Caribbean Cream reported revenues of $646 million for the August quarter this year versus $645 million in 2022, with the year to date revenues slipping to $1.25 billion from $1.257 billion in the previous year. Profit fell to $3.6 million in the August quarter from $7 million in 2022 and rose to $10 million for the six months from $8.5 million in 2022.

Caribbean Cream Kingston outlet

Improvement in production cost pushed gross profit up 10 percent to $390 million for the half year versus $354 million in 2022 and $205 million for the quarter to August this year, up 8.5 percent from $189 million in 2022. Cost savings were only realised in some areas as administrative expenses and finance costs climbed over 2022. Administrative expenses increased 6 percent to $158 million from $149 million, with finance costs climbing 60 percent to $24 million, from $15 million in the August 2022 quarter. For the half year, administrative costs rose 7 percent to $306 million from $286 million the previous year, while finance costs jumped 56 percent from $27 million to $42 million for the half year.

Finance cost associated with the expansion of the warehouse and building out of the cogeneration energy plant is being written off directly as a current expense rather than capitalising it, with the equipment as such, the reported profit over the past three years appears understated as a result of the treatment of this item. Accordingly, the 2023 full year’s profit should be closer to $70 to $80 million than the above figure, and the 2023 half year’s figure should be around $37 million.

Operations generated Gross cash flow of $77 million, growth in working capital and $206 million spent in addition to fixed assets offset by loan inflows net of outflows of $238 million, resulting in funds growing by $78 million during the six months.

Considerable sums have been spent on plant and machinery to improve efficiency and, by extension, increase profit. Accordingly, $439 million was expended over the past year, bringing the gross amount in fixed assets to $2.7 billion from $1.7 billion at the end of February 2022. Most of the new expenditure went into equipping a new cold storage plant that has expanded freezing and cold storage capacity, with some spent on the cogeneration energy plant, which is intended to cut energy costs.

Considerable sums have been spent on plant and machinery to improve efficiency and, by extension, increase profit. Accordingly, $439 million was expended over the past year, bringing the gross amount in fixed assets to $2.7 billion from $1.7 billion at the end of February 2022. Most of the new expenditure went into equipping a new cold storage plant that has expanded freezing and cold storage capacity, with some spent on the cogeneration energy plant, which is intended to cut energy costs.

The company remains financially healthy, with current assets of $539 million, including trade and other receivables of $114 million, cash and bank balances of $145 million and inventories of $248 million, up from $183 million in August 2022. Current liabilities ended at $225 million and net current assets at $314 million.

At the end of August, shareholders’ equity amounts to $836 million, a rise from $807 million at the end of August 2022, with long term borrowings at $1.2 billion and short term loans at $43 million.

Earnings per share for the quarter was one cent and 3 cents for the year to date. IC Insider.com computation projects earnings of 55 cents per share for the fiscal year ending February 2024, with a PE of 7 times current year’s earnings based on the price of $3.95 the stock traded at on the Jamaica Stock Exchange Junior Market on Friday. The PE ratio compared with a market average of 10.7. Net asset value ended the period at $2.21, with the stock selling at just under two times book value.

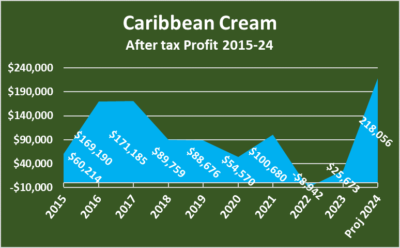

The company has a checkered profit history, as shown by the attached chart of profits, since 2015 and has struggled with increased costs since the disruption caused by COVID-19. The situation is worsened by the treatment of interest incurred to finance the new warehouse.

