Some investors have time and inclination to monitor their investments regularly, but the vast majority do not. In the latter case, investors want to invest for the long haul, expecting that their investment will grow appreciably over time.

There are many factors to consider; these include continued growth of companies, inflation, possible shifts in government policies, and social and economic policy changes that can affect investment returns in the short and long term.

Junior Market stocks have some features that investors should pay observe. Most Main Market stocks have controlling interest that is likely to ensure continuity of ownership for years to come. The same is not so for Junior Market companies where there are few companies where controlling ownership is assured long-term.

Barita public stock offer pulled money away from other JSE stocks.

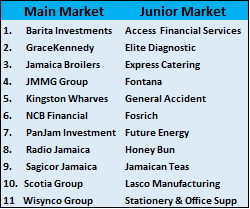

Barita Investments – Bankers are not supposed to be bright; they must be careful; this is an adage within the financial community worldwide. Tell that to the new management at Barita. Maybe if they were told, they might have avoided the negative comments they had to face in 2021. The directors can take comfort that JMMB Group suffered years of rumours about imminent failure, but they persevered and have prospered regardless and are now highly regarded. Barita stands an excellent chance of doing just that.

The recent focus on Barita is partially due to the current management taking a sleepy company and aggressively expanding into new and profitable areas and seems to be disrupting the status quo. They are aggressive and disruptive and are willing to go into areas with good growth potential when others take a more conservative posture. This approach is not risk free, to date, they seem to have prospered and their shareholders love it, having a rich stock price and healthy dividend payments. Additionally, Jamaica’s financial landscape is changing and providing increasing opportunities for growth of newer financial products. Barita has grown based on an increased capital base that stands them in good stead to prosper if management handles the resources at its disposal well. The company could be a significant player in financial services in the next ten years. They have taken a posture of paying out most profits and then going back to the market for added capital. That formula has worked well so far and has rewarded shareholders positively.

GraceKennedy has diversity in products, services, and geographic locations, making them one for the future, with a relatively significant presence in the USA and UK markets. They can enjoy good annual growth for years to come. The diversified product line put them in good stead to benefit from what seems set to be a reasonable period of economic growth for Jamaica. The Group has been acquiring new entities to expand the operations and geometric growth; this will give them increased bargaining power that can lower costs and drive revenues. Investors should not ignore the value of the Grace Brand will continue to be more valuable as the Group continues to make inroads into the international market. Currently, the stock is undervalued. Investors who can wait for the payoff could benefit from unlocking value down the road.

Jamaica Broilers’ product demand and global diversity will see them making money and providing good investment returns. Expected growth in the local tourism sector and the company’s efforts to expand its reach in the US market should augur well for investors from a company that is well managed and produces products that are in high demand in the local market. The negative is the politically sensitive nature of the main product. Management has been able to navigate such challenges and prospered over the years and should be able to do that in the future with their strong links to the farming community.

JMMG Group stock is severely undervalued currently. In addition, regional diversification, the variety of products and services it offers the public, and technology will drive revenues for the next ten years. The company has operations in the Dominican Republic, which is an excellent base for them to continue strong growth in that market with a population of 11 million, nearly four times the size of Jamaica. There is room for remarkable growth in that market that is not a financially developed market like Jamaica. Their banking arm in Jamaica and Trinidad is relatively small and they could enjoy above average growth that would be good for increased profit in the future.

Kingston Wharves has been around for decades and is highly profitable. It controls a significant portion of the logistics and distribution chain for imports and transhipment business, making them one to watch with growth expected in the Jamaican economy and growth in the transhipment. They should grow even faster as they cater to the local market and the expanding transhipment of goods within the region.

NCB Group stumbled in 2020, with the advent of the COVID 19 pandemic that saw major dislocations in businesses in Jamaica and worldwide, including the closure of the tourism industry. The Group suffered from a high degree of nonperforming loans, which is provided against and losses in the investment portfolio. The fourth quarter results for the just concluded year to September show that the worse is behind them and they should see growth in earnings for 2022. The Group is spread throughout the Caribbean and is involved in commercial and investment banking and insurance. Strong growth going forward will be dependent on a buoyant Jamaican economy and, to a lesser degree, that of Trinidad, where Guardian Holding is headquartered. Along the way, investors can expect a good level of dividends as compensation for waiting. The stock is currently in demand, but now could be the best time to start accumulating it.

