Caribbean Assurance Brokers are offering just 52.5 million ordinary shares for sale at the subscription price of $1.91 with a minuscule amount allocated for the general public.

The offer includes 44.36 million units for Reserved Share Applicants, including 5.25 million for Mayberry Investments’ clients with just 8.14 million units available to the general public.

The offer includes 44.36 million units for Reserved Share Applicants, including 5.25 million for Mayberry Investments’ clients with just 8.14 million units available to the general public.

Earnings for the past three years to 2018 have been almost flat, but results to September 2019 show a steep rise putting pretax profit to $71 million compared with $43 million for the full year in 2018. Based on the 2019 results, annualized earnings on 263 million shares that will be in issue after the IPO will translate to earnings of 36 cents per share, with a PE around, five which is well below the Junior Market level.

The company intends to use the net proceeds of the IPO to (i) pay IPO & Listing Expenses, (ii) expand its brokerage operations to other Caribbean territories, (iii) extend the Company’s solar photovoltaic system and for working capital purposes.

The issue opens on February 18 and scheduled to close on March 3, subject to early closure. Investors fortunate to get a good volume will enjoy a nice payday, with the limited supply, the general public will have to be satisfied with the usual dribblings.

The company acts as brokers for International, general and individual Life Insurance and employee benefits.

The directors of the company are Raymond H. Walker, Chairman Chief Executive Officer. Non-executive directors are, Rion B. Hall, Norman Minott, Jennifer Rajpat, Barrington Whyte, Tania Waldron-Gooden, Carlton Barclay and Janice P. Holness.

Caribbean Assurance IPO details out

Growing Lasco Manufacturing profits

Profit at Lasco Manufacturing rose 10.5 percent in the December quarter, to $218 million from $197 million in 2018. For the nine months to December, profit increased by 11 percent to $781 million from $701 million in 2018.

The company’s net results rose modestly, this is due to a hike in its tax bill from $28 million in the 2018 quarter to $71 million in 2019 and from $129 million for the nine months to December 2018, to $169 million in 2019. Before the increased tax charge, the latest quarter results were up a robust 28 percent to $289 million and 14.5 percent for the year to December at $949 million.

The company’s net results rose modestly, this is due to a hike in its tax bill from $28 million in the 2018 quarter to $71 million in 2019 and from $129 million for the nine months to December 2018, to $169 million in 2019. Before the increased tax charge, the latest quarter results were up a robust 28 percent to $289 million and 14.5 percent for the year to December at $949 million.

The improved profit flowed from a rise in sales revenues of 10 percent for the quarter to $2 billion from $1.8 billion in 2018 and 4 percent for the year to date to $5.9 billion from $5.6 billion in 2018.

The gains in 2019, following on from the March 2018 fiscal year when profit moved from $561 in 2017 to $1.07 billion. The 2017 bene was off sharply from $826 million generated in 2016 and $612 million in 2015. The current fiscal year should see the company surpassing the $1m mark in profits for the second time.

Improvement in profit margin, in the first half of the year, continued into the December quarter with 36 percent from 34 percent in 2018 and for the year to date period, from 34 percent in 2018 to 37 percent this year. Input cost rose 6 percent in the December quarter, to $1.28 billion, compared to $1.2 billion in 2018, and was virtually flat for the year to date period at $3.7 billion versus $3.68 billion. The rise in revenues and containment of cost below the growth in revenues resulted in operating profit rising 18 percent in the quarter to $719 million from $611 million and almost 11 percent for the year to date to $2.14 billion from $1.9 billion in 2018.

Lasco’s ICool drinks.

Administrative and Other operating expenses rose 7 percent to $393 million in the quarter and 9 percent in the nine months to $1.1 billion. Finance cost declined in the quarter, to $21 million from $26 million in 2018 and $90 million to $75 million for the nine months.

The company continues to expand its capacity. According to James Rawle, Managing Director, “Capital investments were primarily focused on the expansion of the dry plant at White Marl facility and is expected to be completed by the end of the financial year.”

