Knowledge of a country’s economy is important in making investment decisions. Past performance while important is no guarantee that the future will be the same or better than the past. The Jamaican economy is looking good for 2024, with prospects of slower growth than for 2023, even as the Bank of Jamaica (BOJ) maintains a tight monetary policy that could persist for much of 2024.

Barring increased interest rates, the Jamaican economy should grow around two percent in 2024, which will be down from around 2.7 percent in 2023. Growth in tourism and production at the Alcoa Alumina plant has now moderated from the sharp recovery in the early part of 2023, providing the stimulant for higher growth in 2023 but that added stimulant will not be there in 2024 as output from these sectors return to more normal levels.

In support of the above, the September quarter shows GDP growth moderating to 2.10 percent, this level of growth is unlikely to change much over the next few quarters. But BOJ could ease the tight monetary policy to provide some breathing space for increased production of goods and services, but this will have to await continued moderation in inflation, and there will be a lag of months for such easing to start feeding into increased production when such easing takes place. The early months of the year will be a guide as inflation should continue to moderate as the months unfold and pave the way for some interest rate reduction.

In support of the above, the September quarter shows GDP growth moderating to 2.10 percent, this level of growth is unlikely to change much over the next few quarters. But BOJ could ease the tight monetary policy to provide some breathing space for increased production of goods and services, but this will have to await continued moderation in inflation, and there will be a lag of months for such easing to start feeding into increased production when such easing takes place. The early months of the year will be a guide as inflation should continue to moderate as the months unfold and pave the way for some interest rate reduction.

Inflation, although down sharply from the highs in 2022, is still not fully under control, with the average for 2023 running close to the upper end of the central bank’s target of 4 to 6 percent. Some developments that should help in bringing the rate down, include world oil prices that have fallen in 2023 to the low US$70 level and prices of some other commodities continue to fall into the latter part of 2023 and will have a moderating effect on inflation going forward. Some local costs may have an upward push on inflation but traditionally the period of December to April is usually months of very low inflation and in many cases, negative price movements as local food prices tend to normalize.

A tighter labour market locally could put upward pressure on wages and prices, but tighter monetary policy now in place from last year and some major wage adjustments from 2023 to compensate for loss of purchasing power then, may mean that the expected high wage adjustments may not feed into price rise as may otherwise be expected and could hold prices down for a while.

Despite the tourism sector returning to the usual historical growth levels it is expected that this sector will contribute to growth in 2024 and help stimulate growth in industries with a strong linkage to the sector. Assuming fair weather conditions, Agriculture, the star performer in the economy for several years should return to positive growth in 2024 in recovering from declines in 2023 and the sector will be helped by continued growth in the tourism sector that feeds off it. The BPO sector seems poised to continue to add to growth but there are issues with available manning. With continued growth in housing, road construction and the need for factories and warehousing space, the construction sector could hold its own during the year, but there may well be a lull in the sector with the two south coast roads coming to completion in 2023 or early in 2024. The Montego Bay perimeter road should take over but may not fully fill the gap.

Despite the tourism sector returning to the usual historical growth levels it is expected that this sector will contribute to growth in 2024 and help stimulate growth in industries with a strong linkage to the sector. Assuming fair weather conditions, Agriculture, the star performer in the economy for several years should return to positive growth in 2024 in recovering from declines in 2023 and the sector will be helped by continued growth in the tourism sector that feeds off it. The BPO sector seems poised to continue to add to growth but there are issues with available manning. With continued growth in housing, road construction and the need for factories and warehousing space, the construction sector could hold its own during the year, but there may well be a lull in the sector with the two south coast roads coming to completion in 2023 or early in 2024. The Montego Bay perimeter road should take over but may not fully fill the gap.

ICinsider.com don’t see interest moving higher and most likely will start to decline before midyear with inflation within reach of the BOJ target of 4-6 percent in 2022 and with treasury bill rates seeming to peak in the 8 percent region and remaining relatively stable for several months. Certificate of deposit rates have been holding stable around 10 percent for months.

BOJ interest cuts overnight rate.

Unemployment at 4.5 percent in July last year is expected to fall further in 2024 towards the 3.5 to 4 percent region as more workers are needed to man the economic expansion. Companies will need to find innovative means to keep production going by implementing cost saving initiatives, otherwise, this could mean wage increases could rise above normal in order to retain or attract new workers.

The above is good news for the private sector overall that should see increasing demand for goods and services.

