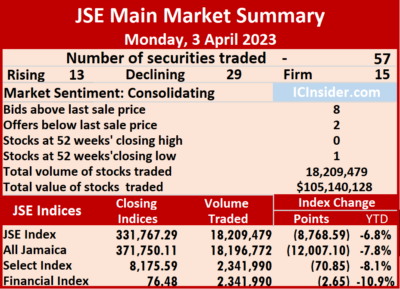

Trading plunged to start the second quarter on a negative note following a big surge in the market index last week, with the All Jamaican Composite Index plunging 12,007.10 points to 371,750.11 and the JSE Main Index dived 8,768.59 points to 331,767.29 at the close of the Jamaica Stock Exchange Main Market on Monday.

At the close of trading, after a 26 percent fall in the volume of stocks traded with an 82 percent lower value than on Friday, resulting from trading in 57 securities compared to 60 on Friday, with 13 rising, 29 declining and 15 ending unchanged and ended with the JSE Financial Index losing 2.65 points to close at 76.48.

At the close of trading, after a 26 percent fall in the volume of stocks traded with an 82 percent lower value than on Friday, resulting from trading in 57 securities compared to 60 on Friday, with 13 rising, 29 declining and 15 ending unchanged and ended with the JSE Financial Index losing 2.65 points to close at 76.48.

A total of 18,209,479 shares were traded for $105,140,128, down from 24,564,536 units at $579,763,758 on Friday.

Trading averaged 319,465 shares at $1,844,564, compared with 409,409 shares at $9,662,729 on Friday, compared to trading in March, with an average of 356,137 units at $3,015,416.

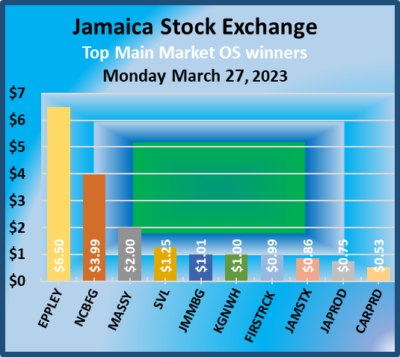

Transjamaican Highway led trading with 6.88 million shares for 37.8 percent of total volume, followed by QWI Investments with 4.42 million units for 24.3 percent of the day’s trade, Wigton Windfarm with 1.83 million units for 10.1 percent market share, Sagicor Select Financial Fund with 1.19 million units for 6.5 percent market share and Supreme Ventures with 1.09 million units for 6 percent market share.

The PE Ratio, a formula used to compute appropriate stock values, averages 13.8 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

The PE Ratio, a formula used to compute appropriate stock values, averages 13.8 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows eight stocks ended with bids higher than their last selling prices and two with lower offers.

