Обновили на порносайте

pornobolt.tv порно страничку о том как парень выебал пизду мачехи, которая устала от своего муженька

Ei jälkiä pölystä: muista tämän puhdistusliuoksen koostumus - Rauman Varaosahalli

Mitkä kukat puutarhurit istuttavat taimille helmikuussa: 3 suosittua lajia - Rauman Varaosahalli

Älä kiirehdi vaihtamaan älypuhelimen akkua: 6 tapaa säästää latausta - Rauman Varaosahalli

Miksi kokeneet emännät eivät heitä pois munakartonkipakkauksia: 6 tarpeellista käyttötarkoitusta - Rauman Varaosahalli

Hernemato ei enää koskaan ilmesty - agronomi on ehdottanut kahta yksinkertaista toimenpidettä - Rauman Varaosahalli

Valurautaiset paistinpannut pysyvät vapaina rasvasta ja noesta: kokeile tätä välttämätöntä ratkaisua - Rauman Varaosahalli

Älä heitä niitä pois: lääkäri selitti, miksi kirsikan lehdet ovat arvokkaampia kuin itse marjat - Rauman Varaosahalli

Älä heitä tölkkejä pois: 12 tapaa käyttää niitä kotona ja maaseudulla - Rauman Varaosahalli

Älä heitä sipulin kuoria pois: sitä varten tämä 'roska' on ennen uutta vuotta - Rauman Varaosahalli

Kuoren maku yllättää sinut: muista tämä paistettujen perunoiden resepti - Rauman Varaosahalli

Älä heitä vanhaa mattoasi pois: 9 ideaa sen käyttämiseen kotona ja maaseudulla - Rauman Varaosahalli

Ikkunalaudastasi tulee kukkivien orkideoiden tuoksuinen: lehtikirja kauniiden kukkien kasvattamiseen - Rauman Varaosahalli

Älä heitä paperipyyhkeiden hylsyjä pois: 9 tapaa käyttää niitä kotona ja keittiössä - Rauman Varaosahalli

Sekoita ruokasooda ja Fairy: et usko, mitä tämä seos voi tehdä - Rauman Varaosahalli

Älä heitä vanhoja muovipusseja pois: 5 tapaa käyttää niitä kotona ja kodissa - Rauman Varaosahalli

Terveysministeriö kertoi, mitä viruksia Valko-Venäjällä tällä hetkellä liikkuu - Rauman Varaosahalli

Älä heitä sipulin kuoria pois: tulet hämmästymään, miten fiksut puutarhurit käyttävät niitä - Rauman Varaosahalli

Mistä tunnistaa kypsän appelsiinin: muutama lehtitieto kypsien ja maukkaiden hedelmien valintaan - Rauman Varaosahalli

Miksi vetyperoksidia lisätään lattioita puhdistettaessa: kokeneiden kotiäitien menetelmä - Rauman Varaosahalli

Älä heitä paperipyyhkeiden hylsyjä pois: 7 tapaa käyttää niitä kotona ja keittiössä - Rauman Varaosahalli

Älä kiirehdi hankkiutumaan eroon vanhasta matosta: 8 hyödyllistä tapaa käyttää sitä kotona ja maaseudulla - Rauman Varaosahalli

Monet kotiäidit kaatavat väärin kiehuvaa vettä lavuaariin: tässä on, mikä voi vahingoittua - Rauman Varaosahalli

Miksi esi-isämme kantoivat mukanaan laakerinlehteä: muutama niksi isoäideiltämme - Rauman Varaosahalli

Miten saat takaisin pehmeyden vuodevaatteisiisi: 8 vinkkiä fiksuilta ja säästäväisiltä emänniltä - Rauman Varaosahalli

Nokkela muurahaisloukku: tämä on ainoa tapa pelastaa hedelmäpuut tuholaisilta - Rauman Varaosahalli

Do ziemniaków i pierogów: zrób najsmaczniejszy sos grzybowy na Boże Narodzenie - Bludenz

Jeśli przegapiłeś ten smak: jak zrobić chrupiącą sałatkę z zielonej cebuli - Bludenz

Marynowane grzyby w kilka godzin - na stół lub dla odmiany - Bludenz

Zbiory będą zadowolone z obfitości: dodaj kaszę gryczaną do gleby w kwietniu - Bludenz

