The Jamaica Stock Exchange should be welcoming another new main market listing, before too long as the latest new entrant to come with an initial public offer, is expected to present their case to the investment public in the coming week.

The Jamaica Stock Exchange should be welcoming another new main market listing, before too long as the latest new entrant to come with an initial public offer, is expected to present their case to the investment public in the coming week.

The issue hopes to raise just over $1 billion that would see shareholders’ equity moving from $700 million to nearly $2 billion if the maximum target is reached. The pricing of the issue is expected to be less than $1.40 per share.

New IPO coming in days

September 7, 2019 by

Jamaica Producers’ 3 years profit surge

September 1, 2019 by

Jamaica Producers profit up 52% in June 2019 quarter.

Jamaica Producers (JP) increased second-quarter revenues by 12 percent to $5.4 billion over the 2018 period and net profit attributable to shareholders by 52 percent to $399 million from $263 million.

For the half-year, JP posted a 52 percent rise in profit due to the group’s shareholders of $629 million compared to $415 million with revenues that rose 9 percent from $9.3 billion to $10.16 billion. Profit was boosted by other income of $191 million in the quarter, up from $100 million in 2018 and $163 for the half-year versus $153 million in the 2018 half-year. The current year is not the only one that profit jumped sharply for the group, in 2018, profit attributable to the Group’s shareholders rose 66.5 percent for the June quarter over that of 2017 and 65 percent for the half-year from revenues that grew 20 percent and 25 percent respectively. The group saw a major improvement in profit from ongoing operations in 2017 over 2016 when profit from operation was negligible.

Gross profit rose 22 percent to $1.85 billion and 23 percent for the half-year to $3.5 billion. Selling, administration and other operating expenses rose 16 percent to $954.4 million in the June quarter from $823.3 million in the similar period in 2018 while the half-year recorded an increase of 12 percent to $1.83 billion from $1.64 billion in 2018.

Jamaica Producers snacks

The group recorded a gain of $575 million on disposal of 30 percent of its interest in JP Snacks but is shown directly in the group’s shareholders’ equity and not a part of the regular profit statement. Producers, as the company is fondly called. reported earnings per share of 36 cents for the quarter and 56 cents for the half-year.

Segment results show the food and drink business with sales of $5.95 billion compared to $5.46 billion in 2018 and contributed profit of $438 million for the group. The Logistics & Infrastructure segment generated revenues of $4.2 billion versus $3.83 billion in 2018 and recorded a profit of $1.56 billion from $1.26 billion in 2018.

The Group closed the half-year with shareholders’ equity of $13.5 billion, loans borrowed amounted to $6 billion, cash funds of $792 million, securities amounting to $5.7 billion, current assets of $10.3 billion and current liabilities of $4.5 billion.

The group’s stock is listed on the main market of the Jamaica Stock Exchange and last traded at $27.50 and a PE of 18 times 2019 earnings.

Profit jumps sharply at Elite

August 25, 2019 by

Drax Hall branch of Elite now completed

Elite Diagnostic last traded on the Junior Market a $6.40 to be up 117 percent for 2019 and is one of three stocks on that market to more than double, this year.

Investors feel there is more to gain from investing in the stock of this technological business as they continue to buy into the stock and pushed the price as high as $7.50 after the company posted full-year results in August.

Elite reported net profit for the June quarter at $24.6 million compared to $3 million for the similar period a year ago. A strong increase in revenues and a fall in repairs of equipment and administrative expenses compared to the year-ago period helped with the strong growth in profit. Profit before tax for the 12 months grew 32 percent to $47.4 million compared to $35.8 million for the similar period a year ago. Gross cash inflows amounted to $103 million but the company had net borrowing of $8 million and purchase of property, plant and equipment amounting to $135 million, down from $295 million purchased in the prior year.