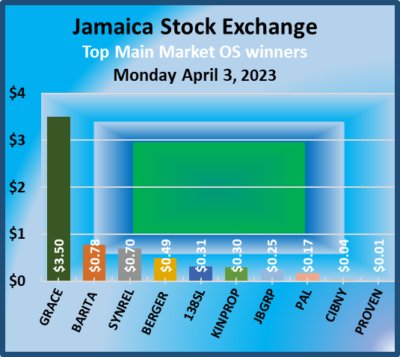

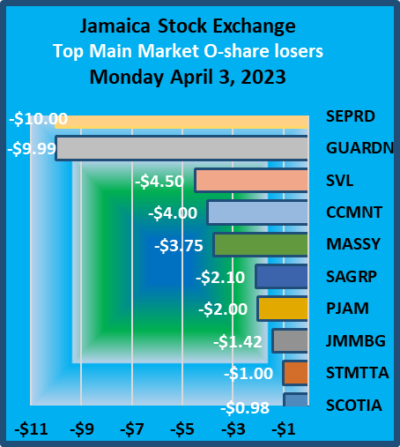

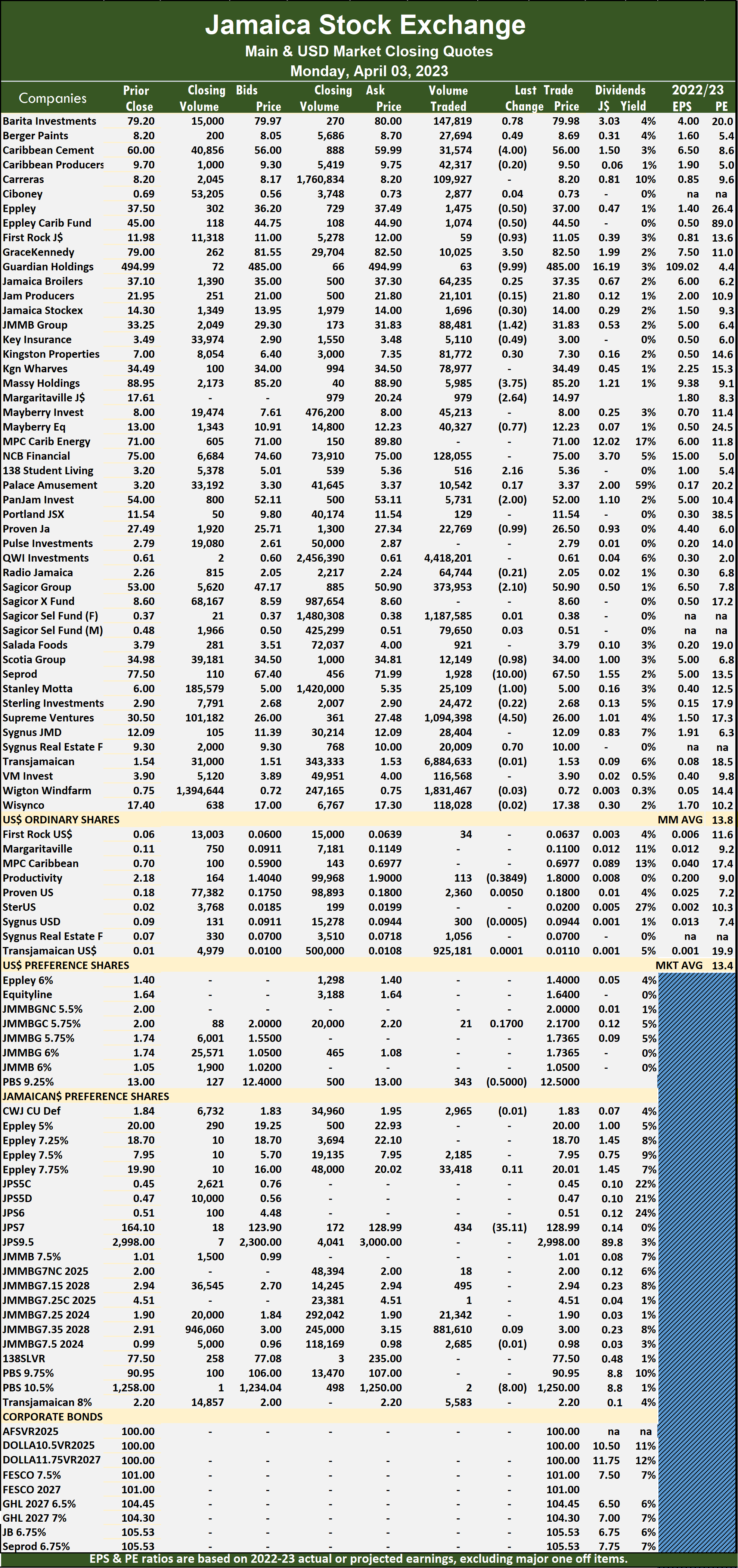

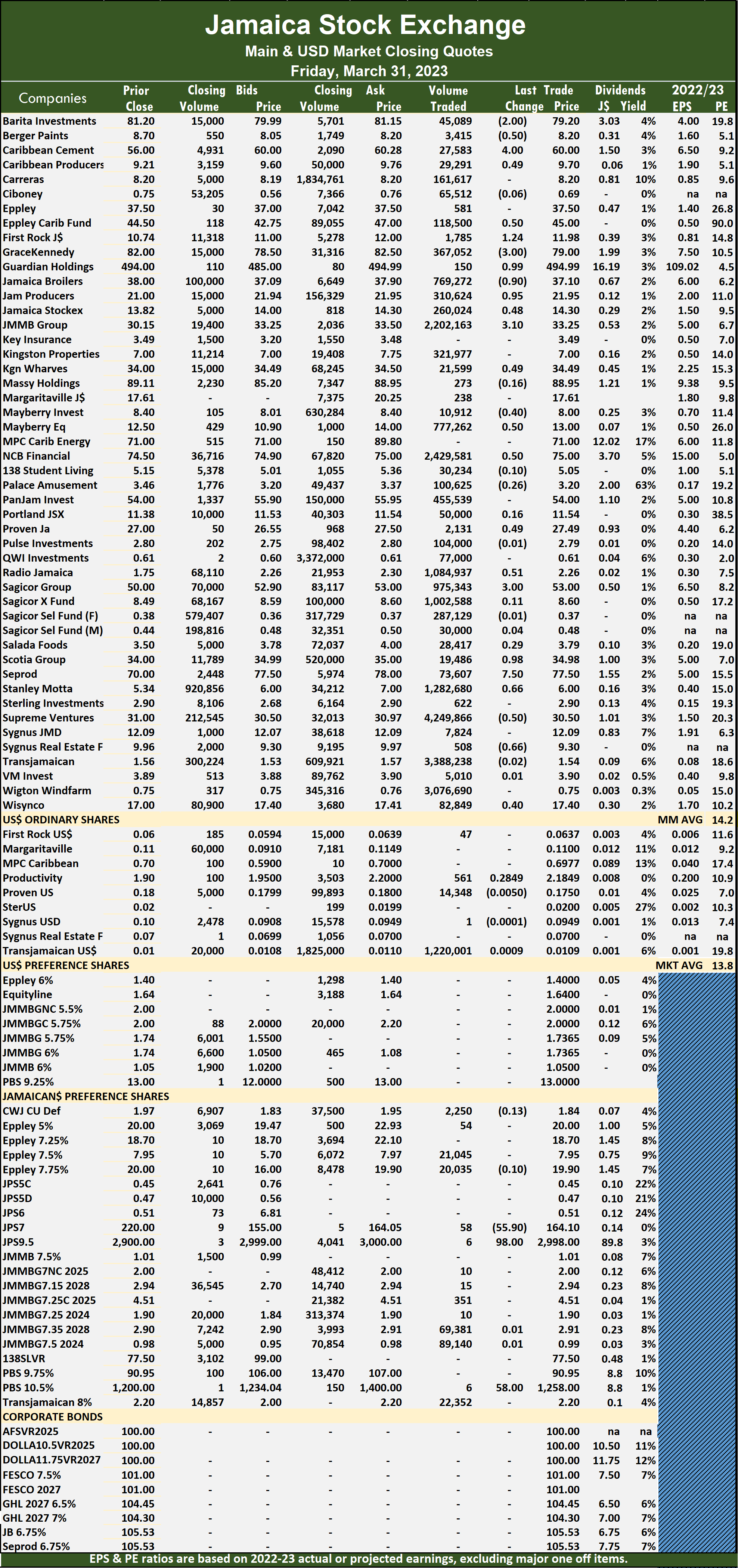

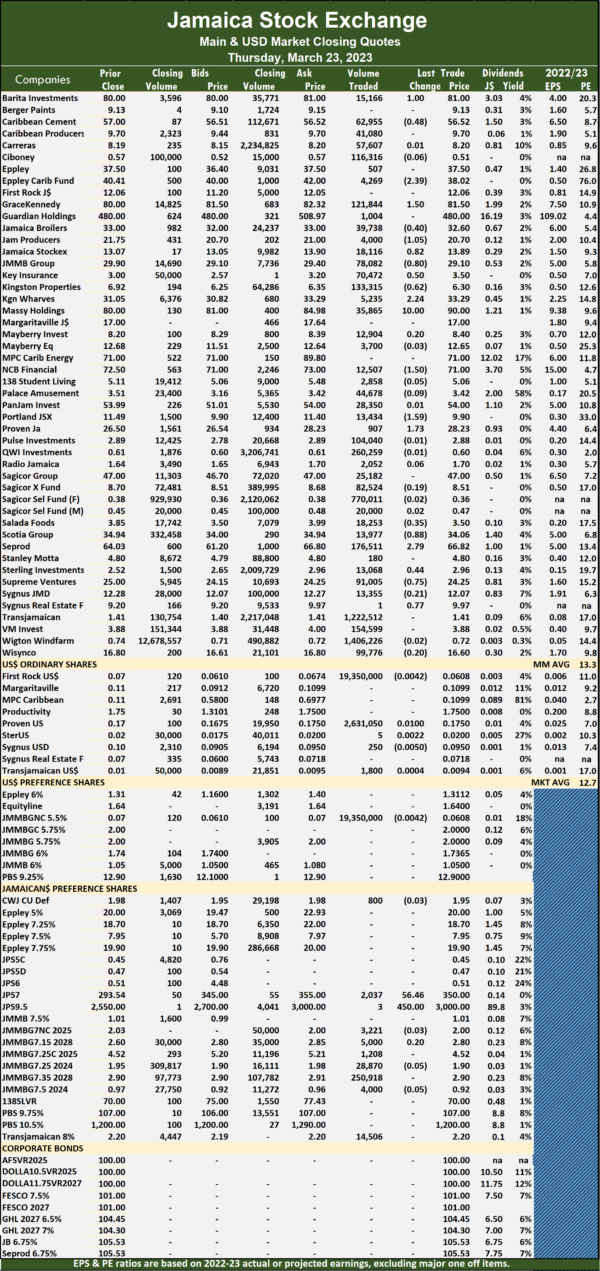

At the close, Barita Investments climbed 78 cents to close at $79.98 after an exchange of 147,819 shares, Berger Paints rallied 49 cents to end at $8.69 with a transfer of 27,694 stocks, but only after hitting an intraday 52 weeks’ low of $7.50, Caribbean Cement dropped $4 after finishing at $56 in an exchange of 31,574 stock units. Eppley shed 50 cents in closing at $37 after an exchange of 1,475 units, Eppley Caribbean Property Fund fell 50 cents to $44.50 with 1,074 stocks crossing the market, First Rock Real Estate dipped 93 cents after ending at $11.05 and closed with 59 units being traded. GraceKennedy popped $3.50 to close at $82.50 in switching ownership of 10,025 stock units, Guardian Holdings lost $9.99 to end at $485 after exchanging 63 shares, JMMB Group declined $1.42 in closing at $31.83, with 88,481 units crossing the market.  Key Insurance shed 49 cents to end at $3 in trading 5,110 stocks, Margaritaville lost $2.64 to close at a 52 weeks’ low of $14.97 with 979 shares clearing the market, Massy Holdings dropped $3.75 to end at $85.20 after a transfer of 5,985 stock units. Mayberry Jamaican Equities fell 77 cents in closing at $12.23 while exchanging 40,327 stocks, Pan Jamaica Group, with an expanded portfolio of companies following the acquisition of companies that were part of Jamaica Producers, declined $2 to $52 with an exchange of 5,731 units, Proven Investments dipped 99 cents after ending at $26.50 with investors transferring 22,769 stock units. Sagicor Group dropped $2.10 in closing at $50.90, with 373,953 shares crossing the market, Scotia Group declined 98 cents to close at $34 in trading 12,149 stocks, Seprod dipped $10 to $67.50 as investors exchanged 1,928 units. Stanley Motta lost $1 after ending at $5 after 25,109 stock units passed through the market, Supreme Ventures shed $4.50 to end at $26 with the swapping of 1,094,398 shares and Sygnus Real Estate Finance gained 70 cents to close at $10, with 20,009 stocks changing hands.

Key Insurance shed 49 cents to end at $3 in trading 5,110 stocks, Margaritaville lost $2.64 to close at a 52 weeks’ low of $14.97 with 979 shares clearing the market, Massy Holdings dropped $3.75 to end at $85.20 after a transfer of 5,985 stock units. Mayberry Jamaican Equities fell 77 cents in closing at $12.23 while exchanging 40,327 stocks, Pan Jamaica Group, with an expanded portfolio of companies following the acquisition of companies that were part of Jamaica Producers, declined $2 to $52 with an exchange of 5,731 units, Proven Investments dipped 99 cents after ending at $26.50 with investors transferring 22,769 stock units. Sagicor Group dropped $2.10 in closing at $50.90, with 373,953 shares crossing the market, Scotia Group declined 98 cents to close at $34 in trading 12,149 stocks, Seprod dipped $10 to $67.50 as investors exchanged 1,928 units. Stanley Motta lost $1 after ending at $5 after 25,109 stock units passed through the market, Supreme Ventures shed $4.50 to end at $26 with the swapping of 1,094,398 shares and Sygnus Real Estate Finance gained 70 cents to close at $10, with 20,009 stocks changing hands.

In the preference segment, Productive Business 10.50% preference share fell $8 to end at $1250 in an exchange of two stock units and Jamaica Public Service 7% shed $35.11 to $128.99 with a transfer of 434 shares.

In the preference segment, Productive Business 10.50% preference share fell $8 to end at $1250 in an exchange of two stock units and Jamaica Public Service 7% shed $35.11 to $128.99 with a transfer of 434 shares.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

ICTOP10 rides big weekly JSE rally

The JSE Main market surged sharply in the past week.

While the Main and Junior Markets rebounded sharply during last week, ICTOP10 stocks ended with varying movements, with gains and losses in both markets hitting 16 percent. It was an interesting week in which the main market gained over 18,000 points for the week with all days closing with gains including the Friday of the previous week, but it sits at a resistance level and is a signal worth watching.

The Junior Market put on 200 points since Thursday, March 23 and had one minor negative trading day during the period, however, the last day accounted for nearly half of the above gains.

While Bank of Jamaica held their overnight rates at 7 percent, their CD rate that fell 16 percent in the previous week to an average of 8.85 percent from over 10 percent where it stood for several months, BOJ offered a huge $35 billion this past week, but the average rate fell to 8.49 percent after $70 billion chased the amount offered. Importantly, the central bank cut the stock of CDS it holds from a peak of $109.5 billion on March 3, but at the latest auction, it amounted to $88.85 billion, marginally up from $82 billion on the 17th.