Sałatka ze szczotką: zwięzły przepis, który pasuje absolutnie do wszystkiego - Bludenz

Nie wyrzucaj klipsów do torebek na chleb: pamiętaj o 9 przydatnych sposobach ich wykorzystania - Bludenz

Wlać bezpośrednio do garnka - mętny bulion stanie się klarowny w ciągu kilku sekund - Bludenz

Idealny przepis dla tych, którzy się spieszą: szybki gulasz z kurczakiem w chińskim stylu - Bludenz

Danie z dawnych czasów: wieloletni przepis na kolache od 'MasterChefa' Vladimira Yaroslavsky'ego - Bludenz

Goście będą oblizywać palce: kanapki z awokado - sekret tkwi w specjalnym sosie - Bludenz

Delikatny, kwaśny i obłędnie pyszny: najlepszy sos do klopsików - goście połkną go językami - Bludenz

Nie wyrzucaj kiełków starych ziemniaków: zręczne gospodynie domowe znalazły dla nich przydatne zastosowania - Bludenz

Królewski luksus na Twoim stole: sekret najbardziej soczystej ryby w piekarniku - Bludenz

Jak jeszcze sprytne hostessy używają folii aluminiowej: 4 niezbędne sytuacje domowe - Bludenz

Oto funkcje, o których istnieniu nawet nie wiedziałeś: nie uwierzysz, co potrafi Twoja kuchenka mikrofalowa - Bludenz

Przepis na magiczny sok dyniowy prosto z Hogwartu: poczuj się jak Harry Potter - Bludenz

Uwaga: Rosjanom powiedziano, jak wybrać gotowe mięso na kebab - Bludenz

Nie wrócisz do innych przepisów - przygotuj ziemniaki w mundurkach metodą Iny Garten - Bludenz

Twarożek czekoladowy i ciasto wiśniowe: palce lizać - Bludenz

Sprzedawane w każdym Magnit: Roskachestvo znalazł najlepsze naleśniki z mięsem - Bludenz

Jedz chipsy w ten sposób: nie szkodzą, tylko bawią - Bludenz

Okulary będą lśnić czystością: pamiętaj o składnikach tego domowego środka czyszczącego - Bludenz

Co najczęściej psuje pralkę: zapamiętaj 5 najczęstszych błędów - Bludenz

Zalej twaróg wrzątkiem: jeśli tak się stanie, wyrzuć go do kosza - Bludenz

Trzy dania, które pokochasz: co zrobić z wczorajszego makaronu? - Bludenz

Kotlety będą soczyste i rozpłyną się w ustach: wystarczy dodać ten produkt do mięsa mielonego - Bludenz

Zostaw łyżkę w worku z mąką - korzyści będą niesamowite: zapomniana sztuczka naszych babć - Bludenz

Pożółkły plastik znów będzie lśnił bielą: wypróbuj ten roztwór czyszczący z mydłem - Bludenz

Nieopisanie świeża i lekka: przepis na pyszną wiosenną sałatkę - Bludenz

Bez piekarnika, bez mąki - pizza na stole w 10 minut - Bludenz

Pasztet z piekarnika w pięć minut, który podbił internet - Bludenz

Najszybszy przepis na delikatne naleśniki - gotują się w kuchence mikrofalowej w 45 sekund - Bludenz

Astrologická předpověď pro 30.04 pro všechna znamení zvěrokruhu - Bludenz

První a nejdůležitější krmení česnekem: 2 lžíce na záhon - velké a šťavnaté hlavy - Dumeto

Rajčata jsou sladká, masitá a téměř 5 kg na keř: zahrádkáři jsou z této nové odrůdy nadšeni - Dumeto

Odstraňte tyto části stromu: příští rok bude růst s bláznivou silou - Dumeto

Tyto 4 druhy zeleniny můžete bez obav sázet i v červenci: sklizeň bude zajištěna - Dumeto

Kde začít s výukou angličtiny: zkuste se naučit první slovíčka - Dumeto

Gladioly potěší bujnými květy - vysazujte je pouze podle těchto pravidel - Dumeto

Mají železné zdraví: 4 dlouhověká plemena koček, která se dožívají až 25 let - Dumeto

