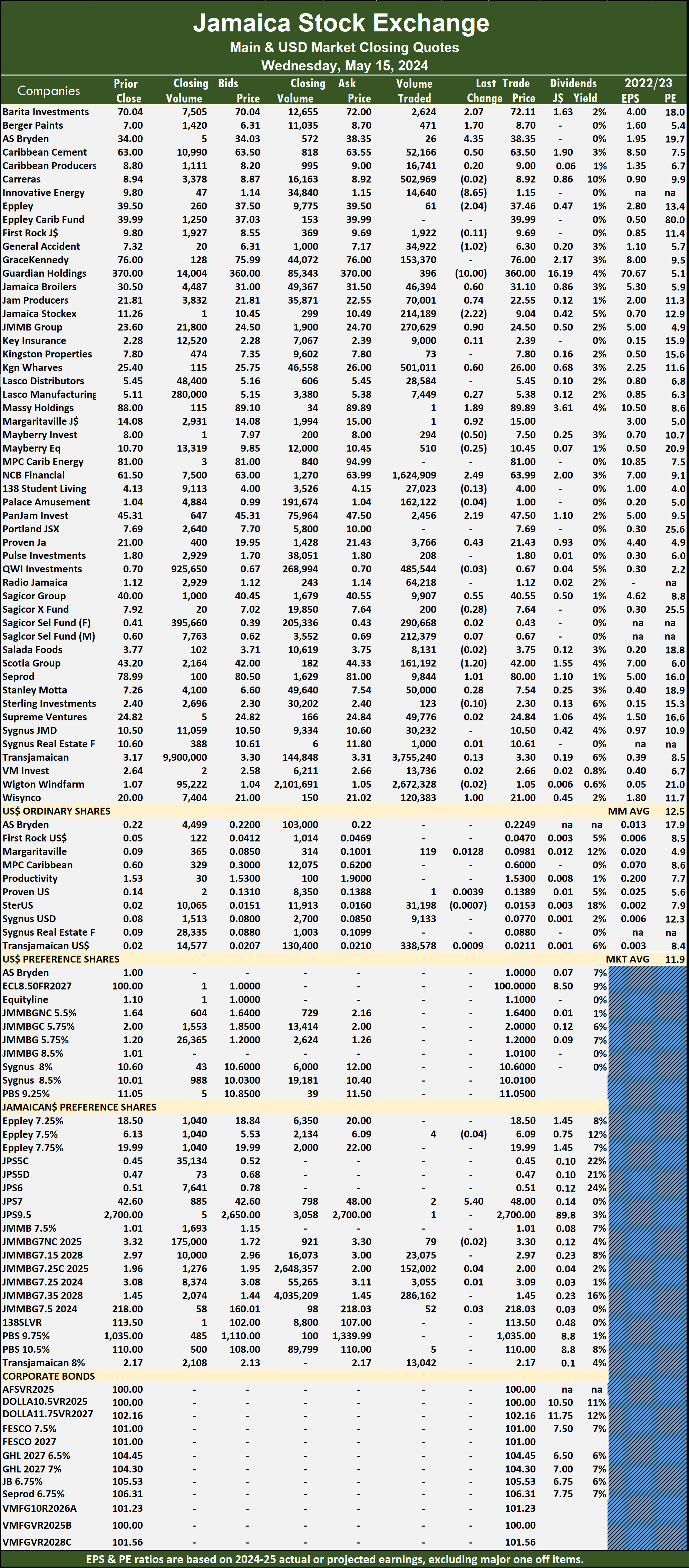

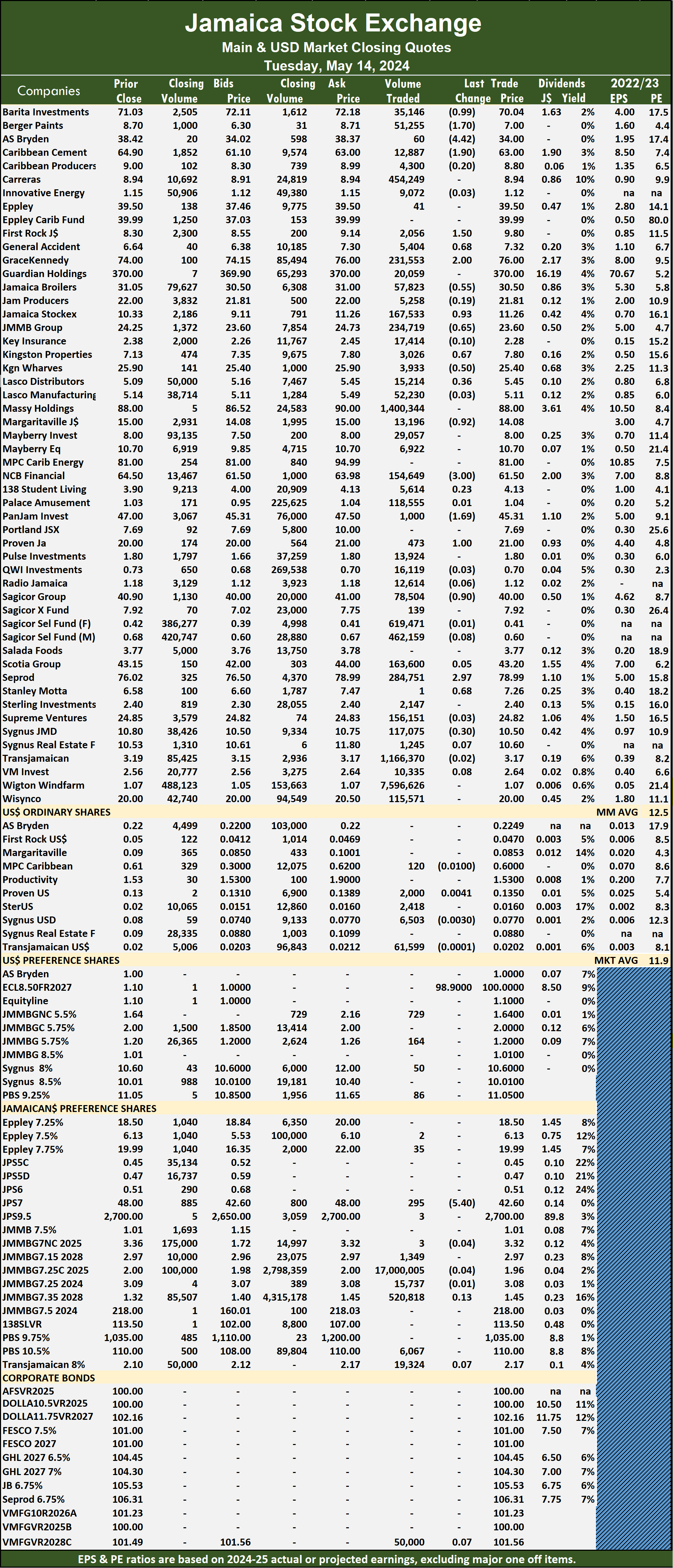

Seprod reported a hike in profit of 14 percent for the six months to June this year, slower than the 34 percent increase in the first quarter. The company posted profit of $698 million for the half year, up from $614 million in 2013 and $298 million in the quarter versus $317 million in the 2013 quarter.

Seprod reported a hike in profit of 14 percent for the six months to June this year, slower than the 34 percent increase in the first quarter. The company posted profit of $698 million for the half year, up from $614 million in 2013 and $298 million in the quarter versus $317 million in the 2013 quarter.

Seprod, involved in the manufacturing and processing of food products, oils, sugar, milk as well as a food product distribution business, enjoyed an 8 percent rise in revenues to $8 billion from $7.4 billion and 12 percent to $4.17 billion in the second quarter from $3.7 billion in the 2013 June quarter. While revenues climbed, Seprod suffered a reversal in the positive gains in investment income in 2013 with a fall of $110 million in the quarter and $118 million in the half year.

Gross profit grew a very strong 53 percent in the June quarter and a much lower 32.8 percent for the six months over the same period in 2013. Gross profit margins climbed to 29.70 percent in the June 2014 quarter, up from only 18.8 percent in 2013, for the six months 29.7 percent and 22.7 percent, respectively. These are good signs of an improving performance of the group. A major part of the improved performance, is the contribution the sugar manufacturing segment made.

Segment results show operating profit for the half year rising 61 percent, against revenues climbing only 11.4 percent, Distribution segment’s operating profit, fell from $99 million to $68 million. The group’s sugar operations made a loss of $15 million in the June quarter for the group net of minority interest and $30 million for the six months, a big improvement over the $166 million lost for the June quarter last year, and $200 million for the six months to June, 2013.