At the end of the past week, in the Junior Market TOP10 four stocks gained and five declined. KLE Group jumped 16 percent to $1.69 and Tropical Battery rose 7 percent to close at $2.08. General Accident dropped 16 percent to $5 and Everything Fresh fell 6 percent to close at $1.45.

At the end of the past week, in the Junior Market TOP10 four stocks gained and five declined. KLE Group jumped 16 percent to $1.69 and Tropical Battery rose 7 percent to close at $2.08. General Accident dropped 16 percent to $5 and Everything Fresh fell 6 percent to close at $1.45.

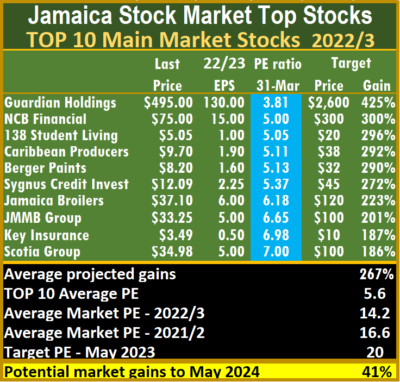

The Main Market TOP10 JMMB Group climbed 15 percent to $33.25, Jamaica Broilers gained 12 percent to $37.10, Caribbean Producers popped 7 percent to $9.70 and NCB Financial with a rise of 6 percent to $75. Berger Paints fell 10 percent to $8.20 and 138 Student Living with a fall of 6 percent to $5.05.

The Junior Market has a long term pattern, with the market starting to rise around a month before quarterly results are due and declining shortly after results are released. This is a pattern worth noting that can be built into investment decisions that can improve returns.

At the end of the week, the average PE for the JSE Main Market TOP 10 is 5.6, well below the market average of 14.2, while the Junior Market Top 10 PE sits at 5.8 compared with the market at 11.4. The differences are important indicators of the level of likely gains for ICTOP10 stocks. The Junior Market is projected to rise by 248 percent and the Main MarketTOP10 by an average of 267 percent, by May 2024, based on 2023 forecasted earnings.

The Junior Market has 11 stocks representing 23 percent of the market, with PEs from 15 to 28, averaging 20.4, well above the average of the market. The top half of the market has an average PE of 16, suggesting that this may be a logical value for junior market stocks currently.

The Main Market 19 highest valued stocks are priced at a PE of 15 to 115, with an average of 29 and 21 excluding the most valued stocks and 20.5 for the top half excluding the stocks with the highest valuation.

The Main Market 19 highest valued stocks are priced at a PE of 15 to 115, with an average of 29 and 21 excluding the most valued stocks and 20.5 for the top half excluding the stocks with the highest valuation.

The above average shows the extent of potential gains for the TOP 10 stocks.

ICTOP10 focuses on likely yearly winners, accordingly, the list includes some of the best companies in the market but not always. ICInsider.com ranks stocks based on projected earnings, allowing investors to focus on the most undervalued stocks and helping to remove emotions in selecting stocks for investments that often result in costly mistakes.

IC TOP10 stocks are likely to deliver the best returns up to the end of May 2023 and are ranked in order of potential gains, computed using projected earnings for the current fiscal year. Expected values will change as stock prices fluctuate and result in weekly movements in and out of the lists. Revisions to earnings are ongoing, based on receipt of new information.

Persons who compiled this report may have an interest in securities commented on in this report.

Another big Main Market rally

Stocks surged sharply for a second day on the Main Market of the Jamaica Stock Exchange following Thursday’s big rally to close out the month slightly higher than the close of February, with the volume of stocks traded rising 83 percent and the value being 450 percent more than on Thursday, following trading in 60 securities similar to Thursday, with prices of 27 rising, 17 declining and 16 ending unchanged.

A total of 24,564,536 shares were traded for $579,763,758, compared with 13,390,755 units at $105,351,603 on Thursday.

A total of 24,564,536 shares were traded for $579,763,758, compared with 13,390,755 units at $105,351,603 on Thursday.

Trading averaged 409,409 shares at $9,662,729 versus 223,179 stocks at $1,756,840 on Thursday and month to date, an average of 356,137 units at $3,015,416, compared with 353,545 shares at $2,691,932 on the previous day. February closed with an average of 183,599 units at $2,160,070.

Supreme Ventures led trading with 4.25 million shares for 17.3 percent of total volume, Transjamaican Highway followed, with 3.39 million units for 13.8 percent of the day’s trade, Wigton Windfarm ended with 3.08 million units for 12.5 percent take of the trades, CB Financial with 2.43 million units for 9.9 percent the market, JMMB Group with 2.20 million units for 9 percent of the total of the market and Stanley Motta, 1.28 million units for 5.2 percent market share.

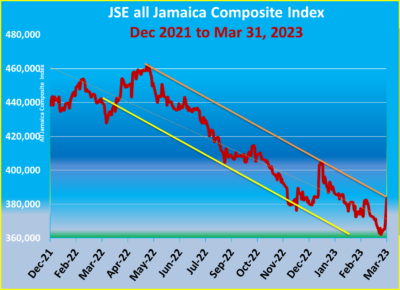

The All Jamaican Composite Index surged 6,292.04 points to 383,757.21, the JSE Main Index ballooned 5,465.11 points to close at 340,535.88 and the JSE Financial Index popped 1.53 points to 79.13. The market now sits at a resistance point within a downward sloping channel and would require a few more days of bid break out for a return of a sustained move higher.

The PE Ratio, a formula used to compute appropriate stock values, averages 14.2 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

The PE Ratio, a formula used to compute appropriate stock values, averages 14.2 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows 11 stocks ended with bids higher than their last selling prices and three with lower offers.

At the close, Barita Investments lost $2 to end at $79.20 after trading 45,089 shares, Berger Paints dipped 50 cents to close at $8.20 after a transfer of 3,415 stocks, Caribbean Cement rallied $4 to end at $60, with 27,583 units changing hands. Caribbean Producers advanced 49 cents to $9.70 in trading 29,291 stock units, Eppley Caribbean Property Fund increased 50 cents in closing at $45 with a transfer of 118,500 stocks, First Rock Real Estate gained $1.24 to close at $11.98 as investors exchanged 1,785 shares. GraceKennedy declined $3 in closing at $79 after an exchange of 367,052 stock units, Guardian Holdings rose 99 cents in ending at $494.99 while exchanging 150 units, Jamaica Broilers fell 90 cents to end at $37.10, with 769,272 stock units crossing the market. Jamaica Producers climbed 95 cents to $21.95 in switching ownership of 310,624 shares, Jamaica Stock Exchange popped 48 cents to close at $14.30 with investors transferring 260,024 units, JMMB Group climbed $3.10 to $33.25 with an exchange of 2,202,163 stocks.  Kingston Wharves advanced 49 cents to $34.49, with 21,599 units crossing the market, Mayberry Investments shed 40 cents to end at $8 in an exchange of 10,912 stocks, Mayberry Jamaican Equities rose 50 cents to $13, with investors exchanging 777,262 stock units. NCB Financial rallied 50 cents to $75, with 2,429,581 shares crossing the exchange, Proven Investments popped 49 cents to end at $27.49 in an exchange of 2,131 stock units, Radio Jamaica rallied 51 cents to close at $2.26 as investors exchanged 1,084,937 stocks. Sagicor Group gained $3 to $53 with 975,343 shares clearing the market, Scotia Group increased 98 cents after ending at $34.98 with the swapping of 19,486 units, Seprod advanced $7.50 to $77.50 while 73,607 stock units passed through the market. Stanley Motta popped 66 cents to end at $6 with a transfer of 1,282,680 units, Supreme Ventures dropped 50 cents to close at $30.50 after an exchange of 4,249,866 shares, Sygnus Real Estate Finance dropped 66 cents to $9.30 with 508 stocks changing hands and Wisynco Group rose 40 cents after ending at $17.40 and 82,849 shares crossed through the market.

Kingston Wharves advanced 49 cents to $34.49, with 21,599 units crossing the market, Mayberry Investments shed 40 cents to end at $8 in an exchange of 10,912 stocks, Mayberry Jamaican Equities rose 50 cents to $13, with investors exchanging 777,262 stock units. NCB Financial rallied 50 cents to $75, with 2,429,581 shares crossing the exchange, Proven Investments popped 49 cents to end at $27.49 in an exchange of 2,131 stock units, Radio Jamaica rallied 51 cents to close at $2.26 as investors exchanged 1,084,937 stocks. Sagicor Group gained $3 to $53 with 975,343 shares clearing the market, Scotia Group increased 98 cents after ending at $34.98 with the swapping of 19,486 units, Seprod advanced $7.50 to $77.50 while 73,607 stock units passed through the market. Stanley Motta popped 66 cents to end at $6 with a transfer of 1,282,680 units, Supreme Ventures dropped 50 cents to close at $30.50 after an exchange of 4,249,866 shares, Sygnus Real Estate Finance dropped 66 cents to $9.30 with 508 stocks changing hands and Wisynco Group rose 40 cents after ending at $17.40 and 82,849 shares crossed through the market.

