Stationery and Office Supplies reported earnings of 26 cents per share for 2016 and IC Insider.com forecast 40 cents pretax for the current year from just over $90 million in pretax profit, a near doubling in profits over the $53 million reported in 2016.

Stationery and Office Supplies reported earnings of 26 cents per share for 2016 and IC Insider.com forecast 40 cents pretax for the current year from just over $90 million in pretax profit, a near doubling in profits over the $53 million reported in 2016.

Revenues increased 11 percent in 2013, just 5 percent in next year, 14 percent in 2015 and 12 percent in 2016 and 20 percent for the first six months of 2017, hitting $702 million in 2016 and seems on target to get to around $850 million for 2017.

Pre-tax Profit in 2016, pre-tax profits jumped 279.5 percent to end at $53 million compared to only $14 million in 2015, and $8 million in 2014.

Improvement in the Company’s revenues has been attributable to organic expansion driven by the achievement of deeper penetration in the market for the Company’s products and services but inflation and devaluation of the Jamaican dollar versus the United States currency would also play roles. Improved profit and cash flow generated in the last two years helped to fund increased inventory making more choices available to customers and that is reflected in a noticeable pick-up in sales. The Company has expanded its product offerings, adding to the list of brands it distributes and venturing into manufacturing its own brands of furniture – Image and Torch.

Gross profit as a percentage of sales was a strong 48 percent in 2016, coming from 43 percent in 2015 and 44.55 percent in 2014. Lower cost of sales led to an improved gross profit position of $339 million in 2016, which 26.09 percent increase over that earned in 2015 and 10 percent more in 2015 over 2014.

Gross profit as a percentage of sales was a strong 48 percent in 2016, coming from 43 percent in 2015 and 44.55 percent in 2014. Lower cost of sales led to an improved gross profit position of $339 million in 2016, which 26.09 percent increase over that earned in 2015 and 10 percent more in 2015 over 2014.

As at the 31 March 2017, SOS reported first quarter revenues of $220 million, 20.7 percent more than the $182 million reported in the corresponding period for 2016. Cost of sales as a proportion of revenue remained in line with the FY 2016 representing 50.66 percent of total revenue; this percentage was however slightly higher than the 48.75 percent for all of 2016. The company reported pretax profits of $30 million compared to $29.5 million in Q1 2016. A number of factors impacted the 2016 results that resulted in higher profits than would normally be the case as such the 2017 profit are better than the figures suggest. In effect the 2016 first quarter could be around $20 million from normal ongoing operation.

Gross profit for the three month period ended 31 March 2017 was $108.64 million or 16.2 percent more than the $93 million reported in 2016. SOS also reported an increase in administrative costs of 21 percent to $53 million and selling expenses climbed 37.5 percent to $18 million.

Total assets were valued at J$498 million at the March this year comprising current assets of $243 million. Inventories stood at $117 million, receivables $93 million and cash of J$12 million. Total liabilities amounted to J$231 million, with trade and other payables of J$78 million. Shareholders equity stood at $270 million or $1.35 per share.

Total assets were valued at J$498 million at the March this year comprising current assets of $243 million. Inventories stood at $117 million, receivables $93 million and cash of J$12 million. Total liabilities amounted to J$231 million, with trade and other payables of J$78 million. Shareholders equity stood at $270 million or $1.35 per share.

The company will benefit greatly from listing and sales to climb above recent levels form the increased exposure that will be gained from listing on an ongoing basis as well as the increased working capital that will provide additional choices for customers and help fuel increased sales. IC Insider.com accords the stock BUY RATED with the price to rise sharply after the stock list.

SOS solidly BUY RATED

This SOS IPO who are the connections?

The McDaniel family owned Stationery and Office Supplies (SOS) after 50 years of serving their more than 3,000 clients, are heading in a new direction. No longer content to hug up 100 percent of the company the family is now are embarking enjoining the public to ride on with them to the next level.

The McDaniel family owned Stationery and Office Supplies (SOS) after 50 years of serving their more than 3,000 clients, are heading in a new direction. No longer content to hug up 100 percent of the company the family is now are embarking enjoining the public to ride on with them to the next level.