Zvyšte výnosy půdy bez kapky 'chemie': metody zkušených dachařů - Dumeto

Jak znovu použít hliníkovou fólii: sedm osvědčených způsobů pro domácnost - Dumeto

Po medvědovi nezůstane ani stopa: jak zachránit brambory před zákeřným škůdcem - geniální trik - Dumeto

Zbavte se plevele pouze v těchto dnech: účinek je okamžitý - Dumeto

Pračka přestane při odstřeďování skákat: 4 tipy pro odstranění vibrací - Dumeto

Vaše sazenice obsadili roztoči - žádný problém: lidový lék za pár drobných vaše sazenice zachrání - Dumeto

Nejmódnější manikúra podzimu-2023: stylová varianta v kávovém odstínu (foto) - Dumeto

Jak ještě šikovné hospodyňky používají mouku v domácnosti: 6 užitečných lifehacků pro domácnost a kuchyň - Dumeto

Rusové 'trik', jak ušetřit peníze na dovolené u moře - technika je velmi jednoduchá - Dumeto

Tento krásný siderát je 100krát lepší než hořčice: zvýší výnosy rajčat a zbaví je plevele - Dumeto

Půdní mušky si zapomenou cestu k sazenicím - prolijte je tímto přípravkem - Dumeto

Budete vypadat jako buran: stylista jmenuje hlavní chybu při výběru kabelky - Dumeto

Nevyhazujte staré plastové karty: 5 způsobů, jak je využít doma i v domácnosti - Dumeto

Venku je -30 °C a sněhová vánice, ale u vás doma je teplo: už žádný průvan z okna - 1 geniální způsob - Dumeto

Nevyhazujte svou starou bundu: 9 užitečných způsobů využití nepotřebného oblečení - Dumeto

Stejně dobré jako luxusní, ale za hubičku: 4 nejlepší levné rtěnky a lesky na rty - Dumeto

Nenechávejte špinavé nádobí přes noc venku: bojte se bakterií a negativní energie - Dumeto

4 věci, které ničí i dokonalé vztahy - Dumeto

Expertul în somn dezvăluie: Bea această poțiune magică și spune adio sforăitului pentru totdeauna - Chelsea Larabee

Fericitul câștigător a 100.000 de cărți de răzuit: 'Oamenii ar fi crezut că sunt nebun.' - Chelsea Larabee

V-ați săturat de calcar în baie? Află cele mai eficiente sfaturi ale experților pentru a scăpa de el - Chelsea Larabee

Kim Kardashian cu vești nebănuite - Chelsea Larabee

Economisiți bani la factura de încălzire: Iată 7 sfaturi eficiente - Chelsea Larabee

Un concurent de la 'Holder vi et år' dezvăluie: Nu vezi asta în program - Chelsea Larabee

O tânără de 22 de ani a postat o fotografie online: 37 de minute mai târziu, și-a dat seama de grozăvia jenantă - Chelsea Larabee

Toată lumea ar trebui să știe acest lucru despre caloriferul lor: Cum să evitați o factură prea mare - Chelsea Larabee

Expert: Trebuie să acționăm curând, altfel Ucraina este doar începutul - Chelsea Larabee

Nicole a încercat să oprească alarma de pe Apple Watch-ul iubitului ei: Apoi a făcut o descoperire care i-a zguduit lumea - Chelsea Larabee

Îl lasă în pantofi peste noapte - pantofii redevin ca și cum ar fi noi - Chelsea Larabee

Un medic avertizează asupra unei pandemii invizibile: Mă tem de ea mai mult decât de Corona - Chelsea Larabee

Coaforul danez oferă 3 motive probabile pentru care părul tău pare decolorat - Chelsea Larabee

Majoritatea oamenilor recunosc o broască la prima vedere: doar câțiva recunosc calul în mai puțin de 10 secunde - Chelsea Larabee

O mamă și-a lăsat fiul de 9 ani singur, fără acces la apă și căldură, timp de doi ani: Atât de lungă este pedeapsa - Chelsea Larabee

Își face un tatuaj cu un breton pentru a-și acoperi chelia, dar izbucnește în lacrimi din cauza rezultatului dezastruos - Chelsea Larabee

Economisiți mii de lire sterline în această iarnă cu ajutorul acestui mnemonic simplu - Chelsea Larabee