In the preference segment, Productive Business 10.50% preference share rallied $58 to end at $1258 in an exchange of 6 units, Jamaica Public Service 7% fell $55.90 in closing at $164.10, with 58 stocks clearing the market and Jamaica Public Service 9.5% gained $98 after ending at $2998 as investors exchanged 6 stock units.

In the preference segment, Productive Business 10.50% preference share rallied $58 to end at $1258 in an exchange of 6 units, Jamaica Public Service 7% fell $55.90 in closing at $164.10, with 58 stocks clearing the market and Jamaica Public Service 9.5% gained $98 after ending at $2998 as investors exchanged 6 stock units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Huge Main Market bounce as winners crush losers

Investors shifted gears and pushed stocks solidly higher on the penultimate day of the 2023 first quarter at the close of the Jamaica Stock Exchange Main Market on Thursday, with a 78 percent fall in the volume of stocks traded, after a 64 percent fall in value than on Wednesday, following trading in 60 securities compared to 56 on Wednesday, with prices of 30 rising, 13 declining and 17 ending unchanged.

A total of 13,390,755 shares were traded for $105,410,403 compared to 60,107,710 units at $290,707,932 on Wednesday.

A total of 13,390,755 shares were traded for $105,410,403 compared to 60,107,710 units at $290,707,932 on Wednesday.

Trading averaged 223,179 shares at $1,756,840 versus 1,073,352 shares at $5,191,213 on Wednesday and month to date, an average of 353,545 units at $2,691,945, compared with 360,213 units at $2,739,777 on the previous day. February closed with an average of 183,599 units at $2,160,070.

Transjamaican Highway led trading with 5.86 million shares for 43.8 percent of total volume followed by Wigton Windfarm with 1.92 million units for 14.3 percent of the day’s trade, Supreme Ventures with 1.15 million units for 8.6 percent share of the day’s trading and Sagicor Select Financial Fund with 1.01 million units for 7.6 percent market share.

The market indices surged, with the All Jamaican Composite Index popping 8,472.58 points to 377,465.17, the JSE Main Index climbing 8,348.24 points to 335,070.77 and the JSE Financial Index rallying 1.45 points to close at 77.60.

The PE Ratio, a formula used to compute appropriate stock values, averages 13.6 for the Main Market. The JSE Main and USD Market PE ratios incorporate ICInsider.com’s earnings forecasts for companies with the financial year ending between November 2022 and August 2023.

The PE Ratio, a formula used to compute appropriate stock values, averages 13.6 for the Main Market. The JSE Main and USD Market PE ratios incorporate ICInsider.com’s earnings forecasts for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows 10 stocks ended with bids higher than their last selling prices and six with lower offers.

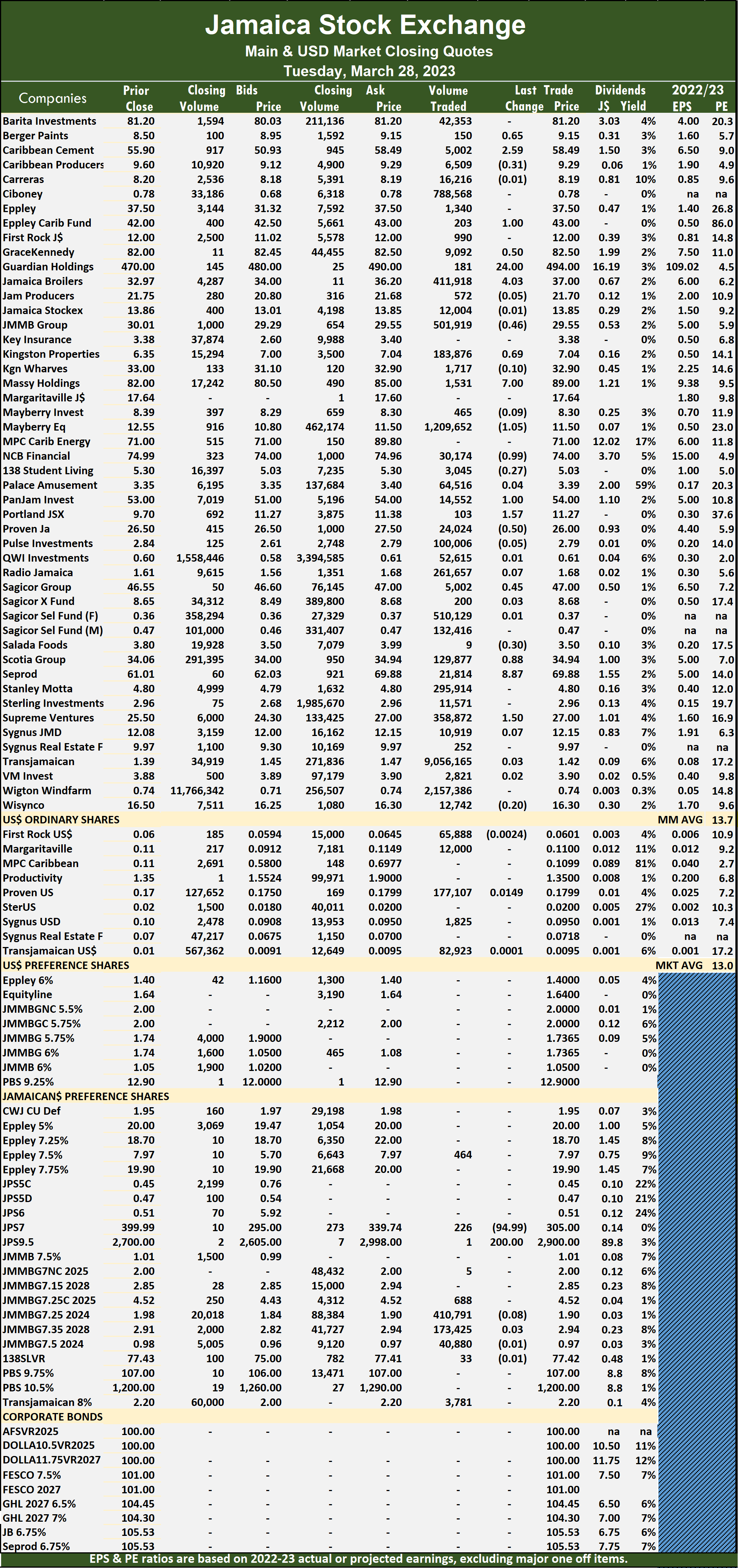

At the close, Barita Investments rose $1.17 to end at $81.20 with investors transferring 45,746 shares, Caribbean Cement climbed $5 to $56 as investors exchanged 15,391 units, Eppley Caribbean Property Fund increased $1.50 to close at $44.50 after a transfer of 4,453 stock units. First Rock Real Estate dipped $1.25 in closing at $10.74 after an exchange of 7,125 stocks, GraceKennedy climbed $2 to $82 with the swapping of 33,004 stock units, Guardian Holdings rallied $4 to $494, with 76 units clearing the market. Jamaica Broilers popped $1 after ending at $38 after an exchange of 453,507 stocks, Jamaica Producers lost 74 cents to close at $21 in switching ownership of 7,618 shares,  Kingston Wharves advanced $1.10 in closing at $34 with an exchange of 22,177 stock units. Massy Holdings increased $8.11 to end at $89.11 in trading 1,002 stocks, NCB Financial shed 48 cents to $74.50, with 10,681 units crossing the market, Proven Investments gained 50 cents to end at $27 and closed with 3,803 shares changing hands. Sagicor Group advanced $3 after ending at $50 in trading 109,283 stocks, Scotia Group dropped 94 cents in closing at $34, with 124,974 shares changing hands, Seprod popped $3 to close at $70 while exchanging 24,463 units. Supreme Ventures rose $3.18 to end at $31 as 1,148,754 stock units passed through the market and Sygnus Real Estate Finance climbed 66 cents in closing at $9.96 in an exchange of 465 stocks.

Kingston Wharves advanced $1.10 in closing at $34 with an exchange of 22,177 stock units. Massy Holdings increased $8.11 to end at $89.11 in trading 1,002 stocks, NCB Financial shed 48 cents to $74.50, with 10,681 units crossing the market, Proven Investments gained 50 cents to end at $27 and closed with 3,803 shares changing hands. Sagicor Group advanced $3 after ending at $50 in trading 109,283 stocks, Scotia Group dropped 94 cents in closing at $34, with 124,974 shares changing hands, Seprod popped $3 to close at $70 while exchanging 24,463 units. Supreme Ventures rose $3.18 to end at $31 as 1,148,754 stock units passed through the market and Sygnus Real Estate Finance climbed 66 cents in closing at $9.96 in an exchange of 465 stocks.

In the preference segment, Jamaica Public Service 7% fell $43.39 in ending at $220, with 26 shares crossing the market, Jamaica Public Service 9.5% declined $98 to $2900 with a transfer of 2 stock units and Productive Business Solutions 9.75% preference share dropped $16.05 to close at $90.95 in an exchange of 62 units.

