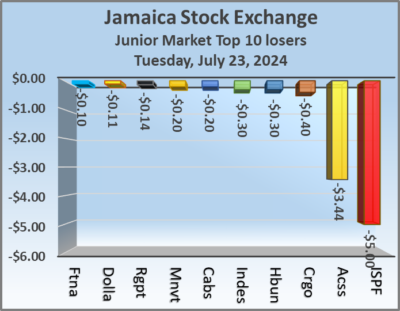

Winners hard to find on Junior Market

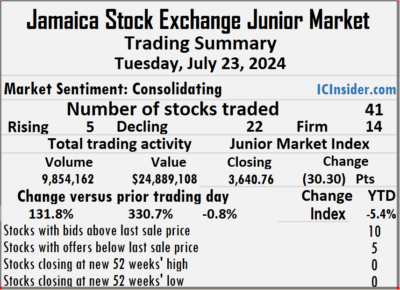

A mere five stocks recorded gains on Tuesday, following trading in 41 securities up from 43 on Monday with prices of 22 declining and 14 closing unchanged, however, the Investor’s Choice bid-offer indicator is flashing positive developments for trading activity on the Junior Market of the Jamaica Stock Exchange on Wednesday, as the market ended with a 132 percent surge in the volume of stocks traded, with a 331 percent greater value than Monday.

The market closed on Tuesday with trading of 9,854,162 stock units for $24,889,108 compared to 4,251,907 shares at $5,779,055 on Monday.

The market closed on Tuesday with trading of 9,854,162 stock units for $24,889,108 compared to 4,251,907 shares at $5,779,055 on Monday.

Trading averaged 240,345 shares at $607,051 up from 98,882 units at $134,397 on Monday with the month to date, averaging 409,509 units at $842,354 compared to 421,225 stock units at $858,650 on the previous day and June with an average of 318,732 units at $696,979.

JFP Ltd led trading with 2.40 million shares for 24.4 percent of total volume followed by EduFocal with 2.26 million stocks for 22.9 percent of the day’s trade, Fontana ended with 1.72 million units for 17.4 percent market share and Dolla Financial with 1.03 million shares for 10.4 percent of total volume.

At the close of trading, the Junior Market Index dropped 30.30 points to close at 3,640.76.

The Junior Market ended trading with an average PE Ratio of 12.4, based on last traded prices in conjunction with earnings projected by ICInsider.com for financial years ending around August 2025.

The Junior Market ended trading with an average PE Ratio of 12.4, based on last traded prices in conjunction with earnings projected by ICInsider.com for financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows 10 stocks ended with bids higher than their last selling prices and five with lower offers.

At the close, Access Financial shed $3.44 to end at $18.51 with investors dealing in 1,500 stock units, Cargo Handlers sank 40 cents to $12 with 2,100 shares crossing the market, Caribbean Assurance Brokers dipped 20 cents to $3.40 as investors traded 5,120 stocks. Dolla Financial sank 11 cents to finish at $2.77 and closed with an exchange of 1,026,165 units, Express Catering climbed 11 cents and ended at $4 with investors trading 115,457 shares, Fontana slipped 10 cents to close at $7.95 after 1,717,590 stocks passed through the market.  Honey Bun fell 30 cents to $8.25 in trading 9,696 units, Indies Pharma skidded 30 cents to close at $2.30, with 158,642 stock units crossing the exchange, following the lifting of the suspension of trading, Iron Rock Insurance increased 12 cents to finish at $2.30 with traders dealing in just one stock with the company posting big gains in profit for the 2023 fiscal year and the first quarter to March. ISP Finance lost $5 and ended at $20, with 2,000 stocks clearing the market, JFP Ltd declined 10 cents in closing at $1.04 with an exchange of 2,402,260 units, Limners and Bards dipped 9 cents to end at $1.50 after investors ended trading 5,000 stock units. Main Event fell 20 cents in closing at $12.50 with a transfer of 30,021 shares and Regency Petroleum dropped 14 cents to $2.26, with 24,424 stocks changing hands.

Honey Bun fell 30 cents to $8.25 in trading 9,696 units, Indies Pharma skidded 30 cents to close at $2.30, with 158,642 stock units crossing the exchange, following the lifting of the suspension of trading, Iron Rock Insurance increased 12 cents to finish at $2.30 with traders dealing in just one stock with the company posting big gains in profit for the 2023 fiscal year and the first quarter to March. ISP Finance lost $5 and ended at $20, with 2,000 stocks clearing the market, JFP Ltd declined 10 cents in closing at $1.04 with an exchange of 2,402,260 units, Limners and Bards dipped 9 cents to end at $1.50 after investors ended trading 5,000 stock units. Main Event fell 20 cents in closing at $12.50 with a transfer of 30,021 shares and Regency Petroleum dropped 14 cents to $2.26, with 24,424 stocks changing hands.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Trading dived on the Junior Market

Trading dropped sharply on the Junior Market of the Jamaica Stock Exchange on Monday, following the big trade in Dolla Financial on Friday with the volume of stocks traded declining 96 percent with a 98 percent lower value, with trading in 43 securities compared with 40 on Friday and ending with prices of 21 rising, 14 declining and eight closing unchanged.