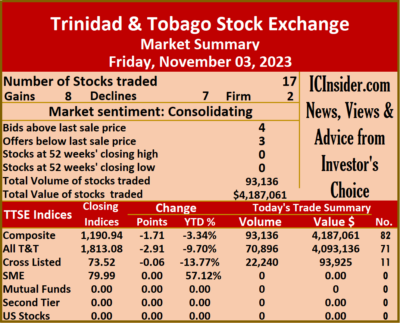

Investors exchanged 93,136 shares for $4,187,061 versus 136,107 stock units at $2,400,320 on Thursday.

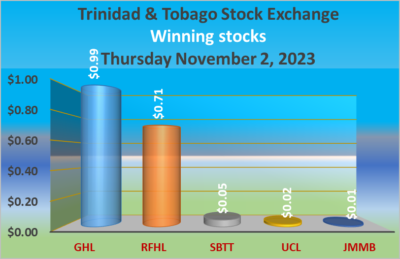

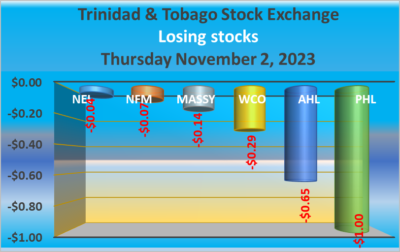

Investors exchanged 93,136 shares for $4,187,061 versus 136,107 stock units at $2,400,320 on Thursday. First Citizens Group popped 10 cents to close trading at $49.35 with an exchange of 1,752 stocks, FirstCaribbean International Bank ended at $7 in the trading of 11,187 units, Guardian Holdings declined 19 cents to close at $19.80 with shareholders swapping 190 stocks. JMMB Group shed 1 cent to close at $1.41 as investors exchanged 11,050 shares, Massy Holdings advanced 14 cents and ended at $4.59 after 19,098 stock units passed through the market, National Enterprises rose 4 cents in closing at $3.55 after an exchange of 5,029 shares. NCB Financial remained at $2.84 with investors transferring three stock units, One Caribbean Media dropped 29 cents in closing at $3.60 in switching ownership of 2,598 stocks,

First Citizens Group popped 10 cents to close trading at $49.35 with an exchange of 1,752 stocks, FirstCaribbean International Bank ended at $7 in the trading of 11,187 units, Guardian Holdings declined 19 cents to close at $19.80 with shareholders swapping 190 stocks. JMMB Group shed 1 cent to close at $1.41 as investors exchanged 11,050 shares, Massy Holdings advanced 14 cents and ended at $4.59 after 19,098 stock units passed through the market, National Enterprises rose 4 cents in closing at $3.55 after an exchange of 5,029 shares. NCB Financial remained at $2.84 with investors transferring three stock units, One Caribbean Media dropped 29 cents in closing at $3.60 in switching ownership of 2,598 stocks,  Prestige Holdings climbed 50 cents to $11, with 199 units clearing the market. Republic Financial increased $1 and ended at $120 in an exchange of 30,355 stocks, Scotiabank slipped 5 cents to close at $72.60 with investors dealing in 817 units, Trinidad & Tobago NGL gained $1.45 to end at $13.95 after 5,564 shares crossed the exchange. Unilever Caribbean rallied 86 cents to $11.48 after a transfer of 2,111 stock units and West Indian Tobacco increased 29 cents to close at $10.30, with stakeholders exchanging 1,824 shares.

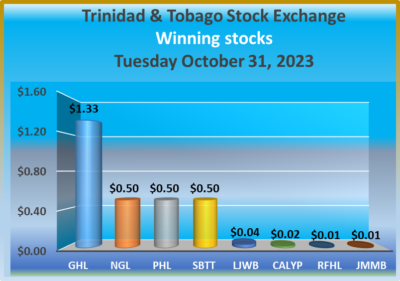

Prestige Holdings climbed 50 cents to $11, with 199 units clearing the market. Republic Financial increased $1 and ended at $120 in an exchange of 30,355 stocks, Scotiabank slipped 5 cents to close at $72.60 with investors dealing in 817 units, Trinidad & Tobago NGL gained $1.45 to end at $13.95 after 5,564 shares crossed the exchange. Unilever Caribbean rallied 86 cents to $11.48 after a transfer of 2,111 stock units and West Indian Tobacco increased 29 cents to close at $10.30, with stakeholders exchanging 1,824 shares. The company operates a restaurant solely in the Turks and Caicos Islands, and delivered revenues of US$1.8 million in the August 2023 quarter, up 27 percent from US$1.42 million in the prior year and produced gross profit of $1.33 billion this year versus US$1.033 million in the previous year.