In the preference segment, Jamaica Public Service 7% fell $43.39 in ending at $220, with 26 shares crossing the market, Jamaica Public Service 9.5% declined $98 to $2900 with a transfer of 2 stock units and Productive Business Solutions 9.75% preference share dropped $16.05 to close at $90.95 in an exchange of 62 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Trading climbs on JSE Main Market

Trading activity on the Jamaica Stock Exchange Main Market ended on Wednesday with a 252 percent jump in the volume of stocks traded, valued at 233 percent more than on Tuesday, with 56 securities trading compared to 55 on Tuesday, with 18 rising, 24 declining and 14 ending unchanged.

A total of 60,107,710 shares were traded for $290,707,932, up from 17,081,333 units at $87,212,275 on Tuesday.

A total of 60,107,710 shares were traded for $290,707,932, up from 17,081,333 units at $87,212,275 on Tuesday.

Trading averaged 1,073,352 shares at $5,191,213 compared with 310,570 shares at $1,585,678 on Tuesday and month to date, an average of 360,213 units at $2,739,813, compared with 324,461 units at $2,616,913 on the previous day. February closed with an average of 183,599 units at $2,160,070.

Key Insurance led trading with 44.75 million shares for 74.5 percent of total volume, followed by Transjamaican Highway with 7.36 million units for 12.2 percent of the day’s trade, Wigton Windfarm with 2.69 million units for 4.5 percent market share and Supreme Ventures with 1.19 million units for 2 percent of stocks traded.

The All Jamaican Composite Index surged 3,756.40 points to 368,992.59, the JSE Main Index popped 976.04 points to finish at 326,722.53 and the JSE Financial Index rallied 0.68 points to 76.15.

The All Jamaican Composite Index surged 3,756.40 points to 368,992.59, the JSE Main Index popped 976.04 points to finish at 326,722.53 and the JSE Financial Index rallied 0.68 points to 76.15.

The PE Ratio, a formula used to compute appropriate stock values, averages 13.7 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows seven stocks ended with bids higher than their last selling prices and four with lower offers.

At the close, Barita Investments lost $1.17 to end at $80.03 in switching ownership of 10,847 shares, Berger Paints shed 65 cents in closing at $8.50, with 1,081 stock units crossing the exchange, Caribbean Cement fell $7.49 to $51 after trading 9,596 stocks.  GraceKennedy dipped $2.50 in ending at $80 as 270,948 units passed through the market, Guardian Holdings dropped $4 to close at $490 in an exchange of 25 units, JMMB Group gained 45 cents to close at $30 after trading 88,644 shares. Massy Holdings declined $8 to end at $81 after trading 500,481 stock units, Mayberry Jamaican Equities increased $1 in closing at $12.50 with the swapping of 7,309 stocks, NCB Financial popped 98 cents to close at $74.98 after exchanging 11,726 stock units. Proven Investments rallied 50 cents after ending at $26.50 with investors transferring 1,144 stocks, Seprod shed $2.88 after finishing at $67 with a transfer of 21,165 shares, Stanley Motta rose 54 cents to $5.34, with 190,246 units changing hands. Supreme Ventures advanced 82 cents to end at $27.82, with 1,194,866 stocks crossing the market,

GraceKennedy dipped $2.50 in ending at $80 as 270,948 units passed through the market, Guardian Holdings dropped $4 to close at $490 in an exchange of 25 units, JMMB Group gained 45 cents to close at $30 after trading 88,644 shares. Massy Holdings declined $8 to end at $81 after trading 500,481 stock units, Mayberry Jamaican Equities increased $1 in closing at $12.50 with the swapping of 7,309 stocks, NCB Financial popped 98 cents to close at $74.98 after exchanging 11,726 stock units. Proven Investments rallied 50 cents after ending at $26.50 with investors transferring 1,144 stocks, Seprod shed $2.88 after finishing at $67 with a transfer of 21,165 shares, Stanley Motta rose 54 cents to $5.34, with 190,246 units changing hands. Supreme Ventures advanced 82 cents to end at $27.82, with 1,194,866 stocks crossing the market,  Sygnus Real Estate Finance declined 67 cents to close at $9.30, with 1,600 stock units clearing the market and Wisynco Group climbed 40 cents to $16.70 while exchanging 206,419 shares.

Sygnus Real Estate Finance declined 67 cents to close at $9.30, with 1,600 stock units clearing the market and Wisynco Group climbed 40 cents to $16.70 while exchanging 206,419 shares.

In the preference segment, Jamaica Public Service 7% dropped $41.61 to end at $263.39 and closed with 649 units changing hands and Jamaica Public Service 9.5% rallied $98 to close at $2998 as investors exchanged just one stock.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Winning Main Market stocks beat out losers

Rising stocks had the upper hand over decliners in trading on the Jamaica Stock Exchange Main Market on Tuesday, following an 80 percent decline in the volume of stocks traded valued 49 percent less than Monday, following trading in 55 securities down from 59 on Monday, with 24 rising, 18 declining and 13 ending unchanged.

A total of 17,081,333 shares were exchanged for $87,212,275 versus 83,621,528 units at $169,448,467 on Monday.

A total of 17,081,333 shares were exchanged for $87,212,275 versus 83,621,528 units at $169,448,467 on Monday.

Trading on Tuesday averaged 310,570 shares at $1,585,678 compared to 1,417,314 shares at $2,872,008 on Monday and month to date, an average of 324,461 units at $2,616,876, compared with 325,180 units at $2,670,281 on the previous day. In contrast, February closed with an average of 183,599 units at $2,160,070.

Transjamaican Highway led trading with 9.06 million shares for 53 percent of total volume followed by Wigton Windfarm with 2.16 million units for 12.6 percent of the day’s trade and Mayberry Jamaican Equities with 1.21 million units for 7.1 percent of market share.

The All Jamaican Composite Index popped 40.23 points to 365,236.19, the JSE Main Index rallied 2,546.17 points to 325,746.49 and the JSE Financial Index popped 0.16 points to close at 75.47.

The PE Ratio, a formula to ascertain appropriate stock values, averages 13.7 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasts by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

The PE Ratio, a formula to ascertain appropriate stock values, averages 13.7 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasts by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows seven stocks ended with bids higher than their last selling prices and six with lower offers.

At the close, Berger Paints rallied 65 cents to $9.15 after a transfer of 150 shares, Caribbean Cement rallied $2.59 to $58.49 with the swapping of 5,002 stock units, Eppley Caribbean Property Fund gained $1 to close at $43 after exchanging 203 stocks. GraceKennedy climbed 50 cents to end at $82.50 after 9,092 units passed through the market, Guardian Holdings advanced $24 to $494 after an exchange of 181 shares, Jamaica Broilers popped $4.03 after ending at $37 with investors transferring 411,918 stocks. JMMB Group dipped 46 cents to close at $29.55 as investors exchanged 501,919 stock units, Kingston Properties rose 69 cents to $7.04 in an exchange of 183,876 units, Massy Holdings gained $7 in closing at $89 in trading 1,531 stock units.  Mayberry Jamaican Equities lost $1.05 to end at $11.50 with 1,209,652 shares crossing the exchange, NCB Financial shed 99 cents in closing at $74, with 30,174 stocks changing hands, PanJam Investment climbed $1 to end at $54 after 14,552 units passed through the market. Portland JSX increased $1.57 after ending at $11.27 with 103 units changing hands, Proven Investments lost 50 cents to $26 in an exchange of 24,024 stock units, Sagicor Group rallied 45 cents to close at $47 in trading 5,002 shares. Scotia Group popped 88 cents to $34.94 with 129,877 stocks clearing the market, Seprod rose $8.87 to end at $69.88 while exchanging 21,814 stock units and Supreme Ventures advanced $1.50 to close at $27 in trading 358,872 stocks.

Mayberry Jamaican Equities lost $1.05 to end at $11.50 with 1,209,652 shares crossing the exchange, NCB Financial shed 99 cents in closing at $74, with 30,174 stocks changing hands, PanJam Investment climbed $1 to end at $54 after 14,552 units passed through the market. Portland JSX increased $1.57 after ending at $11.27 with 103 units changing hands, Proven Investments lost 50 cents to $26 in an exchange of 24,024 stock units, Sagicor Group rallied 45 cents to close at $47 in trading 5,002 shares. Scotia Group popped 88 cents to $34.94 with 129,877 stocks clearing the market, Seprod rose $8.87 to end at $69.88 while exchanging 21,814 stock units and Supreme Ventures advanced $1.50 to close at $27 in trading 358,872 stocks.

In the preference segment, Jamaica Public Service 7% declined by $94.99 after ending at $305 in switching ownership of 226 shares and Jamaica Public Service 9.5% increased by $200 in closing at $2,900 with an exchange of one unit.

In the preference segment, Jamaica Public Service 7% declined by $94.99 after ending at $305 in switching ownership of 226 shares and Jamaica Public Service 9.5% increased by $200 in closing at $2,900 with an exchange of one unit.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

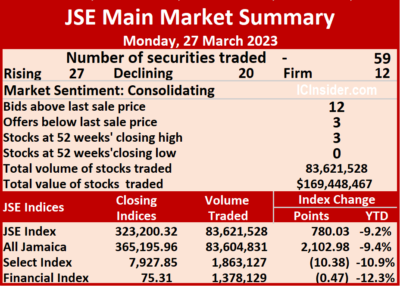

Trading gains for JSE Main Market

Trading volume surged 765 percent after 157 percent more money entered the Jamaica Stock Exchange Main Market on Monday compared to Friday and resulted in 59 securities trading, up from 55 on Friday, with 27 rising, 20 declining and 12 ending unchanged.

