New Lubricant plant at Walton Park Road

Profit at Paramount Trading, jumped 137 percent to $34 in the first quarter to August last year, but declined by 35 percent in the November quarter, to $24 million from $37 million in 2016.

For the six months to November, profit rose only 13 percent to $58 million from $51 million in 2016. Sale revenues rose 28 percent for the November quarter, to $257 million from $200 million in 2016 and increased 31 percent for the year to date, to $487 million from $370 million in 2016.

The board of directors in their report to shareholders accompanying the quarterly, stated that “our lubricant business line produced strong sales during the quarter when compared to the last year growing $28 million or 261 percent and by $41.6 million with a 248 percent increase year to date. Technical grade product sales grew by $47 million or 137 on quarterly basis and $83 million or 133 percent year over the period year. We expect this trend to continue into the last two quarters.”

Processing and storage tanks inside factory.

Profit margin declined in the November quarter to 28 percent from 30 percent in the 2016, and slipped to 29 percent from 31 percent for the year to date period. The effect, gross profit rose 15 percent in the quarter to $99 million from $86 million and 19 percent for the year to date, to $200 million from $169 million in 2016.

While revenues rose solidly, so did administrative expenses that jumped 47 percent to $72 million in the quarter and increased 13 percent in the six months period to $121 million. Finance cost declined in the quarter, to a negative $2 million from $4 million in 2016 and from $7 million to $1.5 million for the half year.

Earnings per share came out at 1.5 cents for the quarter and 3.7 cents for the six months and should end the fiscal year ending to March around 25 cents with four months production and sales from the lubricant plant and the expanded chlorine and bleach operations.

Gross cash flow, brought in $72 million but growth in receivables, inventories, addition to fixed assets offset by loan inflows and reduced Payables wiped out the gains.

Another view inside of the factory.

Shareholders’ equity stands at $739 million with borrowings at just $77 million. Net current assets ended the period at $486 million, well over payables of $237 million. Inventories rose to $394 million from $320 million at the end of November 2016 and receivables climbed to $321 million from $238 million with cash and investments ending at $78 million.

The company commenced operation of the joint venture lubricant plant from around a month ago as well as production of bleach, an addition of a new product line. When the lubricant plant was announced in 2015, the estimate for revenues was in the US$5 million range but now that Alpart is reopened, the amount should rise.

The stock traded at $3.10 on the Junior Market of the Jamaica Stock Exchange with a PE ratio of 5.6 times IC Insider.com, 2019 earnings of around 55 cents per share.

The Jamaica Stock Exchange hit a new record within 1 minute of today’s opening with the JSE All Jamaican Composite Index jumping 4,576.37 points to 327,071.44 and the JSE Index climbing 4,169.59 points to a record 297,999.05.

The Jamaica Stock Exchange hit a new record within 1 minute of today’s opening with the JSE All Jamaican Composite Index jumping 4,576.37 points to 327,071.44 and the JSE Index climbing 4,169.59 points to a record 297,999.05.

that has languished just above the $30 level for months has broken into the $40 range and moved down to the second half of the list. The sharp price change follows an announcement that the company signed an agreement to buyback leased assets during this year. The buyback is set to save around $2 billion per annum before tax.

that has languished just above the $30 level for months has broken into the $40 range and moved down to the second half of the list. The sharp price change follows an announcement that the company signed an agreement to buyback leased assets during this year. The buyback is set to save around $2 billion per annum before tax. Revenues for the half year to December last year grew 11 percent to $493 million and profit rising 138 percent, continuing the normal annual growth. Revenues will hit the billion mark for the first time in the company’s history, for the current fiscal year and remain over that level going forward. The performance of the economy is critical to the future fortunes and to a lesser degree, the quality of films. Data shows that with tight economy, patronage in Kingston suffered badly with the fall in the economy from in 2008 onwards. At the same time strong growth said to be around 7 percent per annum in the Montego Bay economy, shows up in strong revenues gains there compared to Kingston. With the overall economy recovering, Palace is benefitting.

Revenues for the half year to December last year grew 11 percent to $493 million and profit rising 138 percent, continuing the normal annual growth. Revenues will hit the billion mark for the first time in the company’s history, for the current fiscal year and remain over that level going forward. The performance of the economy is critical to the future fortunes and to a lesser degree, the quality of films. Data shows that with tight economy, patronage in Kingston suffered badly with the fall in the economy from in 2008 onwards. At the same time strong growth said to be around 7 percent per annum in the Montego Bay economy, shows up in strong revenues gains there compared to Kingston. With the overall economy recovering, Palace is benefitting.

The group is expected to continue to enjoy increased earnings in 2018 and the focus on expansion of new projects will be beneficial to them going forward.

The group is expected to continue to enjoy increased earnings in 2018 and the focus on expansion of new projects will be beneficial to them going forward.

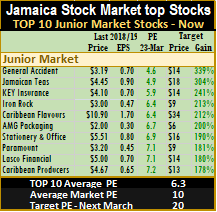

There were no entrants or exists from to the Junior Market TOP 10 list but

There were no entrants or exists from to the Junior Market TOP 10 list but  It just a matter of time for the break out to take place, regardless the channel points upwards for the market. Profit results for 2018 first quarter, will be important in helping to fuel the break out but with Treasury bill rates falling to 3.16 percent on the 182 days instrument during the past week, an important leg for a rally to come, is in place.

It just a matter of time for the break out to take place, regardless the channel points upwards for the market. Profit results for 2018 first quarter, will be important in helping to fuel the break out but with Treasury bill rates falling to 3.16 percent on the 182 days instrument during the past week, an important leg for a rally to come, is in place. At the same time the main market ended the week with a PE of 6.7 for the top stocks compared to a market average of close to 12.

At the same time the main market ended the week with a PE of 6.7 for the top stocks compared to a market average of close to 12.

Marketing and sales cost rose 16 percent to $9.6 million, administrative cost rose 34 percent to $43 million, reflecting added associated with the KIW acquisition, but finance cost fell 51 percent to $4.6 million.

Marketing and sales cost rose 16 percent to $9.6 million, administrative cost rose 34 percent to $43 million, reflecting added associated with the KIW acquisition, but finance cost fell 51 percent to $4.6 million.

SOS had acquired a building which was converted to a warehouse to allow for expansion of It’s offerings, this is now in use with some 6,000 square feet occupied. According to reports there are “lots of plans and expectations going forward for good business growth”. IC Indsider.com gathers that the December quarter that is normally the worse quarter for them due to the holidays, but the 2017 last quarter was the best quarter in the company’s history.

SOS had acquired a building which was converted to a warehouse to allow for expansion of It’s offerings, this is now in use with some 6,000 square feet occupied. According to reports there are “lots of plans and expectations going forward for good business growth”. IC Indsider.com gathers that the December quarter that is normally the worse quarter for them due to the holidays, but the 2017 last quarter was the best quarter in the company’s history.