The company operates a restaurant solely in the Turks and Caicos Islands, and delivered revenues of US$1.8 million in the August 2023 quarter, up 27 percent from US$1.42 million in the prior year and produced gross profit of $1.33 billion this year versus US$1.033 million in the previous year.

Investors exchanged 136,107 shares for $2,400,320 versus 310,882 stock units at $1,784,800 on Wednesday.

Investors exchanged 136,107 shares for $2,400,320 versus 310,882 stock units at $1,784,800 on Wednesday. Endeavour Holdings remained at $15 after a transfer of 50 stock units, First Citizens Group ended at $49.25, with 4,188 shares changing hands, GraceKennedy remained at $3.40 with investors trading 350 units. Guardian Holdings advanced 99 cents to end at $19.99 in switching the ownership of 7,796 stocks, JMMB Group popped 1 cent in closing at $1.42 as investors exchanged 475 stock units, L.J. Williams B share ended at $2.40 after two shares crossed the market. Massy Holdings lost 14 cents and ended at $4.45 with an exchange of 79,939 stock units, National Enterprises declined 4 cents to $3.51, with 7,787 stocks clearing the market, National Flour Mills fell 7 cents to close at $1.53 with traders dealing in 2,001 units.

Endeavour Holdings remained at $15 after a transfer of 50 stock units, First Citizens Group ended at $49.25, with 4,188 shares changing hands, GraceKennedy remained at $3.40 with investors trading 350 units. Guardian Holdings advanced 99 cents to end at $19.99 in switching the ownership of 7,796 stocks, JMMB Group popped 1 cent in closing at $1.42 as investors exchanged 475 stock units, L.J. Williams B share ended at $2.40 after two shares crossed the market. Massy Holdings lost 14 cents and ended at $4.45 with an exchange of 79,939 stock units, National Enterprises declined 4 cents to $3.51, with 7,787 stocks clearing the market, National Flour Mills fell 7 cents to close at $1.53 with traders dealing in 2,001 units.  NCB Financial remained at $2.84 in an exchange of 7 shares, Prestige Holdings skidded $1 in closing at $10.50 with investors dealing in 4,068 units, Republic Financial increased 71 cents to end at $119, with 2,541 stocks crossing the exchange. Scotiabank climbed 5 cents to $72.65 in trading 14,657 stock units, Trinidad & Tobago NGL ended at $12.50 with shareholders swapping 1,430 shares, Unilever Caribbean rose 2 cents in closing at $10.62 in an exchange of 906 units and West Indian Tobacco dropped 29 cents to end at a 52 weeks’ low of $10.01 after 300 stocks passed through the market.

NCB Financial remained at $2.84 in an exchange of 7 shares, Prestige Holdings skidded $1 in closing at $10.50 with investors dealing in 4,068 units, Republic Financial increased 71 cents to end at $119, with 2,541 stocks crossing the exchange. Scotiabank climbed 5 cents to $72.65 in trading 14,657 stock units, Trinidad & Tobago NGL ended at $12.50 with shareholders swapping 1,430 shares, Unilever Caribbean rose 2 cents in closing at $10.62 in an exchange of 906 units and West Indian Tobacco dropped 29 cents to end at a 52 weeks’ low of $10.01 after 300 stocks passed through the market. Investors exchanged 310,882 shares for $1,784,800 versus 282,937 stock units at $2,364,755 on Tuesday.