The banking sector showed loans growing at an annual pace of 13.5 percent per annum up to $1,216 billion to September over the $1,071 billion at the end of September 2022, data from Bank of Jamaica shows. Increased loan rates may be negatively affecting some areas and thus stymie demand. With what could be a year of reducing interest rates engineered by BOJ there could be even faster loan growth in 2023 than in 2022. Data for the September quarter show loans increasing by nearly 4 percent or 16 percent annualized compared with just 2 percent in the June quarter or 8 percent for twelve months.

Remittances in 2023 are down by 1.2 percent to the end of September to US$2.53 billion and appear that it will be just short of the US$3.44 billion generated in 2022 but should come in at just over $3.4 billion for the year. Based on trends it may be steady in 2024.

Jamaica’s Net International Reserves continue to grow and are at a healthy $4.75 billion in December, last year, data released by Bank of Jamaica shows, a huge improvement over $3.98 billion in December 2022.

Jamaica’s Net International Reserves continue to grow and are at a healthy $4.75 billion in December, last year, data released by Bank of Jamaica shows, a huge improvement over $3.98 billion in December 2022.

With continued growth in tourism, the resurgence in the Alumina sector and relatively stable remittances, improvements in local exports and continued growth in the BPO sector, the country should be enjoying record inflows of foreign exchange in 2024, putting BOJ in a good position to lower interest rates during the year as the reserves have been significantly built up.

Developments on the foreign exchange front will result in greater stability in the exchange rate for the local dollar as the tight monetary policy resulted in a US$770 million increase in the NIR and is likely to result in further build-up in the NIR in 2024. Investors should not be surprised if there is some revaluation of the local currency as well, especially in the first half of the year as the tight monetary policy pressures demand for foreign exchange.

The manufacturing sector should continue to continue positively to growth following expansions taking of a number of large companies.

The entertainment and transportation sectors seem poised to get a shot in the arm and benefit from the rebound in tourism, increased employment in the country and the general buoyancy in the wider economy.

Investors should pay attention to developments in the political seen as developments here can cause economic disruptions and muddy the investments environment.

The present government will be in power for four years at the end of August, but they have seen a reversal a huge lead over the opposition party in 2022 evaporated in one poll, with the opposition party having a slim lead. Another polling body done in August had the governing party leading with an increased margin over the previous poll, that showed both parties in a close race. Local government elections are due by February 2024, and barring some major negative development these elections appear ae set to proceed as planned. If the opposition does well in these elections it could result in the political heat being turned up a notch or two on the government going forward and could well trigger the calling of General Elections earlier than September 2025.

The present government will be in power for four years at the end of August, but they have seen a reversal a huge lead over the opposition party in 2022 evaporated in one poll, with the opposition party having a slim lead. Another polling body done in August had the governing party leading with an increased margin over the previous poll, that showed both parties in a close race. Local government elections are due by February 2024, and barring some major negative development these elections appear ae set to proceed as planned. If the opposition does well in these elections it could result in the political heat being turned up a notch or two on the government going forward and could well trigger the calling of General Elections earlier than September 2025.

The above are positive developments but investors cannot ignore the impact that the war in Ukraine hand the Israeli-Hamas war can have going forward that could affect the world economies.

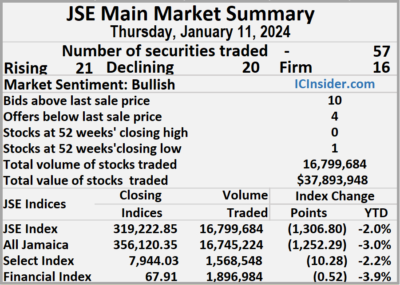

The market closed with an exchange of 16,799,684 shares costing a total of $37,893,948 compared to 12,511,690 units at $136,341,735 on Wednesday.

