Stocks are set for a major ride higher in 2024 following two years of subpar performance of the Jamaica Stock Exchange. The market did not perform well in 2023, the Main Market fell 8.5 percent and the Junior Market the US dollar market declined by 3.5 percent and 1.2 percent respectively, but technical reading of the Main Market is pointing to a solid rally ahead, with some stocks breaking out of a prolonged period of consolidation.

Bank of Jamaica (BOJ) raised interest rates in 2021 with the overnight rate landing at 7 percent in November 2022 and has remained there since, with BOJ keeping a tight lid on market rates by the use of Certificate of Deposits with rates mostly around 10 percent on average, to tame inflation that peaked close to 12 percent in early 2023.

Bank of Jamaica (BOJ) raised interest rates in 2021 with the overnight rate landing at 7 percent in November 2022 and has remained there since, with BOJ keeping a tight lid on market rates by the use of Certificate of Deposits with rates mostly around 10 percent on average, to tame inflation that peaked close to 12 percent in early 2023.

The stock market has not performed well in that environment. Contrasting that with the US where the Federal Reserve raised rates over two years, with the last increase in July last year. Notwithstanding, the US stock market indices were racing forward and are now at record levels while the JSE Main Market is still below the Covid-19-affected levels but the Junior Market trades at much higher levels than the lows of 2020.

Many investors consider that higher interest rates reduce stock prices, but they are only partially correct. Interest rates affect the valuation of stocks not necessarily the price of stocks. Put another way, higher rates reduce the PE ratios used to value stocks but if profits are rising faster than the increase in rates, stock values will tend to rise as the company is more valuable despite the rate increase. With rising rates the PE ratio mostly used in stock valuation will fall with rising rates and rise when rates are declining.

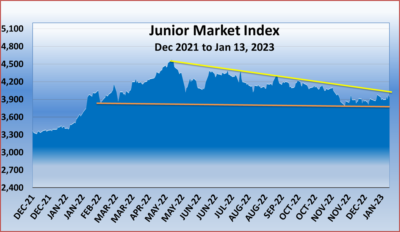

The Junior Market is presently in a triangular formation that will lead to a big breakout soon.

If profits don’t rise above the level of PE decline then the market will most likely adjust the stock price down. So while interest rates remained stable in 2023 at levels higher than 2021, a total of 31 companies posted gains in the market last year. That is the reason why Scotia Group posted gains from late 2023 into 2024, with some others doing likewise. Other factors to consider are that higher rates may result in higher interest costs for some companies or reduced revenues that could reduce profit but companies with investment funds may enjoy higher profits as they may enjoy increased interest income.

The lack of performance for the Jamaica Stock Exchange last year was not interest rates, but mostly lacklustre profit performance by several companies. What the issue illustrates is the import of careful stock selection with a focus on companies with a good track record of growing profits consistently over several years.

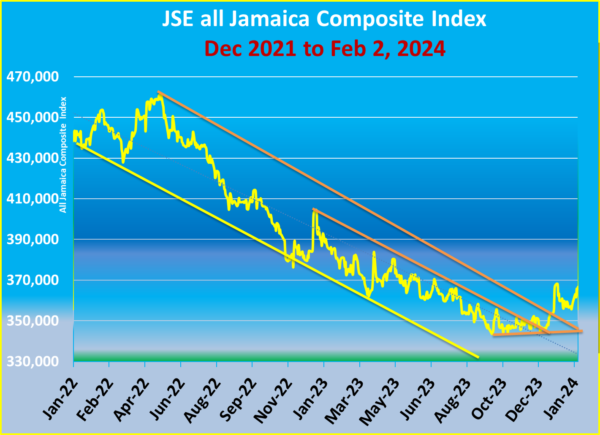

Technical indicators are pointing to a bottoming out of the Main Market that has broken out from a market squeeze, with technical indicators indicating a huge run ahead for the market, see market index chart. At the same time, the Junior Market closed 2023, with a negative undertone that could remain in place for a while until events push it in a new direction. Company profits seem the most likely factor in the medium term.

Part of the decline in the Junior Market in 2023 is due to an overall level of over-exuberance by investors in 2022, pushing the prices of a limited number of Junior Market stocks to unrealistic levels, with sharp correction for some of these in 2023 and helping to drag the market. The situation in the Main Market was somewhat different with a lack of interest from institutional investors until the final quarter of the year which is reflected in a continuous slide in the Main Market Index throughout the year until the end of September, indeed from a two-year high of 461,783 points on the All Jamaica Composite Index in May 2022 until it bottomed at the end of September 2023 at 344,153 points and put on almost 23,000 points to the end of the year. While the Main Market declined for two consecutive years, the Junior Market was experiencing its first yearly decline since 2020.

Part of the decline in the Junior Market in 2023 is due to an overall level of over-exuberance by investors in 2022, pushing the prices of a limited number of Junior Market stocks to unrealistic levels, with sharp correction for some of these in 2023 and helping to drag the market. The situation in the Main Market was somewhat different with a lack of interest from institutional investors until the final quarter of the year which is reflected in a continuous slide in the Main Market Index throughout the year until the end of September, indeed from a two-year high of 461,783 points on the All Jamaica Composite Index in May 2022 until it bottomed at the end of September 2023 at 344,153 points and put on almost 23,000 points to the end of the year. While the Main Market declined for two consecutive years, the Junior Market was experiencing its first yearly decline since 2020.

Inflation moderated during the year within the central bank’s target of 4 to 6 percent on a number of occasions. By the end of November, the year over year inflation rate was just above the bank’s upper limit of 6 percent, with the rate hitting 6.9 percent in December. Certain price adjustments particularly in public transportation impacted inflation negatively towards the latter part of the year, some of these may carry over into 2024. The bank also fears possible wage increases that could be unusually high and place upward pressure on inflation.