The group is now in the last six months of the year, when little income will be generated from the sugar operation at Golden Grove Sugar Factory in St Thomas. The cost associated with this operation will be absorbed and will dent profits in other areas. For the second half of 2013 the group picked up $322 million in losses from the sugar operation. Much progress has been made in reducing losses in the sugar operation but there is still some way to go to move to a profitable business. A lot will depend on increasing significantly, the amount of canes to be milled by the factory and by extension the sugar to be produced. They now need to produce around 3,000 to 4,000 tonnes more sugar, to break even.

Expenses| Selling expenses rose sharply by 43 percent in the quarter to $142 million compared with $100 million in 2013 and 22 percent for the six months to $241 million from $198 million. Administrative cost rose 25 percent to $428 million in the quarter versus $373 million in 2013. For the six months period, it rose only 7 percent from $784 million to $839 million.

Finances| Seprod has $4 billion in cash and investments. Borrowing stood at $2.55 billion up from $2.26 billion at June 2013, current assets are well in excess of current liabilities by more than 2 to 1 and equity stands at a strong $10 billion.

Longer term| For 2015 and beyond, a lot is predicated on the fortunes of the sugar operations in St Thomas, where the target is for the processing of 300,000 tonnes of canes and to produce around 25,000 tonnes of sugar. In 2013, Management indicated that the cane farms are already planted and increased production should be coming in from the 2014 crop. For the 2014 crop the factory, reached its highest-ever production levels, with 19,300 tonnes of sugar.

the group produced profits of $907 million last year and is expected to better this in 2014 by some. The stock remains buy rated.

Search Results for: SEPROD

Sugar helps Seprod hike profit

Seprod considering a dividend

Seprod advised that at a meeting of the board to be held on October 6, 2014, a dividend payment will be considered.

Seprod advised that at a meeting of the board to be held on October 6, 2014, a dividend payment will be considered.

Seprod paid a dividend of 55 cents per share on July 4, this year. Last year a dividend of 30 cents per share was paid on November 15 and 53 cents per share on July 8.

Seprod reported a hike in profit of 14 percent for the six months to June this year, slower than the 34 percent increase in the first quarter. The company posted profit of $698 million for the half year, up from $614 million in 2013.

Seprod added, others now BUY RATED

Seprod is added to the BUY RATED list for the first time, as profit seems to be settling down with reduced losses in the sugar production operations. The PE for the stock is currently at 4.4, with an eye on 2015 when results should get even better.

Radio Jamaica is now elevated to BUY RATED list, from market watch, based on a big improvement in the first quarter results, to June and IC Insider’s forecast for earnings of 35 cents per share for the fiscal year. The stock is trading at $1.22, giving it a very attractive PE of 3.

Cargo Handlers third quarter results is up on 2013, putting earnings in 2015 in the $3.40 per share level and close to $3 per share for 2014 fiscal year, to September, putting the PE at 5. Berger Paints Jamaica is moved to the BUY RTAED list, with gains in its first quarter results, to June and IC Insider forecasting of 43 cents per share earnings, for the year to March 2015. The prices of Consolidated Bakery, Caribbean Flavours and Paramount Trading, have all pulled back sharply from earlier levels making them more attractive buys.

Supreme Ventures and Jamaica Stock Exchange are added to the Market Watch list. The latter is based on a virtual wipe out of losses in the June quarter and an eye on the stock market activity that should be picking up going forward and thus enhancing the earnings and the value of heightened trades.

Supreme Ventures and Jamaica Stock Exchange are added to the Market Watch list. The latter is based on a virtual wipe out of losses in the June quarter and an eye on the stock market activity that should be picking up going forward and thus enhancing the earnings and the value of heightened trades.

Cable & Wireless is still on the list with good top line growth, coming mainly from strong mobile growth. The company is heading for a break even position or small profit for the current fiscal year. Supply of the stock is low and a big payoff should take place in 2015, if the present trend in revenue continues.

Profit up, margins shrink at Seprod

Shrinking margins and lower gross profit could not prevent Seprod from enjoying a bump in profit of $312 million in the June quarter versus $161 million in 2012 and $542 million for the six months period versus $453 million in 2012.