A total of 83,621,528 shares were exchanged for $169,448,467 versus 9,662,580 units at $65,850,660 on Friday.

A total of 83,621,528 shares were exchanged for $169,448,467 versus 9,662,580 units at $65,850,660 on Friday.

Trading averaged 1,417,314 shares at $2,872,008 versus 175,683 units at $1,197,285 on Friday and month to date, an average of 325,180 units at $2,670,281, up from 260,937 units at $2,658,456 on the prior day. February averaged 183,599 units at $2,160,070.

Transjamaican Highway led trading with 75.63 million shares for 90.4 percent of total volume followed by Wigton Windfarm with 2.86 million units for 3.4 percent of the day’s trade and Sagicor Real Estate Fund with 905,709 units for 1.1 percent market share.

The All Jamaican Composite Index increased 2,102.98 points to 365,195.96, the JSE Main Index advanced 780.03 points to 323,200.32 and the JSE Financial Index fell 0.47 points to end at 75.31.

The PE Ratio, a formula used to ascertain appropriate stock values, averages 13.4 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

The PE Ratio, a formula used to ascertain appropriate stock values, averages 13.4 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows 12 stocks ended with bids higher than their last selling prices and three with lower offers.

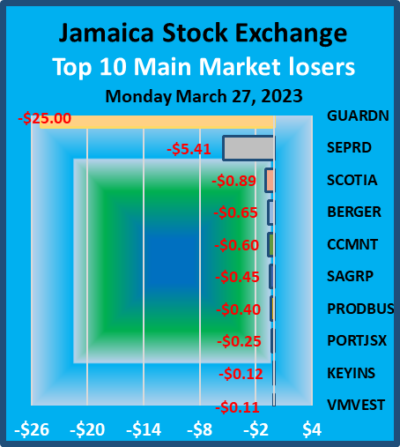

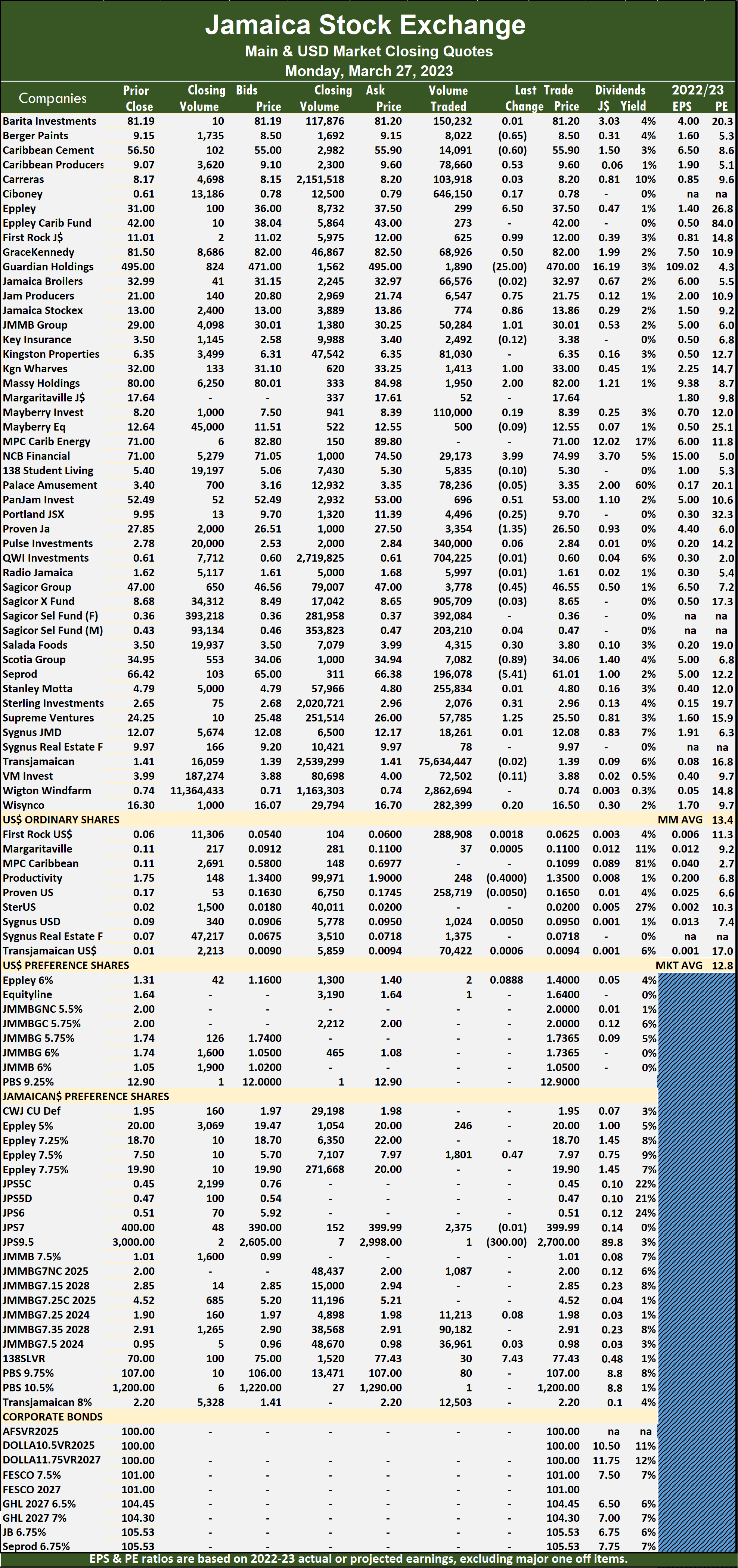

At the close, Berger Paints fell 65 cents to $8.50 after trading 8,022 shares, Caribbean Cement dipped 60 cents in closing at a 52 weeks’ low of $55.90, with 14,091 units passing through the market, Caribbean Producers rose 53 cents to close at $9.60 after a transfer of 78,660 stock units. Eppley climbed $6.50 after ending at $37.50 as investors exchanged 299 stocks, First Rock Real Estate rallied 99 cents to end at $12 with a transfer of 625 units, GraceKennedy popped 50 cents after ending at $82, with 68,926 stock units changing hands.  Guardian Holdings dropped $25 to close at a 52 weeks’ low of $470 with 1,890 stocks clearing the market, Jamaica Producers gained 75 cents to end at $21.75 after an exchange of 6,547 shares, Jamaica Stock Exchange rallied 86 cents to $13.86, with 774 stock units crossing the exchange. JMMB Group advanced $1.01 in closing at $30.01 after 50,284 stocks changed hands, Kingston Wharves gained $1 after ending at $33, with 1,413 units crossing the market, Massy Holdings climbed $2 to end at $82 after an exchange of 1,950 shares. NCB Financial rose $3.99 to close at $74.99, with 29,173 stocks crossing the market, PanJam Investment rallied 51 cents to $53 in an exchange of 696 units, Proven Investments lost $1.35 in closing at $26.50 with the swapping of 3,354 shares. Sagicor Group declined 45 cents to $46.55 with investors transferring 3,778 stock units, Scotia Group shed 89 cents to end at $34.06 in an exchange of 7,082 stocks, Seprod declined $5.41 after ending at $61.01 while exchanging 196,078 shares and Supreme Ventures advanced $1.25 to close at $25.50 and closed with 57,785 units changing hands.

Guardian Holdings dropped $25 to close at a 52 weeks’ low of $470 with 1,890 stocks clearing the market, Jamaica Producers gained 75 cents to end at $21.75 after an exchange of 6,547 shares, Jamaica Stock Exchange rallied 86 cents to $13.86, with 774 stock units crossing the exchange. JMMB Group advanced $1.01 in closing at $30.01 after 50,284 stocks changed hands, Kingston Wharves gained $1 after ending at $33, with 1,413 units crossing the market, Massy Holdings climbed $2 to end at $82 after an exchange of 1,950 shares. NCB Financial rose $3.99 to close at $74.99, with 29,173 stocks crossing the market, PanJam Investment rallied 51 cents to $53 in an exchange of 696 units, Proven Investments lost $1.35 in closing at $26.50 with the swapping of 3,354 shares. Sagicor Group declined 45 cents to $46.55 with investors transferring 3,778 stock units, Scotia Group shed 89 cents to end at $34.06 in an exchange of 7,082 stocks, Seprod declined $5.41 after ending at $61.01 while exchanging 196,078 shares and Supreme Ventures advanced $1.25 to close at $25.50 and closed with 57,785 units changing hands.

In the preference segment, Eppley 7.50% preference share popped 47 cents in closing at $7.97 in switching ownership of 1,801 stock units, Jamaica Public Service 9.5% dropped $300 to close at $2700 in trading one stock and 138 Student Living preference share increased $7.43 in closing at $77.43 with investors transferring 30 shares.

