The allocation formula for the recent Initial public offering of tTech shares which closed shortly after opening on Wednesday with more than 300 percent over subscription, should be known by Monday coming.

The allocation formula for the recent Initial public offering of tTech shares which closed shortly after opening on Wednesday with more than 300 percent over subscription, should be known by Monday coming.

The likely date was obtained by IC Insider today from a spokesperson at NCB Capital Markets. The recommended formula has been passed on to the company for the approval the spoke person stated. tTech offered more than 25.65 million shares for purchase up to $2.50 each and was well received by investors raising over $50 million that they went to the market.

The spokesperson also indicated that they will be looking into the matter of investor being asked to pay the central depository fee, although it was not included in the prospectus.

tTech allocation by Monday

December 18, 2015 by

tTech IPO JCSD fee breaches prospectus terms

December 17, 2015 by

NCB Capital Markets imposes cess on tTech investors in breach prospectus terms.

The imposition of JCSD processing fee is not only untidy, it is in breach of the terms of the prospectus and must be returned to those investors who paid it. There are no references to JCSD processing fee in the prospectus and under the heading of Statutory and General Information items 6 of the prospectus states, “All Applicants (including Reserved Share Applicants) will be required to pay in full the Subscription Price of $2.50 per Share, subject to discounts, where applicable. No further sum will be payable on allotment”. Most junior market IPOs, are highly anticipated, with several issues closing shortly after opening, leading most investors to apply for shares ahead of the opening day and so ensure that their application are on a timely basis. On Tuesday ahead of the opening of the tTech issue, a statement appeared on the website of the Jamaica Stock Exchange, to indicate that the “application form found in Appendix 1 of IPO Prospectus did not include any mention of the JCSD processing fee of J$134.00 (inclusive of GCT) that each application would be subject to. As such, the application form has been updated to include such commentary”.

Most persons would not have been aware of the charge and so put in their applications without it while some included it, having seen the change. This places some applicants at a disadvantage small though it may be. Some investors are shocked that, the company and the broker did not absorb the charge for the cess and that the Financial Services Commission and the Jamaica Stock Exchange have permitted the late imposition of it. The charging of the JCSD processing fee inclusive of GCT is an irritant for investors and there are few solid reasons why companies are not treating the cess as a part of the cost of listing rather than asking investors to pay for it directly.

Over 300% over the top for tTech

December 16, 2015 by

The latest entrant to seek junior market listing, tTech Limited is reporting a successful initial public offering. The issue officially opened at 9 on Wednesday morning and should have closed on December 18, 2015.

Edward Alexander CEO of the company informed the IC Insider that at 8 am the report from NCB Capital Markets the brokers to the deal had the level of over subscription at more than 300 percent with more applications coming in after. Reports to IC Insider indicated that the level of subscription was in excess of the offering at mid-day on Tuesday. The offering was for 25.65 million shares to raise $50,263,900.

Alexander disclosed that tTech picked up additional clients and garnered more business from existing ones after the IPO was priced.

At the same time the offering of CAC 2000 Limited was still open around 3 pm on the opening day but our informed source suggests that it could well be closed off before the day ends or by Thursday. The feedback is that the 2016 fiscal year should see increased revenues and profits from ongoing contracts and new ones. The issue is expected to raise $120,545,327 from 29 million shares on offer up $4.85 each. VM Wealth Management are the brokers to the CAC issue.

CAC 2000 not priced to bounce

December 10, 2015 by

Add your HTML code here...

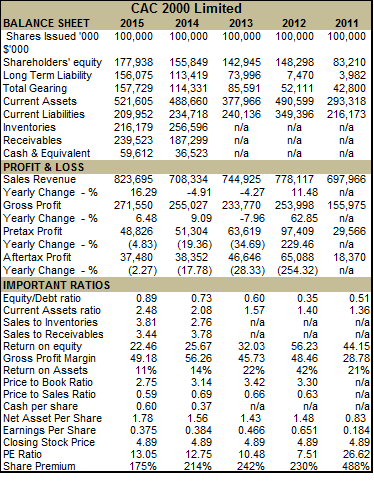

![]() CAC 2000 Limited is offering 29,032,258 ordinary shares to the public next starting Wednesday December 16, at $4.89 each. The price values the company at a PE of 10 based on full year results to July this year. There is no room for a bounce with junior market stocks priced at an average PE of 8.4 with 7 stocks selling above CAC’s valuation.