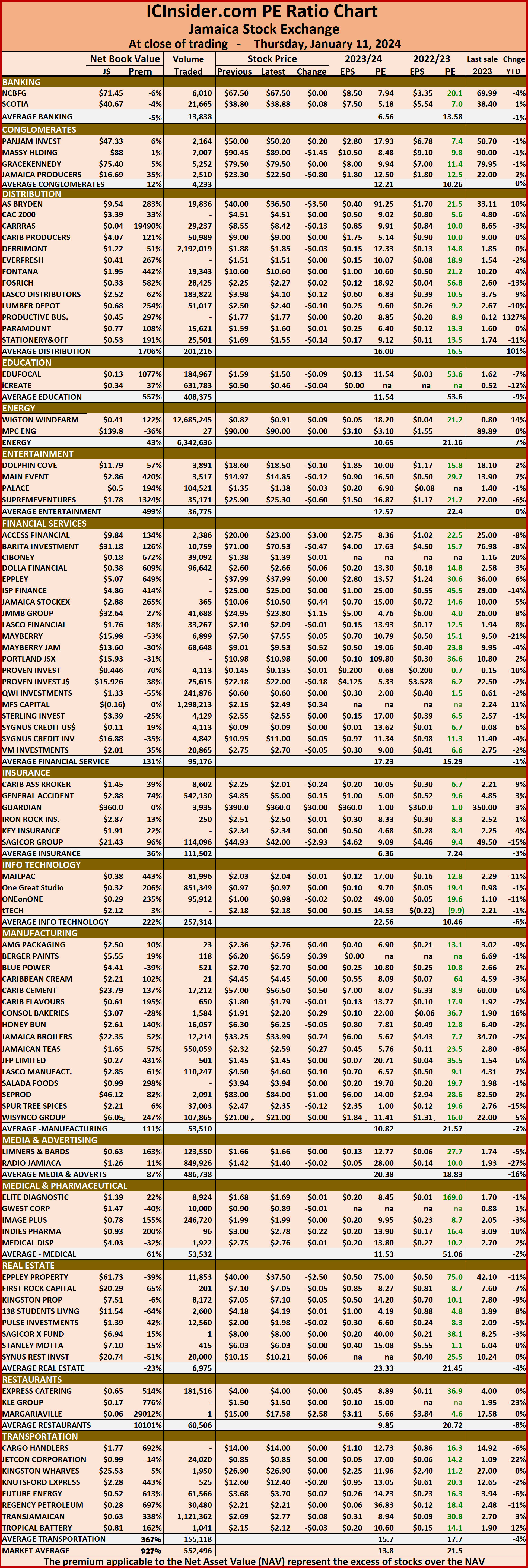

The market closed with an exchange of 16,799,684 shares costing a total of $37,893,948 compared to 12,511,690 units at $136,341,735 on Wednesday. The Main Market ended trading with an average PE Ratio of 13.5. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending around August 2024.