For the first three months of 2024, it should be instructive to see where inflation is likely to be and what could become of interest rates during the year. What is clear is that falling market rates in the USA are likely to set the tone ultimately in Jamaica and that should be aided by expectations that the FED will start reducing rates during the second quarter of 2024.

A look at the stock market at this juncture suggests that profits should continue to be positive as can be seen from a compilation of company results for the third quarter of 2023. Data shows that profits for the nine months are up 4 percent and for the quarter up a B 46 percent over similar periods in 2022. A major part of the drag on profits was approximately $11 billion provisions made by NCB Financial for staff redundancies and one-time bonus compensation.

Barring increased interest rates, the Jamaican economy should grow just around two percent in 20224 and that ought to be sufficient to help generate increased demand for goods and services and assist many listed companies to increase profits from existing operations. Expanding companies will see above average performances.

Barring increased interest rates, the Jamaican economy should grow just around two percent in 20224 and that ought to be sufficient to help generate increased demand for goods and services and assist many listed companies to increase profits from existing operations. Expanding companies will see above average performances.

The Junior Market and the Main Market of the Jamaica Stock Exchange are flashing bullish signals that suggest an uptick in the market. This is reflected in projected PE ratios for 2024 for both markets with the projected ratios well below the current levels of valuation for 2023.

The average PE for the JSE Main and Junior Market for 2024 based on that year’s earnings is 10.5 and 9 respectively, compared to the current levels of 14 based on 2023 earnings, at the same time the ICTOP 15 based on 2024 earnings stand at around 5, well below the market average of 14, barring increases in interest rates and disappointing profits, PE ratios should return to the average around 14, resulting in a 180 percent jump in values for the IC TOP15 stocks during 2024 at the minimum, and more if the country’s central bank lowers rates during 2024, with a 50 percent rise in the overall market.

Data for the market in 2023 showed that companies with outstanding profit growth found favour with investors who bid the prices of those stocks higher in most cases. Stocks of companies with profit declining or with moderate profit increases were mostly marked down by the investing public. Examples, are to be found in TransJamaican Highway, Lasco Distributors, Lasco Manufacturers, Dolphin Cove, General Accident, Fontana, Main Event, Knutsford Express and Scotia Group with Wisynco Group to name a few that enjoyed price gains. A number of the performances of these stocks benefited from recovery in the tourism sector directly or indirectly.

For 2024, companies that are expanding may be worth investing in as they are likely to enjoy above-average growth in revenues and profits going forward. Companies in this category include Wisynco, Caribbean Cement, Caribbean Cream, Grace Kennedy, Jamaican Teas, Caribbean Producers, Jetcon, Fontana, Express Catering, Stationery and Office Supplies, Edufocal, Transjamaican Highway, Stanley Motta, and Tropical Battery.

The Junior Market ICTOP15 is set for a significant upward climb over the next 15 months as solid economic growth continues and interest rates pull back in 2023. There will be a considerable uptick in Tourism arrivals for the winter season as the sector delivers record performance as it will have fully recovered from the disrupter to the industry in 2020 and deliver record revenues and profits for several companies.

The Junior Market ICTOP15 is set for a significant upward climb over the next 15 months as solid economic growth continues and interest rates pull back in 2023. There will be a considerable uptick in Tourism arrivals for the winter season as the sector delivers record performance as it will have fully recovered from the disrupter to the industry in 2020 and deliver record revenues and profits for several companies.

Caribbean Cream – EPS 2023 is 70 cents, and $1.30 for 2024

Caribbean Cream – EPS 2023 is 70 cents, and $1.30 for 2024

Honey Bun – projected EPS of $1 per share for the 2023 fiscal year and $1.85 for 2024

Honey Bun – projected EPS of $1 per share for the 2023 fiscal year and $1.85 for 2024

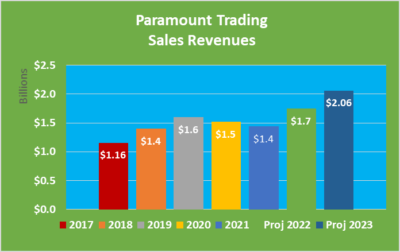

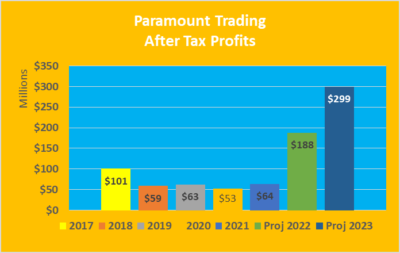

According to the company’s Chairman, Radcliff Knibbs in his report to shareholders on the half year results, “Paramount’s improved performance was achieved by employment of a robust growth strategy.” He went on to state, “we will continue to pivot our operations to take advantage of any possible opportunities that may arise.” He concluded that “we expect that our strategic objectives will be realized through strong income growth and cost containment.

According to the company’s Chairman, Radcliff Knibbs in his report to shareholders on the half year results, “Paramount’s improved performance was achieved by employment of a robust growth strategy.” He went on to state, “we will continue to pivot our operations to take advantage of any possible opportunities that may arise.” He concluded that “we expect that our strategic objectives will be realized through strong income growth and cost containment. Earnings per share came out at 2 cents for the quarter and 3 cents for the year to date. IC Insider.com is forecasting 12 cents per share for the fiscal year ending May 2022 and 20 cents for 2023. The stock that is now added to IC Insider.com

Earnings per share came out at 2 cents for the quarter and 3 cents for the year to date. IC Insider.com is forecasting 12 cents per share for the fiscal year ending May 2022 and 20 cents for 2023. The stock that is now added to IC Insider.com