In furtherance of this new thrust SOS is now seeking to list on the Jamaica Stock Exchange Junior Market with an initial public offering 50,024,100 ordinary shares, to raise approximately $95,048,200 before expenses. The issue is inclusive of 22,500,000 reserved shares some of which are being sold at $1.60 for staff, with the rest being made available to the general public at $2 per share the offer opening at 9 on July 19th, with the closing set for 4:30 P.M. on July 26th.

The Company reported pretax profits of $53 million in 2016, from sales of $702 million, with earnings of 26.5 cents per share, resulting in a PE of 7.5 before tax. Earnings for 2017 is estimated at around 40 cents on a pretax basis at an attractive PE of 5.6 times 2017 earnings. Revenues for the first six months of 2017, are up almost 20 percent over the similar period in 2016. Office furnishing and fixtures account for approximately 60 percent of sales revenues and stationery and office supplies for 40 percent management advised IC Insider.com.

The Company estimates that the expenses in the invitation will not exceed $12,000,000 inclusive of General Consumption Tax and an expanded marketing and publicity spend, expected to not only drive interest in the IPO but create greater awareness about the company. and its products.

The Company estimates that the expenses in the invitation will not exceed $12,000,000 inclusive of General Consumption Tax and an expanded marketing and publicity spend, expected to not only drive interest in the IPO but create greater awareness about the company. and its products.

Minimum raise| The Company needs to raise at least $50,000,000 to qualify for listing on the Junior Market. If that amount is not achieved an application will not be made for the shares to be admitted to the Junior Market and all funds will be returned to the persons who made them.

History| The Company started business in July 1965 under the guidance of Richard Hing, George Hew and David McDaniel. In 1970, the Company became wholly owned by the McDaniel family when all of the issued ordinary shares were acquired by David and Marjorie McDaniel. The Company now operates out of a 35,000 square feet warehouse, office and showroom on Beechwood Avenue in Kingston and a 3,000 square feet location in Montego Bay that houses 1,200 square feet of office and showroom space and a 1,800 square foot warehousing facility supported by a staff complement of sixteen. The Head Office currently employs eighty-three team members. Eleven delivery vehicles are operated by the company including trucks, which support delivery to customers.

Products|The Company now sells and market office supplies and stationery items, modular office furniture, partitions, metal products, chairs, cabinets and shelving. The Company is the sole local distributor for the leading international brands in office furniture – Fursys and Boss. In 2011, lower priced items were introduced to meet growing demand, by introducing the first of two proprietary brands, the first being the “Image” brand and shortly thereafter in 2012, the Company introduced its second brand “Torch”. SOS also does a small amount of sales to the eastern Caribbean and will be seeking expand business into that Region. According to the company’s management, the increased warehouse space will be critical to this effort. A lesser known service the company carries out, is the servicing of office equipment. This area they indicate has room for increased revenues and profit.

During the last six years, the Company added commercial shredding to its suite of services offered to the general public. The service has become popular among entities which have large volumes of waste paper and other sensitive material that stores data, but are concerned about improper disposal methods. The Company’s states that its “shredding facility meets international best practice standards and has the capacity to shred up to 5,000 pounds of paper per day as well as the destruction of tapes, hard drives and compact discs. The Company’s shredding facility offers the customer the ability to view an on-line real-time video stream of the shredding process being undertaken on-site on their behalf, or if preferred the customer may also be present when the shredding process is being undertaken”.

The directors of the company are, David McDaniel, Marjorie McDaniel, Allan McDaniel, Stephen Todd, Kerri (McDaniel) Todd, Kelli (McDaniel) Muschett, Anthony Bell, Gary “Butch” Hendrickson and Evan Thwaites.

Radio Jamaica looks promising

Radio Jamaica generated revenues of $1.2 billion in the March 2017 quarter, $156 million less than the December quarter but had $49 million more in direct expenses in the March quarter when it was expected that direct expenses would have fallen in keeping with the reduced income.

Radio Jamaica generated revenues of $1.2 billion in the March 2017 quarter, $156 million less than the December quarter but had $49 million more in direct expenses in the March quarter when it was expected that direct expenses would have fallen in keeping with the reduced income.

