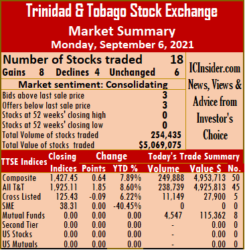

Stock prices mostly rose at the end of market activity on Monday, resulting in the market rising after trading 72 percent more shares, with 82 percent higher value than on Friday, on the Trinidad and Tobago Stock Exchange.

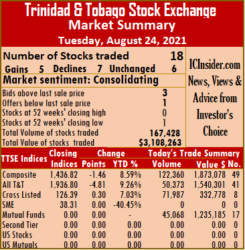

At the close, 18 securities traded compared to 19 on Friday, with eight stocks rising, four falling, leaving six unchanged. The Composite Index rose 0.64 points to 1,427.45, the All T&T Index increased 1.85 points to 1,925.11 and the Cross-Listed Index fell 0.09 points to 125.43.

At the close, 18 securities traded compared to 19 on Friday, with eight stocks rising, four falling, leaving six unchanged. The Composite Index rose 0.64 points to 1,427.45, the All T&T Index increased 1.85 points to 1,925.11 and the Cross-Listed Index fell 0.09 points to 125.43.

A total of, 254,435 shares traded for $5,069,075 versus 147,901 units at $2,783,955 on Friday. An average of 14,135 units traded at $281,615, up from 7,784 shares at $146,893 on Friday, with trading month to date averaging 10,137 units at $180,124 versus 8,937 units at $149,677. August averaged 16,186 units at $226,311.

Investor’s Choice bid-offer indicator shows three stocks ended with bids higher than their last selling prices and three with lower offers.

At the close, Agostini’s popped 40 cents to $24.40 after exchanging one share, Angostura Holdings spiked 43 cents to $17 in exchanging 7,668 stock units, Ansa Mcal remained at $57, with 40,830 stocks traded. Calypso Macro Investment Fund climbed 30 cents to $16.50 in an exchange of 558 units, Clico Investment Fund remained at $26.80, after 3,989 stocks crossed the market, First Citizens Bank lost 24 cents in closing at $50.26 with the swapping of 1,610 shares. GraceKennedy dipped 1 cent to $6.29, with 1,000 units changing hands, Guardian Holdings closed at $33, with 400 stock units crossing the market, JMMB Group remained at $2.15 in switching ownership of 10,149 stock units.  Massy Holdings added 2 cents to end at $82.02, with 18,716 shares changing hands, National Enterprises remained at $3.41 trading 50 units, National Flour Mills popped 8 cents to $1.90 with an exchange of 10,898 stocks. One Caribbean Media slipped 2 cents to $4.86 while exchanging 155,667 shares, Republic Financial Holdings rallied 5 cents to $135.50, after trading 100 units, Scotiabank gained 2 cents to $59.02 after exchanging 329 stocks. Trinidad & Tobago NGL fell 25 cents to $17.30, with 1,220 stock units crossing the exchange, Trinidad Cement rose 8 cents to $4 with the swapping of 1,000 shares and Unilever Caribbean finished trading 250 stock units at $16.40.

Massy Holdings added 2 cents to end at $82.02, with 18,716 shares changing hands, National Enterprises remained at $3.41 trading 50 units, National Flour Mills popped 8 cents to $1.90 with an exchange of 10,898 stocks. One Caribbean Media slipped 2 cents to $4.86 while exchanging 155,667 shares, Republic Financial Holdings rallied 5 cents to $135.50, after trading 100 units, Scotiabank gained 2 cents to $59.02 after exchanging 329 stocks. Trinidad & Tobago NGL fell 25 cents to $17.30, with 1,220 stock units crossing the exchange, Trinidad Cement rose 8 cents to $4 with the swapping of 1,000 shares and Unilever Caribbean finished trading 250 stock units at $16.40.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Guardian Holdings rallied 15 cents to $33 with an exchange of 28,567 shares, JMMB Group remained at $2.15 with the swapping of 13,671 stocks, Massy Holdings shed 90 cents to $82 in trading 8,455 units. National Enterprises added 1 cent in closing at $3.41 and exchanging 100 shares, National Flour Mills popped 1 cent to end at $1.82 in switching ownership of 7,198 stock units, Republic Financial Holdings shed 3 cents ending at $135.45, with 1,500 units crossing the market. Scotiabank fell 49 cents to $59 after exchanging 921 stocks, Trinidad & Tobago NGL lost 5 cents to end at $17.55 with the swapping of 1,050 shares, Trinidad Cement dipped 7 cents to $3.92 in trading 3,135 stock units and West Indian Tobacco declined 50 cents to $31 in exchanging 346 units.