In the preference segment, Eppley 7.50% preference share popped 47 cents in closing at $7.97 in switching ownership of 1,801 stock units, Jamaica Public Service 9.5% dropped $300 to close at $2700 in trading one stock and 138 Student Living preference share increased $7.43 in closing at $77.43 with investors transferring 30 shares.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Key Insurance highest ICTOP10 jumps 37%

Stocks dropped to their lowest levels this past week after falling even lower than they did to close of the previous week as investors continue to shun the market, but the time is not far off that Bank of Jamaica will begin lowering interest rates and fuel a market resurgence as they sent the clearest signal that interest rates have not only peaked but will be headed downwards this past week.

The first signs of an easing of rate came this past week with BOJ CDs rates plunging 16 percent to an average of 8.85 percent from over 10 percent where it stood for several months. Importantly, the central bank cut the stock of CDS it holds from a peak of $109.5 billion on March 3, down to $82 billion at the latest auction, far less than from mid-January to the end of February, as more than $58 billion chasing after the $18 billion that was offered last week. While this happened the foreign exchange market looks very liquid with the rate falling under $152 to one US dollar from $155 earlier in February.

Performance in the past week for the Junior Market TOP10 saw only two stocks rising and seven falling, the majority of the declining stocks registering fell by 3 percent or less. General Accident jumped 20 percent to $5.98, but the bids are not there at the close, to support the price, but selling has abated for this stock currently. Everything Fresh rose 9 percent to close at $1.55 and actually traded at $1.65 during the week. Iron Rock Insurance fell 13 percent to $2 and Caribbean Assurance Brokers lost 6 percent to $1.90.

The Main Market TOP10 saw the highest gaining stock rising just 34 percent, after Key Insurance jumped to $3.50 and was followed by 138 Student Living with an 8 percent rise to $5.40, but Caribbean Producers dropped 8 percent to $9.07. All other movements were 3 percent or less.

The Main Market TOP10 saw the highest gaining stock rising just 34 percent, after Key Insurance jumped to $3.50 and was followed by 138 Student Living with an 8 percent rise to $5.40, but Caribbean Producers dropped 8 percent to $9.07. All other movements were 3 percent or less.

The Junior Market has a long term pattern, with the market starting to rise around a month before quarterly results are due and declining shortly after results are released. This is a pattern worth noting that can be built into investment decisions that can improve returns.

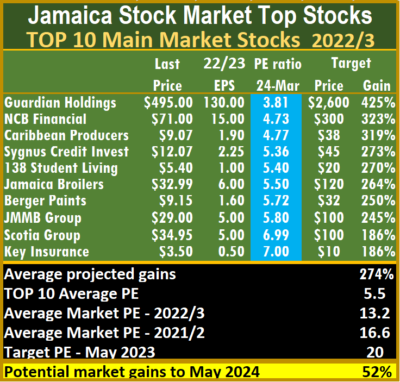

At the end of the week, the average PE for the JSE Main Market TOP 10 is 5.5, well below the market average of 13.2, while the Junior Market Top 10 PE sits at 5.9 compared with the market at 10.6. The differences are important indicators of the level of likely gains for ICTOP10 stocks. The Junior Market is projected to rise by 248 percent and the Main Market TOP10 an average of 274 percent, to May 2024, based on 2023 forecasted earnings.

The Junior Market has 9 stocks representing 19 percent of the market, with PEs from 15 to 24, averaging 19, well above the average of the market. The top half of the market has an average PE of 15, suggesting that this may be a logical value for junior market stocks currently.

The Main Market 16 most valued stocks are priced at a PE of 15 to 100, with an average of 29 and 19 excluding the highest valued stocks and 18 for the top half excluding the stocks with the highest valuation. The above average shows the extent of potential gains for the TOP 10 stocks.

The Main Market 16 most valued stocks are priced at a PE of 15 to 100, with an average of 29 and 19 excluding the highest valued stocks and 18 for the top half excluding the stocks with the highest valuation. The above average shows the extent of potential gains for the TOP 10 stocks.

ICTOP10 focuses on likely yearly winners, accordingly, the list includes some of the best companies in the market but not always. ICInsider.com ranks stocks based on projected earnings, allowing investors to focus on the most undervalued stocks and helping to remove emotions in selecting stocks for investments that often result in costly mistakes.

IC TOP10 stocks are likely to deliver the best returns up to the end of May 2023 and are ranked in order of potential gains, computed using projected earnings for the current fiscal year. Expected values will change as stock prices fluctuate and result in weekly movements in and out of the lists. Revisions to earnings are ongoing, based on receipt of new information.

Persons who compiled this report may have an interest in securities commented on in this report.

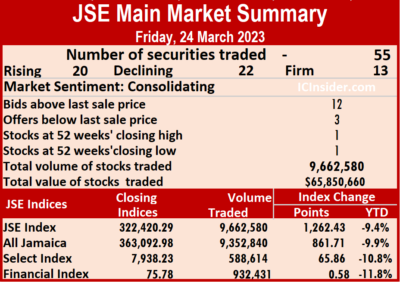

JSE Main Market rises on boosted volume

The Jamaica Stock Exchange Main Market recorded gains at the close on Friday, with trading picking up over Thursday, with 69 percent rise in volume traded at a 32 percent higher value than that on Thursday, with trading in 55 securities compared to 54 on Thursday, as prices of 20 rose, 22 declined and 13 ending unchanged.

A total of 9,662,580 shares were exchanged for $65,850,660 versus 5,709,003 units at $49,903,876 on Thursday.

A total of 9,662,580 shares were exchanged for $65,850,660 versus 5,709,003 units at $49,903,876 on Thursday.

Trading averages 175,683 units at $1,197,285 versus 105,722 shares at $924,146 on Thursday and month to date, an average of 260,937 units at $2,658,456, compared with 265,883 units at $2,743,184 on the previous day. February ended with an average of 183,599 units at $2,160,070.

Wigton Windfarm led trading with 4.91 million shares for 50.8 percent of the total volume Transjamaican Highway followed, with 1.19 million units for 12.3 percent of the day’s trade and Sagicor Select Financial Fund with 888,269 units for 9.2 percent market share.

The All Jamaican Composite Index rallied 861.71 points to 363,092.98, the JSE Main Index gained 1,262.43 points to close at 322,420.29 and the JSE Financial Index rose 0.58 points to settle at 75.78.

The PE Ratio, a formula used to ascertain appropriate stock values, averages 13.2 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

The PE Ratio, a formula used to ascertain appropriate stock values, averages 13.2 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows 12 stocks ended with bids higher than their last selling prices and one stock with a lower offer.