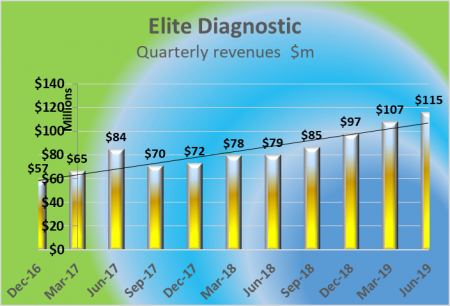

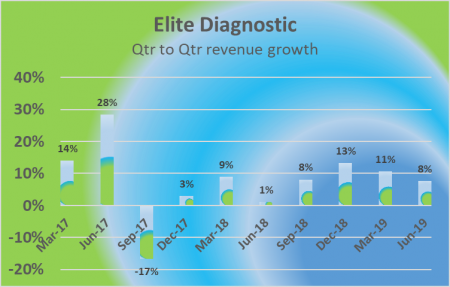

Revenues were $115 million for the 4th quarter, an increase of 46 percent over the $79 million for the same period last year. Revenues for the 12 months to June 2019 jumped 35 percent to $404 million compared to $298 million for the similar period a year ago. The directors in their report to shareholders accompanying the financials, stated, “the increase in revenue was due to greater utilization of the Liguanea branch which also extended their hours of operation”.

Importantly, revenues not only grew year over year but for each of the last 7 quarters it increased quarter to quarter. For the 2020 fiscal year, revenues should hit $500 million from the two Kingston locations. Cost of sales remains static in dollars, in spite of the sharp rise in revenues.

Direct cost rose from $28 million in the June 2018 fourth quarter, to $30 million in 2019 and from $117 in the year to June 2018 versus just $119 million in 2019 and $96 million in 2017. Increased growth from the two existing locations should have a powerful impact on profits, resulting from the near static direct cost.

Administrative cost fell from $36 million to $33 million in the June quarter of 2019 but rose sharply by 52 percent for the year to $152 million. Depreciation charge climbed from $$7.5 million for the quarter to $14 million in 2019 and moved from $28 million to $56 million for the year.

Elite enjoying a long period of increased quarterly growth in revenues since December 2017.

The company closed the fiscal year with shareholders’ equity of $447 million, loans borrowed amounting to $196 million, cash funds of $94 million, current assets of $119 million and current liabilities of $50 million.

“Demand for imaging services remains strong and the company continues to execute its plan providing exceptional patient care, excellent service, expanding its services and gaining market share.

The construction of the new St Ann (Drax Hall) location is completed and the company expects to open its doors in September 2019. This new location will have full imaging services and doctors’ offices,” the directors reported.

IC Insider.com forecast earnings for the full year ending 2020 at 55 cents, on this basis the stock is priced at a PE ratio of 12, but the next two years is when the full pay off will take place when the expansions should be maturing.

Lasco Manufacturing Q1 profit up 19%

August 24, 2019 by

Add your HTML code here...

Revenues at Lasco Manufacturing rose just 3 percent in the June quarter to $1.79 billion but improved profit margin lifted profit after tax by 19 percent to $282 million.

Revenues at Lasco Manufacturing rose just 3 percent in the June quarter to $1.79 billion but improved profit margin lifted profit after tax by 19 percent to $282 million.

The slow growth in the quarter contrast to a 6 percent rise in revenues in the fiscal year to March 2019 when the company posted revenues of $7.6 billion. The June quarter’s revenues are lower than the $2 billion achieved in the March quarter but are consistent with September and December quarters last year with $1.7 billion and $1.8 billion respectively.

Operating cost rose 7 percent to $330 million but cost of sales declined to $1.19 billion from $1,125 billion in 2018 with the change resulting in gross profit margin rising to 37 percent from 35 percent in 2018. Finance cost was virtually flat at $32 million but taxation rose from $34 million to $40 million. Lasco generated other income of $17 million in the quarter versus just $3 million in 2018. Earnings per share rose to 6 cents from 5 cents in 2018 and are expected to exceed the 26 cents per share realised in the fiscal year to March, with IC Insider.com forecasting 38 cents per share.

According to the managing director’s report, “the positive outturn reflects gains from ongoing improvements in operational efficiencies, reduction in structural costs and streamlining of the operations. Capital improvements for the period totaled $60 million with the main focus during the period being the completion of the powder plant expansion.”

Lasco generated gross cash flow of $348 million for the quarter but paid $250 million in dividends and repaid loans amounting to $106 million. At the end of the period, cash and bank balance stood at $995 million. Long-term loans outstanding amounts to $876 million.

Lasco Manufacturing products.

Loans amounting to $464 million is due to be repaid in the next twelve months. The company seems to be heading into a period of greater maturity, when loans will be repaid from the strong annual cash flows that the company is slated to generate, going forward.

Shareholders equity stands at $5.9 billion and net current assets $2.2 billion, which exceed current liabilities of $1.5 billion.

There has been increased interest in the stock with the recent announcement that the United Cannabis Corporation, the American company that is partnering with Lasco Manufacturing for the production of cannabis-infused water among other cannabis medicinals, has been issued a license to cultivate cannabis through a company called Cannabinoid Research and Development.