Guardian Holdings rallied 15 cents to $33 with an exchange of 28,567 shares, JMMB Group remained at $2.15 with the swapping of 13,671 stocks, Massy Holdings shed 90 cents to $82 in trading 8,455 units. National Enterprises added 1 cent in closing at $3.41 and exchanging 100 shares, National Flour Mills popped 1 cent to end at $1.82 in switching ownership of 7,198 stock units, Republic Financial Holdings shed 3 cents ending at $135.45, with 1,500 units crossing the market. Scotiabank fell 49 cents to $59 after exchanging 921 stocks, Trinidad & Tobago NGL lost 5 cents to end at $17.55 with the swapping of 1,050 shares, Trinidad Cement dipped 7 cents to $3.92 in trading 3,135 stock units and West Indian Tobacco declined 50 cents to $31 in exchanging 346 units. JMMB Group remained at $2.15 after 2,385 shares crossed the market, L.J. Williams B share remained at $1.35 in trading 1,450 units. Massy Holdings rose 90 cents to $82.90, with 4,062 stock units clearing the market, National Enterprises fell 20 cents in closing at $3.40 with an exchange of 517 shares, Point Lisas ended at $3.20, with 400 stocks changing hands. Prestige Holdings rallied 40 cents to $7.40 in switching ownership of 66 stock units, Republic Financial Holdings popped 3 cents to $135.48 while exchanging 811 shares, Scotiabank remained at $59.49, trading 1,051 units. Trinidad & Tobago NGL lost 6 cents in ending at $17.60 with the swapping of 585 stocks, Trinidad Cement increased 9 cents to $3.99 after exchanging 11,543 shares, Unilever Caribbean ended at $16.40 after 7,855 stocks crossed the market and West Indian Tobacco closed $31.50, after trading 1,035 stock units.

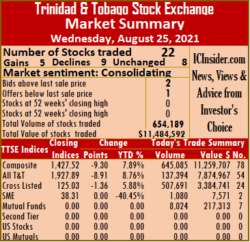

JMMB Group remained at $2.15 after 2,385 shares crossed the market, L.J. Williams B share remained at $1.35 in trading 1,450 units. Massy Holdings rose 90 cents to $82.90, with 4,062 stock units clearing the market, National Enterprises fell 20 cents in closing at $3.40 with an exchange of 517 shares, Point Lisas ended at $3.20, with 400 stocks changing hands. Prestige Holdings rallied 40 cents to $7.40 in switching ownership of 66 stock units, Republic Financial Holdings popped 3 cents to $135.48 while exchanging 811 shares, Scotiabank remained at $59.49, trading 1,051 units. Trinidad & Tobago NGL lost 6 cents in ending at $17.60 with the swapping of 585 stocks, Trinidad Cement increased 9 cents to $3.99 after exchanging 11,543 shares, Unilever Caribbean ended at $16.40 after 7,855 stocks crossed the market and West Indian Tobacco closed $31.50, after trading 1,035 stock units. At the close, 22 securities traded compared to 20 on Monday, with six stocks rising, six declining and 10 remaining unchanged. The Composite Index fell 1.59 points to 1,430.24, the All T&T Index dipped 5.40 points to 1,929.51 and the Cross-Listed Index gained 0.35 points to settle at 125.58.

At the close, 22 securities traded compared to 20 on Monday, with six stocks rising, six declining and 10 remaining unchanged. The Composite Index fell 1.59 points to 1,430.24, the All T&T Index dipped 5.40 points to 1,929.51 and the Cross-Listed Index gained 0.35 points to settle at 125.58. L.J. Williams B share remained at $1.35 while trading 700 stock units, National Flour Mills rose 1 cent to $1.81 after 4,676 units crossed the market, NCB Financial Group popped 2 cents to $8.25 in exchanging 110,667 shares. One Caribbean Media spiked 62 cents to $4.88 in an exchange of 1,000 stock, Point Lisas remained at $3.20 in trading 1,000 shares, Republic Financial Holdings dipped 1 cent to $135.45 with 8,198 stocks clearing the market. Scotiabank remained at $59.49 while exchanging 21 units, Trinidad & Tobago NGL declined 6 cents to $17.66 with the swapping of 5,979 stock units, Unilever Caribbean remained at $16.40 with an exchange of 737 stocks and West Indian Tobacco ended at $31.50 in exchanging 565 units.