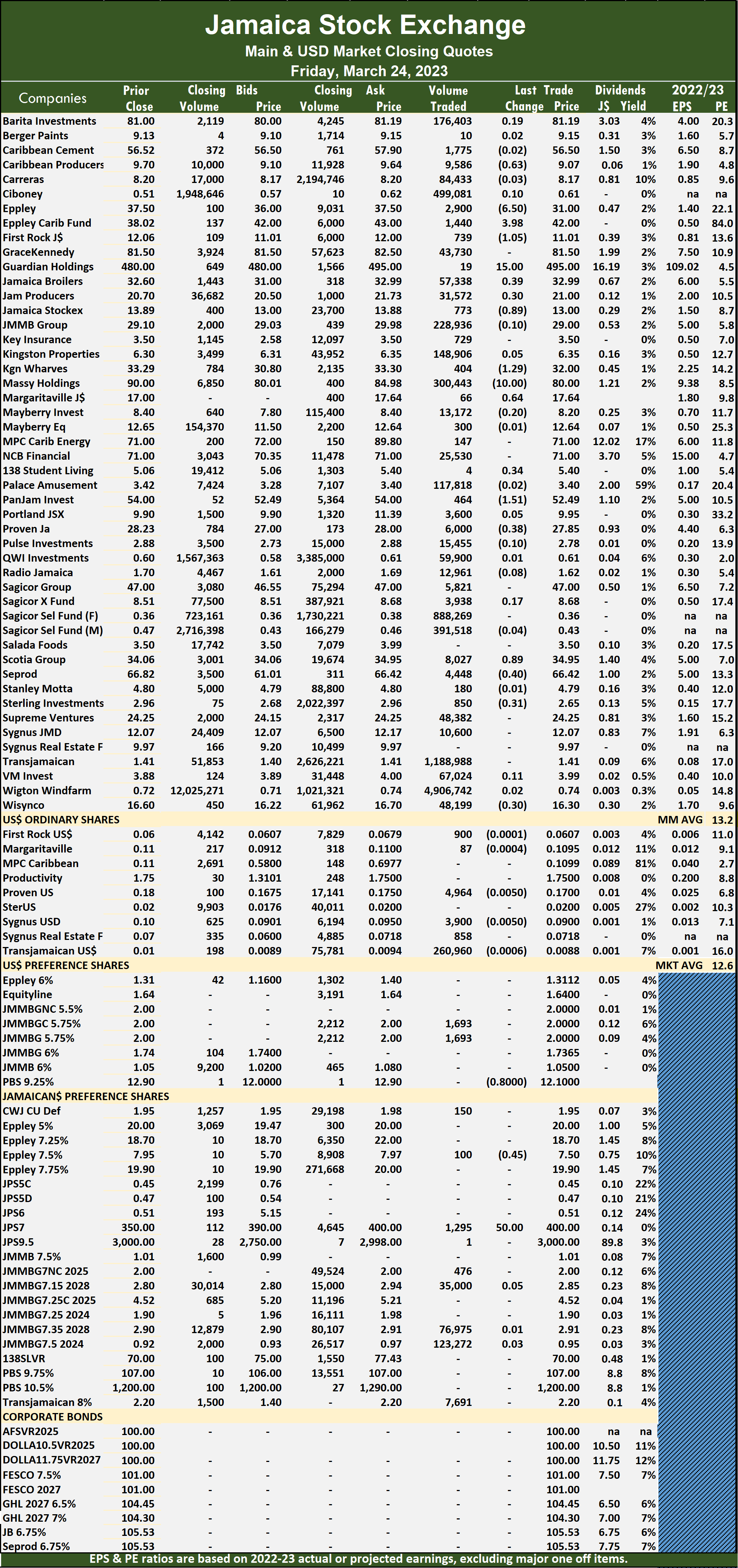

At the close, Caribbean Producers dipped 63 cents to end at $9.07, with 9,586 shares clearing the market, Eppley declined $6.50 in closing at $31 in an exchange of 2,900 stock units, Eppley Caribbean Property Fund advanced $3.98 to close at $42 with investors trading 1,440 units. First Rock Real Estate lost $1.05 to finish at $11.01 after trading 739 stocks, Guardian Holdings climbed $15 to $495, with 19 stocks crossing the exchange, Jamaica Broilers rallied 39 cents to $32.99 with a transfer of 57,338 stock units. Jamaica Producers increased 30 cents in closing at $21 after an exchange of 31,572 shares,  Jamaica Stock Exchange fell 89 cents to $13 after exchanging 773 units, Kingston Wharves dropped $1.29 to $32 as investors exchanged 404 stocks. Margaritaville popped 64 cents to close at $17.64 in trading 66 shares, Massy Holdings shed $10 to close at $80, with 300,443 stock units changing hands, 138 Student Living rose 34 cents to $5.40 with an exchange of 4 units. PanJam Investment fell $1.51 to $52.49, with 464 shares crossing the market, Proven Investments shed 38 cents to end at $27.85, with 6,000 stock units passing through the exchange, Scotia Group gained 89 cents in closing at $34.95 after 8,027 units changed hands. Seprod declined 40 cents to close at $66.42 while exchanging 4,448 stocks, Sterling Investments dipped 31 cents to $2.65 in switching ownership of 850 units and Wisynco Group dropped 30 cents to $16.30 after a transfer of 48,199 stock units.

Jamaica Stock Exchange fell 89 cents to $13 after exchanging 773 units, Kingston Wharves dropped $1.29 to $32 as investors exchanged 404 stocks. Margaritaville popped 64 cents to close at $17.64 in trading 66 shares, Massy Holdings shed $10 to close at $80, with 300,443 stock units changing hands, 138 Student Living rose 34 cents to $5.40 with an exchange of 4 units. PanJam Investment fell $1.51 to $52.49, with 464 shares crossing the market, Proven Investments shed 38 cents to end at $27.85, with 6,000 stock units passing through the exchange, Scotia Group gained 89 cents in closing at $34.95 after 8,027 units changed hands. Seprod declined 40 cents to close at $66.42 while exchanging 4,448 stocks, Sterling Investments dipped 31 cents to $2.65 in switching ownership of 850 units and Wisynco Group dropped 30 cents to $16.30 after a transfer of 48,199 stock units.

In the preference segment, Eppley 7.50% preference share lost 45 cents in closing at $7.50 in an exchange of 100 shares and Jamaica Public Service 7% gained $50 to a record high of $400 with the swapping of 1,295 stocks.

In the preference segment, Eppley 7.50% preference share lost 45 cents in closing at $7.50 in an exchange of 100 shares and Jamaica Public Service 7% gained $50 to a record high of $400 with the swapping of 1,295 stocks.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

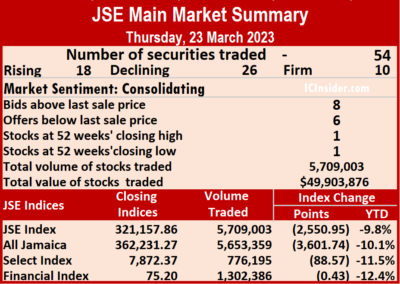

Main Market trading and prices drop

Trading activity on the Jamaica Stock Exchange Main Market ended on Thursday, with the volume of stocks traded declining 63 percent and the value 20 percent more than on Wednesday, with trading in 54 securities compared to 50 on Wednesday, with 18 rising, 26 declining and 10 ending unchanged

A total of 5,709,003 shares were traded for $49,903,876 versus 15,400,994 units at $41,503,503 on Wednesday.

A total of 5,709,003 shares were traded for $49,903,876 versus 15,400,994 units at $41,503,503 on Wednesday.

Trading averaged 105,722 shares at $924,146 versus 308,020 stocks at $830,070 on Wednesday and month to date, an average of 265,883 units at $2,743,229, compared to 275,557 units at $2,853,106 on the previous day. February closed with an average of 183,599 units at $2,160,070.

Wigton Windfarm led trading with 1.41 million shares for 24.6 percent of total volume, followed by Transjamaican Highway with 1.22 million units for 21.4 percent of the day’s trade and Sagicor Select Financial Fund with 770,011 units for 13.5 percent market share.

The All Jamaican Composite Index dropped 3,601.7 points to 362,231.27, the JSE Main Index fell 2,550.95 points to 321,157.86 and the JSE Financial Index lost 0.43 points to close at 75.20.

The PE Ratio, a formula used to ascertain appropriate stock values, averages 13.3 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

The PE Ratio, a formula used to ascertain appropriate stock values, averages 13.3 for the Main Market. The JSE Main and USD Market PE ratios incorporate earnings forecasted by ICInsider.com for companies with the financial year ending between November 2022 and August 2023.

Investor’s Choice bid-offer indicator shows nine stocks ended with bids higher than their last selling prices and six with lower offers.

At the close, Barita Investments advanced $1 to $81 trading 15,166 shares, Caribbean Cement fell 48 cents to close at $56.52 in an exchange of 62,955 units, Eppley Caribbean Property Fund dropped $2.39 to end at $38.02 after 4,269 stocks changed hands. GraceKennedy rose $1.50 in closing at $81.50 as investors exchanged 121,844 stock units, Jamaica Broilers lost 40 cents after ending at $32.60 in swapping of 39,738 stocks, Jamaica Producers declined $1.05 to close at $20.70 in switching ownership of 4,000 stock units. Jamaica Stock Exchange rallied 82 cents to $13.89, with 18,116 units crossing the market, JMMB Group shed 80 cents to end at $29.10 with investors transferring 78,082 shares,  Key Insurance gained 50 cents in closing at $3.50, with 70,472 units crossing the market. Kingston Properties dipped 62 cents to $6.30, with an exchange of 133,315 stock units, Kingston Wharves increased $2.24 to $33.29 after a transfer of 5,235 stocks, Massy Holdings popped $10 in closing at $90 with an exchange of 35,865 shares. NCB Financial shed $1.50 to close at $71 with the swapping of 12,507 stock units, Portland JSX fell $1.59 to $9.90 with an exchange of 13,434 shares, Proven Investments climbed $1.73 to end at $28.23 while exchanging 907 stocks. Scotia Group dipped 88 cents to end at $34.06, with 13,977 units clearing the market, Seprod advanced $2.79 to close at $66.82, with 176,511 stocks changing hands, Sterling Investments increased 44 cents in ending at $2.96 after trading 13,068 units. Supreme Ventures lost 75 cents in closing at $24.25 in an exchange of 91,005 shares and Sygnus Real Estate Finance gained 77 cents to end at $9.97 with just one unit passed through the market.

Key Insurance gained 50 cents in closing at $3.50, with 70,472 units crossing the market. Kingston Properties dipped 62 cents to $6.30, with an exchange of 133,315 stock units, Kingston Wharves increased $2.24 to $33.29 after a transfer of 5,235 stocks, Massy Holdings popped $10 in closing at $90 with an exchange of 35,865 shares. NCB Financial shed $1.50 to close at $71 with the swapping of 12,507 stock units, Portland JSX fell $1.59 to $9.90 with an exchange of 13,434 shares, Proven Investments climbed $1.73 to end at $28.23 while exchanging 907 stocks. Scotia Group dipped 88 cents to end at $34.06, with 13,977 units clearing the market, Seprod advanced $2.79 to close at $66.82, with 176,511 stocks changing hands, Sterling Investments increased 44 cents in ending at $2.96 after trading 13,068 units. Supreme Ventures lost 75 cents in closing at $24.25 in an exchange of 91,005 shares and Sygnus Real Estate Finance gained 77 cents to end at $9.97 with just one unit passed through the market.

In the preference segment, Jamaica Public Service 7% climbed $56.46 ending at another record high of $350 with a transfer of 2,037 stocks and Jamaica Public Service 9.5% popped $450 in closing at $3000 with the swapping of 3 units.

In the preference segment, Jamaica Public Service 7% climbed $56.46 ending at another record high of $350 with a transfer of 2,037 stocks and Jamaica Public Service 9.5% popped $450 in closing at $3000 with the swapping of 3 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.