Investors exchanged 310,882 shares for $1,784,800 versus 282,937 stock units at $2,364,755 on Tuesday. First Citizens Group remained at $49.25 in trading 210 stocks, FirstCaribbean Bank increased 25 cents to close at $7 after a transfer of 25,000 shares, GraceKennedy popped 1 cent to close at $3.40 in switching ownership of 68,412 stocks. Guardian Holdings declined 99 cents and ended at $19 after an exchange of 56 stock units, Guardian Media gained 19 cents in closing at $2.20, with 800 stock units changing hands, L.J. Williams B share rose 1 cent to close at $2.40 after 94 shares crossed the exchange. Massy Holdings lost 1 cent to end at $4.59 with traders dealing in 50,442 stocks, National Enterprises advanced 4 cents in closing at $3.55 while exchanging 302 units, National Flour Mills dipped 3 cents to $1.60 with investors swapping 830 stock units. NCB Financial ended at $2.84 after an exchange of 137,593 shares, Prestige Holdings remained at $11.50 after 14,316 stock units crossed the market, Republic Financial fell 46 cents to end at $118.29 with an exchange of 3,803 units.

First Citizens Group remained at $49.25 in trading 210 stocks, FirstCaribbean Bank increased 25 cents to close at $7 after a transfer of 25,000 shares, GraceKennedy popped 1 cent to close at $3.40 in switching ownership of 68,412 stocks. Guardian Holdings declined 99 cents and ended at $19 after an exchange of 56 stock units, Guardian Media gained 19 cents in closing at $2.20, with 800 stock units changing hands, L.J. Williams B share rose 1 cent to close at $2.40 after 94 shares crossed the exchange. Massy Holdings lost 1 cent to end at $4.59 with traders dealing in 50,442 stocks, National Enterprises advanced 4 cents in closing at $3.55 while exchanging 302 units, National Flour Mills dipped 3 cents to $1.60 with investors swapping 830 stock units. NCB Financial ended at $2.84 after an exchange of 137,593 shares, Prestige Holdings remained at $11.50 after 14,316 stock units crossed the market, Republic Financial fell 46 cents to end at $118.29 with an exchange of 3,803 units.  Scotiabank rallied 9 cents to $72.60 after investors ended trading 738 stocks, Trinidad & Tobago NGL rose $1 to $12.50 with an exchange of 5,242 units, Trinidad Cement skidded 3 cents to close at $2.90 and closed with an exchange of 1,254 stocks. Unilever Caribbean remained at $10.60 with investors transferring 1,251 shares and West Indian Tobacco dipped 1 cent to end at a 52 weeks’ low of $10.30, with 358 stock units crossing the market.

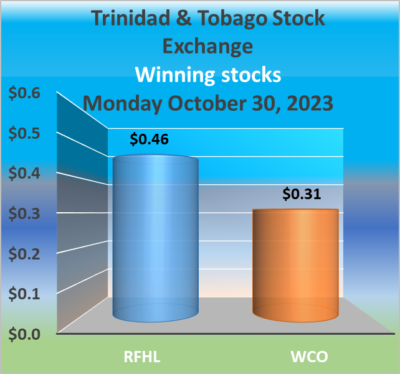

Scotiabank rallied 9 cents to $72.60 after investors ended trading 738 stocks, Trinidad & Tobago NGL rose $1 to $12.50 with an exchange of 5,242 units, Trinidad Cement skidded 3 cents to close at $2.90 and closed with an exchange of 1,254 stocks. Unilever Caribbean remained at $10.60 with investors transferring 1,251 shares and West Indian Tobacco dipped 1 cent to end at a 52 weeks’ low of $10.30, with 358 stock units crossing the market. Investors exchanged 282,937 shares for $2,364,755 versus 234,948 stock units at $1,661,450 on Monday.