L.J. Williams B share remained at $1.35 while trading 700 stock units, National Flour Mills rose 1 cent to $1.81 after 4,676 units crossed the market, NCB Financial Group popped 2 cents to $8.25 in exchanging 110,667 shares. One Caribbean Media spiked 62 cents to $4.88 in an exchange of 1,000 stock, Point Lisas remained at $3.20 in trading 1,000 shares, Republic Financial Holdings dipped 1 cent to $135.45 with 8,198 stocks clearing the market. Scotiabank remained at $59.49 while exchanging 21 units, Trinidad & Tobago NGL declined 6 cents to $17.66 with the swapping of 5,979 stock units, Unilever Caribbean remained at $16.40 with an exchange of 737 stocks and West Indian Tobacco ended at $31.50 in exchanging 565 units. GraceKennedy shed 8 cents to close at $6.21 after 87,090 shares changed hands, Guardian Holdings advanced 25 cents to $32.95 in trading 3,577 units, Guardian Media remained at $3.03 after 100 stock units crossed the market. JMMB Group popped 1 cent to $2.16 in switching ownership of 870 stocks, Massy Holdings fell 99 cents at $82, with 2,931 shares changing hands, National Enterprises traded 10,599 units at $3.60. National Flour Mills remained at $1.80, with 1,320 units clearing the market, NCB Financial Group slipped 2 cents to $8.23 with an exchange of 532 stocks, One Caribbean Media shed 58 cents to end at $4.26 after an exchange of 100 stock units. Republic Financial Holdings popped 1 cent to $135.46, trading 381 shares, Scotiabank climbed 89 cents to $59.49 after trading 50,073 stocks, Trinidad & Tobago NGL remained at $17.72 after exchanging 1,011 stock units. Trinidad Cement ended at $3.90 while trading 5,666 units and West Indian Tobacco remained at $31.50, with 625 shares changing hands.

GraceKennedy shed 8 cents to close at $6.21 after 87,090 shares changed hands, Guardian Holdings advanced 25 cents to $32.95 in trading 3,577 units, Guardian Media remained at $3.03 after 100 stock units crossed the market. JMMB Group popped 1 cent to $2.16 in switching ownership of 870 stocks, Massy Holdings fell 99 cents at $82, with 2,931 shares changing hands, National Enterprises traded 10,599 units at $3.60. National Flour Mills remained at $1.80, with 1,320 units clearing the market, NCB Financial Group slipped 2 cents to $8.23 with an exchange of 532 stocks, One Caribbean Media shed 58 cents to end at $4.26 after an exchange of 100 stock units. Republic Financial Holdings popped 1 cent to $135.46, trading 381 shares, Scotiabank climbed 89 cents to $59.49 after trading 50,073 stocks, Trinidad & Tobago NGL remained at $17.72 after exchanging 1,011 stock units. Trinidad Cement ended at $3.90 while trading 5,666 units and West Indian Tobacco remained at $31.50, with 625 shares changing hands. At the close, 18 securities traded, down from 20 on Thursday, with six stocks rising, five declining and seven remaining unchanged. The Composite Index rallied 5.49 points to settle at 1,430.96, the All T&T Index spiked 6.41 points to 1,933.61 and the Cross-Listed Index added 0.63 points to settle at 125.17.

At the close, 18 securities traded, down from 20 on Thursday, with six stocks rising, five declining and seven remaining unchanged. The Composite Index rallied 5.49 points to settle at 1,430.96, the All T&T Index spiked 6.41 points to 1,933.61 and the Cross-Listed Index added 0.63 points to settle at 125.17. Guardian Holdings shed 25 cents to $32.70 with the swapping of 2,090 units, JMMB Group dipped 1 cent to $2.15, trading 1,970 shares, Massy Holdings jumped $1.84 to $82.99 in exchanging 9 shares. National Enterprises remained at $3.60, 35 stock units crossing the market, National Flour Mills ended at $1.80, with 101,875 units clearing the market, NCB Financial Group rallied 26 cents to $8.25 after exchanging 25 stocks. Point Lisas closed at $3.20 after 20 stocks crossed the market, Republic Financial Holdings fell 3 cents to $135.45 in trading 2,390 stock units, Scotiabank traded 3,850 shares at $58.60. Trinidad & Tobago NGL dipped 1 cent to $17.72 with an exchange of 7,536 units, Trinidad Cement closed at $3.90 after exchanging 270 shares and West Indian Tobacco traded 3,208 stock units at $31.50.