Seprod got a boost of $107 million from the sales of equities in the June quarter. Also in the quarter, they benefitted from a gain of $54 million from holding of assets in foreign currency. Finance and other operating income rose to $112 million in the quarter, up from $80 million in 2012 and for the six months, $206 million versus $167 million. Management has kept selling and administration cost under control with both areas falling in the latest quarter and just rising slightly for the year to date period. Selling expenses which came out at $100 million for the quarter was $6 million less than in 2012 and admin cost came out at $372 million versus $374 million in 2012. For the six months, selling expenses climbed by $4 million to $198 million and admin went to $784 million up from $751 million in 2012. Finance cost moved up to $42 million from $26 million in the June quarter and in the six months period, it rose from $48 million in 2012 to $82 million in the latest period.

Revenues | Revenues were down 2 percent in the first quarter, falling to $3.7 billion and off by $74 million from the year ago period. However, revenues increased by a healthy 17 percent to $3.7 billion in the June quarter and is up 7 percent for the 6 months to June.

The biggest issue the company is currently having is a sharp fall in profit margin. To June 2012, gross profit as a percentage of direct cost was 28.2 percent and has fallen to 24 percent for the 6 months to June this year and to only 21 percent versus 24 percent in the June quarter. The deterioration has occurred in the distribution segment as profit stagnated at $99 million, a slight 3 percent rise in that area while sales rose 11.5 percent. In the manufacturing segment, profit is up by 12.5 percent to $893 million and revenues is up 3.5 percent to $4.7 billion.

Earnings per share for the 6 month period is $1.05 and the full 12 months to December should be around $1.80-$2.

Finances | Seprod has $3.9 billion in cash and investments. Borrowing is at $2.26 billion up a billion dollars from June 2012. Current assets are well in excess of current liabilities by 3 to 1 and equity stands at a strong $9.6 billion.

Longer term | Seprod has never been one of those sexy companies but it has done remarkably well since listing back in the 1990s. It appears that for 2014 and beyond a lot is being predicated on the fortunes of the sugar operations in St Thomas where the target for sugar production is the processing of 300,000 tonnes of canes that should work out to around 25,000 tonnes of sugar. Management indicates that the expanded canes farms are already planted and the production should be coming in the 2014 crop. The group acquired Bowden Estates with 3,000 acres along with another property in the area and lands that were in bananas have now been planted out in canes. Management states that the sugar company is critical to them as a foreign exchange earner that can supply foreign currencies for the group when needed.

Related posts | Seprod’s dividend consideration | What’s really up at Seprod?

Seprod’s dividend consideration

The Board of Directors of Seprod Limited will meet to consider the payment of a dividend at a meeting scheduled for June 3, 2013. The company last paid a dividend amounting to $0.30 per share on November 9, 2012. Prior to the November payment the company paid a dividend of $0.53 per share on August 7, 2012.

Seprod recently reported profits for the first quarter of this year that was down on the similar quarter in 2012. Profit after tax profit slipped to $231 million compared to $292 million in the 2012 first quarter.

For the last IC Insider report ‘What’s really up at Seprod‘, Click here

What’s really up at Seprod?

Revenues are down to $3.6 billion for the March quarter for Seprod, who manufactures and processes oils, fats, cornmeal, soaps, milk, sugar and run a cattle farm. In the 2012 period, the group recorded revenues of $3.7 billion. Profit followed in the path of revenues slipping to after tax profit of $231 million compared to $292 million in the 2012 first quarter. While sales declined, cost of sales moved up, resulting in just over $100 million less gross profit. Costs in other areas were kept well within the amounts for the previous year. Had it not been for a significant foreign exchange gains, the decline in profits would have been far worse than reported.

It was the cash generated from operations that is eye catching with nearly $500 million generated in the first quarter this year. Those figures translate to $2 billion per annum. However, these numbers include income from the sugar operations and for the rest of the year this operation will provide no sales for fresh inflows. The company also benefited from $95 million in FX gains which is unlikely to recur this year. Hence, the cash inflows will be much less and more likely to be just over a billion dollars for the full year. Loan payment of $330 million has to be made in the next 12 months and could reduce the net cash inflows along with the payment of dividends which would use up more than $400 million.