Investors exchanged 282,937 shares for $2,364,755 versus 234,948 stock units at $1,661,450 on Monday. At the close, Agostini’s shed $2.50 to end at $65 with investors trading 2,253 shares, Calypso Macro Investment Fund rallied 2 cents in closing at $22.52 after 20,000 stocks passed through the market, First Citizens Group fell 20 cents to end at $49.25 after 3,211 shares were traded. FirstCaribbean International Bank dipped 25 cents to close at $6.75 in an exchange of 1,304 stock units, GraceKennedy ended at $3.39 with shareholders swapping 8,800 shares, Guardian Holdings popped $1.33 to $19.99 after an exchange of a mere one unit. JMMB Group gained 1 cent to end at $1.41 in trading 46,700 stocks, L.J. Williams B share rose 4 cents in closing at $2.39, with 1,000 stock units crossing the market, Massy Holdings lost 1 cent and ended at $4.60 with an exchange of 168,455 shares. National Enterprises remained at $3.51, with 51 stock units crossing the market, National Flour Mills remained at $1.63 in an exchange of 50 stocks, One Caribbean Media ended at $3.89 after an exchange of 50 units.

At the close, Agostini’s shed $2.50 to end at $65 with investors trading 2,253 shares, Calypso Macro Investment Fund rallied 2 cents in closing at $22.52 after 20,000 stocks passed through the market, First Citizens Group fell 20 cents to end at $49.25 after 3,211 shares were traded. FirstCaribbean International Bank dipped 25 cents to close at $6.75 in an exchange of 1,304 stock units, GraceKennedy ended at $3.39 with shareholders swapping 8,800 shares, Guardian Holdings popped $1.33 to $19.99 after an exchange of a mere one unit. JMMB Group gained 1 cent to end at $1.41 in trading 46,700 stocks, L.J. Williams B share rose 4 cents in closing at $2.39, with 1,000 stock units crossing the market, Massy Holdings lost 1 cent and ended at $4.60 with an exchange of 168,455 shares. National Enterprises remained at $3.51, with 51 stock units crossing the market, National Flour Mills remained at $1.63 in an exchange of 50 stocks, One Caribbean Media ended at $3.89 after an exchange of 50 units.  Prestige Holdings climbed 50 cents in closing at $11.50 with investors dealing in 14 shares, Republic Financial increased 1 cent to end at $118.75 after a transfer of 3,716 units, Scotiabank advanced 50 cents to close at $72.51 with investors exchanging 168 stocks. Trinidad & Tobago NGL popped 50 cents to $11.50 with a transfer of 20,067 stock units, Trinidad Cement dropped 2 cents to end at $2.93 as investors exchanged 3,191 shares, Unilever Caribbean remained at $10.60 in switching ownership of 3,421 stocks and West Indian Tobacco ended at $10.31 with traders dealing in 485 units.

Prestige Holdings climbed 50 cents in closing at $11.50 with investors dealing in 14 shares, Republic Financial increased 1 cent to end at $118.75 after a transfer of 3,716 units, Scotiabank advanced 50 cents to close at $72.51 with investors exchanging 168 stocks. Trinidad & Tobago NGL popped 50 cents to $11.50 with a transfer of 20,067 stock units, Trinidad Cement dropped 2 cents to end at $2.93 as investors exchanged 3,191 shares, Unilever Caribbean remained at $10.60 in switching ownership of 3,421 stocks and West Indian Tobacco ended at $10.31 with traders dealing in 485 units. Investors exchanged 234,948 shares for $1,661,450, down from 1,423,065 stock units at $13,187,235 on Friday.

Investors exchanged 234,948 shares for $1,661,450, down from 1,423,065 stock units at $13,187,235 on Friday. At the close, Agostini’s ended at $67.50 with shareholders swapping 88 units, First Citizens Group declined 55 cents to end at $49.45, with 989 stock units traded, FirstCaribbean International Bank ended at $7 with investors trading 3,802 shares, GraceKennedy ended trading of 109,377 stock units at $3.39. Guardian Holdings lost $1.34 to close at $18.66 with traders dealing in 600 shares, L.J. Williams B share dipped 4 cents to $2.35 in an exchange of 830 units, Massy Holdings fell 7 cents in closing at $4.61 after 10,784 stocks passed through the market. National Enterprises ended at $3.51 in trading 2,852 stock units, NCB Financial ended at $2.84 after exchanging 75,568 shares, One Caribbean Media skidded 4 cents to close at $3.89, with 250 stock units crossing the market. Point Lisas remained at $3.50 in an exchange of 1,137 units,