CAC 2000 Limited is offering 29,032,258 ordinary shares to the public next starting Wednesday December 16, at $4.89 each. The price values the company at a PE of 10 based on full year results to July this year. There is no room for a bounce with junior market stocks priced at an average PE of 8.4 with 7 stocks selling above CAC’s valuation.

A total of 14,516,129 shares are reserved for priority share applicants. The issue is expected to raise $120,545,327 to inject additional working capital into its operations, to allow it to increase its ability to take on new business.

Earnings before tax of $49 million, was achieved for the year to July 2015, from revenues of $824 million, with earnings per share of 48.8 cents, putting the PE ratio at 10. In 2014 revenues were $708 million and pretax profit at $51 million. The of listing of the shares on the junior market, will result in tax free status for 5 years making the use of the pretax earnings, the appropriate figure to use in computing the value of the shares.

Steven Marston,

Chief Executive Officer

The company was incorporated in Jamaica in July 2000, and is a provider of commercial Air Conditioning systems and refrigeration and energy solutions in Jamaica, with a share of the residential market. The Company sells, services and supports the air conditioning systems in Jamaica.

The minimum amount to be raised is $50 million as a result, if this threshold is not attained, the company will not make an application for the shares to be admitted to the Junior Market and all funds will be returned.

Currently, there are 100 million issued ordinary shares and 148,037,000 variable rate cumulative redeemable preference shares maturing July 2018. The redeemable preference shares attracts dividends of 10 percent per annum for the first year and thereafter a variable rate of 2.5 percentage points above the weighted average yield rate applicable to the six months Jamaica Treasury Bill Tender, held immediately prior to the commencement of each quarterly interest period until maturity.

There have been no six months treasuries but with the 90 days bill rate being just over 6 percent interest cost going forward should be around 8.5 percent.

There have been no six months treasuries but with the 90 days bill rate being just over 6 percent interest cost going forward should be around 8.5 percent.Some positives of the company include the fact that the current owners and CEO have strong engineering backgrounds, and should know their business. Their expertise should help growth in new related areas of business. There is the potential to expand to other engineering services including alternative energy and into Mechanical, Electrical and Plumbing (MEP) contractor. On the negative front is an unsettled negligence claim against them and large blocks of revenues from large projects that could result in revenues being sporadic. The level of receivables is too high at 4 months on average, with large amounts due for over 4 months, a big negative, as it exposes the company to bad debts as well as the possibility of cutting off potential revenues. The level of inventories being carried is also high but may well be a product of a sliding Jamaican dollar.

The prospectus does not include the September quarter’s results that could shed light on what is currently happening. That is a negative as its absence suggest that it cannot help in selling the issue.

tTech is BUY RATED for strong growth

December 6, 2015 by

tTech is going to the capital market this month to raise approximately $50 million by the issuing for subscription 25,652,000 shares to the general public and special interest group with the general public being asked to pay $2.50 each for 16.4 million being made available to them.

IC Insider assessed the company’s record and forecast increased earnings for 2016 and 2016 and accorded it the BUY RATED honour.

Edward Alexander, Chief Executive Officer, in an interview with IC Insider stated that the staff of the company indicates that they will all be taking up their full allotment, if so there will be few of these shares available for the public to acquire at the IPO stage.

The Company was incorporated in Jamaica on December 1st, 2006, and is a managed information technology (“IT”) service provider, or what industry insiders refer to as a “Managed Services Provider”. That is, for the most part, the Company’s main service offering is the management of other businesses’ IT infrastructure remotely and on a pre-paid basis.

The company is growing at an attractive rate with revenues that are up 28 percent for the half year to June to $81.4 million versus expenses increasing 18 percent and only 14 percent when technical fees, services and products that are part of direct expenses are excluded.

From Left: Mr. Hugh Allen, Resolution Manager and Executive Director; Mrs. Natalya Petrekin, Service Desk

Manager; Mr. Norman Chen, Technical Services Director; Mr. John Gibson, Senior IT Security Officer; Mr.

Edward Alexander, CEO; Mrs. Hortense Gregory-Nelson, Finance and Administrative Manager; Mr. G.

Christopher Reckord, Sales and Marketing Director. Mr. Omar Bell.