The market closed on Monday with the trading of 4,251,907 shares for $5,779,055 down from 106,310,225 units at $249,915,230 on Friday.

The market closed on Monday with the trading of 4,251,907 shares for $5,779,055 down from 106,310,225 units at $249,915,230 on Friday.

Trading averaged 98,882 shares at $134,397 compared with 2,657,756 units at $6,247,881 on Friday with the month to date, averaging 421,225 stock units at $858,650 compared to 446,472 stock units at $915,377 on the previous day and June with an average of 318,732 units at $696,979.

EduFocal led trading with 2.03 million shares for 47.8 percent of total volume followed by Dolla Financial with 957,337 units for 22.5 percent of the day’s trade and JFP Ltd with 256,593 units for 6 percent market share.

At the close of trading, the Junior Market Index gained 30.31 points to end at 3,671.06.

The Junior Market ended trading with an average PE Ratio of 12.6, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows four stocks ended with bids higher than their last selling prices and three with lower offers.

At the close, Blue Power fell 27 cents and ended at $4.11 after the trading of 2,288 shares, Cargo Handlers rallied 55 cents to close at $12.40 after an exchange of 2,600 stock units, Caribbean Cream increased 9 to end at $3.44 with investors dealing in 312 stocks, Dolla Financial climbed 8 cents in closing at $2.88 with a transfer of 957,337 units, Dolphin Cove declined 18 cents to finish at $23 as investors exchanged 4,741 shares, Elite Diagnostic rose 6 cents to close at $1.54 after a transfer of 2,782 units. Express Catering advanced 19 cents to $3.89, with just 2 stock units changing hands, Fontana sank 43 cents and ended at $8.05 in trading 12,095 stock units, Future Energy popped 8 cents in closing at $3.29 with 150,050 shares clearing the market. Honey Bun slipped 5 cents to finish at $8.55 with an exchange of 1,486 units, iCreate sank 5 cents to end at 50 cents, with 54,113 stocks crossing the market, Indies Pharma gained 14 cents to close at $2.60 with investors trading 1,771 stock units. Jamaican Teas shed 18 cents to end at $2.12 in an exchange of 11,081 shares,

At the close, Blue Power fell 27 cents and ended at $4.11 after the trading of 2,288 shares, Cargo Handlers rallied 55 cents to close at $12.40 after an exchange of 2,600 stock units, Caribbean Cream increased 9 to end at $3.44 with investors dealing in 312 stocks, Dolla Financial climbed 8 cents in closing at $2.88 with a transfer of 957,337 units, Dolphin Cove declined 18 cents to finish at $23 as investors exchanged 4,741 shares, Elite Diagnostic rose 6 cents to close at $1.54 after a transfer of 2,782 units. Express Catering advanced 19 cents to $3.89, with just 2 stock units changing hands, Fontana sank 43 cents and ended at $8.05 in trading 12,095 stock units, Future Energy popped 8 cents in closing at $3.29 with 150,050 shares clearing the market. Honey Bun slipped 5 cents to finish at $8.55 with an exchange of 1,486 units, iCreate sank 5 cents to end at 50 cents, with 54,113 stocks crossing the market, Indies Pharma gained 14 cents to close at $2.60 with investors trading 1,771 stock units. Jamaican Teas shed 18 cents to end at $2.12 in an exchange of 11,081 shares, JFP Ltd popped 13 cents to end at $1.14 with traders dealing in 256,593 stock units, KLE Group climbed 21 cents in closing at $2.23 with an exchange of 4,149 units. Knutsford Express increased 15 cents to finish at $10.90 with investors swapping 616 stocks, Mailpac Group rallied 8 cents and ended at $2.16 in switching ownership of 4,342 shares, Main Event rose 70 cents to close at $12.70, with an exchange of 37 stock units. Omni Industries lost 6 cents to close at $1.04 with investors trading 25,956 stocks, Regency Petroleum gained 8 cents and ended at $2.40 after 40,602 units passed through the market, Spur Tree Spices advanced 23 cents to end at $2.15 after an exchange of 23,366 shares and tTech popped 24 cents in closing at $2.94, with just 2 stock units crossing the market.