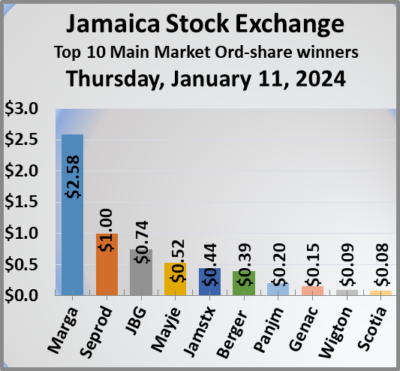

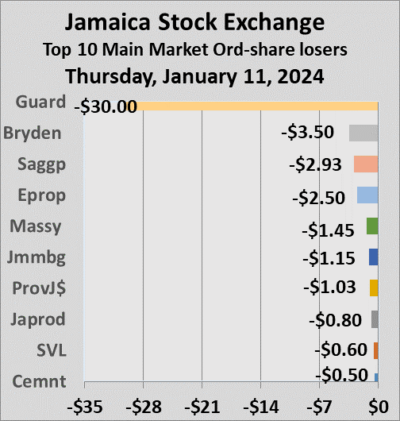

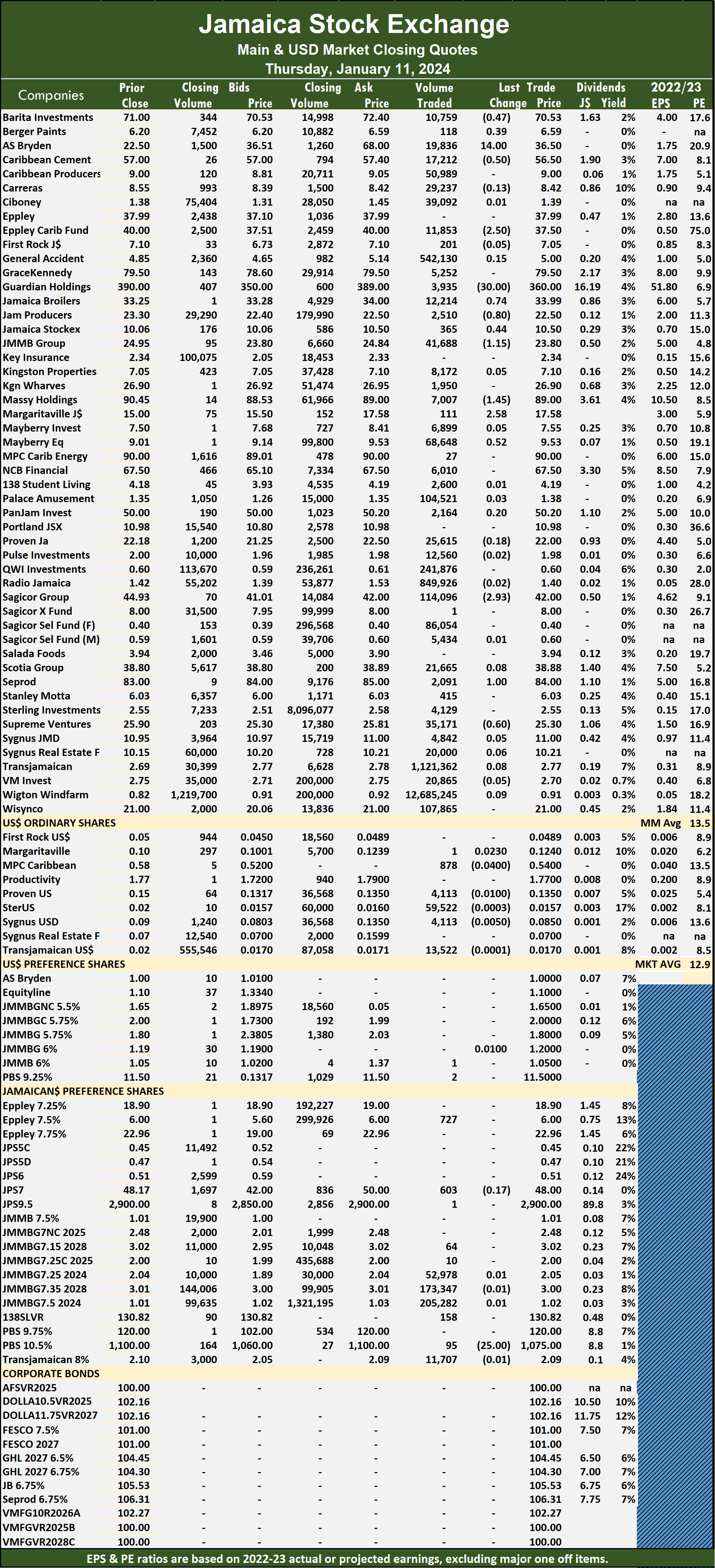

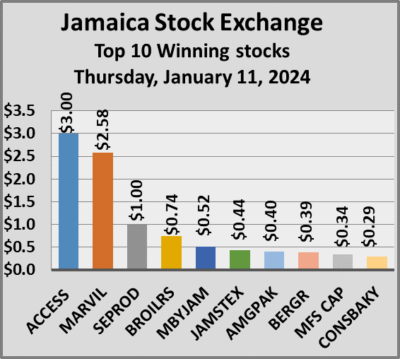

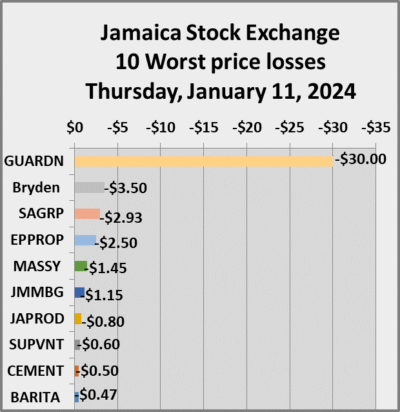

The Main Market ended trading with an average PE Ratio of 13.5. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending around August 2024. JMMB Group dipped $1.15 to close at 52 weeks’ low of $23.80, with 41,688 stock units passing through the market, Margaritaville rose $2.58 to $17.58 after exchanging 111 stocks, Massy Holdings skidded $1.45 to $89 in trading 7,007 units. Mayberry Jamaican Equities gained 52 cents to end at $9.53 after an exchange of 68,648 stock units, Sagicor Group lost $2.93 in closing at $42 with a transfer of 114,096 shares, Seprod climbed $1 and ended at $84 with investors trading 2,091 shares and Supreme Ventures shed 60 cents to end at $25.30 in switching ownership of 35,171 units.