Seprod has $3.7 billion in cash and investments plus $253 million to be collected from short term receivable in the next 12 months from March. The big question is, what are the funds being piled up for?

Seprod has $3.7 billion in cash and investments plus $253 million to be collected from short term receivable in the next 12 months from March. The big question is, what are the funds being piled up for?

Sugar operations | Long term loans increased by $977 million in the quarter primarily for use in the sugar operations. The target for sugar production is based on processing 300,000 tonnes of cane that should work out to around 25,000 tonnes of sugar and that all depends on the sucrose contents of the canes. Added to that, St Thomas, where the operations are, has heavy rainfall close to the beginning and the end of the crop each year. The timing to reap is critical in maximizing the quantity of sugar that is extracted from the canes.

Management indicates that the expanded cane farms are already planted and the increased production should be coming in the 2014 crop. The group acquired Bowden Estates with 3,000 acres and another property in the area plus lands that were in bananas are now planted out in cane. For the current year’s crop 18,000 tonnes of sugar were produced at about a break even level. If the important things go well and they make close to next year’s target, the operations should end with a profit.

Management states that the sugar company is critical to them as a foreign exchange earner for the group. The sugar factory can be pushed up to grind 400,000 of cane but no decision has been taken on that. It would require major capital injection to get to that level of production. The cost of energy for the group is an important area of focus and thought has been given to increase the generation of power at the sugar factory and wheel it to others in the group. The estimate for such a project would be in the order of US$15 million, which would allow for the installation of new broilers to power the factory using bagasse, the byproduct of cane milling, to generate heat and steam for electricity thus cutting the overall energy cost for the group.

Management states that the sugar company is critical to them as a foreign exchange earner for the group. The sugar factory can be pushed up to grind 400,000 of cane but no decision has been taken on that. It would require major capital injection to get to that level of production. The cost of energy for the group is an important area of focus and thought has been given to increase the generation of power at the sugar factory and wheel it to others in the group. The estimate for such a project would be in the order of US$15 million, which would allow for the installation of new broilers to power the factory using bagasse, the byproduct of cane milling, to generate heat and steam for electricity thus cutting the overall energy cost for the group.

The company indicates that they are always on the lookout for acquisition. The funds being built up are to allow for acquisitions when suitable ones arise as well as for capital spend. But the main focus is to fully turn around the Duckenfield sugar operations. That objective is important since Seprod profits have been stagnated subsequent to their investment in sugar production. It has proven much more difficult than most of the directors first thought possible. At the first annual general meeting, one shareholder warned them of the challenges they were going to meet. Three to four years later and after more capital injection than originally contemplated, management has had enough time and experience to appreciate the unsolicited advice.

Notwithstanding the challenges faced, the group is in a very healthy financial state with $9 billion in equity and a relatively small amount of debt. Working capital is also in good nick as well.

Stock outlook | The company’s stock last traded at $15 and seems fully valued based on current market conditions. Investors will need to bear in mind the softening in the price of sugar on the world market and commodity prices in general which could push up the breakeven level and continue to have a drag on profits as well as eat up more capital. These risk factors need to be factored in when considering the investment in this stock.

Grace pushes JSE trading on Friday

A surge in trading on the Jamaica Stock Exchange Main Market ended on Friday, with a 336 percent jump in the volume of stocks traded with a value of 1,246 percent more than on Thursday, after investors traded nearly 5.3 million shares in GraceKennedy and ended trading in 57 securities compared with 54 on Thursday, with prices of 22 stocks rising, 24 declining and 11 ending unchanged.

The market closed with 26,822,609 shares trading for $484,009,143 up from just 6,147,676 units for a mere $35,957,977 on Thursday.

The market closed with 26,822,609 shares trading for $484,009,143 up from just 6,147,676 units for a mere $35,957,977 on Thursday.

Trading averaged 470,572 shares at $8,491,388 up sharply from 113,846 units at $665,888 on Thursday and month to date, an average of 434,071 units at $2,732,653 compared with 431,153 units at $2,272,278 on the previous day and April that closed with an average of 680,802 units at $3,619,595.

JMMB Group 7.25% preference share due 2024 led trading with 13.0 million shares for 48.5 percent of total volume followed by GraceKennedy with 5.27 million stocks for 19.6 percent of the day’s trade, Wigton Windfarm with 3.31 million units for 12.3 percent market share, Carreras with 1.87 million stock units for 7 percent of trading and Transjamaican Highway with 1.47 million shares for 5.5 percent of total volume.