JFP Ltd popped 13 cents to end at $1.14 with traders dealing in 256,593 stock units, KLE Group climbed 21 cents in closing at $2.23 with an exchange of 4,149 units. Knutsford Express increased 15 cents to finish at $10.90 with investors swapping 616 stocks, Mailpac Group rallied 8 cents and ended at $2.16 in switching ownership of 4,342 shares, Main Event rose 70 cents to close at $12.70, with an exchange of 37 stock units. Omni Industries lost 6 cents to close at $1.04 with investors trading 25,956 stocks, Regency Petroleum gained 8 cents and ended at $2.40 after 40,602 units passed through the market, Spur Tree Spices advanced 23 cents to end at $2.15 after an exchange of 23,366 shares and tTech popped 24 cents in closing at $2.94, with just 2 stock units crossing the market.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Trading surged on 103m Dolla Financial shares

A block of 100 million shares of Dolla Financial was put through the market at 13 minutes after noon on Friday at $2.37 each, with a value of $237 million pushing the stock to the leading trade in the market before the company released first quarter results with increased revenues and profit, after the close of the Junior Market of the Jamaica Stock Exchange. The trade pushed the volume of stock traded to 106,310,225 shares for $249,915,230, up sharply from 2,685,073 units at $6,623,219 on Thursday.

Trading averaged 2,657,756 shares at $6,247,881 compared to 63,930 units at $157,696 on Thursday. Trading for the month to date, averages 446,472 stock units at $915,377 compared with 272,698 stock units at $496,319 on the previous day and June with an average of 318,732 units at $696,979.

Trading averaged 2,657,756 shares at $6,247,881 compared to 63,930 units at $157,696 on Thursday. Trading for the month to date, averages 446,472 stock units at $915,377 compared with 272,698 stock units at $496,319 on the previous day and June with an average of 318,732 units at $696,979.

Trading ended with an exchange of 40 securities compared with 42 on Thursday and ending with prices of 13 rising, 17 declining and 10 closing unchanged.

Dolla Financial led trading with 102.78 million shares for 96.7 percent of total volume followed by Omni Industries with 1.05 million units for 1 percent of the day’s trade and Jamaican Teas with 890,611 units for 0.8 percent market share.

At the close of trading, the Junior Market Index sank 42.17 points to conclude trading at 3,640.75.

The Junior Market ended trading with an average PE Ratio of 12.5, based on last traded prices with earnings projected by ICInsider.com for financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and three with lower offers.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and three with lower offers.

At the close of the market, AMG Packaging lost 17 cents to close trading at $3.02 with an exchange of 1,000 shares, Cargo Handlers sank $1.09 to $11.85 after an exchange of 1,500 shares, Caribbean Assurance Brokers rallied 14 cents to end at $3.64 in trading 262 units. Caribbean Cream fell 10 cents in closing at $3.35 after an exchange of 13,719 stocks, Consolidated Bakeries dropped 24 cents to end at $2 with a transfer of 8,354 units, Dolla Financial popped 31 cents and ended at $2.80, with 102,780,357 shares crossing the exchange. EduFocal advanced 5 cents to 48 cents with traders dealing in 206,402 stock units, Elite Diagnostic sank 7 cents in closing at $1.48 in an exchange of 25,853 stocks, Express Catering skidded 20 cents to close at $3.70 after 30,048 shares passed through the market. Fontana rose 35 cents to finish at $8.48 as investors exchanged 5,556 units, Indies Pharma declined 13 cents and ended at $2.46, with 10,067 stocks changing hands, Jamaican Teas climbed 5 cents to end at $2.30 and closed with an exchange of 890,611 stock units.  JFP Ltd shed 16 cents in closing at $1.01 in trading 226,072 shares, Lasco Financial increased 10 cents to $1.80 after a transfer of 7,435 units, Limners and Bards dipped 24 cents and ended at $1.56, with 88,000 stocks crossing the market. Main Event slipped $1 to close at $12 with investors trading 100 stock units, MFS Capital Partners sank 5 cents to end at 83 cents with 2,660 shares clearing the market, Omni Industries gained 6 cents to finish at $1.10 with investors swapping 1,051,161 stock units. One Great Studio skidded 5 cents to 77 cents in switching ownership of 56,670 stocks and tTech rose 5 cents to close at $2.70, with 1,001 units crossing the market.

JFP Ltd shed 16 cents in closing at $1.01 in trading 226,072 shares, Lasco Financial increased 10 cents to $1.80 after a transfer of 7,435 units, Limners and Bards dipped 24 cents and ended at $1.56, with 88,000 stocks crossing the market. Main Event slipped $1 to close at $12 with investors trading 100 stock units, MFS Capital Partners sank 5 cents to end at 83 cents with 2,660 shares clearing the market, Omni Industries gained 6 cents to finish at $1.10 with investors swapping 1,051,161 stock units. One Great Studio skidded 5 cents to 77 cents in switching ownership of 56,670 stocks and tTech rose 5 cents to close at $2.70, with 1,001 units crossing the market.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Big plunge for Junior Market

The Junior Market of the Jamaica Stock Exchange dropped sharply on Thursday, following a 55 percent decline in the volume of stocks traded, with a 28 percent lower value than Wednesday with trading in 42 securities up from 40 on Wednesday and ending with prices of 13 rising, 19 declining and 10 finishing unchanged.