Un clip sălbatic devine viral: Transportă o întreagă colonie de albine pe braț - Chelsea Larabee

De aceea, mingile de tenis și bilele de staniol sunt de aur pentru rufele tale - Chelsea Larabee

Un bărbat aflat într-un Range Rover a intrat direct într-o mulțime de oameni pe o stradă pietonală din Germania - Chelsea Larabee

Experții avertizează: Nu ignorați niciodată aceste mirosuri - Chelsea Larabee

Donald Trump, cu o soluție drastică la o problemă care se agravează: Împușcați-i - Chelsea Larabee

Trucul cu staniol pe balcon: La ce se folosește? - Chelsea Larabee

Testul de vedere: Ai ochi de șoim dacă poți vedea ce ardei iute este desenat - Chelsea Larabee

O femeie deschide o conservă de fasole cumpărată din supermarket - și găsește un șarpe - Chelsea Larabee

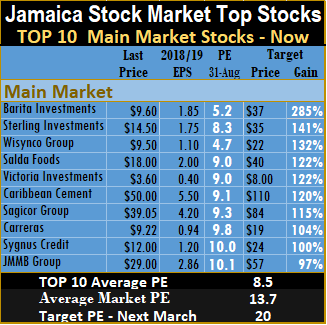

returns within a 12 months period. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

returns within a 12 months period. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

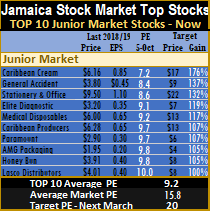

higher this week with buying orders in for 139,000 shares at $15. The price of Stanley Motta climbed to $5.27 during the week from $4.81 in the previous week and exited the main market list.

higher this week with buying orders in for 139,000 shares at $15. The price of Stanley Motta climbed to $5.27 during the week from $4.81 in the previous week and exited the main market list.

for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

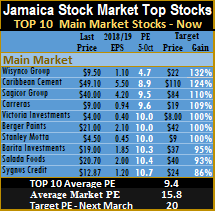

During the past week, the main market of the Jamaica Stock Exchange, racked up more record closes but pulled back on sharply on Thursday and Junior market hit new highs during the week but dropped sharply on Friday due mainly to

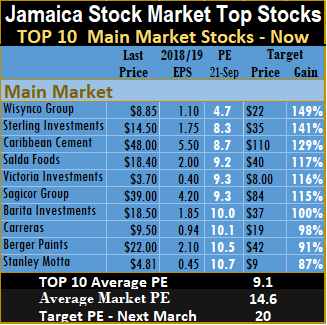

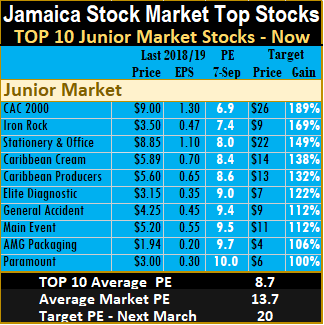

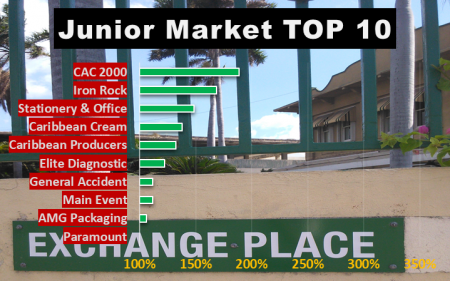

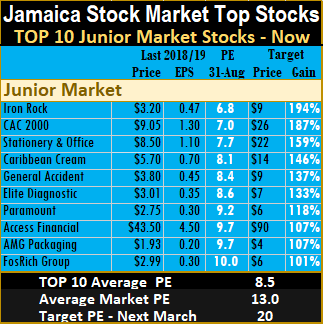

During the past week, the main market of the Jamaica Stock Exchange, racked up more record closes but pulled back on sharply on Thursday and Junior market hit new highs during the week but dropped sharply on Friday due mainly to  The PE ratio for Junior Market Top 10 stocks average 9.3 up from 8.9 last week, as the market continues to revalue the multiple higher and the main market PE is now 9.1, up from 8.8 last week, for the top stocks.