Gross cash flow brought in $975 million, but funds were used to finance a number of items, with $314 million going into stock market investments, funding of a rise in receivables and inventories. Addition to fixed assets absorbed $166 million, while $220 million in loan net of inflows was repaid, with $250 million going into dividend payment. At the end of December, shareholders’ equity stood at $6.5 billion, with borrowings at just $1 billion inclusive of $484 million that will is payable within a year. Net current assets ended the period at $2.4 billion inclusive of trade and other receivables of $2 million, cash and bank balances of $719 million. Current liabilities ended the period at $1.6 billion.

Earnings per share came out at 5 cents for the quarter and 19 cents for the nine months. IC Insider.com is forecasting 30 cents per share for the year to March and 45 cents for the 2021 fiscal year.

The stock traded at $4.25 on the Junior Market of the Jamaica Stock Exchange with a PE ratio of 14 times earnings for 2020 and just seven times that of 2021. Net asset value is $1.57, with the stock selling at 2.5 times book value. At prices around the current level, the stock is a buy.

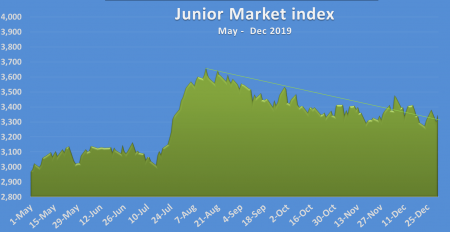

Lousy 2019 for Junior Market stocks

Junior Market trades

Junior Market did not end 2019 with glory splashed all over it with the market for small and medium-size companies, gaining just 3.1 percent in 2019, down from 18.8 percent in 2018 and 24.3 percent in 2017.

While the premier stocks rose appreciably in 2019, stocks on the Junior Market faltered in its performance in 2019, with the price of only one stock listed on the market at the end of 2018 doubling in value in 2019 and another coming close, with a rise of 97 percent. The Junior Market that saw a half of its listings declining in the year had just four stocks gaining over 100 percent. Three new listings in the Junior Market occupied the top three positions. Fontana, pharmacy operators, was the top performer and closed the year at $7.30 with a rise of 288 percent on the expectation that the new store at Waterloo Road that opened in the December quarter, will boost income and profit in the 2020 fiscal year. The second-best performer, the advertising and production company – Limners and Bards, was listed in summer and delivered a 200 percent increase for investors who bought the stock at the IPO stage. The recently listed MailPac Group, with gains of 111 percent from the IPO price of $1 took up the number three position.

Honey Bun fresh from the expansion of its bakery operations and a 20.4 percent growth in revenues in the September quarter and profit after tax rising 67 percent for the full 2019 fiscal year, doubled in price with a 103 percent increase. Elite Diagnostic is the sole Junior Market stock from the 2018 TOP 10 to remain in the TOP 10 in 2019. tTech 6th worse performer in 2018, made it to the 2019 Top 10 in the eight position. Jetcon Corporation, the number 9 worse performer and GWest Corporation at number 10 in 2018 again ended in the worse ten performing stocks in 2019, in fourth for GWest and 10th position for Jetcon.

Elite Diagnostic is the sole Junior Market stock from the 2018 TOP 10 to remain in the TOP 10 in 2019. tTech 6th worse performer in 2018, made it to the 2019 Top 10 in the eight position. Jetcon Corporation, the number 9 worse performer and GWest Corporation at number 10 in 2018 again ended in the worse ten performing stocks in 2019, in fourth for GWest and 10th position for Jetcon.

One major reason for the divergence for the performances of the Main Market and the Junior Market is to be found it the valuation multiple for both markets.

While both markets close 2018, with PE ratios around 16 times 2018 earnings the market moved decidedly in different paths with Main Market stocks approaching PE ratio around 20 leaving the Junior Market at just over 14.

Gains fin the Junior Market peaked at 12.8% on August 14 and drifted down since.