Stephen Facey Chairman & Paul Hanworth Chief Operating Officer

PanJam Investment spans an array of activities from property development and ownership, many of them in prime areas in Jamaica, Investments, a significant owner in Sagicor Group and hotels. They are currently pushing into property investments in downtown Kingston and Montego Bay, the latter to be a hotel in the Montego Freeport area geared to business visitors. Buying into PanJam gives investors a strong involvement in Sagior Group, with the company owning around 30 percent of the shares. The Group has a long history of good performance and the suite of assets and quality management place them in an excellent position to grow at an attractive pace over the next ten years. While at it, don’t forget the heightened level of inflation that is currently afoot worldwide. PanJam, with its real estate and stock market portfolio, is well positioned to generate positive returns form as a result and protect investors against losing value in their investment in the company.

Radio Jamaica has lots of scope to grow revenues that will increase as the economy grows and swell profits as most of the revenues will fall to the bottom-line as operating costs are partly fixed. Most investors continue to focus on the old RJR but fail to recognize the Group’s invaluable assets, including the highly watched and profitable television station. The digital footprint is not to be ignored, with the Gleaner’s website being a big winner in the future, with the RJR site following. There are many developments taking place within the Group that will add to revenues and profit in the future. The digitization of television will create more flexibility in targeting markets with the signals and allow for expansion and increased income from the offerings it currently owns. Investors can look forward to reasonable dividend payments as profits grow in the future.

Sagicor Group & PanJam hit new closing highs.

Sagicor Jamaica is historically a strong performer that will benefit from continued growth in the Jamaican economy and buoyancy in the financial products that provide high returns. Apart from life insurance, they are involved in Health insurance and general insurance, investments, investment brokerage and banking. They control a sizeable portion of the local market and have a presence outside of Jamaica.

Scotia Group has had a long history of growing profits and dividends, with the stock price delivering attractive gains to investors over the years. In more recent years, things have not all gone well for the Group, with significant shifts in the financial market as new players and products came into the market and increased aggressiveness from the market leader NCB. The Group is now focusing on restructuring its branch network that will lead to lower costs while loans will be growing and driving interest income to help add to profits. The recent increase in interest rates will be highly beneficial to the Group. They will be generating more revenue from the government bonds as interest rates get some elevation from the Bank of Jamaica’s recent moves.

Wisynco Group is one of Jamaica’s larger manufacturing and distribution companies. The company has accumulated a wad of cash and will continue to do so with a very profitable operation that generates positive free cash flows. The growing buildup of cash places them in a healthy position to expand the group. The Group is involved in the manufacturing and distribution of products mainly for the local consumer market. It is a significant supplier to the tourism industry, with around 15 percent of the company’s goods. The sector continues to see growth with new hotel rooms being built and plans for more to come on stream in the future. It does not hurt with the company having a good management team, one of the most important elements in ensuring continued success in the business into the future.

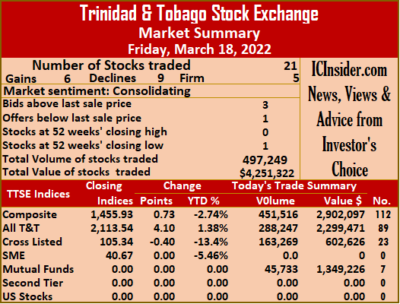

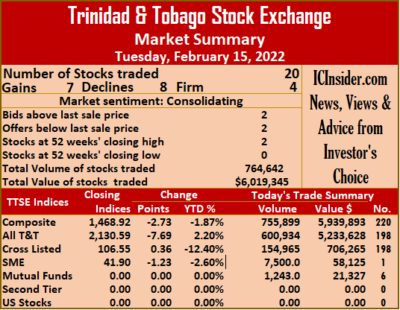

A total of 18 securities traded compared to 22 on Tuesday, with six rising, five declining and seven remaining unchanged. The Composite Index declined 0.71 points to 1,454.77, the All T&T Index slipped 0.97 points in ending at 2,107.35 and the Cross-Listed Index declined 0.06 points to 105.93.