The market closed with trading of 2,685,073 shares for $6,623,219 down from 5,990,982 units at $9,247,492 on Wednesday.

The market closed with trading of 2,685,073 shares for $6,623,219 down from 5,990,982 units at $9,247,492 on Wednesday.

Trading averaged 63,930 shares at $157,696 compared with 149,775 units at $231,187 on Wednesday with the month to date, averaging 272,698 units at $496,319 compared with 291,473 stock units at $526,774 on the previous day and June with an average of 318,732 units at $696,979.

Stationery and Office Supplies led trading with 824,225 shares for 30.7 percent of total volume followed by Fosrich with 328,942 stock units for 12.3 percent of the day’s trade and Dolla Financial with 316,992 units for 11.8 percent market share.

At the close of trading, the Junior Market Index dived 68.15 points to close at 3,682.92.

The Junior Market ended trading with an average PE Ratio of 12.6, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows just one stock ending with a bid higher than the last selling price and three with lower offers, indicating a slight negative bias in trading on Friday.

At the close, AMG Packaging declined 11 cents to $3.19 in switching ownership of 24,500 stocks, Cargo Handlers popped $1.24 to close at $12.94 after 450 shares passed through the market, Caribbean Assurance Brokers fell 24 cents to finish at $3.50 trading 7,728 stocks. Caribbean Cream lost 30 cents and ended at $3.45 after an exchange of 28,357 stock units, Caribbean Flavours dipped 6 cents in closing at $1.54 with 5,300 stocks, Derrimon Trading slipped 5 cents to end at $2 after investors exchanged 501 shares. Dolla Financial dipped 11 cents to $2.49 with a transfer of 316,992 stock units, Dolphin Cove gained 18 cents and ended at $23.18, with 2,933 units crossing the exchange, EduFocal sank 5 cents to finish at a 52 weeks’ low of 43 cents with investors swapping 4,265 shares. Express Catering shed 13 cents to end at $3.90 and closed after an exchange of 8,352 units, Fontana dropped 35 cents in closing at $8.13 with investors dealing in 8,570 stocks, Honey Bun skidded 15 cents to close at $8.60 after an exchange of 33,962 stock units. Indies Pharma rose 9 cents to $2.59 in trading 840 shares,

At the close, AMG Packaging declined 11 cents to $3.19 in switching ownership of 24,500 stocks, Cargo Handlers popped $1.24 to close at $12.94 after 450 shares passed through the market, Caribbean Assurance Brokers fell 24 cents to finish at $3.50 trading 7,728 stocks. Caribbean Cream lost 30 cents and ended at $3.45 after an exchange of 28,357 stock units, Caribbean Flavours dipped 6 cents in closing at $1.54 with 5,300 stocks, Derrimon Trading slipped 5 cents to end at $2 after investors exchanged 501 shares. Dolla Financial dipped 11 cents to $2.49 with a transfer of 316,992 stock units, Dolphin Cove gained 18 cents and ended at $23.18, with 2,933 units crossing the exchange, EduFocal sank 5 cents to finish at a 52 weeks’ low of 43 cents with investors swapping 4,265 shares. Express Catering shed 13 cents to end at $3.90 and closed after an exchange of 8,352 units, Fontana dropped 35 cents in closing at $8.13 with investors dealing in 8,570 stocks, Honey Bun skidded 15 cents to close at $8.60 after an exchange of 33,962 stock units. Indies Pharma rose 9 cents to $2.59 in trading 840 shares,  Jamaican Teas lost 7 cents to finish at $2.25, with 4,256 stock units crossing the market, Knutsford Express slipped 15 cents and ended at $10.75 with traders dealing in 1,685 stocks. Lasco Financial sank 14 cents to end at $1.70 after a transfer of 6,200 stock units, Limners and Bards skidded 9 cents in closing at $1.80 with investors trading 1,462 shares, Lumber Depot rallied 5 cents to close at $2.80 after an exchange of 500 units. Main Event increased 50 cents to $13 with investors trading 7,700 stocks, One Great Studio climbed 5 cents to close at 82 cents in an exchange of 67,623 stock units, Regency Petroleum fell 9 cents to finish at $2.32 with 12,005 shares changing hands and Spur Tree Spices advanced 5 cents and ended at $1.95 with an exchange of 283,557 stocks.