The group also reported lower profits in the March quarter compared with the December quarter and suffered a loss before taxation of $30 million and $65 million after an increased taxation charge of $35 million, bringing the full year taxation provision to $75 million. RJR ended the fiscal year with profit after tax of $145 million or just 6 cents per share. Results for 2018 should be much better as staff cost will fall with reduction in staffing while some one off cost that affected profit, should not recur.

In the March quarter, general expenses fell by $110 million from the December quarter to reach $562 million. The sharp change could result from reclassification of some expenses to direct cost, resulting in the jump in this area in the last quarter of the fiscal year. In the December quarterly report, the company stated that “increased cost of $64 million was incurred largely from further operational investments and one- off costs”. The areas that incurred the cost are continued rollout of 1 Spot Media, legal expenses incurred in protecting copy rights and defending legal action and repairs to broadcast transmitters. This was reconfirmed by Managing Director, Gary Allen in response to questions posed by IC Insider.com as the reason why profit in the Television segment had fallen even as revenues rose.

“The figures have seven months of the old structure. Only five months of HR synergies were realised in the financial year under review, as redundancies took place in September/November” Gary Allen, Managing Director advised IC Insider.com, in response to our question of how much staff cost is in the 2107 figures for person who were made redundant?

Prior to the merger investors were advised of major cost reduction and improved revenues that will flow from the merged entity. Allen stated ‘they have started with the HR synergies. Others are being realised as we integrate systems in the operations. Most elements will be implemented by the end of 2018/2019.”

Cash flow from operating activities was $363 million but $248 million was spent on acquiring fixed assets with the group ending with cash and equivalent of $291 million at the end of the year. RJR also has investments in bonds and Government of Jamaica securities amounting to $487 million.

Gleaner & RJR execs signing merger agreement in 2015

The RJR Group underwent major changes with the acquisition of the Gleaner media business. Comparing the 2017 fiscal year’s results with that of 2016 makes little sense with the latter having very little financial data of the acquired business.

Data contained in the segment results, provide some indication as to the performance of various parts of the group. The performance of the segments in 2017 over 2016 show, Audio Visual generating just $65 million more in revenues in 2017 to end with $1.868 billion and contributed $72 million to profits compared to $157 million in 2016, Audio comprising radio operations had revenues of $711 million compared to $567 million and contributed profit of $238 million versus $112 million, Independent Radio coming on stream and growth in Outside Broadcasts contributed to the increase. The print division showed revenues of only $78 million in 2016 and a loss of $190 million saw a major about turn, with revenues of $2.8 billion and profit of $173 million for 2017.

Allen went on to state that “the market will remain competitive and the economic conditions of Jamaica will continue to impact media spend. Improvements will come from those able to leverage market leadership positions, product diversification, overseas earnings and new marketing strategies. RJR has all the necessary ingredients to meet these challenges and the opportunities on the horizon.”

The stock traded at $1.60 on the Jamaica Stock Exchange on Friday and with IC Insider.com projecting earnings of 25 cents per share for 2018 fiscal year ending in March, the stock seems attractive coming against a back ground of continued growth in the Jamaican economy.

AMG eases Dolphin Cove out of TOP 10

AMG Packaging back in IC TOP 10.

Only one change occurred in the TOP 10 list for the past week with AMG Packaging reentering the list and Dolphin Cove moving out, as the price of the latter moved back to $20 from $18, the week before.

In the main market Berger Paints jumps to third position from 7 with the price tumbling from $17.31 to $12.50 during the week after trading at a low of $12.05.

The other news worthy development of the week was the increase in the price of former TOP 10 Junior Market listing, Jetcon Corporation that drop out of the top list last week. The stock closed at a new high during the past week but ended at $5.90 after 3 for 1 stock split took effect on Thursday, with attempts to trade at $7.40 on Friday thwarted by the circuit breaker rules. The trade was cancelled after the market closed.

Thursday, with attempts to trade at $7.40 on Friday thwarted by the circuit breaker rules. The trade was cancelled after the market closed.

Market movement continues to be constrained by near term resistance levels but it does not prevent stocks from moving in either direction, but it will tend to keep prices overall from big movements upwards.