JMMB Group dipped $1.15 to close at 52 weeks’ low of $23.80, with 41,688 stock units passing through the market, Margaritaville rose $2.58 to $17.58 after exchanging 111 stocks, Massy Holdings skidded $1.45 to $89 in trading 7,007 units. Mayberry Jamaican Equities gained 52 cents to end at $9.53 after an exchange of 68,648 stock units, Sagicor Group lost $2.93 in closing at $42 with a transfer of 114,096 shares, Seprod climbed $1 and ended at $84 with investors trading 2,091 shares and Supreme Ventures shed 60 cents to end at $25.30 in switching ownership of 35,171 units. Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

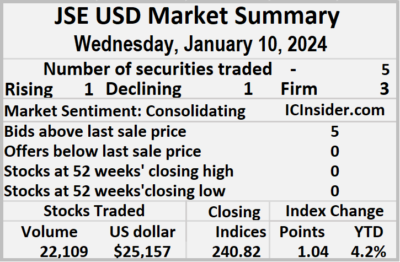

Prices of securities trading are those for the last transaction of each stock unless otherwise stated. The market closed with an exchange of 81,185 shares for US$2,499 compared with 22,109 units at US$25,157 on Wednesday.

The market closed with an exchange of 81,185 shares for US$2,499 compared with 22,109 units at US$25,157 on Wednesday. Sterling Investments dipped 0.03 of a cent to 1.57 US cents, with investors exchanging 59,522 stocks, Sygnus Credit Investments slipped 0.5 of one cent to close at 8.5 US cents with an exchange of 3,146 stock units and Transjamaican Highway skidded 0.01 of a cent to 1.7 US cents after 13,522 shares cleared the market.

Sterling Investments dipped 0.03 of a cent to 1.57 US cents, with investors exchanging 59,522 stocks, Sygnus Credit Investments slipped 0.5 of one cent to close at 8.5 US cents with an exchange of 3,146 stock units and Transjamaican Highway skidded 0.01 of a cent to 1.7 US cents after 13,522 shares cleared the market. The market closed on Thursday, with 7,215,549 shares changing hands for $14,447,149 up from 4,153,063 units at $9,236,370 on Wednesday.

The market closed on Thursday, with 7,215,549 shares changing hands for $14,447,149 up from 4,153,063 units at $9,236,370 on Wednesday. Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and six with lower offers.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and six with lower offers. Lasco Distributors climbed 12 cents to close at $4.10, with 183,822 stock units crossing the market, Lasco Manufacturing increased 10 cents to $4.60 in switching ownership of 110,247 stocks, Lumber Depot sank 10 cents and ended at $2.40 after 51,017 units passed through the market. Main Event dropped 12 cents to close at $14.85 with an exchange of 3,517 shares, MFS Capital Partners advanced 34 cents in closing at $2.49 with traders dealing in 1,298,213 stocks, following an announcement of a directors’ meeting to consider recapitalization of the company, Spur Tree Spices dipped 12 cents to end at $2.35, with 37,003 units crossing the market and Stationery and Office Supplies sank 14 cents in closing at $1.55 with investors dealing in 25,501 stock units.

Lasco Distributors climbed 12 cents to close at $4.10, with 183,822 stock units crossing the market, Lasco Manufacturing increased 10 cents to $4.60 in switching ownership of 110,247 stocks, Lumber Depot sank 10 cents and ended at $2.40 after 51,017 units passed through the market. Main Event dropped 12 cents to close at $14.85 with an exchange of 3,517 shares, MFS Capital Partners advanced 34 cents in closing at $2.49 with traders dealing in 1,298,213 stocks, following an announcement of a directors’ meeting to consider recapitalization of the company, Spur Tree Spices dipped 12 cents to end at $2.35, with 37,003 units crossing the market and Stationery and Office Supplies sank 14 cents in closing at $1.55 with investors dealing in 25,501 stock units. Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated. At the close of trading on Thursday, the JSE Combined Market Index dropped 991.34 points to 332,385.19, the All Jamaican Composite Index declined 1,252.29 points to 356,120.35, the JSE Main Index dropped 1,306.80 points to 319,222.85. The Junior Market Index added 26.75 points to settle at 3,768.57 and the JSE USD Market Index shed 2.75 points to close at 238.07.

At the close of trading on Thursday, the JSE Combined Market Index dropped 991.34 points to 332,385.19, the All Jamaican Composite Index declined 1,252.29 points to 356,120.35, the JSE Main Index dropped 1,306.80 points to 319,222.85. The Junior Market Index added 26.75 points to settle at 3,768.57 and the JSE USD Market Index shed 2.75 points to close at 238.07. At the close of the market, some of the major rising Main Market stocks are Margaritaville rose $2.58 to $17.58 and Seprod climbed $1 and ended at $84.

At the close of the market, some of the major rising Main Market stocks are Margaritaville rose $2.58 to $17.58 and Seprod climbed $1 and ended at $84. Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock.