Jamaican Teas lost 7 cents to finish at $2.25, with 4,256 stock units crossing the market, Knutsford Express slipped 15 cents and ended at $10.75 with traders dealing in 1,685 stocks. Lasco Financial sank 14 cents to end at $1.70 after a transfer of 6,200 stock units, Limners and Bards skidded 9 cents in closing at $1.80 with investors trading 1,462 shares, Lumber Depot rallied 5 cents to close at $2.80 after an exchange of 500 units. Main Event increased 50 cents to $13 with investors trading 7,700 stocks, One Great Studio climbed 5 cents to close at 82 cents in an exchange of 67,623 stock units, Regency Petroleum fell 9 cents to finish at $2.32 with 12,005 shares changing hands and Spur Tree Spices advanced 5 cents and ended at $1.95 with an exchange of 283,557 stocks.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

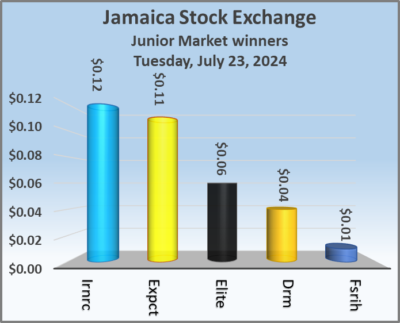

Junior market rises with negative sentiments

The Junior Market of the Jamaica Stock Exchange rallied on Wednesday, with trading in 40 securities, up marginally from 39 on Tuesday and ended with prices of 13 rising, 21 declining and six closing unchanged, with the market closing with negative market sentiment that is reflected in the Investor’s Choice bid-offer indicator on a day when trading volume and value were marginally different compared with Tuesday.

The market closed with an exchange of 5,990,982 shares for $9,247,492 compared with 5,601,327 stock units at $9,640,939 on Tuesday.

The market closed with an exchange of 5,990,982 shares for $9,247,492 compared with 5,601,327 stock units at $9,640,939 on Tuesday.

Trading averaged 149,775 shares at $231,187 versus 143,624 units at $247,204 on Tuesday with the month to date, averaging 291,473 units at $526,774 compared to 304,747 stock units at $554,463 on the previous day and June with an average of 318,732 units at $696,979.

EduFocal led trading with 1.75 million shares for 29.2 percent of total volume, with the stock trading at an intraday 52 weeks’ low of 40 cents followed by Stationery and Office Supplies with 1.07 million units for 17.9 percent of the day’s trade and Dolla Financial with 731,534 units for 12.2 percent market share.

At the close of trading, the Junior Market Index rallied 28.88 points to close at 3,751.07.

The Junior Market ended trading with an average PE Ratio of 12.6, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows four stocks ended with bids higher than their last selling prices and eight with lower offers.