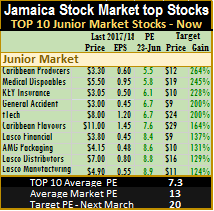

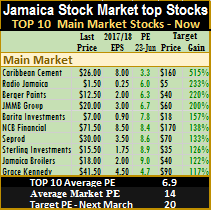

The average PE ratio for the Junior Market Top stocks is 7.3 and 6.9 in the main market, these compare favourably with 13.5 for the overall main market and 13 for Junior Market, based on 2017 estimated earnings.  Several stocks are trading below these averages, and have potential for more gains in the months ahead, barring major negative developments.

Several stocks are trading below these averages, and have potential for more gains in the months ahead, barring major negative developments.

At the close of the week, IC Insider.com’s TOP 10 Junior Market stocks now trade at an average discount of 43 percent to the Junior Market average, while those in the main market are trading at a 49 percent discount, to the average of the market, leaving stocks with room for growth in the months ahead. At the end of April the reading was 35 percent discount for the juniors and 53 percent for the majors.

Jamaica abounds with opportunities

Attentive shareholders at Jetcon recently held 2017 AGM

The successful performance of Jetcon Corporation since listing in 2016, reveals the rich opportunities that exist in Jamaica for Jamaicans to better themselves financially, chairman of the company, John Jackson said, in addressing shareholders at the company’s first Annual General Meeting, as a public company.

Jackson went on to state “ordinary Jamaicans need adequate education, need to corporate with and trust one another, share our assets in an organized manner and the sky is the limit to what can be achieved’. “Many opportunities exist for Jamaicans to profit from, however, they need to learn how to find them.” This means, with greater financial sophistication born out of knowledge, coupled with the advent and buoyancy of the Junior Market, ordinary Jamaican families can capitalize on various financial prospects that exist in the country”. The success of Jetcon and other newer businesses in the country suggests the need for an intervention of the Jamaican authorities to educate Jamaicans on the immense opportunities that exist to lift their quality of life through financial education and investments by pooling of their financial resources.

Jackson was speaking against the back drop of Jetcon Corporation’s doubling in profits for 2016 with preliminary data to May 2017, showing revenues rising by 75 percent and profit of approximately 150 percent over 2016.

Main Event inadequate Q2 report

Three directors of Main Event, including the mentor who is respossible to ensure compliance with teh JSE rules.

The 2017 junior listed Main Event Entertainment, made a loss in the last six months of the 2016 fiscal year, ending the year with a profit of $56 million, down from $64 million for the six months to April.

The latest figures from the entertainment company for 2017, show a profit of $75 million for the half year and $51 million for the April quarter.

The figures reveal seasonal differences in the operation, with higher revenues and profit in the first half and lower revenues and losses or minimal profit in the second half. The Jamaica Stock Exchange rules require that seasonality in operations is to be reported on, in a listed company financial report. There is total silence on this issue in Main Event’s report, leaving investors to guess what the second half will be like, it should not take the stock exchange rules to put to this. Good investors’ relations suggest that this is absolutely needed in this situation of wide variation in the two periods. Astonishingly, a review of the company’s prospectus gives no indication of seasonality of revenues and earnings.

The directors’ report accompanying the half year results, speaks to a reduction in direct expenses due to continued investment in fleet and transportation solutions, and rental equipment and human resources. At the same time administrative cost had a big increase due mainly to increased transportation and fleet management costs. It appears that these added costs should be treated as a part of direct cost and not administrative.

Revenue in the April quarter at $319 million was flat with the 2016 out turn but the half year rose 8 percent to $652 million. The data to date show no indication that the second half year results will show much if any improvement over the outcome for 2016 except for the removal of taxes.

At the initial public offer in January the issued share capital was 240,004,000 shares and 60,001,000 shares were issued to the public, resulting in an average number of shares issued for the April quarter of 300,005,000 units but only 270 million units for the half year. The report shows the fully issued number of shares at the end of April is used in computing earnings per share (EPS) for all periods.