IC Insiders’ forecast, based on continuation of good revenue growth, is for profit before tax for 2015 to end at $36 million or 45 cents per share and $27 million or 35 cents per share after tax and $64 million or 60 cents per share for 2016. This gives it a PE based on 2015 earnings before tax of 5.5 and for 2016 of 4 and compares with junior market stocks with PE of 8, with half of the market selling above the average, suggesting that the stock should enjoy a nice bounce over the next twelve months or less. The company has $51 million in cash and no borrowed funds with current liability of just $27 million, so why do they need to raise the funds? “Expansion into security services will require added equipment, software working capital for continued expansion” Alexander stated, in addition listing allows the staff to be part owners and benefit from future growth.

There are a number of positives for the company it is in a good growth industry with potential for regional expansion, the Grace Kennedy contract and relationship could provide them the experience to take on other large regional conglomerates. They are a service-based business with high gross profit margin which is a big positive and if growth continues at current levels would contribute to a big increase in profit. A lot of the business is recurring, providing stability to the operation. The founders’ vested interest will remain strong as they will still hold relatively large percentage of the company after the IPO.

There are a number of positives for the company it is in a good growth industry with potential for regional expansion, the Grace Kennedy contract and relationship could provide them the experience to take on other large regional conglomerates. They are a service-based business with high gross profit margin which is a big positive and if growth continues at current levels would contribute to a big increase in profit. A lot of the business is recurring, providing stability to the operation. The founders’ vested interest will remain strong as they will still hold relatively large percentage of the company after the IPO.Only about 15% shares being offered to the general public the stock almost guaranteeing that it will be in relatively short supply which could drive price up quickly after listing, this is especially so being the first tech company on the JSE.

Subscription opens at 9 am on December 16th, 2015 and closes at 4:30 p.m. on the December 18th, 2015, subject to the right of the Company to shorten or extend the time for closing. All completed Application Forms must be delivered to NCB Capital Markets.

tTech offer seems a buy

December 2, 2015 by

tTech a company most investors would hardly have heard about, will be going to the capital market this month, to raise approximately $50,263,900, by the issuing for subscription 25,652,000 ordinary shares to the general public and special persons related to the company at $2.50 each.

In reality only 16.4 million are allocated for the general public, a relatively small number. The Company that was formed in 2006 currently provides outsourced IT solutions to businesses currently in Jamaica. IC Insider’s preliminary assessment indicates earnings per share around 40 cents before taxation for a PE of 6.3 and would make the stock a buy.

The purpose of the offer is to provide working capital support to its operations and in order to allow the Company to augment its productive capacity and thereby to take advantage of new business opportunities as well as benefit from listing on the stock exchange and improve staff compensation by allowing them to buy the shares that are bound to increase sharply in price after listing.

The Company estimates that the expenses in the Invitation will not exceed $10 million. Subscription opens at 9 am on December 16th, 2015 and closes at 4:30 p.m. on the December 18th, 2015, subject to the right of the Company to shorten or extend the time for closing. If the Invitation is fully subscribed and is successful in raising $50,263,900, the Company will make an application to the JSE for the Shares to be admitted to the Junior Market. The company has been profitable with revenues growing at an attractive rate. The Company has adopted a dividend policy of paying 25 percent of profits each year.

All completed Application Forms must be delivered to NCB Capital Markets.

IC Insider will have a fuller report at a later date.

Sagicor rights grab $5.2b

September 7, 2015 by

Hilton Rose Hall -Sagicor X Fund recent acquisition

The additional shares were available to shareholders as shares over and above their provisional allotment. The funds received from the Rights Issue will be invested as equity in a new subsidiary, X Fund Properties LLC established in the USA. X Fund Properties LLC will purchase the DoubleTree Hilton at the Entrance to Universal in Orlando, Florida.

The DoubleTree by Hilton at the entrance to Universal is 742 guest rooms hotel with over 62,800 square feet of meeting and convention space. It is located in Orlando at the entrance to the Universal Theme Park. The purchase price for the Hotel is US$75 million. The balance of the purchase price is expected to be financed by a US institutional lender.

Notwithstanding, the overwhelming support the stock is overvalued at the right issue price of $6.95 each. Sagicor Real Estate Fund reported profit before taxation in the first quarter of $293 million from revenues of $1.19 billion, the net position in the June quarter was only $72 million from just $37 million less income from the hotel.

Investors grab Sagicor rights

August 24, 2015 by

Hilton Rose Hall Sagicor X Fund recent acquisition

These shares (“Up-sizable Shares”) are available to shareholders as additional shares over and above their provisional allotment.

Shareholders may apply for Up-sizable Shares at the rights issue price of J$6.95 per share in one of 2 ways: (a) by completing an Application for additional shares; or (b) by completing Box 5 in their Provisional Allotment Letter (in the case of shareholders who have not yet returned their Provisional Allotment Letter).