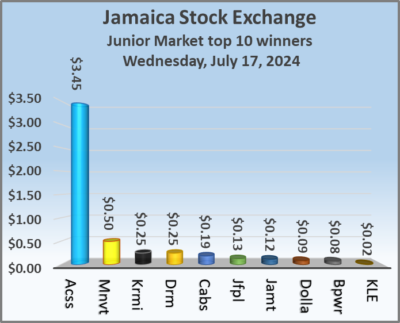

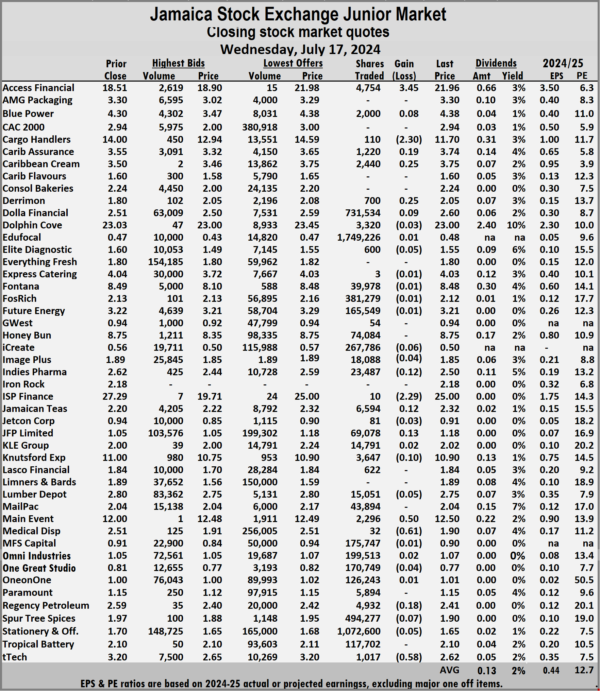

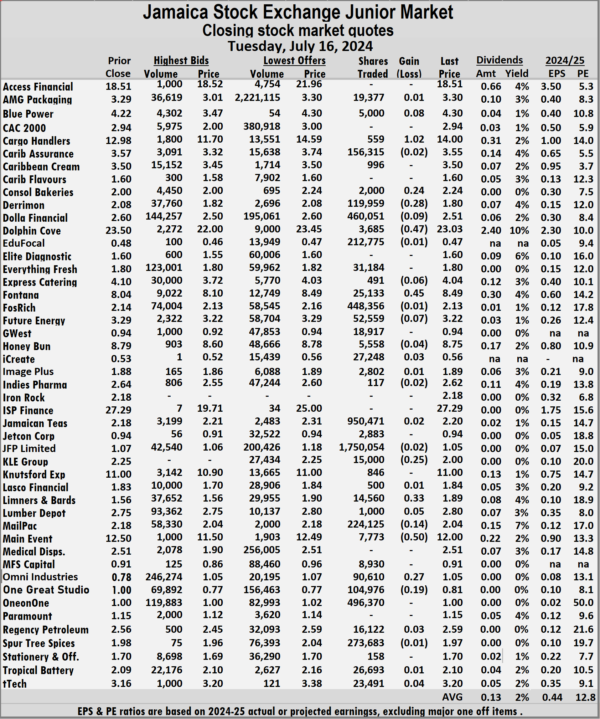

At the close, Access Financial climbed $3.45 to finish at $21.96 in an exchange of 4,754 stocks, Blue Power popped 8 cents to $4.38 after the trading of 2,000 units, Cargo Handlers sank $2.30 to close at $11.70 after a transfer of a mere 110 shares. Caribbean Assurance Brokers rallied 19 cents and ended at $3.74 with investors dealing in 1,220 stock units, Caribbean Cream increased 25 cents in closing at $3.75 with 2,440 shares clearing the market, Derrimon Trading advanced 25 cents to end at $2.05 in switching ownership of 700 stocks. Dolla Financial rose 9 cents in closing at $2.60 after 731,534 units passed through the market, Elite Diagnostic slipped 5 cents to $1.55 in trading 600 stock units, iCreate fell 6 cents to close at 50 cents after 267,786 shares crossed the market. Indies Pharma dipped 12 cents to finish at $2.50 with traders dealing in 23,487 stock units, ISP Finance sank $2.29 and ended at $25 after an exchange of 10 units, Jamaican Teas gained 12 cents to end at $2.32 with investors trading 6,594 stocks. JFP Ltd rose 13 cents in closing at $1.18 with an exchange of 69,078 shares,

At the close, Access Financial climbed $3.45 to finish at $21.96 in an exchange of 4,754 stocks, Blue Power popped 8 cents to $4.38 after the trading of 2,000 units, Cargo Handlers sank $2.30 to close at $11.70 after a transfer of a mere 110 shares. Caribbean Assurance Brokers rallied 19 cents and ended at $3.74 with investors dealing in 1,220 stock units, Caribbean Cream increased 25 cents in closing at $3.75 with 2,440 shares clearing the market, Derrimon Trading advanced 25 cents to end at $2.05 in switching ownership of 700 stocks. Dolla Financial rose 9 cents in closing at $2.60 after 731,534 units passed through the market, Elite Diagnostic slipped 5 cents to $1.55 in trading 600 stock units, iCreate fell 6 cents to close at 50 cents after 267,786 shares crossed the market. Indies Pharma dipped 12 cents to finish at $2.50 with traders dealing in 23,487 stock units, ISP Finance sank $2.29 and ended at $25 after an exchange of 10 units, Jamaican Teas gained 12 cents to end at $2.32 with investors trading 6,594 stocks. JFP Ltd rose 13 cents in closing at $1.18 with an exchange of 69,078 shares,  Knutsford Express skidded 10 cents to $10.90 and closed after an exchange of 3,647 stocks, Lumber Depot lost 5 cents to finish at $2.75, with 15,051 stock units crossing the exchange. Main Event rallied 50 cents and ended at $12.50 with investors swapping 2,296 stock units, Medical Disposables declined 61 cents to end at $1.90 with a transfer of 32 shares, Regency Petroleum shed 18 cents to close at $2.41, with 4,932 stock units crossing the market. Spur Tree Spices shed 7 cents to close at a 52 weeks’ low of $1.90 with investors trading 494,277 stock units, Stationery and Office Supplies lost 5 cents in closing at $1.65, with 1,072,600 units changing hands and tTech skidded 58 cents to close at $2.62 after an exchange of 1,017 shares.

Knutsford Express skidded 10 cents to $10.90 and closed after an exchange of 3,647 stocks, Lumber Depot lost 5 cents to finish at $2.75, with 15,051 stock units crossing the exchange. Main Event rallied 50 cents and ended at $12.50 with investors swapping 2,296 stock units, Medical Disposables declined 61 cents to end at $1.90 with a transfer of 32 shares, Regency Petroleum shed 18 cents to close at $2.41, with 4,932 stock units crossing the market. Spur Tree Spices shed 7 cents to close at a 52 weeks’ low of $1.90 with investors trading 494,277 stock units, Stationery and Office Supplies lost 5 cents in closing at $1.65, with 1,072,600 units changing hands and tTech skidded 58 cents to close at $2.62 after an exchange of 1,017 shares.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Steady Junior Market trades

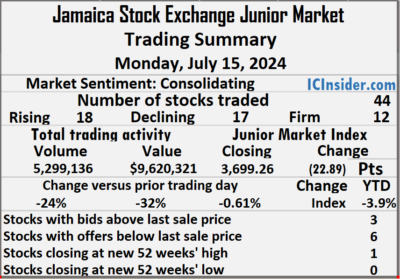

Market activity on Tuesday mirrored trading on Monday with a slightly elevated level with 5,601,327 shares changing hands for $9,640,939 up from 5,299,136 units at $9,620,321 on Monday on the Junior Market of the Jamaica Stock Exchange, resulting from trading in 39 securities down from 44 on Monday and ending with prices of 15 rising, 16 declining and eight closing unchanged. tTech traded at a 52 weeks’ high of $3.20, this follows last week’s announcement that the major ownership changed hands.