The PE ratio for Junior Market Top 10 stocks average 9.3 up from 8.9 last week, as the market continues to revalue the multiple higher and the main market PE is now 9.1, up from 8.8 last week, for the top stocks. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

the sole factor influencing the change.

the sole factor influencing the change.

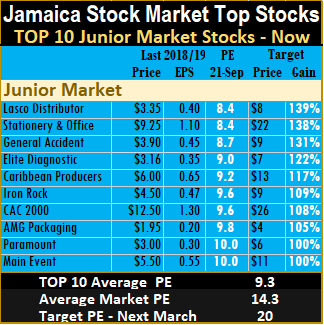

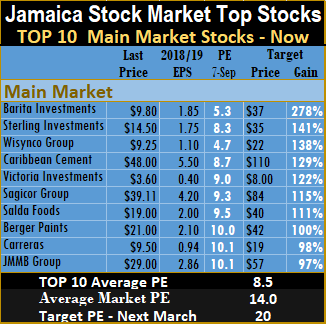

The latest valuation compares to an average PE for the overall market of 13.7, based on 2018 estimated earnings. The main market PE is now 8.5 and is the same level as last week, for the top stocks, compared to a market average of 14.

The latest valuation compares to an average PE for the overall market of 13.7, based on 2018 estimated earnings. The main market PE is now 8.5 and is the same level as last week, for the top stocks, compared to a market average of 14. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well. Both the Jamaica Stock Exchange, main and Junior markets reached higher levels during the past week, with the main market hitting a series of new record highs. The coming weeks should see more gains as investors seek out opportunities as fixed interest returns have tanked.

Both the Jamaica Stock Exchange, main and Junior markets reached higher levels during the past week, with the main market hitting a series of new record highs. The coming weeks should see more gains as investors seek out opportunities as fixed interest returns have tanked.  The company is in the process of another acquisition, this time overseas, this should continue to help boost profit going forward. Fosrich posted good second quarter results and is on target to reach IC Insider.com’s forecasted earnings of 30 cents per share. Fosrich too, could be making an acquisition later this year, or early 2019, unofficial, but credible reports suggest. JMMB Group posted good first quarter results with a 59 percent increase in net profit. Some of the strong gains came from the relatively sharp fall in the value of the Jamaican dollar in the period that is not expected to continue.

The company is in the process of another acquisition, this time overseas, this should continue to help boost profit going forward. Fosrich posted good second quarter results and is on target to reach IC Insider.com’s forecasted earnings of 30 cents per share. Fosrich too, could be making an acquisition later this year, or early 2019, unofficial, but credible reports suggest. JMMB Group posted good first quarter results with a 59 percent increase in net profit. Some of the strong gains came from the relatively sharp fall in the value of the Jamaican dollar in the period that is not expected to continue. Work done by IC Insider.com suggests that the PE ratio is likely to end 2018 around 16 to 18 times earnings, as investors continue to upgrade the multiple they are prepared to pay for stocks, which would lift prices sharply over the next several months from current levels. The latest government bond offer with a 4.58 years tenor, was heavily oversubscribed, resulting in rates dropping to 3.95 percent, suggesting that investors are satisfied that the economic policies will continue to lead to low inflation for a considerable time. These rates suggest more funds will be going into stocks as liquidity remains high in the financial system.

Work done by IC Insider.com suggests that the PE ratio is likely to end 2018 around 16 to 18 times earnings, as investors continue to upgrade the multiple they are prepared to pay for stocks, which would lift prices sharply over the next several months from current levels. The latest government bond offer with a 4.58 years tenor, was heavily oversubscribed, resulting in rates dropping to 3.95 percent, suggesting that investors are satisfied that the economic policies will continue to lead to low inflation for a considerable time. These rates suggest more funds will be going into stocks as liquidity remains high in the financial system.

TOP 10 stocks are likely to deliver the best returns within a 12 months period. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

TOP 10 stocks are likely to deliver the best returns within a 12 months period. Stocks are selected based on projected earnings for each company’s current fiscal year. Based on an assumed PE for each, the likely gains are determined and then ranked, with the stocks with the highest potential gains ranked first followed by the rest, in descending order. Potential values will change as stock prices fluctuate and will result in movements of the selection in and out of the lists for most weeks. Earnings per share are revised on an ongoing basis based on new information received that can result in changes in and out of the list as well.