The effect is that the  reported in the interim results are wrong and in effect understated as the number of shares used in the computation is overstated. Instead of earnings per share of 25 cents for the half year it is 27.7 cents and for the 2016 period 26.8 cents and not 21 cent. The earnings for the 2016 April quarter, is 17.2 cents and for the full 2016 fiscal year 23.5 cents.

reported in the interim results are wrong and in effect understated as the number of shares used in the computation is overstated. Instead of earnings per share of 25 cents for the half year it is 27.7 cents and for the 2016 period 26.8 cents and not 21 cent. The earnings for the 2016 April quarter, is 17.2 cents and for the full 2016 fiscal year 23.5 cents.

There are clearly weaknesses in the report and its handling, but worse it is also showing weaknesses in the overall management inclusive of the directorate.

The company expended over $107 million on fixed assets, increased borrowed funds by a mere $10 million more than at the end of October with cash ending at $65 million from just $19 million at the end of October.

With the interim results ending at 28 cents per share, it is going be challenging for earnings for the full year to be much higher than 35 cents IC Insider.com is forecasting for the year to October, barring a sizable rise in revenues. It could go on to earn 50 cents for 2018, IC Insider.com’s forecast shows. At the current price of $6 on the Junior Market of the Jamaica Stock Exchange the PE ratio is 17, suggesting that the price may revolve around this level for a while.

Berger returns to TOP 10

Shuffling of stocks in the TOP 10 list was quite pronounced this past week with two companies exiting and entering each list. Jetcon Corporation and CAC 2000 slipped out of the Junior Market TOP 10, and were replaced by Dolphin Cove and Lasco Financial.

Shuffling of stocks in the TOP 10 list was quite pronounced this past week with two companies exiting and entering each list. Jetcon Corporation and CAC 2000 slipped out of the Junior Market TOP 10, and were replaced by Dolphin Cove and Lasco Financial.

Entering the TOP 10 main market list are Berger Paints, returning after a recent fall from the list and Grace Kennedy that dropped out previously.

In the main market of the Jamaica Stock Exchange, Scotia Investments earnings per share have been sharply reduced with the latest results for the half year showing no growth, with the stock falling off the TOP 10 list as a result, while Salada Foods price rose to $10, resulting in it being pushed off the list.

TOP 10 list as a result, while Salada Foods price rose to $10, resulting in it being pushed off the list.

In trading last week, tTech demand is building while selling has eased with limited supply being shown in the market. Elsewhere, NCB Financial Group is hitching for a major breakout from a wedge formation.

As indicated in recent weeks, market movement continues to be constrained by near term resistance levels which is acting as short term restraint to a break out from current levels for the time being.

The average PE ratio for the Junior Market Top stocks is 7.4 and 7.2 in the main market, these compare favourably with 13.8 for the overall main market and 13 for Junior Market, based on 2017 estimated earnings. Several stocks are trading below the average, and have the potential for more gains for the rest of 2017, barring major negative developments.

In a number of cases, the TOP stocks will need to deliver results in the upcoming quarter in order to send a message that the potential they have will be manifested.

In a number of cases, the TOP stocks will need to deliver results in the upcoming quarter in order to send a message that the potential they have will be manifested.

At the close of the week, IC Insider.com’s TOP 10 Junior Market stocks now trade at an average discount of 45 percent to the Junior Market average, while those in the main market are trading at a 48 percent discount, to the average of the market, leaving stocks with room for growth in the months ahead. At the end of April the reading was 35 percent discount for the juniors and 53 percent for the majors.

16% rise in Scotia Group Q2 profit

Scotia Group reports a 14 percent increase in profit compared to the period in 2016. The banking group added $718 million more in profit to $5.7 billion for the six months to April 2017 over 2016.

Scotia Group reports a 14 percent increase in profit compared to the period in 2016. The banking group added $718 million more in profit to $5.7 billion for the six months to April 2017 over 2016.

Net income for the second quarter rose 16 percent to $3.4 billion, versus $2.94 billion in the same period in 2016. Total revenues for the April quarter amounted to $16.7 billion while in 2016 the group generated revenues of $11 billion while revenues for the six months ended at $23 billion versus $21 billion.

“The positive movement was achieved through increased loan and transaction volumes across our business lines,” the Group stated in a report accompanying the results. Net interest income after impairment losses for the six month period was $12.2 billion, $399 million or 3 percent above the same period in 2016

“Net fees and commission income amounted to $4.4 billion, driven by higher transaction volumes and the growth in our credit card, merchant services, and asset management business. Insurance revenue increased by 31% given the growth in core insurance business and actuarial reserve release from changes in assumptions on valuation of the portfolios. Net gains on foreign currency activities and financial assets amounted to $1.3 billion based on trading volumes,” the Group stated.