Trading averaged 143,624 shares at $247,204 compared with 120,435 units at $218,644 on Monday with the month to date, averaging 304,747 units at $554,463 compared to 320,942 stock units at $585,348 on the previous day and June with an average of 318,732 units at $696,979.

Trading averaged 143,624 shares at $247,204 compared with 120,435 units at $218,644 on Monday with the month to date, averaging 304,747 units at $554,463 compared to 320,942 stock units at $585,348 on the previous day and June with an average of 318,732 units at $696,979.

JFP Ltd led trading with 1.75 million shares for 31.2 percent of total volume, with the price hitting an intraday 52 weeks’ low of $1 followed by Jamaican Teas with 950,471 stocks for 17 percent of the day’s trade and ONE on ONE Educational with 496,370 units for 8.9 percent market share.

At the close of trading, the Junior Market Index rallied 22.93 points to lock up trading at 3,722.19.

The Junior Market ended trading with an average PE Ratio of 12.8, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows four stocks ended with bids higher than their last selling prices and four with lower offers.

At the close, Blue Power climbed 8 cents to close at $4.30, with 5,000 stock units crossing the market, Cargo Handlers rose $1.02 to $14 as investors exchanged just 559 shares, Consolidated Bakeries rallied 24 cents in closing at $2.24 after 2,000 stocks passed through the market. Derrimon Trading sank 28 cents to finish at $1.80 in an exchange of 119,959 units, Dolla Financial declined 9 cents and ended at $2.51, with 460,051 shares changing hands, Dolphin Cove shed 47 cents to end at $23.03 with 3,685 stock units crossing the exchange.  Express Catering sank 6 cents to $4.04 with investors dealing in 491 stocks, Fontana increased 45 cents to close at $8.49 after an exchange of 25,133 units, Future Energy skidded 7 cents to end at $3.22 with investors trading 52,559 stocks. KLE Group lost 25 cents in closing at $2 after 15,000 shares crossed the market, Limners and Bards popped 33 cents to finish at $1.89 with a transfer of 14,560 units, Lumber Depot gained 5 cents and ended at $2.80 after an exchange of 1,000 stock units. Mailpac Group dipped 14 cents to $2.04 and closed after 224,125 shares changed hands and Main Event fell 50 cents and ended at $12 with traders dealing in 7,773 units of its shares.

Express Catering sank 6 cents to $4.04 with investors dealing in 491 stocks, Fontana increased 45 cents to close at $8.49 after an exchange of 25,133 units, Future Energy skidded 7 cents to end at $3.22 with investors trading 52,559 stocks. KLE Group lost 25 cents in closing at $2 after 15,000 shares crossed the market, Limners and Bards popped 33 cents to finish at $1.89 with a transfer of 14,560 units, Lumber Depot gained 5 cents and ended at $2.80 after an exchange of 1,000 stock units. Mailpac Group dipped 14 cents to $2.04 and closed after 224,125 shares changed hands and Main Event fell 50 cents and ended at $12 with traders dealing in 7,773 units of its shares.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

tTech jumps 54% in three days

Shareholders in the Junior Market listed tTech have seen share price jumping more than 54 percent in the stock since it closed at $2.05 last Wednesday with it closing at a 52 weeks’ high of $3.16 on Monday, with more seeming likely, with only three offers to sell, between $3.56 and $6 just ahead of the close but end with just two offers at $4.05 and above.

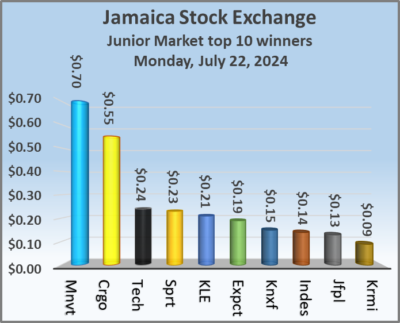

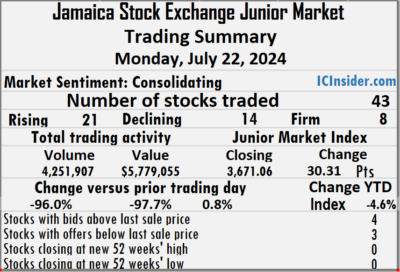

The Junior Market of the Jamaica Stock Exchange closed on Monday, with a 24 percent decline in the volume of stocks traded and a 32 percent lower value than Friday resulting in trading of 44 securities up sharply from just 33 on Friday and ending with prices of 18 rising, 17 declining and nine closing unchanged.