If the aggregate number of shares applied for from the Un-allocated Pool shall exceed the number of shares available in the Pool, then all applications will be scaled down pro rata.

The Rights Issue will close at 4:30 p.m. on September 2, 2015 – unless extended by the Directors.

The funds received from the Rights Issue will be invested as equity in a new subsidiary X Fund Properties LLC established in the USA. X Fund Properties LLC will purchase the DoubleTree Hilton at the Entrance to Universal in Orlando, Florida.

The DoubleTree by Hilton at the Entrance to Universal is 742 guest rooms (inclusive of 17 suites) hotel with over 62,800 square feet of meeting and convention space. It is located in Orlando at the entrance to the Universal Theme Park. The purchase price for the Hotel is US$75,000.000. The balance of the purchase price is expected to be financed by a US institutional lender.

Another IPO eyes on TTSE

June 11, 2015 by

Trinidad & Tobago Stock Exchange seems set to welcome another new listing later this year, if all goes well. According to reports out of the twin island state, the country’s Minister of Finance Howai said recently, the Phoenix Park Gas Processors initial public offering (IPO) will “come to market in the next few weeks” with some 75,852,000 shares for the public to purchase.

Trinidad & Tobago Stock Exchange seems set to welcome another new listing later this year, if all goes well. According to reports out of the twin island state, the country’s Minister of Finance Howai said recently, the Phoenix Park Gas Processors initial public offering (IPO) will “come to market in the next few weeks” with some 75,852,000 shares for the public to purchase.

According to the company’s website, “Phoenix Park Gas Processors Limited (PPGPL) is a Trinidad and Tobago company formed in May 1989” PPGPL is one of the largest gas processing facilities in the Americas. We provide natural gas of a high quality standard to our customer by processing raw, natural gas delivered to our facility from their existing natural gas pipeline system. Processing involves the extraction of natural gas liquids (NGLs). The natural gas is delivered by our customer to downstream facilities that use it as a fuel and feedstock. We also fractionate the extracted NGLs into three components: propane, butane and natural gasoline. The propane and butane are marketed in the Caribbean and Central America and the natural gasoline is marketed internationally.

In 2013, the government sold off a part of First Citizens Bank to the public, with the shares being listed on the Trinidad and Tobago Stock exchange, providing investors with a healthy profit from their purchase.

IS a PE of 13 right for Proven?

April 9, 2015 by

Proven Investments is accomplishing an unusual feat in the local stock market that not many person were attracted to last year when stocks were selling dirt-cheap.

Proven Investments is accomplishing an unusual feat in the local stock market that not many person were attracted to last year when stocks were selling dirt-cheap.

With the average PE of the market, around 5 times 2015 earnings, and with many blue chip stocks selling at no more than 7 times earnings, it is remarkable that Proven is getting strong demand for their rights issue with the company’s PE around 13 times 2015 earnings. Not surprisingly the directors have agreed to the issue being increased over the initial level of 122,896,618 shares with option for an equivalent amount now sanctioned, in keeping with the term of the prospectus. If both amounts are fully taken up it would increase the ordinary shares from 368,689,855 units to 614.6 million units and would raise nearly US$40 million in fresh capital for the investment bankers.

Proven in a release to the stock exchange advised that the Lead Brokers to the Offer have received applications in excess of the allotted US$19.66 million for the Renounceable Rights Issue of 1 new ordinary share for every block of 3 ordinary shares held in Proven Investments, as offered in the Prospectus dated March 12, 2015. The Board of Directors of Proven have therefore approved the upsizing of the shares made available for subscription, via the Conditional Offer described in the said Prospectus, and the extension of the closing date to April 17, 2015 to allow shareholders the ability to apply for additional shares over their original allotment, as contemplated by the Conditional Offer.

Proven reported profit from continuous operations of US$3.16 million for the nine months to December last year or just under 9 cents per share, in 2013 for the same period profit of US$2.79 million was reported.

There may be a number of factors encouraging investors to go after the stock in such numbers, one is the diversification the issue offers especially for large investors with large amounts of existing listings. With interest rates well under 10 percent a PE of 13 would not be regarded as expensive looked on by itself. Then again investors snapped up Sagicor Real Estate Fund at high prices two years ago in a market that was nowhere as bullish as the current market.

It will be interesting how this one trades in the months ahead and more so against some of the other top performing companies.