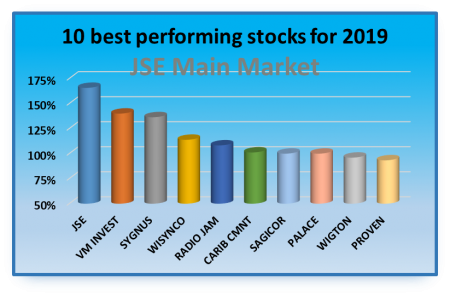

9 JSE Main Market stocks double in 2019

Last year was a mixed one for investors in the Jamaican stock market. On the one hand, Investors in Main Market stock enjoyed gains of more than 30 percent for the second year in a row, but Investors in Junior Market Stocks had far less to cheer about with a market rise of 3 percent.

Ten JSE Main Market stocks doubled in price in 2019 with the Jamaica Stock Exchange ordinary share leading the group with a gain of 177 percent with the Main market rising 34.3 percent for the year, upon the 31.7 percent rise in 2018.

Ten JSE Main Market stocks doubled in price in 2019 with the Jamaica Stock Exchange ordinary share leading the group with a gain of 177 percent with the Main market rising 34.3 percent for the year, upon the 31.7 percent rise in 2018.

VM Investments rose 120 percent to hold down the number two spot followed by Sygnus Credit Investments, Wisynco Group and Radio Jamaica. All three ended up on the worse 10 performing stocks in 2018 along with Proven Investments, the 10th best performer in 2019, with a 93 percent gain. Palace Amusement stock gained 100 percent, in 2019 and is the only 2018 TOP 10 stock to reappear in the top 10, in 2019. In 2018, it came in at number 3 best performing stock, compared to eight position in 2019. Palace has a remarkable record of more than doubling in each year, from 2016 to end in the TOP 10 for all of them

First Rock heads to market for US$18m

First Rock Capital Holdings, the real estate owners and developers in January next year open their public share offering to the Jamaica capital market to raise up to US$18,487,465 in added capital.

First Rock Capital Holdings, the real estate owners and developers in January next year open their public share offering to the Jamaica capital market to raise up to US$18,487,465 in added capital.

The Company issued 166 million class A shares before commencing commercial operations in the first quarter of 2019, following the successful closure of its private placement in March 2019 that raised US$15.5 million.

The Initial Public Offer by First Rock is up to 106,083,332 Shares in two classes with Class A comprising 51,053,333 US$ Class A Ordinary Shares at 12 US cents each and 10.8 US cents for Reserved shares. Additionally, 55,029,999 Class B Ordinary shares are Jamaica dollar-denominated and priced similar to the class A share. The company reserves the right to upsize the offer by an additional 53,041,666 shares in the event of oversubscription.

The general public will be offered Shares of 16,250,000 Class A Ordinary shares, with 14,553,333 units reserved for Key Strategic Partners and 20,250,000 reserved for First Rock Affiliates. Of the 55,029,999 units of the Class B Ordinary shares, 37,916,666 are available for the general public, with 3,613,333 shares are reserved for subscription to Key Strategic Partners and 13,500,000 shares are reserved for subscription by First Rock Affiliates. Application to list on the JSE is dependent upon the Company’s raising at least $200 million or the US dollar equivalent.

The company owns properties in Jamaica, Cayman Islands, Costa Rica and in the USA.

Opening Date January 13, next year and scheduled to close on January 31.

First Rock reported a loss from operations of US$203,648 before a US$374,301 forex gain to September resulted in a pretax profit of US$170,653.

The forecasted is for the profit of US$2,647,696 in 2020, US$4,653,992 in 2021 and US$6,614,802 in 2022 with income coming from rental and from 2021 includes revenues from the sale of units. The projections have annual inflows from foreign exchange gains and fair value increase in investment properties. While the fair value gains may well occur as forecasted, there is no certainty that there will be annual forex gains.

The company’s directors are, Dr. David Lowe, Douglas Halsall, York Page Seaton, Kisha Anderson, Norman Reid 8 Davis Avenue, Alton Morgan and Lisandra Rickards. Sagicor Investments are brokers to the issue.

Limners & Bards revise EPS

Kimala Bennett, Chief Executive Officer of The Lab.