The stock traded on the Junior Market of the Jamaica Stock Exchange on Friday at $5.50.

Sales up 24% in 2019 at Knutsford

August 22, 2019 by

One of Knutsford Express buses.

For the nine months to February, revenues were up 24 percent, with the February quarter showing a healthy increase of 22 percent. Revenues rose 22 percent from $249 million in the 2018 May quarter to end at $304 million, while revenues for the February quarter rose from $232 million to $286 million and for the full year, it rose from $926 million to $1.15 billion.

Profit rose just 6 percent from $178 million for the full year to $188 million for earnings per share of 38 cents. Resulting from the losses in the foreign operations, profit in the final quarter fell from $50 million in the 2018 May quarter, to $30 million in the same period this year. The company generated income of J$21 million and incurred a loss of J$25 million in the Florida operation that commenced in the February quarter. According to Managing director Oliver Townsend, “the Florida operation is a long term investment which we believe will come into its own in the second year of operations.” Townsend was responding to a query by IC Insider.com as to when this operation would break even.

Knutsford does not break out direct operational expenses, making it difficult to determine the gross profit generated by the company.

Knutsford’s New Kingston depot

In addition, the absence of that critical data makes it impossible for investors to measure the efficiency of the operations. Data extracted suggest it could be in the region of 40 percent. Overall expenses rose 28 percent to $963 million for the year with fuel rising 28 percent and labour cost 30 percent.

The company benefitted from the hub at Sangster Airport resulting in more foreign arrivals utilising the services, especially those journeying to and from Negril, the company reported.

Fixed assets grew to $733 million with additions of $406 million during the year, cash and short-term investments ended at $355 million with borrowings at $215 million and shareholders’ equity of $780 million.

Knutsford trades on the Junior Market and closed at $11.10 on Tuesday, with a PE of 29 based on historical earnings. IC Insider is forecasting profits in the current year to be in the region of 75 cents per share that would result in a PE of 15 and slightly above the Junior Market’s average of 13.

Pressure on Jetcon’s sales easing

August 20, 2019 by

Jetcon sales are bouncing back since June after a sharp fall between January and May.

In its recent report on second-quarter results, management reported another challenging period following a sharp fall in sales and profit for the first quarter. Revenues fell 26 percent and profits by 75 percent and for the half-year, revenues declined by 23 percent and profit by 70 percent.

The first half performance reverses three years of solid growth for the company. “We are pleased to report that we are now seeing positive developments since June, with sales up 10 percent ahead of 2018, in both June and July. Orders for August, suggest that we will enjoy a much better sales than in 2018. Sales in August last year were below the historical pattern. Our projection calls for higher sales than 2018 in the second half of the financial year,” the company’s management stated in the report accompanying the results.

Revenues fell to $221 million from $300 million in the June 2018 quarter with a fall in gross margin, from 18 percent to 16.5 percent and a decline in pretax profit, to $9 million versus $35 million in 2018. Earnings per share ended at 1.5 cents versus 6 cents in 2018.

Attentive shareholders at Jetcon’s AGM

“We reduced prices in some areas to move inventories in the first half of the year and this negatively affected our gross margin. We expect that the discounting will ease as the year progresses,” the management report stated.

Jetcon shares traded on the Junior Market of the Stock Exchange at a 52 weeks’ low of $1.58 on Friday but bounced to $1.70 on Monday.

Persons connected with ICInsider.com are also connected with the company.

NCB solid stock for the future

August 13, 2019 by

NCB Financial Group (NCB) produced net profit of $21.3 billion for the nine months to June 2019 with profit attributable to stockholders of $20.7 billion, a marginal increase of $87 million over 2018.

NCB Financial Group (NCB) produced net profit of $21.3 billion for the nine months to June 2019 with profit attributable to stockholders of $20.7 billion, a marginal increase of $87 million over 2018.

For the quarter to June, NCB reported $8.3 billion in profit attributable to shareholders inclusive of $2.3 billion resulting from the increased value of the near 30 percent interest NCB owned in Guardian (GHL) before acquiring majority shares, during the quarter. Results include the consolidation of two months of GHL’s income coupled with the gain from revaluing the shares that NCB held in GHL previously, as an associated company.

For the nine months ended June, net operating income rose 22 percent to $63 billion from $51.6 billion in the prior year while it increased 28 percent to $24.5 billion in the June quarter over 2018.