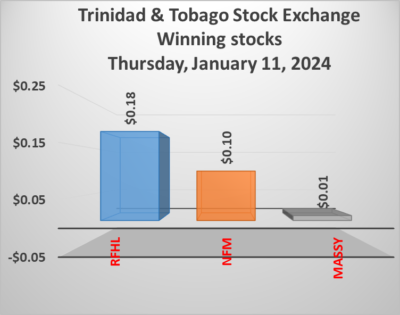

Investors should use the chart to help make rational decisions when investing in stocks close to the average for the sector and not going too far from it unless there are compelling reasons to do so. This approach helps to remove emotions from investment decisions and place them on fundamentals while at the same time not being too far from the majority of investors. Investors who buy when the price of a stock is close to the average will find that they are not inclined to overpay for a stock. The Composite Index fell 9.49 points to end at 1,205.61, the All T&T Index shed 18.44 points to settle at 1,803.79, the SME Index slipped 0.35 points to 78.23 and the Cross-Listed Index popped 0.01 points to 79.14.

The Composite Index fell 9.49 points to end at 1,205.61, the All T&T Index shed 18.44 points to settle at 1,803.79, the SME Index slipped 0.35 points to 78.23 and the Cross-Listed Index popped 0.01 points to 79.14. At the close, Agostini’s ended at $68.50 and closed with an exchange of 266 units, Angostura Holdings dropped $2.69 in closing at $20.05 with 145 stocks being traded, CinemaOne shed 10 cents to $6.90 with investors transferring 100 shares. First Citizens Group declined 1 cent and ended at $50 with 15,918 stocks trading, FirstCaribbean International Bank fell 5 cents to close at $7 with investors swapping 10,000 shares, GraceKennedy skidded 6 cents to $4.11 with an exchange of 17,082 stock units. Guardian Holdings lost 25 cents in closing at $18 with investors trading 2,000 units, JMMB Group remained at $1.28 with a transfer of 19,207 stocks, Massy Holdings popped 1 cent and ended at $4.45 while exchanging 57,812 units. National Enterprises sank 10 cents to close at $3.55 with investors trading 20,771 stocks,

At the close, Agostini’s ended at $68.50 and closed with an exchange of 266 units, Angostura Holdings dropped $2.69 in closing at $20.05 with 145 stocks being traded, CinemaOne shed 10 cents to $6.90 with investors transferring 100 shares. First Citizens Group declined 1 cent and ended at $50 with 15,918 stocks trading, FirstCaribbean International Bank fell 5 cents to close at $7 with investors swapping 10,000 shares, GraceKennedy skidded 6 cents to $4.11 with an exchange of 17,082 stock units. Guardian Holdings lost 25 cents in closing at $18 with investors trading 2,000 units, JMMB Group remained at $1.28 with a transfer of 19,207 stocks, Massy Holdings popped 1 cent and ended at $4.45 while exchanging 57,812 units. National Enterprises sank 10 cents to close at $3.55 with investors trading 20,771 stocks,  National Flour Mills gained 10 cents to end at $1.99, with 42,102 shares changing hands, Point Lisas remained at $3.90 in trading 2,076 stock units. Prestige Holdings ended at $9.30 after an exchange of 2,011 shares, Republic Financial rose 18 cents and ended at $122.58 after 1,728 units passed through the market, Scotiabank dipped 1 cent to close at $69.98 with traders dealing in 469 stocks and Trinidad & Tobago NGL fell $1.28 to a 52 weeks’ low of $9.38 with 28,871 stock units clearing the market.

National Flour Mills gained 10 cents to end at $1.99, with 42,102 shares changing hands, Point Lisas remained at $3.90 in trading 2,076 stock units. Prestige Holdings ended at $9.30 after an exchange of 2,011 shares, Republic Financial rose 18 cents and ended at $122.58 after 1,728 units passed through the market, Scotiabank dipped 1 cent to close at $69.98 with traders dealing in 469 stocks and Trinidad & Tobago NGL fell $1.28 to a 52 weeks’ low of $9.38 with 28,871 stock units clearing the market.