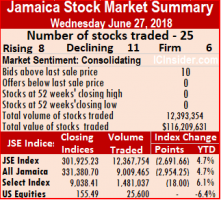

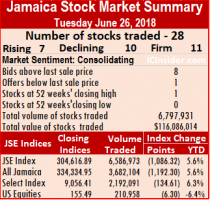

At the close of market activity, 12,367,754 units valued at $115,843,551 changed hands compared to 6,586,973 units valued at $111,180,207, on Tuesday.

At the close of market activity, 12,367,754 units valued at $115,843,551 changed hands compared to 6,586,973 units valued at $111,180,207, on Tuesday. The JSE USD Equities Index closed unchanged at 155.49.

The JSE USD Equities Index closed unchanged at 155.49.

Trading volume was dominated by

Trading volume was dominated by  Proven Investments traded 203,000 units at 20 US cents. The JSE USD Equities Index dropped 6.30 points to close at 155.49.

Proven Investments traded 203,000 units at 20 US cents. The JSE USD Equities Index dropped 6.30 points to close at 155.49. At the close on the Jamaica Stock Exchange on Monday, the All Jamaican Composite Index rose 867.41 points to 335,527.25 while the JSE Index gained 790.30 points to 305,703.21.

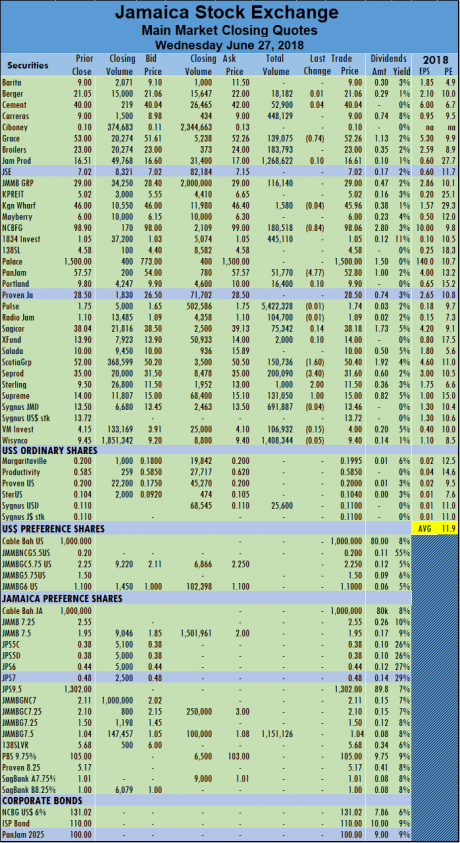

At the close on the Jamaica Stock Exchange on Monday, the All Jamaican Composite Index rose 867.41 points to 335,527.25 while the JSE Index gained 790.30 points to 305,703.21.  JMMB Group 7.50% preference share with 1,618,000 units that accounted for 40.08 percent of the main market volume followed by Carreras with 677,448 stock units or 16.78 percent and Scotia Group with 363,434 shares.

JMMB Group 7.50% preference share with 1,618,000 units that accounted for 40.08 percent of the main market volume followed by Carreras with 677,448 stock units or 16.78 percent and Scotia Group with 363,434 shares. Trading resulted in an average of 168,216 units valued at an average of $2,319,549 compared to 691,163 units valued at $10,961,779 on Friday. For the month to date 216,970 units traded with an average value of $5,389,348 and on the previous day 219,629 units traded with an average value of $5,567,307 on average. May closed with an average of 589,414 shares with a value of $16,532.367, for each security traded.

Trading resulted in an average of 168,216 units valued at an average of $2,319,549 compared to 691,163 units valued at $10,961,779 on Friday. For the month to date 216,970 units traded with an average value of $5,389,348 and on the previous day 219,629 units traded with an average value of $5,567,307 on average. May closed with an average of 589,414 shares with a value of $16,532.367, for each security traded. Some 3,200 applications with more than $3.8 billion chased after the

Some 3,200 applications with more than $3.8 billion chased after the  The company intends to pay out up to 85 percent of its net income as dividends to shareholders, payable on a quarterly basis. The target dividend yield is over 7 percent on the IPO price.

The company intends to pay out up to 85 percent of its net income as dividends to shareholders, payable on a quarterly basis. The target dividend yield is over 7 percent on the IPO price.