Following IC Insider.com’s report that the earnings per share (EPS) for Limners & Bards were incorrect, the audited accounts of the company are now revised to reflect the EPS the article suggested they should be.

The revised audited reports now state that the calculation of earnings per stock unit is based on the profit after taxation and the weighted average number of stock units in issue during the year. Net profit attributable to shareholders of $94,746,238 in 2019, $62,313,858 in 2018. The weighted average number of ordinary stock units is 803,836,715 in 2019 and 756,552,202 in 2018, resulting in Basic and diluted earnings per stock unit of12 cents in 2019 and 8 cents in 2018.

The original audited financial statements showed the basic and diluted earnings per stock unit at 10 cents for the 2019 fiscal year and 7 cents for 2018 based on the weighted average of ordinary stock units 945,690,252 in each year.

IC Insider’s report on Tuesday stated that “Limners and Bards released full-year results with profit after taxation of $95 million, up by an impressive 52 percent from the $62 million earned in 2018 from healthy gains in revenues, with earnings per share (EPS) works out at 12 cents for 2019 and 8 cents for 2018.”

The company’s operating revenues grew 31 percent to $632 million from $483 million in 2018, with the last quarter growing a stunning 58 percent to $146 million, generating income just below the $152 million generated in the July quarter and profit before tax of $18 million versus $16.5 million in the July quarter.  While revenues for the year rose 31 percent, direct cost rose at a slower pace, resulting in the gross profit climbing 39.4 percent over 2018 as gross profit margin rose to 36 percent compared to 33.7 percent in 2018. Administrative cost rose well ahead of revenue growth with a 41 percent increase over 2018, but the full-year increase is below a 70 percent surge in the July quarter while the fourth quarter saw a rise of 39 percent over 2018, is in line with the full-year increase.

While revenues for the year rose 31 percent, direct cost rose at a slower pace, resulting in the gross profit climbing 39.4 percent over 2018 as gross profit margin rose to 36 percent compared to 33.7 percent in 2018. Administrative cost rose well ahead of revenue growth with a 41 percent increase over 2018, but the full-year increase is below a 70 percent surge in the July quarter while the fourth quarter saw a rise of 39 percent over 2018, is in line with the full-year increase.

In a statement accompanying the nine months results, Chairman, Steven Gooden and Kimala Bennett, Chief Executive Officer stated, “Administration expenses increased by $23.737 million, or 42 percent, which represent 16.63 percent of revenue for the nine months compared to 14.60 percent to the corresponding period ended July 31, 2018. These increases are primarily attributable to staff costs (due to increase work volume), subcontractors (on retainer contracts), depreciation charges and security costs”.

The company reports on three segments comprising Production, Media and Agency. For 2019 Production generated earnings of $226 million and profit of $100 million while Media raked in $292 million but ended with just $40 million in profit and agency the most profitable brought in $114 million and delivered $85 million in net income.

The company ended the year with cash and equivalent of $292 million with shareholders’ equity of $356 million, up from $123 million in 2018. Borrowings stood at $50 million with payables of $83 million and current assets of $387 million.

IC Insider.com forecast earnings per share of 20 cents for 2020 that puts the PE ratio at 15 with the stock closing trading at $3 on Tuesday on the Junior Market of the Jamaica Stock Exchange and is a stock to be watched into 2020.

Auditors spoil good Lab results

Limners and Bards released full-year results with profit after taxation of $95 million, up by an impressive 52 percent from the $62 million earned in 2018 from healthy gains in revenues.

Earnings per share (EPS) works out at 12 cents for 2019 and 8 cents for 2018. Operating revenues rose 31 percent to $632 million from $483 million in 2018, the last quarter grew at a stunning 58 percent to $146 million, just below the $152 million generated in the July quarter and profit before tax of $18 million versus $16.5 million in the July quarter.

Auditors are required to check records of companies and ensure that they accord with various regulations and the financial statements which they audit and certify are free form errors and misstatements.

Kimala Bennett, Managing Director of The Lab.