Banking and investment activities netted $55.8 billion, up 13 percent over the $49.4 billion for the comparative 2018 period and for the quarter the enlarged group produced $21 billion compared to $18 billion in 2018. A 14 percent growth in our loan portfolio helped in pushing net interest income to $32.4 billion or 27 percent over $25.4 million generated in 2018. For the quarter, net interest income grew to 30 percent to $12.4 billion.

Net fee and commission income rose from $4 billion in 2018 to $5 billion for the June quarter and from $11.7 billion to $13.4 billion for the nine months period. Gains on foreign exchange trading declined sharply from $11.4 billion to $8.7 billion for the nine months period and from $4.2 billion in 2018 to $2.8 billion for the June quarter.

The net result from insurance activities grew 218 percent over the prior year to $7.2 billion from $2.3 billion in the prior year nine months period. For the quarter, net income tripled the $1.15 billion in the 2018 June quarter to reach $3.4 billion in 2019. “One of our Jamaican life insurance subsidiaries benefitted from improved spread performance and changing mortality assumptions, resulting in a significant contribution to the net profit. The consolidation of GHL’s insurance activities contributed 45 percent of net insurance revenues reported for the third quarter,” the group directors reported in their commentary to shareholders.

The net result from insurance activities grew 218 percent over the prior year to $7.2 billion from $2.3 billion in the prior year nine months period. For the quarter, net income tripled the $1.15 billion in the 2018 June quarter to reach $3.4 billion in 2019. “One of our Jamaican life insurance subsidiaries benefitted from improved spread performance and changing mortality assumptions, resulting in a significant contribution to the net profit. The consolidation of GHL’s insurance activities contributed 45 percent of net insurance revenues reported for the third quarter,” the group directors reported in their commentary to shareholders.

Operating expenses including loan and securities losses accounted for $46 billion, an increase of $13 billion or 41 percent over the prior nine months in 2018. “The consolidation of GHL and an additional quarter of Clarien’s results in the current reporting period contributed to 43 percent of this increase,” the group reported.

Impairment losses on loans and securities increased by 166 percent to $3.65 billion from $2.46 in the nine months and from just $941 million in the June 2018 quarter to $1.7 billion in the 2019 period.

Total assets grew with the acquisition of majority shares in GHL to $1.6 trillion, an increase of $635 billion or 68 percent over the prior year. “The consolidation of GHL, net of adjustments, added $517 billion in assets to the Group’s portfolio. The Group’s loans and advances, net of provision for credit losses, stood at $412 billion, an increase of $50.5 billion or 14 percent over the prior year, attributable to strong growth in our Jamaican portfolio along with the consolidation of GHL’s $14.6 billion of loans and receivables” the NCB directors report stated.

Customer deposits reached $509 billion at the end of June, an increase of 10 percent or $45 billion over the prior year. Policyholders’ liabilities increased from $39 billion in June 2018 to $422 billion due to the consolidation of GHL. Investment Securities and Reverse Repurchase Agreements Investment securities, including pledged assets, and reverse repurchase agreements amounted to $780 billion. This portfolio grew by 106 percent or $400.6 billion over the prior year, primarily due to the consolidation of GHL’s portfolio valued at $369 billion. Stockholders’ equity amounted to $137 billion, a 10 percent or $12.8 billion increase over the prior year due primarily to an 18 percent increase in retained earnings.

Earnings per share for the quarter came in at $3.42 but that includes one-time income and expenses, ongoing earnings could be in the region of $3 per share or around $12 annually. For the nine months earnings per share reported was at $8.49. Going forward the growth in the loan portfolio is one of the most critical factors to look for in assessing prospects going forward, with the acquisition of the General Insurance portfolio this area is also very critical to growth in the future. There are areas of duplication in the operations of Guardian and NCB accordingly, investors can expect rationalization to come and with that reduced cost and likely more robust sourcing for new business. NCB stock that last traded on the Jamaica Stock Exchange at $220 is a good long term investment.

The Board of Directors declared an interim dividend of 90 cents per ordinary stock unit. The dividend is payable on August 27, to stockholders of record as on August 13.

SOS & tTech head IC MarketWatch

August 8, 2019 by

SOS anticipates maximising profits from every business line in 2019.

Second-quarter results are coming out but still, a number of them are due out over the next few days. Results released today throws up a few strong numbers and the stocks of these companies are worth watching.