The Junior Market of the Jamaica Stock Exchange closed on Monday, with a 24 percent decline in the volume of stocks traded and a 32 percent lower value than Friday resulting in trading of 44 securities up sharply from just 33 on Friday and ending with prices of 18 rising, 17 declining and nine closing unchanged.

At the close of the day, tTech gained 26 percent but did little to ease the pain of the Junior Market that dropped, with the average price of heavily weighted Derrimon Trading and a near $2 drop in Access Financial helping to pull the market down. At the close of trading, the Junior Market Index dropped 22.89 points to wrap up trading at 3,699.26.

The market closed with trading of 5,299,136 shares for $9,620,321 compared with 6,927,786 units at $14,113,440 on Friday.

Trading averaged 120,435 shares at $218,644 compared with 209,933 units at $427,680 on Friday with the month to date, averaging 320,942 units at $585,348 compared to 346,589 stock units at $632,252 on the previous day and June with an average of 318,732 units at $696,979.

Derrimon Trading led trading with 1.28 million shares for 24.1 percent of total volume followed by Omni Industries with 1.17 million stocks for 22 percent of the day’s trade and Spur Tree Spices with 479,681 units for 9.1 percent market share.

The Junior Market ended trading with an average PE Ratio of 12.8, based on last traded prices and earnings projected by ICInsider.com for the financial years ending around August 2025.

The Junior Market ended trading with an average PE Ratio of 12.8, based on last traded prices and earnings projected by ICInsider.com for the financial years ending around August 2025.

Investor’s Choice bid-offer indicator shows just three stocks ending with bids higher than their last selling prices and six with lower offers.

At the close, Access Financial dropped $1.44 to $18.51 as investors exchanged 15,465 shares, AMG Packaging rose 10 cents in closing at $3.29 after 36,326 stock units passed through the market, Blue Power slipped 8 cents to $4.22 with an exchange of 1,050 units. Caribbean Assurance Brokers declined 18 cents to close at $3.57, with 402 stocks changing hands, Caribbean Cream sank 25 cents to finish at $3.50 after 17,916 units passed through the exchange, Caribbean Flavours advanced 6 cents and ended at $1.60 in trading just 333 shares. Consolidated Bakeries skidded 25 cents to $2 after an exchange of a mere 1,301 stock units, Dolla Financial popped 10 cents to end at $2.60 with investors trading 26,882 stocks, Fontana lost 26 cents in closing at $8.04 with 70,473 shares clearing the market.

Honey Bun climbed 10 cents to finish at $8.79 with a transfer of 3,510 stock units, Jamaican Teas shed 17 cents and ended at $2.18, with investors trading 314,434 units, Knutsford Express rallied 10 cents to close at $11 after an exchange of 1,150 stocks. Lasco Financial gained 13 cents to close at $1.83 with investors trading 2,319 shares, Mailpac Group rallied 12 cents to end at $2.18 after a transfer of 72,793 stocks, Main Event increased 95 cents in closing at $12.50 with an exchange of 5,099 units. MFS Capital Partners dropped 5 cents to close at 91 cents in an exchange of 83,559 stock units, Regency Petroleum popped 24 cents to finish at $2.56 with traders dealing in 50,895 shares, Stationery and Office Supplies advanced 5 cents and ended at $1.70 in an exchange of 69,395 stocks. Tropical Battery fell 9 cents to $2.09 after 54,548 units passed through the market and tTech rose 66 cents and ended at a 52 weeks’ high of $3.16 with investors dealing in 214,359 stock units.

Honey Bun climbed 10 cents to finish at $8.79 with a transfer of 3,510 stock units, Jamaican Teas shed 17 cents and ended at $2.18, with investors trading 314,434 units, Knutsford Express rallied 10 cents to close at $11 after an exchange of 1,150 stocks. Lasco Financial gained 13 cents to close at $1.83 with investors trading 2,319 shares, Mailpac Group rallied 12 cents to end at $2.18 after a transfer of 72,793 stocks, Main Event increased 95 cents in closing at $12.50 with an exchange of 5,099 units. MFS Capital Partners dropped 5 cents to close at 91 cents in an exchange of 83,559 stock units, Regency Petroleum popped 24 cents to finish at $2.56 with traders dealing in 50,895 shares, Stationery and Office Supplies advanced 5 cents and ended at $1.70 in an exchange of 69,395 stocks. Tropical Battery fell 9 cents to $2.09 after 54,548 units passed through the market and tTech rose 66 cents and ended at a 52 weeks’ high of $3.16 with investors dealing in 214,359 stock units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.