The Limners and Bards financials is the latest report to indicate that there is a problem with the industry and that a number of the players are eroding the confidence investors have it the financial reports they certify. To be fair to the company auditors, they are not solely to blame. Management, including the directors, is also responsible for preventing financial with errors going out to the public, as they also have to sign off on the financials.

The computation of earnings per share is an area of problem for some of the smaller audit firms. In the past, there are instances where the calculation is wrong when there are stock splits and new share issues.

According to the Limners and Bards financial statements, the basic and diluted earnings per stock unit is 10 cents for the 2019 fiscal year and 7 cents for 2018 based on the weighted average of ordinary stock units 945,690,252 in each year. That is entirely wrong. What are the facts? The company had 756.55 million shares in issue before the sale of 189,138,050 shares to the public in July this year with the company listing on the stock exchange on July 26. The EPS computation for 2018 is to be based on 756.6 million shares and for 2019, just over 800 million units. The company’s stock closed trading on Monday at $2.78 for a PE of 21 times 2019 earnings before tax and 14 times 2020 earnings of 20 cents per share.

MailPac set to jump

MailPac shares were listed on Wednesday and closed at $1.32 for a rise of 32 percent, with less than 49,373 units traded.

MailPac shares were listed on Wednesday and closed at $1.32 for a rise of 32 percent, with less than 49,373 units traded.

The most recent information has the highest buying price at $1.72 for 305,000 shares, followed by 73,247 shares at $1.70 a lot of 26,388 units at $1.51 and 300,001 units at $1.50. At $1.49, there is buying for 60,357 units and at $140 to buy 4.37 million.

Selling starts at $1.35 with 24,092 shares, followed by 21,227 units at $1.44 and 21,227 at $1.45, with a total of 82 offers posted so far.

Trading in the early trading session on Thursday resulted in just 56,620 units changing hands at $2.10 at a PE ratio of 15. The maximum price that it can trade at for the day is $2.18. With the price movement to date, the stock has moved out of the IC Insider.com TOP 10 list.

Profit stays strong at Sagicor Group

Sagicor Group last traded at $66 on the JSE.

Profit before tax rose by just 8 percent in the quarter to $5.23 billion from $4.85 billion and 27 percent for the year to September to $14.5 billion from $11.47 billion in 2018.

“The main contributing factors were the depreciation of the Jamaican dollar, which positively impacted realized and unrealized gains attributable to US dollar positions and the 36 percent appreciation of the Jamaica Stock Exchange Main Market indices, benefitting the Group by way of trading gains and capital appreciation,” a statement from the chairman and CEO stated.

Net profit attributable to shareholders continues an upward trend from the start of the financial year, with Q1 posting profit of $2.7 billion and moving to $3.7 billion in Q2 and $4.4 billion in the current quarter. Earnings per stock rose to $1.15 for the September quarter compared to 91 cents in the 2018 quarter, and $2.79 for the nine months to September, versus $2.27 year to September 2018.

Total income rose 28 percent for the quarter to $25 billion from $19.5 billion and 31 percent for the year to date to $67.5 billion from $51.48 billion in 2018. “Contributing to the overall revenue outturn in the September quarter was a 23 percent increase in net premium income, investment revenue of 28 percent and an increase of 10 percent in fees and other income,” the management stated in their report accompanying the quarterly.

The results for the nine months to September reflected gains of 18 percent in net premium revenue, to $33.8 billion and 23 percent for the September quarter to reach $12.7 billion while investment income climbed 42 percent in the nine months to $19.3 billion and 28 percent for the quarter to $7.4 billion. Fees and other income rose 16 percent to $10.5 billion and 10 percent in the quarter to $3.7 billion.

Insurance benefits, administrative and other expenses climbed 37 percent to $19.46 billion from $14.24 billion, compared to a 35 percent increase to $53.66 billion from $39.87 billion in 2018 for the year to date.

Net insurance benefits rose 28 percent in the quarter to $8 billion from $6.3 billion in 2018 and from $19 billion to $21.2 billion for the nine months.