Guardian Holdings shed 25 cents to $32.70 with the swapping of 2,090 units, JMMB Group dipped 1 cent to $2.15, trading 1,970 shares, Massy Holdings jumped $1.84 to $82.99 in exchanging 9 shares. National Enterprises remained at $3.60, 35 stock units crossing the market, National Flour Mills ended at $1.80, with 101,875 units clearing the market, NCB Financial Group rallied 26 cents to $8.25 after exchanging 25 stocks. Point Lisas closed at $3.20 after 20 stocks crossed the market, Republic Financial Holdings fell 3 cents to $135.45 in trading 2,390 stock units, Scotiabank traded 3,850 shares at $58.60. Trinidad & Tobago NGL dipped 1 cent to $17.72 with an exchange of 7,536 units, Trinidad Cement closed at $3.90 after exchanging 270 shares and West Indian Tobacco traded 3,208 stock units at $31.50. GraceKennedy remained at $6.30 in switching ownership of 1,670 shares, Guardian Holdings rose 5 cents to $32.95 with an exchange of 2,188 units, JMMB Group remained at $2.16, with 8,880 stock units crossing the market. Massy Holdings shed $1.60 to end at $81.15, with 1,074 shares changing hands, National Enterprises remained at $3.60 in an exchange of 3 stocks, National Flour Mills popped 1 cent in closing at $1.80, with 50,000 units clearing the market. NCB Financial Group remained at $7.99 while exchanging 25,000 stocks, One Caribbean Media remained unchanged at $4.84, with 27,630 units crossing the market, Point Lisas advanced 5 cents to $3.20 after exchanging 1,000 shares. Scotiabank fell 30 cents to $58.60 in trading 12,000 stock units, Trinidad & Tobago NGL lost 3 cents in closing at $17.73, with 5,549 stocks clearing the market, Trinidad Cement exchanged 109 units at $3.90. Unilever Caribbean climbed 14 cents to $16.40 with an exchange of 7,900 stock units and West Indian Tobacco remained at $31.50, trading 200 shares.

GraceKennedy remained at $6.30 in switching ownership of 1,670 shares, Guardian Holdings rose 5 cents to $32.95 with an exchange of 2,188 units, JMMB Group remained at $2.16, with 8,880 stock units crossing the market. Massy Holdings shed $1.60 to end at $81.15, with 1,074 shares changing hands, National Enterprises remained at $3.60 in an exchange of 3 stocks, National Flour Mills popped 1 cent in closing at $1.80, with 50,000 units clearing the market. NCB Financial Group remained at $7.99 while exchanging 25,000 stocks, One Caribbean Media remained unchanged at $4.84, with 27,630 units crossing the market, Point Lisas advanced 5 cents to $3.20 after exchanging 1,000 shares. Scotiabank fell 30 cents to $58.60 in trading 12,000 stock units, Trinidad & Tobago NGL lost 3 cents in closing at $17.73, with 5,549 stocks clearing the market, Trinidad Cement exchanged 109 units at $3.90. Unilever Caribbean climbed 14 cents to $16.40 with an exchange of 7,900 stock units and West Indian Tobacco remained at $31.50, trading 200 shares.

Guardian Media spiked 39 cents to $3.03 while exchanging 10,000 shares, JMMB Group shed 14 cents to close at $2.16 in exchanging 62,318 stock units. Massy Holdings rose 74 cents to $82.75 in switching ownership of 49,914 stock units, National Enterprises dropped 30 cents at $3.60 after 14,940 shares crossed the market, National Flour Mills added 1 cent in closing at $1.79, with 9 units changing hands. NCB Financial Group shed 36 cents to $7.99, with 229,406 stocks clearing the market, Prestige Holdings remained unchanged at $7 after 2,460 stocks crossed the exchange, Republic Financial Holdings remained at $135.48, with 17,318 shares changing hands. Scotiabank dropped 10 cents to end at $58.90, with 837 stock units crossing the market, Trinidad & Tobago NGL close at $17.76 in exchanging 5,671 units, Trinidad Cement declined 6 cents to $3.90 in trading 2,531 shares and West Indian Tobacco fell 50 cents to $31.50, with 7,298 units clearing the market.

Guardian Media spiked 39 cents to $3.03 while exchanging 10,000 shares, JMMB Group shed 14 cents to close at $2.16 in exchanging 62,318 stock units. Massy Holdings rose 74 cents to $82.75 in switching ownership of 49,914 stock units, National Enterprises dropped 30 cents at $3.60 after 14,940 shares crossed the market, National Flour Mills added 1 cent in closing at $1.79, with 9 units changing hands. NCB Financial Group shed 36 cents to $7.99, with 229,406 stocks clearing the market, Prestige Holdings remained unchanged at $7 after 2,460 stocks crossed the exchange, Republic Financial Holdings remained at $135.48, with 17,318 shares changing hands. Scotiabank dropped 10 cents to end at $58.90, with 837 stock units crossing the market, Trinidad & Tobago NGL close at $17.76 in exchanging 5,671 units, Trinidad Cement declined 6 cents to $3.90 in trading 2,531 shares and West Indian Tobacco fell 50 cents to $31.50, with 7,298 units clearing the market. At the close, 18 securities traded, up from 14 on Monday, with five stocks rising, seven declining and six closing unchanged. One stock closed at a 52 weeks’ low.