A total of 18 securities traded compared to 22 on Tuesday, with six rising, five declining and seven remaining unchanged. The Composite Index declined 0.71 points to 1,454.77, the All T&T Index slipped 0.97 points in ending at 2,107.35 and the Cross-Listed Index declined 0.06 points to 105.93. Guardian Holdings fell 25 cents in closing at $28 after trading 1,310 units, JMMB Group shed 1 cent in ending at $2.25 after an exchange of 56,800 stock units, Massy Holdings inched 1 cent higher to end at $6 in exchanging 85,298 stock units. National Enterprises dropped 4 cents to $2.81, with 60,000 shares clearing the market, National Flour Mills finished at $1.84 in switching ownership of 848 units, One Caribbean Media declined 5 cents to $4.15 while exchanging 67,790 stocks. Republic Financial Holdings rallied 1 cent to $141.01, with 16,795 stocks crossing the exchange, Scotiabank popped $1.90 in closing at $81.90 after exchanging 899 shares, Trinidad & Tobago NGL ended unchanged at $20.25 in trading 25,842 units. Trinidad Cement remained at $3.50 with an exchange of 10,486 stock units, Unilever Caribbean finished at $15 after exchanging 2,860 shares and West Indian Tobacco ended at $24 with 3,224 units changing hands.

Guardian Holdings fell 25 cents in closing at $28 after trading 1,310 units, JMMB Group shed 1 cent in ending at $2.25 after an exchange of 56,800 stock units, Massy Holdings inched 1 cent higher to end at $6 in exchanging 85,298 stock units. National Enterprises dropped 4 cents to $2.81, with 60,000 shares clearing the market, National Flour Mills finished at $1.84 in switching ownership of 848 units, One Caribbean Media declined 5 cents to $4.15 while exchanging 67,790 stocks. Republic Financial Holdings rallied 1 cent to $141.01, with 16,795 stocks crossing the exchange, Scotiabank popped $1.90 in closing at $81.90 after exchanging 899 shares, Trinidad & Tobago NGL ended unchanged at $20.25 in trading 25,842 units. Trinidad Cement remained at $3.50 with an exchange of 10,486 stock units, Unilever Caribbean finished at $15 after exchanging 2,860 shares and West Indian Tobacco ended at $24 with 3,224 units changing hands. Guardian Holdings ended at $28.25 in exchanging 353 shares, JMMB Group dropped 10 cents to end at $2.25, with 79,707 units changing hands, L.J Williams B share slipped 10 cents to $2 with 284 stock units clearing the market. Massy Holdings remained at $6 after 184,173 stocks crossed the market, National Flour Mills finished at $1.84 after trading 1,000 units, NCB Financial Group rose 1 cent in closing at $6.02 in an exchange of 76,053 shares. Prestige Holdings fell 15 cents to end at $6.90 in trading 155 stock units, Republic Financial Holdings ended unchanged at $141.75 with 856 units crossing the exchange, Scotiabank rallied $2 to $80 in exchanging 3,719 stock units. Trinidad & Tobago NGL advanced 15 cents to close at $20.65 with the swapping of 29,517 shares, Trinidad Cement shed 20 cents in closing at $3.50 with an exchange of 5,000 stocks, Unilever Caribbean lost 24 cents to close at a 52 weeks’ low $15, with 687 stocks crossing the market and West Indian Tobacco finished at $24, with 38,856 units changing hands.

Guardian Holdings ended at $28.25 in exchanging 353 shares, JMMB Group dropped 10 cents to end at $2.25, with 79,707 units changing hands, L.J Williams B share slipped 10 cents to $2 with 284 stock units clearing the market. Massy Holdings remained at $6 after 184,173 stocks crossed the market, National Flour Mills finished at $1.84 after trading 1,000 units, NCB Financial Group rose 1 cent in closing at $6.02 in an exchange of 76,053 shares. Prestige Holdings fell 15 cents to end at $6.90 in trading 155 stock units, Republic Financial Holdings ended unchanged at $141.75 with 856 units crossing the exchange, Scotiabank rallied $2 to $80 in exchanging 3,719 stock units. Trinidad & Tobago NGL advanced 15 cents to close at $20.65 with the swapping of 29,517 shares, Trinidad Cement shed 20 cents in closing at $3.50 with an exchange of 5,000 stocks, Unilever Caribbean lost 24 cents to close at a 52 weeks’ low $15, with 687 stocks crossing the market and West Indian Tobacco finished at $24, with 38,856 units changing hands. In more recent times, some investors are demonstrating levels of exuberance in buying some stocks at excessive values that will take a long time to generate a reasonable return on investment.

In more recent times, some investors are demonstrating levels of exuberance in buying some stocks at excessive values that will take a long time to generate a reasonable return on investment.

The numbers climbed to 11 each as we could not separate the 11th ones from the lists. The listings are a compilation based on inputs from some knowledgeable investors as well as ICInsider.com’s own assessment. The selections are based on an evaluation of the quality of management, products and services each company offers to their customers, and prospects for growth by these companies and the economies they service.