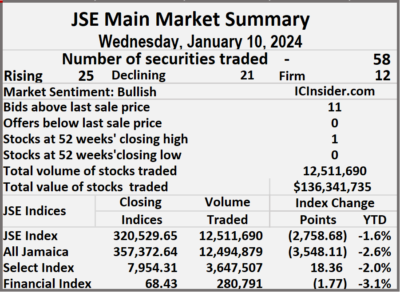

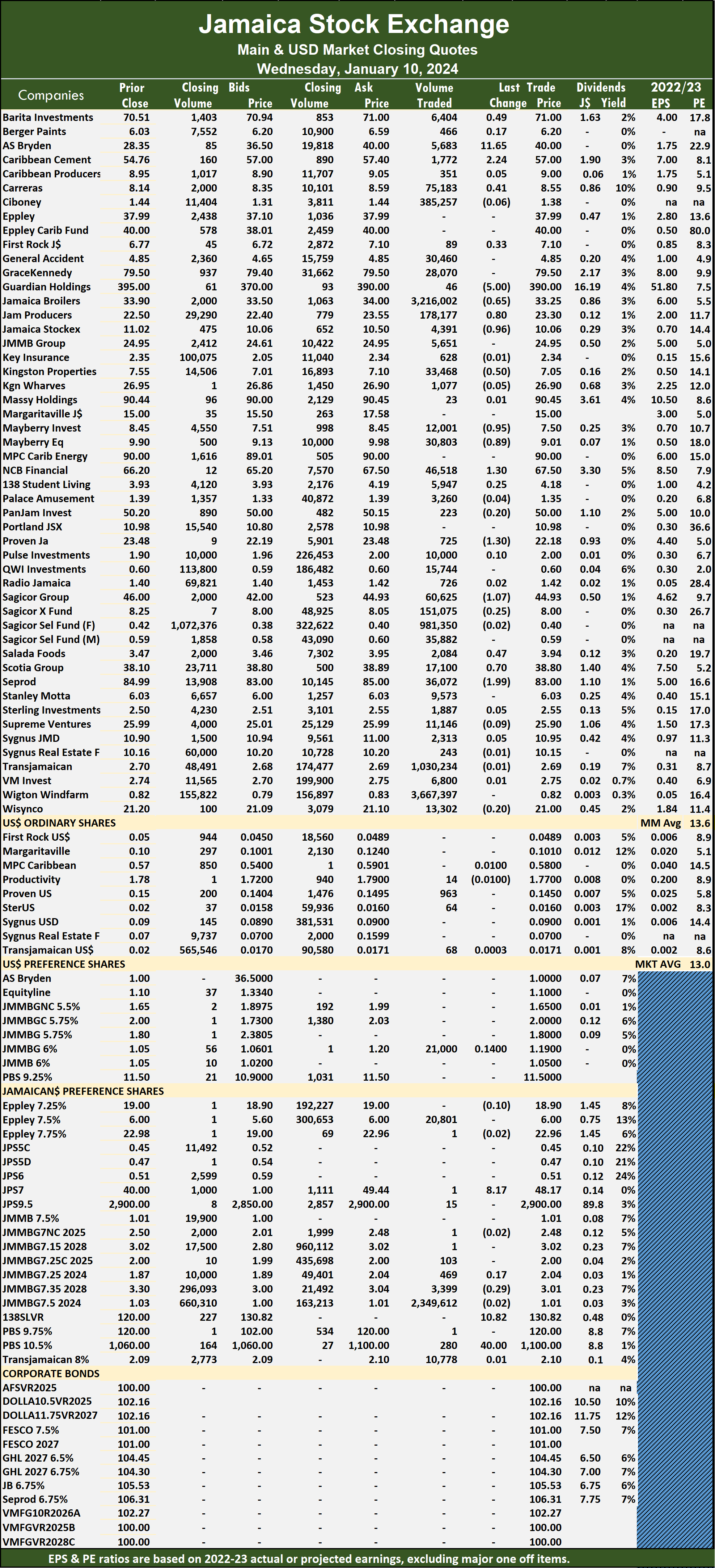

The market closed with an exchange of 12,511,690 shares at $136,341,735 from 5,418,018 units at $22,750,182 on Tuesday.

The market closed with an exchange of 12,511,690 shares at $136,341,735 from 5,418,018 units at $22,750,182 on Tuesday. The Main Market ended trading with an average PE Ratio of 13.6. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending around August 2024.