At the close, Agostini’s ended at $67.50 with shareholders swapping 88 units, First Citizens Group declined 55 cents to end at $49.45, with 989 stock units traded, FirstCaribbean International Bank ended at $7 with investors trading 3,802 shares, GraceKennedy ended trading of 109,377 stock units at $3.39. Guardian Holdings lost $1.34 to close at $18.66 with traders dealing in 600 shares, L.J. Williams B share dipped 4 cents to $2.35 in an exchange of 830 units, Massy Holdings fell 7 cents in closing at $4.61 after 10,784 stocks passed through the market. National Enterprises ended at $3.51 in trading 2,852 stock units, NCB Financial ended at $2.84 after exchanging 75,568 shares, One Caribbean Media skidded 4 cents to close at $3.89, with 250 stock units crossing the market. Point Lisas remained at $3.50 in an exchange of 1,137 units, Prestige Holdings ended at $11, with 4,086 stocks passing through the market, Republic Financial rose 46 cents in closing at $118.74 after a transfer of 4,340 shares. Scotiabank shed 74 cents to close at $72.01, with 3,663 stock units crossing the exchange, Trinidad & Tobago NGL remained at $11 with investors dealing in 1,430 stocks, Trinidad Cement ended at $2.95 while exchanging 11,000 units. Unilever Caribbean dived 89 cents to end at a 52 weeks’ low of $10.60, with investors transferring 4,132 stocks and West Indian Tobacco rallied 31 cents to close at $10.31 after an exchange of 20 units.

Prestige Holdings ended at $11, with 4,086 stocks passing through the market, Republic Financial rose 46 cents in closing at $118.74 after a transfer of 4,340 shares. Scotiabank shed 74 cents to close at $72.01, with 3,663 stock units crossing the exchange, Trinidad & Tobago NGL remained at $11 with investors dealing in 1,430 stocks, Trinidad Cement ended at $2.95 while exchanging 11,000 units. Unilever Caribbean dived 89 cents to end at a 52 weeks’ low of $10.60, with investors transferring 4,132 stocks and West Indian Tobacco rallied 31 cents to close at $10.31 after an exchange of 20 units. Earnings per share for the quarter was $2.28, up from $1.42 in 2022 and $5.15 versus $5 for the year to September.

Earnings per share for the quarter was $2.28, up from $1.42 in 2022 and $5.15 versus $5 for the year to September. In relation to the cash flows, “Net cash provided by operating activities” was $5.7 billion for the nine months and $2.46 billion for the quarter. The cash flow generation during the quarter and the available cash at the beginning of the period have allowed the Group to invest $4 billion during the nine months of the year and $2 billion during the second quarter, leaving the company with $639 million in cash and bank balance at the end of the period.

In relation to the cash flows, “Net cash provided by operating activities” was $5.7 billion for the nine months and $2.46 billion for the quarter. The cash flow generation during the quarter and the available cash at the beginning of the period have allowed the Group to invest $4 billion during the nine months of the year and $2 billion during the second quarter, leaving the company with $639 million in cash and bank balance at the end of the period.

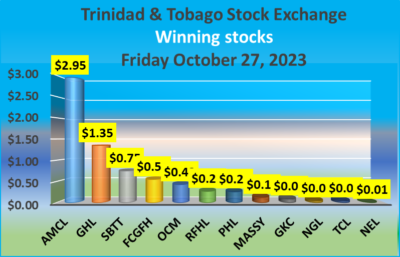

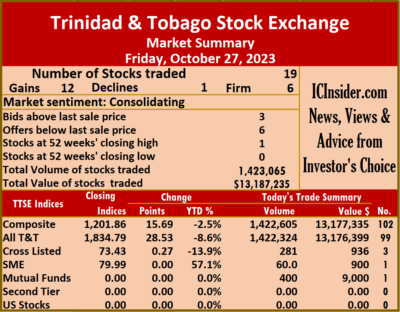

Investors exchanged a total of 1,423,065 shares for $13,187,235, up sharply from 320,823 stock units at $2,253,057 on Thursday.