Operating Expenses amounted to $11.1 billion for the six month period, an increase of $300 million or 3 percent compared to prior year. Salaries and staff benefit costs increased by $201 million, which was offset by lower other operating expenses of $87 million. Asset tax increased by $112 million or 12% to $1.1 billion due to the increase in the Group’s assets.

Impairment losses on loans amounted to $975 million, up $367 million from last year as higher write-offs on unsecured retail loan portfolio grew by $7 billion or 4 percent year over year, with loans after allowance for impairment losses, increasing to $164.2 billion.

Berger & Scotia Group jump TOP 10

Scotiabank jumped out of TOP 10.

The main market of the Jamaica Stock Exchange, moved forward on each day of the past week except for a fall on Thursday to sit close to the all-time high on Friday. Movement in the Junior Market was up and down but a few stocks traded at new highs during the week.

In the main market, IC Insider downgraded the earnings of Carreras to $9 after the company reported full year results, the stock jumped to a record $89 at the close of the week and is out of the top listing. Carreras exit allowed for Jamaica Broilers to return to the main market listing. Jetcon Corporation returns to the Junior Market list and Lasco Financial moves out of the TOP 10.

The week’s movement continue to be constrained by near term resistance levels which could be acting as short term restraint to a break out from current levels.

The week’s movement continue to be constrained by near term resistance levels which could be acting as short term restraint to a break out from current levels.

The average PE ratio for the Junior Market Top stocks is 7.5 and 6.8 in the main market, these compare favourably with 13.7 for the overall main market and 13.4 for Junior Market, based on 2017 estimated earnings. With several stocks trading below the average, the potential for more gains for the rest of 2017 seems positive, barring any major negative developments.

In the main market, decline in the prices of Seprod down to $30 and Sterling Investments to $15.50 moved them into the top list and replaced Berger Paints and Scotia Group that maintained their prices and are now some distance from the top list.

Recent TOP 10 listings that remain just below the top spots include Access Financial that hit a new record high close of $50 and Blue Power up to $55 at the close of the week.

Cable Bahamas list on JSE Friday

This Friday June 2, will see the latest listing of a new company on the Jamaica Stock Exchange. The Bahamian based Cable Bahamas will see its shares available for trading on the local exchange for the first time.

This Friday June 2, will see the latest listing of a new company on the Jamaica Stock Exchange. The Bahamian based Cable Bahamas will see its shares available for trading on the local exchange for the first time.

Earlier this month the exchange approved the listing of the company’s shares. Information available to IC Insider.com is that the list will be on the US dollar exchange and will comprise ordinary and preference shares.

According to the company’s financials there are 43,884,754 ordinary shares and 8 different category of preference shares issued. The net asset value of the ordinary shares are around BH$2 each but the stock trades in the Bahamas at BH$4.05, with 1,000 units trading. Selling by investors is at $4.40 and above with buying interest at $4.05 and below. The 52 weeks high is $6.76 on June 9, 2016 and a low of $3.80, on the 9th of February, this year.

Revenue earned for the 2016 December quarter, was BH$47.887 million compared to BH$41.730 million and for the year to December BH$180.588 versus BH$165.678. The company reported losses of BH$9.2 million in the December quarter inclusive of a fixed asset write off of BH$5.8 million and $7.8 million for the year. Total shareholders’ equity stood at BH$91 million at the end of December 2016 and losses incurred in the March 2017 quarter of BH$7 million pushed shareholders’ equity down to BH$84 million at the end of March this year. Revenues in the March 2017 quarter rose 17 percent to $51 million up from $43.7 million in 2016 but operating cost jumped even faster by 60 percent to $46.6 million from $29 million with depreciation and amortization rising from $9 million to $16.8 million.

Two other listing should be heading to the market within weeks as Stationery and Supplies and the Musson subsidiary Productive Business Solutions with operations in the Caribbean, Central America and the USA come to the market with a US$41 million offer of ordinary shares.