Jamaica Producers former headquarters in Kingston Jamaica

Profit surged 102 percent in the September quarter, to $330 million from $164 million in 2019 for shareholders of Jamaica Producers. For the nine months to September, profit jumped 66 percent to $959 million from $578 million in 2019 on the back of a modest rise in revenues.

Sale revenues rose just 5 percent for the quarter, to $5.22 billion from $4.96 billion but gained a stronger 8 percent for the year to date, to hit $15.4 billion from $14.3 billion in 2019. The third-quarter revenues grew more slowly than second-quarter revenues, which increased 12 percent to $5.4 billion over the 2018 period and net profit attributable to shareholders increased then by 52 percent to $399 million.

The group’s main activities are port terminal operations, logistics, food and juice manufacturing, the cultivation, marketing and distribution of fresh produce, land management and the holding of investments. The group has operations in the UK, Europe, Jamaica and some other Caribbean countries.

The current year is not the only one that profits jumped sharply for the group. In 2018, profit attributable to the Group’s shareholders rose 66.5 percent for the June quarter over that of 2017 and 65 percent for the half-year from revenues that grew 20 percent and 25 percent, respectively. The group had significant growth in profit from ongoing operations in 2017 over 2016 with negligible profit from operations.

Improvement in profit margin in the half of the year to 34 percent from 31 percent in 2018 continued at the same pace in the September quarter with 34 percent from 29 percent in 2018 and for the year to September, 34 percent from 30 percent in 2018. The improved margin helped push gross profit up 24 percent in the quarter to $1.76 billion from $1.42 million and rose 23 percent for the year to date, to $5.3 billion from $4.3 billion in 2019.

Selling, administration and other operating expenses rose 18 percent to $958 million in the quarter and increased 14 percent in the nine months to $2.8 million. Finance cost declined in the quarter, to $78 million from $89 million in 2018 and from $234 million to $277 million for the nine months.

Earnings per share (EPS) came out at 29.4 cents for the quarter and 85.5 cents for the nine months. EPS should end the fiscal year ending December to $1.25 with a PE ratio of 17 at the price of $21.50 it last traded on the main market of the Jamaica Stock Exchange and is in line with the average for main market stocks. The net asset value ended at $12.30, with the stock selling at 1.75 book value.

Gross cash flow brought in $3.7 billion, growth in receivables, investment transactions, purchase of fixed assets and the paying of $125 million in dividends resulted in cash funds at the ending at $927 million. At the end of September, shareholders’ equity stood at $14 billion, with borrowings at just $6 billion. Net current assets ended the period at $6.4 billion inclusive of trade and other receivables of $9 million, cash and bank balances of $927 million. Current liabilities stood at $3.2 billion at the end of September.

Jamaica Producers is a buy for the medium to long term.

With its best performance in the last five years with a 92 percent jump in profit to $1 billion in 2019 financial year,

With its best performance in the last five years with a 92 percent jump in profit to $1 billion in 2019 financial year,

MPC Caribbean Clean Energy (MPCL) stock traded at a record $275 on the Jamaica Stock Exchange last week, as investors positioned to buy into 22,848,320 class B shares offered to shareholders by way of rights.

MPC Caribbean Clean Energy (MPCL) stock traded at a record $275 on the Jamaica Stock Exchange last week, as investors positioned to buy into 22,848,320 class B shares offered to shareholders by way of rights.

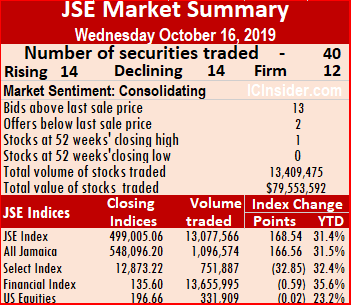

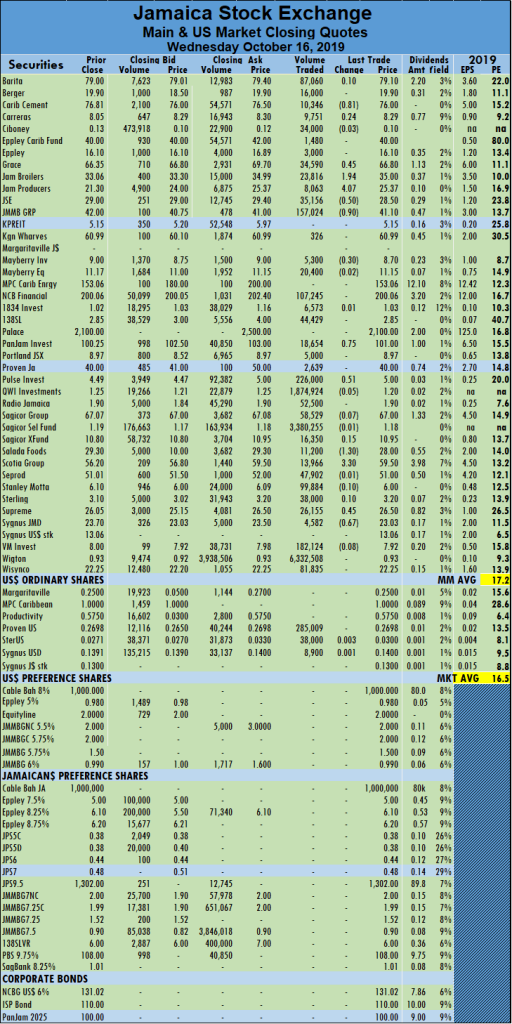

The Jamaica Stock Exchange main market climbed marginally on lower volume and value with the JSE All Jamaican Composite Index adding just 166.56 points to close at 548,096.20, the JSE Index rising 168.54 points to 499,005.06 and the JSE Financial Index slipping 0.59 points to 135.60.

The Jamaica Stock Exchange main market climbed marginally on lower volume and value with the JSE All Jamaican Composite Index adding just 166.56 points to close at 548,096.20, the JSE Index rising 168.54 points to 499,005.06 and the JSE Financial Index slipping 0.59 points to 135.60. The average volume and value for the month to date amounts to 951,792shares at a value of $17,309,566 for each security traded and previously 1,004,254 shares at $18,786,922 for each stock traded. The market closed out September with an average of 1,585,081 units valued at $14,071,562 for each security traded.

The average volume and value for the month to date amounts to 951,792shares at a value of $17,309,566 for each security traded and previously 1,004,254 shares at $18,786,922 for each stock traded. The market closed out September with an average of 1,585,081 units valued at $14,071,562 for each security traded. Pulse Investments closed 51 cents higher to a new closing high of $5 in an exchange of 226,000 shares. Salada Foods fell by $1.30 to $28 with 11,200 shares traded, Scotia Group advanced by $3.30, after 13,966 shares changed hands to settle at $59.50, Supreme Ventures gained 45 cents to close at $26.50 with 26,155 shares being exchanged and Sygnus Credit Investments lost 67 cents, in closing at $23.03 after trading 4,582 shares.

Pulse Investments closed 51 cents higher to a new closing high of $5 in an exchange of 226,000 shares. Salada Foods fell by $1.30 to $28 with 11,200 shares traded, Scotia Group advanced by $3.30, after 13,966 shares changed hands to settle at $59.50, Supreme Ventures gained 45 cents to close at $26.50 with 26,155 shares being exchanged and Sygnus Credit Investments lost 67 cents, in closing at $23.03 after trading 4,582 shares. The financial news out of

The financial news out of

Profit at

Profit at