Investors exchanged a total of 1,423,065 shares for $13,187,235, up sharply from 320,823 stock units at $2,253,057 on Thursday. At the close, Ansa McAl popped $2.95 to close at $57, with a mere 11 stock units crossing the market, Ansa Merchant Bank ended at $42.12, with investors trading just two shares, Calypso Macro Investment Fund ended at $22.50 after 400 stock units passed through the market, Endeavour Holdings remained at $15 in an exchange of 60 stocks. First Citizens Group rallied 55 cents and ended at $50, with 4,572 stocks being traded, GraceKennedy rose 9 cents to end at $3.39 with investors dealing in 251 units. Guardian Holdings advanced $1.35 in closing at $20 in an exchange of 100 stocks, Massy Holdings increased 13 cents to $4.68 and closed after an exchange of 1,351,960 units, National Enterprises popped 1 cent and ended at $3.51 with stakeholders trading 3,648 shares, National Flour Mills remained at $1.63 with a transfer of 200 stock units. NCB Financial ended at $2.84, with 30 shares crossing the market, One Caribbean Media gained 43 cents to close at $3.93 with investors transferring 1,000 units, Prestige Holdings popped 26 cents to close at a 52 weeks’ high of $11, with 1,560 stocks changing hands,

At the close, Ansa McAl popped $2.95 to close at $57, with a mere 11 stock units crossing the market, Ansa Merchant Bank ended at $42.12, with investors trading just two shares, Calypso Macro Investment Fund ended at $22.50 after 400 stock units passed through the market, Endeavour Holdings remained at $15 in an exchange of 60 stocks. First Citizens Group rallied 55 cents and ended at $50, with 4,572 stocks being traded, GraceKennedy rose 9 cents to end at $3.39 with investors dealing in 251 units. Guardian Holdings advanced $1.35 in closing at $20 in an exchange of 100 stocks, Massy Holdings increased 13 cents to $4.68 and closed after an exchange of 1,351,960 units, National Enterprises popped 1 cent and ended at $3.51 with stakeholders trading 3,648 shares, National Flour Mills remained at $1.63 with a transfer of 200 stock units. NCB Financial ended at $2.84, with 30 shares crossing the market, One Caribbean Media gained 43 cents to close at $3.93 with investors transferring 1,000 units, Prestige Holdings popped 26 cents to close at a 52 weeks’ high of $11, with 1,560 stocks changing hands,  Republic Financial advanced 27 cents in closing at $118.28 after a transfer of 52,557 stock units. Scotiabank rose 75 cents and ended at $72.75 as investors exchanged 3,549 shares, Trinidad & Tobago NGL rose 5 cents to end at $11 in trading 1,180 stocks, Trinidad Cement increased 5 cents to close at $2.95 after exchanging 25 units. Unilever Caribbean lost 5 cents to close at $11.49 with shareholders swapping 30 stock units and West Indian Tobacco remained at $10 while exchanging 1,930 shares.

Republic Financial advanced 27 cents in closing at $118.28 after a transfer of 52,557 stock units. Scotiabank rose 75 cents and ended at $72.75 as investors exchanged 3,549 shares, Trinidad & Tobago NGL rose 5 cents to end at $11 in trading 1,180 stocks, Trinidad Cement increased 5 cents to close at $2.95 after exchanging 25 units. Unilever Caribbean lost 5 cents to close at $11.49 with shareholders swapping 30 stock units and West Indian Tobacco remained at $10 while exchanging 1,930 shares.