Net insurance benefits rose 28 percent in the quarter to $8 billion from $6.3 billion in 2018 and from $19 billion to $21.2 billion for the nine months.Administrative expenses climbed 17 percent in the quarter to $5.2 billion from a similar period in 2018 and 16 percent in the nine months to $15.3 billion.

For the nine months to September, the group’s segment results show Individual Insurance revenues rising a healthy 24 percent to $25.8 billion from $20.9 billion in 2018 but resulting in segment profit falling from $4.1 billion to $3.8 billion. Investment Banking accounted for $4.5 billion of revenues in 2019, up 67 percent from $2.7 billion in 2018, with profit nearly doubling to $2 billion from $1.1 billion. Employee Benefits revenues climbed from $17.6 billion in 2018 to $20.4 billion, and profit rising from $2.9 billion to $3.2 billion and Commercial Banking revenues rose 19 percent from $8.3 billion in 2018 to $9.9 billion with profit hitting $1.95 billion from $1.4 billion in 2018. All other segments added revenues of $6.4 billion in 2019 from $2.9 billion, with profit rising from $270 million in 2018 to $415 million.

The stock last traded on the JSE Main Market at $66 for a PE ratio of 16.5 compared to a market average of 19, an indication that the price is undervalued.

At the end of September, shareholders’ equity stood at $88.4 billion up from $73 billion at the end of September 2018. Assets ended the period at $458 billion inclusive of financial investments of $196 billion, cash and bank balances of $25 billion and liabilities at $338 billion.

Earnings per share came out at $1.15 for the quarter and $2.79 for the nine months. IC Insider.com is forecasting $4 per share for PE of 16.5 times earnings at the last traded price of $66.

Sagicor Group results for the nine months to September include the consolidation of the new subsidiaries, Sagicor Real Estate Fund and Travel Cash Jamaica. The Group’s latest acquisition, Advantage General Insurance, in which the Group acquired a 60 percent interest on September 30, did not affect earnings for the nine months.

Big jump in Honey Bun profit

![]() Another major milestone in Honey Bun’s brief history of listing on the JSE Junior Market was reached at the end of the 2019 fiscal year, ending in September, with record revenues and profit.

Another major milestone in Honey Bun’s brief history of listing on the JSE Junior Market was reached at the end of the 2019 fiscal year, ending in September, with record revenues and profit.

The full-year results show pretax profit rising 73 percent to $183 million versus $106 million in 2018 and profit after tax rising 67 percent to hit $157 million from a 17 percent rise in revenues to $1.54 billion. Revenues grew even faster in the final quarter by 20.4 percent improvement over the 18.9 that revenues grew in the third quarter over 2018.

The results benefited from improved efficiency with cost sales rising well below the growth in revenues, with input cost increasing 12 percent for the year, driving gross profit margin to 48 percent, an improvement from the 46 percent in 2018. Selling and Distribution expenses rose 16 percent to $250 million from $214, Administrative Cost excluding depreciation rose 18 percent $284 million from $249 million.

Earnings per share rose to 33 cents in the just concluded year from just 18 cents in 2018. Importantly, the company is on the way to earn 70 cents per share for 2020 for a profit of $335 million and should go on to earn $1 per share or $490 million in 2021 and $1.30 or $600 million in the following year when the tax concession for half the regular rate ends.

One Honey Bun’s Products.

The company is benefitting from a capital expenditure of $330 million spent over the last two years to expand the factory and bring manufacturing under one location as well as an expansion of product range. The operations generated gross cash flow of $230 million up from $145 million in 2018.

Shareholders’ equity climbed to $741 million from $618 million. Current assets increased from $209 million to $353 million with net current assets ending at $185 million from $89 million in 2018. Cash and cash equivalents stood at $193 million, up from $100 million, but the company has Investments of $92 million comprising quoted shares and money market instruments treated as non-current assets.

The company manufacture and distributes baked products for the local and export markets.

The stock receives the IC BUY RATED seal of approval. The stock traded at $7 on the Jamaica Stock Exchange Junior Market for a PE of 10.