The numbers climbed to 11 each as we could not separate the 11th ones from the lists. The listings are a compilation based on inputs from some knowledgeable investors as well as ICInsider.com’s own assessment. The selections are based on an evaluation of the quality of management, products and services each company offers to their customers, and prospects for growth by these companies and the economies they service.

JMMB Group increased 10 cents to $2.35 with an exchange of 101,627 stocks, Massy Holdings closed at $6 after the trading of 200,180 shares, National Enterprises ended unchanged at $2.85, with 42,810 stock units crossing the market. National Flour Mills lost 1 cent in closing at $1.84 with the swapping of 25 units, NCB Financial Group shed 8 cents to end at a 52 weeks’ low of $6.01, with 41,495 stocks clearing the market, One Caribbean Media rallied 5 cents to $4.20 after exchanging 20,000 stock units. Prestige Holdings shed 5 cents in ending at $7.05 after trading 19 shares, Republic Financial Holdings dropped 25 cents to $141.75, with 500 stock units crossing the exchange, Scotiabank remained at $78 after 3,415 units passed through the market. Trinidad & Tobago NGL lost 15 cents to end at $20.50 trading 4,011 stocks, Unilever Caribbean fell 1 cent in closing at $15.24 in trading 2,006 shares and West Indian Tobacco ended unchanged at $24 in exchanging 11,615 stocks.

JMMB Group increased 10 cents to $2.35 with an exchange of 101,627 stocks, Massy Holdings closed at $6 after the trading of 200,180 shares, National Enterprises ended unchanged at $2.85, with 42,810 stock units crossing the market. National Flour Mills lost 1 cent in closing at $1.84 with the swapping of 25 units, NCB Financial Group shed 8 cents to end at a 52 weeks’ low of $6.01, with 41,495 stocks clearing the market, One Caribbean Media rallied 5 cents to $4.20 after exchanging 20,000 stock units. Prestige Holdings shed 5 cents in ending at $7.05 after trading 19 shares, Republic Financial Holdings dropped 25 cents to $141.75, with 500 stock units crossing the exchange, Scotiabank remained at $78 after 3,415 units passed through the market. Trinidad & Tobago NGL lost 15 cents to end at $20.50 trading 4,011 stocks, Unilever Caribbean fell 1 cent in closing at $15.24 in trading 2,006 shares and West Indian Tobacco ended unchanged at $24 in exchanging 11,615 stocks. A total of 19 securities were traded, down from 21 on Wednesday and ended with six rising, seven declining and six ending unchanged. NCB Financial ended at another 52 weeks’ low at the close. The Composite Index rose 4.80 points to 1,455.20, the All T&T Index gained 19.00 points to close at 2,109.44 and the Cross-Listed Index shed 1.46 points to end at 105.74.

A total of 19 securities were traded, down from 21 on Wednesday and ended with six rising, seven declining and six ending unchanged. NCB Financial ended at another 52 weeks’ low at the close. The Composite Index rose 4.80 points to 1,455.20, the All T&T Index gained 19.00 points to close at 2,109.44 and the Cross-Listed Index shed 1.46 points to end at 105.74. JMMB Group ended unchanged at $2.25 in an exchange of 12,553 stock units, Massy Holdings rallied 10 cents in closing at $6 after 467,294 stocks crossed the exchange, National Flour Mills ended at $1.85 after exchanging 9,855 shares. NCB Financial Group dropped 11 cents to a 52 weeks’ low of $6.09 after 25,070 stocks changed hands, Republic Financial Holdings rose $2 to close at $142, after 134 shares crossed the market, Scotiabank finished at $78 trading 35 units. Trinidad & Tobago NGL climbed $1.62 to end at $20.65 with an exchange of 9,893 stock units, Trinidad Cement declined 5 cents in closing at $3.70 while exchanging 3,000 units, Unilever Caribbean advanced 5 cents to close at $15.25 after 44,465 stocks crossed the market and West Indian Tobacco remained at $24 in an exchange of 45,128 shares.