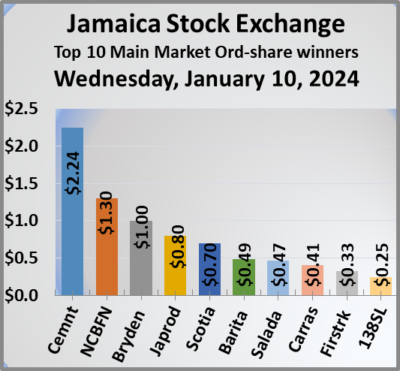

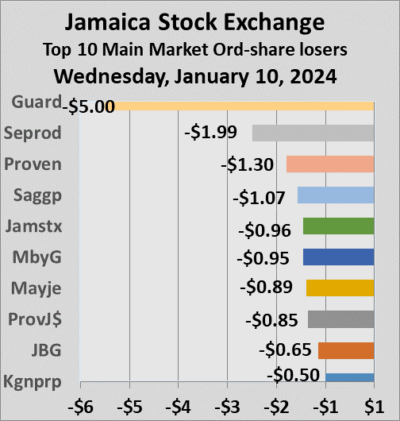

The Main Market ended trading with an average PE Ratio of 13.6. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending around August 2024. Kingston Properties fell 50 cents and ended at $7.05 in switching ownership of 33,468 stocks being traded, Mayberry Group fell 95 cents to $7.50 with 12,001 units, Mayberry Jamaican Equities shed 89 cents to close at $9.01 in trading 30,803 stocks. NCB Financial gained $1.30 in closing at $67.50 with 46,518 units crossing the exchange, Proven Investments dropped $1.30 and ended at $22.18 with traders dealing in 725 stocks, Sagicor Group skidded $1.07 to end at $44.93 after a transfer of 60,625 shares. Salada Foods popped 47 cents to $3.94, with 2,084 stock units crossing the market, Scotia Group advanced 70 cents to close at $38.80 after an exchange of 17,100 shares and Seprod sank $1.99 and ended at $83 with investors transferring 36,072 stock units.

Kingston Properties fell 50 cents and ended at $7.05 in switching ownership of 33,468 stocks being traded, Mayberry Group fell 95 cents to $7.50 with 12,001 units, Mayberry Jamaican Equities shed 89 cents to close at $9.01 in trading 30,803 stocks. NCB Financial gained $1.30 in closing at $67.50 with 46,518 units crossing the exchange, Proven Investments dropped $1.30 and ended at $22.18 with traders dealing in 725 stocks, Sagicor Group skidded $1.07 to end at $44.93 after a transfer of 60,625 shares. Salada Foods popped 47 cents to $3.94, with 2,084 stock units crossing the market, Scotia Group advanced 70 cents to close at $38.80 after an exchange of 17,100 shares and Seprod sank $1.99 and ended at $83 with investors transferring 36,072 stock units. Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated. The market closed with an exchange of 22,109 shares for US$25,157 compared to 135,574 units at US$3,223 on Tuesday.

The market closed with an exchange of 22,109 shares for US$25,157 compared to 135,574 units at US$3,223 on Tuesday. Investor’s Choice bid-offer indicator shows five stocks ended with bids higher than their last selling prices and none with a lower offer.

Investor’s Choice bid-offer indicator shows five stocks ended with bids higher than their last selling prices and none with a lower offer. The market closed on wednesday with an exchange of 4,153,063 stock units at $9,236,370 from 9,032,533 shares at $15,706,426 on Tuesday.

The market closed on wednesday with an exchange of 4,153,063 stock units at $9,236,370 from 9,032,533 shares at $15,706,426 on Tuesday. The Junior Market ended trading with an average PE Ratio of 13.1, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2024.

The Junior Market ended trading with an average PE Ratio of 13.1, based on last traded prices in conjunction with earnings projected by ICInsider.com for the financial years ending around August 2024. Fosrich popped 7 cents to $2.25 and closed with an exchange of 12,450 shares, ISP Finance increased 13 cents and ended at $25 after 3,877 stocks changed hands, Jamaican Teas dropped 17 cents to close $2.32, with 298,178 shares changing hands. Lasco Financial gained 18 cents to end at $2.10 after investors ended trading 78,250 units, Limners and Bards advanced 11 cents to $1.66 after an exchange of 42,289 stocks, Main Event rose 67 cents to close at $14.97, with 7,944 stock units clearing the market. Spur Tree Spices advanced 12 cents and ended at $2.47 in an exchange of 11,408 shares and Stationery and Office Supplies popped 8 cents in closing at $1.69 after 241,682 stocks passed through the market.

Fosrich popped 7 cents to $2.25 and closed with an exchange of 12,450 shares, ISP Finance increased 13 cents and ended at $25 after 3,877 stocks changed hands, Jamaican Teas dropped 17 cents to close $2.32, with 298,178 shares changing hands. Lasco Financial gained 18 cents to end at $2.10 after investors ended trading 78,250 units, Limners and Bards advanced 11 cents to $1.66 after an exchange of 42,289 stocks, Main Event rose 67 cents to close at $14.97, with 7,944 stock units clearing the market. Spur Tree Spices advanced 12 cents and ended at $2.47 in an exchange of 11,408 shares and Stationery and Office Supplies popped 8 cents in closing at $1.69 after 241,682 stocks passed through the market.