First, out the block today was tTech an IC TOP 10 BUY RATED selection with possible gains of 167 percent. The company reported a 20 percent increase in revenues in the second quarter of $91 million and a 62 percent rise in profit to $16 million and 15 cents per share with flat profit of $17 million or 16 cents per share for the half-year. The stock climbed to $6.50 at the close on Thursday and seems headed higher.

Stationery and Office Supplies reported a strong 195 percent rise in profit fro the second quarter to reach $34 million compared to just $12 million in 2018 from a 23 percent rise in sales to $295 million. for the half-year profit rose 63 percent to $92 million from $56 million from a 23 percent revenue increase to $639 million. The company is on target to meet IC Insider.com’s forecast of 75 cents for the full year. Radio Jamaica is yet to release its first-quarter results but investors have sent to stock to a high of $1.90 on Thursday.  Demand has built and supplies shrank sharply and that should help move the price higher.

Demand has built and supplies shrank sharply and that should help move the price higher.

Caribbean cement traded 3,770,741shares up to $85 and is worth watching with supply falling. Sagicor Select ETF Fund was listed on Thursday but demand resulted in the price exceeding the 30 percent limit permitted by the JSE with investors attempting to trade the stock as high as $1.90 but the stock closed with no trading and closed with bids amounting 12 million shares at $1.30 and 324,520 were the lowest offers at $1.85. Lasco Manufacturing could be moving higher in coming trading days as supply declines and demand rises.

JSE continues to lead the world

August 2, 2019 by

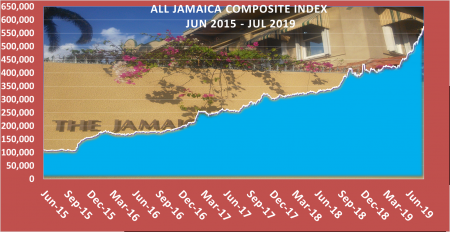

Jamaica Stock Exchange (JSE) performance continues to lead the global markets by a big margin according to data tracked by Bloomberg Business.

Jamaica Stock Exchange (JSE) performance continues to lead the global markets by a big margin according to data tracked by Bloomberg Business.

Last year, the JSE was rated as the best performing market in the world. The main market of the local stock exchange, grew 67.5 percent over the past twelve months the JSE index is up 38 percent for the first seven months of this year. The nearest rival is Argentina Merval TR Index, up 43 percent and 37 percent over the same periods. Brazil Ibovespa Brasil Sao Paulo Stock Exchange Index chips in at 33 percent for the last twelve months and 17 percent for 2019 to date.

The next best performance half a world away from the west, with New Zealand X20 Index coming in with 29 percent for the twelve months period and 25 percent for 2019 to date.

The data shows that the vast majority of markets are having a tough time with many of them suffering declines.

Carib Cement 2019 profit mixed

July 31, 2019 by

Carib Cement silos

Caribbean Cement revenues climbed 5.6 percent in the June quarter to $4.68 billion and 4 percent year to June, with $9.13 billion booked.

The company reported lower profit the June quarter than in 2018, due mainly to $485 million incurred as foreign currency losses and ended up with profit after tax at $368 million versus $674 million in 2018. Or the half-year profit after tax grew 48.6 percent to $15 billion. The company reported earnings per share of 43 cents versus 79 cents in the similar quarter in 2018 and $1.76 compared to $1.18 in the 2018 six months period.

Expenses excluding depreciation and finance grew 2.7 percent for the quarter to $2.94 billion and fell 21 percent for the half-year to $5.47 billion. The sharp reduction in cost results from the termination of an equipment lease agreement with the parent company and the purchase of those assets. The acquisition of the assets drove depreciation charge for the quarter to $405 million from $340 million in 2018 and $796 million from $467 million for the six months periods. Finance cost including foreign exchange losses rose to $688 million from $412 million for the quarter and $856 million versus $386 million for the half-year.

The results boosted shareholders’ equity to $7.9 billion from $6.4 billion at the end of December last year as the company wiped out accumulated losses of $994 million at the end of 2018 leaving a surplus of $493 million. Borrowing amounts to $9.8 billion while cash funds amount to $394 million and net current assets stood at negative $759 million.

The stock trades at $80 on the Jamaica Stock Exchange main market. IC Insider.com projects earnings for the full year to December at $5 per share that would place the PE ratio at 16, just around the markets PE of 17. With the economy doing well and increased construction activities, investors should have their eyes focused on increased future earnings.