JMMB Group ended unchanged at $2.25 in an exchange of 12,553 stock units, Massy Holdings rallied 10 cents in closing at $6 after 467,294 stocks crossed the exchange, National Flour Mills ended at $1.85 after exchanging 9,855 shares. NCB Financial Group dropped 11 cents to a 52 weeks’ low of $6.09 after 25,070 stocks changed hands, Republic Financial Holdings rose $2 to close at $142, after 134 shares crossed the market, Scotiabank finished at $78 trading 35 units. Trinidad & Tobago NGL climbed $1.62 to end at $20.65 with an exchange of 9,893 stock units, Trinidad Cement declined 5 cents in closing at $3.70 while exchanging 3,000 units, Unilever Caribbean advanced 5 cents to close at $15.25 after 44,465 stocks crossed the market and West Indian Tobacco remained at $24 in an exchange of 45,128 shares. The company was listed on the Junior Market of the Jamaica Stock Exchange and Monday brought the total listings on the market to 44, the number of listed companies to 43 and the listing of companies on the exchange to 97 companies.

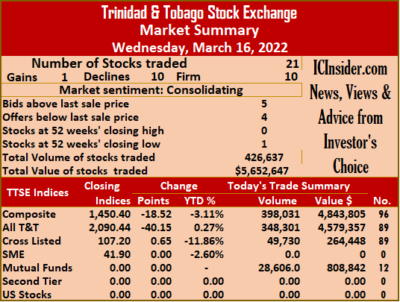

The company was listed on the Junior Market of the Jamaica Stock Exchange and Monday brought the total listings on the market to 44, the number of listed companies to 43 and the listing of companies on the exchange to 97 companies. At the close the Composite Index dropped 18.52 points to 1,450.40, the All T&T Index plunged 40.15 points to settle at 2,090.44, but the Cross-Listed Index popped 0.65 points to settle at 107.20.

At the close the Composite Index dropped 18.52 points to 1,450.40, the All T&T Index plunged 40.15 points to settle at 2,090.44, but the Cross-Listed Index popped 0.65 points to settle at 107.20. GraceKennedy shed 1 cent in closing at $5.99 crossing trading 1,000 shares, Guardian Holdings declined 50 cents to close at $29 in switching ownership of 1,104 units, JMMB Group finished at $2.25 after exchanging 10,000 shares. L.J. Williams B share remained at $2.10 with the swapping of 25 units, Massy Holdings dropped 10 cents to close at $5.90, with 288,551 stocks clearing the market, National Enterprises dropped 7 cents in closing at $2.85 after trading 7,106 stock units. NCB Financial Group lost 30 cents ending at a 52 weeks’ low of $6.20 after finishing trading 4,000 units, One Caribbean Media shed 5 cents to end at $4.15, with 1,000 stocks crossing the market, Point Lisas ended at $3.50, with 50 shares changing hands. Prestige Holdings closed at $7.10 while exchanging 100 stock units, Republic Financial Holdings finished at $140 with an exchange of 286 shares, Scotiabank fell $3.99 to end at $78 in switching ownership of 1,225 units. Trinidad & Tobago NGL declined $1.82 to $19.03 with the swapping of 1,000 stock units, Trinidad Cement remained at $3.75 trading 10 stocks and West Indian Tobacco finished at $24 in exchanging 2,810 units.

GraceKennedy shed 1 cent in closing at $5.99 crossing trading 1,000 shares, Guardian Holdings declined 50 cents to close at $29 in switching ownership of 1,104 units, JMMB Group finished at $2.25 after exchanging 10,000 shares. L.J. Williams B share remained at $2.10 with the swapping of 25 units, Massy Holdings dropped 10 cents to close at $5.90, with 288,551 stocks clearing the market, National Enterprises dropped 7 cents in closing at $2.85 after trading 7,106 stock units. NCB Financial Group lost 30 cents ending at a 52 weeks’ low of $6.20 after finishing trading 4,000 units, One Caribbean Media shed 5 cents to end at $4.15, with 1,000 stocks crossing the market, Point Lisas ended at $3.50, with 50 shares changing hands. Prestige Holdings closed at $7.10 while exchanging 100 stock units, Republic Financial Holdings finished at $140 with an exchange of 286 shares, Scotiabank fell $3.99 to end at $78 in switching ownership of 1,225 units. Trinidad & Tobago NGL declined $1.82 to $19.03 with the swapping of 1,000 stock units, Trinidad Cement remained at $3.75 trading 10 stocks and West Indian Tobacco finished at $24 in exchanging 2,810 units. Massy Holdings fell 1 cent to $6 trading 515,384 units, National Enterprises declined 3 cents to $2.92 after trading 1,600 stocks, National Flour Mills popped 1 cent to close at $1.85 after exchanging 15,146 stock units. NCB Financial Group rallied 49 cents to a 52 weeks’ low of $6.50, with 14,528 shares crossing the market, One Caribbean Media climbed 5 cents in closing at $4.20 after 2,391 units changed hands, Prestige Holdings gained 10 cents to end at $7.10 with the swapping of 3,501 stock units. Republic Financial Holdings shed $1 to close at $140, with 1,213 stocks changing hands, Scotiabank advanced $7 in closing at 52 weeks’ high of $81.99 after 6,024 stocks crossed the market, Trinidad & Tobago NGL rose 33 cents in ending at $20.85 with the swapping of 13,935 shares. Unilever Caribbean dropped 5 cents to end at $15.20 with an exchange of 1,000 stock units and West Indian Tobacco ended unchanged at $24 in switching ownership of 26,928 units.