At the close, 18 securities traded, up from 14 on Monday, with five stocks rising, seven declining and six closing unchanged. One stock closed at a 52 weeks’ low. First Citizens Bank traded 2,000 stocks unchanged at $50.50, GraceKennedy rose 2 cents to $6.32, with 32,913 units changing hands, Guardian Holdings rallied 25 cents to $32.90 in exchanging 10,299 stocks. Guardian Media lost 46 cents to close at a 52 weeks’ low of $2.64 in swapping 1,333 shares, JMMB Group popped 5 cents to $2.30 after trading 33,086 stock units, Massy Holdings dropped $2.99 in closing at $82.01 in swapping of 781 stock units. National Flour Mills fell 12 cents to $1.78 while exchanging 4,115 units, NCB Financial Group remained at $8.35 after trading 5,988 shares, Point Lisas exchanged 2,900 stocks at $3.15, Prestige Holdings shed 40 cents to close at $7 after exchanging 1,800 stock, Republic Financial Holdings rose 3 cents to $135.48 in an exchange of 112 stock units, Scotiabank remained at $59 in trading 4,121 units. Trinidad & Tobago NGL shed 24 cents in ending at $17.76, with 9,390 shares clearing the market, Unilever Caribbean declined 14 cents to $16.26, with 737 units changing hands and West Indian Tobacco gained 35 cents to end at $32 in exchanging 6,205 shares.

First Citizens Bank traded 2,000 stocks unchanged at $50.50, GraceKennedy rose 2 cents to $6.32, with 32,913 units changing hands, Guardian Holdings rallied 25 cents to $32.90 in exchanging 10,299 stocks. Guardian Media lost 46 cents to close at a 52 weeks’ low of $2.64 in swapping 1,333 shares, JMMB Group popped 5 cents to $2.30 after trading 33,086 stock units, Massy Holdings dropped $2.99 in closing at $82.01 in swapping of 781 stock units. National Flour Mills fell 12 cents to $1.78 while exchanging 4,115 units, NCB Financial Group remained at $8.35 after trading 5,988 shares, Point Lisas exchanged 2,900 stocks at $3.15, Prestige Holdings shed 40 cents to close at $7 after exchanging 1,800 stock, Republic Financial Holdings rose 3 cents to $135.48 in an exchange of 112 stock units, Scotiabank remained at $59 in trading 4,121 units. Trinidad & Tobago NGL shed 24 cents in ending at $17.76, with 9,390 shares clearing the market, Unilever Caribbean declined 14 cents to $16.26, with 737 units changing hands and West Indian Tobacco gained 35 cents to end at $32 in exchanging 6,205 shares. First Citizens Bank spiked 30 cents to $50.50 after finishing trading 432 stocks, GraceKennedy remained unchanged at $6.30 in exchanging 65,925 shares. Guardian Holdings remained at $32.65, with 800 units crossing the exchange, L.J Williams B share ended unchanged at $1.35 in trading 3,426 stock units. NCB Financial Group rallied 36 cents to $8.35 after an exchange of 320 shares. One Caribbean Media rose 59 cents to $4.84 with an exchange of 36,500 stocks, Point Lisas ended trading 10,142 units at $3.15, Republic Financial Holdings declined 49 cents to $135.45, with 862 stock units changing hands. Scotiabank popped 3 cents in closing at $59 with the swapping of 6,471 units and West Indian Tobacco slipped 35 cents to $31.65 after exchanging 125 shares.

First Citizens Bank spiked 30 cents to $50.50 after finishing trading 432 stocks, GraceKennedy remained unchanged at $6.30 in exchanging 65,925 shares. Guardian Holdings remained at $32.65, with 800 units crossing the exchange, L.J Williams B share ended unchanged at $1.35 in trading 3,426 stock units. NCB Financial Group rallied 36 cents to $8.35 after an exchange of 320 shares. One Caribbean Media rose 59 cents to $4.84 with an exchange of 36,500 stocks, Point Lisas ended trading 10,142 units at $3.15, Republic Financial Holdings declined 49 cents to $135.45, with 862 stock units changing hands. Scotiabank popped 3 cents in closing at $59 with the swapping of 6,471 units and West Indian Tobacco slipped 35 cents to $31.65 after exchanging 125 shares.