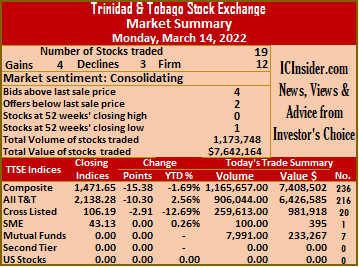

Massy Holdings fell 1 cent to $6 trading 515,384 units, National Enterprises declined 3 cents to $2.92 after trading 1,600 stocks, National Flour Mills popped 1 cent to close at $1.85 after exchanging 15,146 stock units. NCB Financial Group rallied 49 cents to a 52 weeks’ low of $6.50, with 14,528 shares crossing the market, One Caribbean Media climbed 5 cents in closing at $4.20 after 2,391 units changed hands, Prestige Holdings gained 10 cents to end at $7.10 with the swapping of 3,501 stock units. Republic Financial Holdings shed $1 to close at $140, with 1,213 stocks changing hands, Scotiabank advanced $7 in closing at 52 weeks’ high of $81.99 after 6,024 stocks crossed the market, Trinidad & Tobago NGL rose 33 cents in ending at $20.85 with the swapping of 13,935 shares. Unilever Caribbean dropped 5 cents to end at $15.20 with an exchange of 1,000 stock units and West Indian Tobacco ended unchanged at $24 in switching ownership of 26,928 units. A total of 19 securities traded compared to 16 on Friday, with four rising, three declining and 12 remaining unchanged. The Composite Index declined 15.38 points to 1,471.65, the All T&T Index fell 10.30 points to finish at 2,138.28 and the Cross-Listed Index dropped 2.91 points to settle at 106.19.

A total of 19 securities traded compared to 16 on Friday, with four rising, three declining and 12 remaining unchanged. The Composite Index declined 15.38 points to 1,471.65, the All T&T Index fell 10.30 points to finish at 2,138.28 and the Cross-Listed Index dropped 2.91 points to settle at 106.19. National Flour Mills remained at $1.84 trading 7,791 units, NCB Financial Group fell 44 cents to a 52 weeks’ low of $6.01 in exchanging 39,765 stock units, One Caribbean Media ended unchanged at $4.15, with 2,648 stocks crossing the market. Point Lisas closed at $3.50 in an exchange of 2,000 stock units, Prestige Holdings lost 10 cents after ending at $7 after 4,465 shares crossed the market, Republic Financial Holdings gained $1 to end at $141 exchanging 282 stocks. Scotiabank ended at $74.99 trading 60 units, Trinidad & Tobago NGL finished at $20.52 with the swapping of 3,836 stocks, Unilever Caribbean ended unchanged at $15.25 trading 8,500 shares and West Indian Tobacco advanced 65 cents after ending at $24, with 9,253 units crossing the market.

National Flour Mills remained at $1.84 trading 7,791 units, NCB Financial Group fell 44 cents to a 52 weeks’ low of $6.01 in exchanging 39,765 stock units, One Caribbean Media ended unchanged at $4.15, with 2,648 stocks crossing the market. Point Lisas closed at $3.50 in an exchange of 2,000 stock units, Prestige Holdings lost 10 cents after ending at $7 after 4,465 shares crossed the market, Republic Financial Holdings gained $1 to end at $141 exchanging 282 stocks. Scotiabank ended at $74.99 trading 60 units, Trinidad & Tobago NGL finished at $20.52 with the swapping of 3,836 stocks, Unilever Caribbean ended unchanged at $15.25 trading 8,500 shares and West Indian Tobacco advanced 65 cents after ending at $24, with 9,253 units crossing the market.