The All Jamaican Composite Index climbed 1,282.66 points to 358,400.25, the JSE Main Index increased 854.69 points to end trading at 321,317.22 and the JSE Financial Index rose 0.34 points to settle at 68.27.

The All Jamaican Composite Index climbed 1,282.66 points to 358,400.25, the JSE Main Index increased 854.69 points to end trading at 321,317.22 and the JSE Financial Index rose 0.34 points to settle at 68.27.

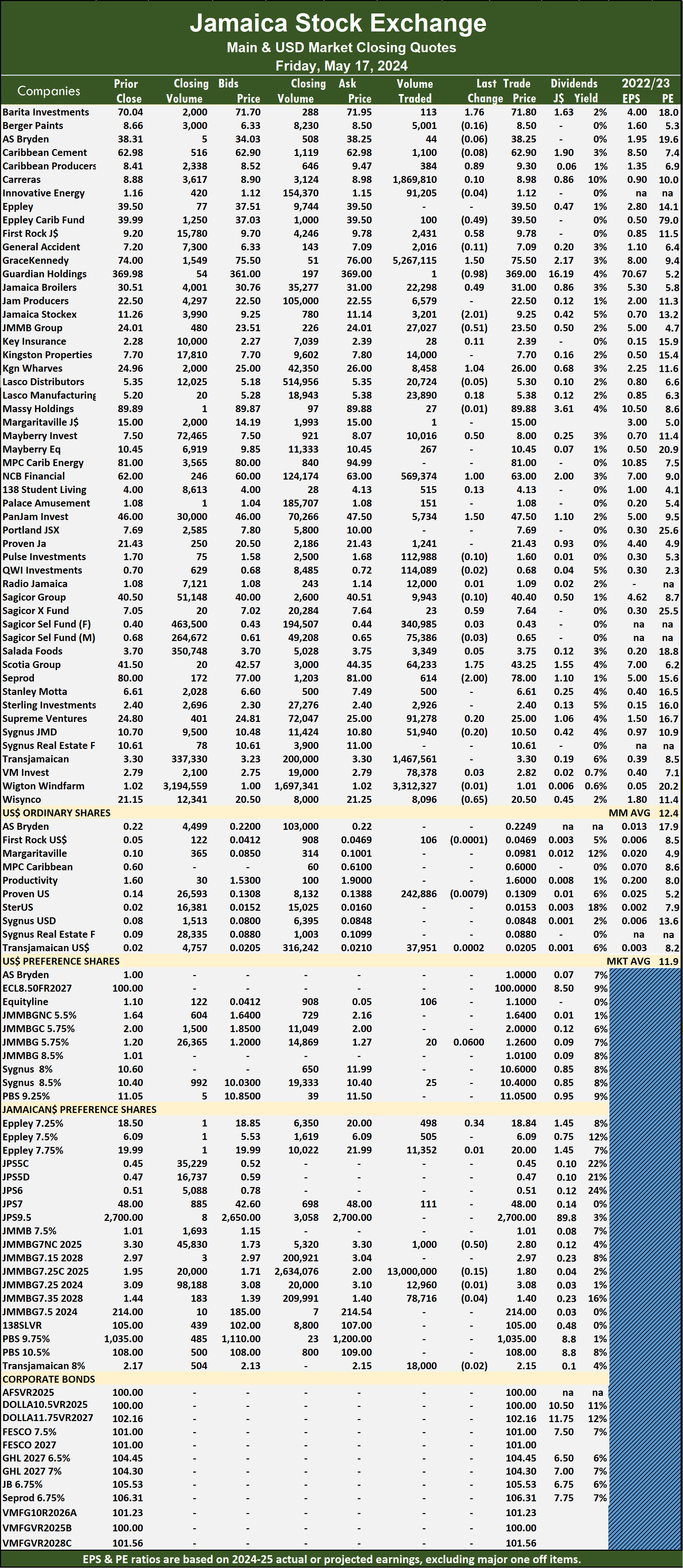

The Main Market ended trading with an average PE Ratio of 12.4. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with financial year ending around August 2025.

Investor’s Choice bid-offer indicator shows eight stocks ended with bids higher than their last selling prices and one with a lower offer.

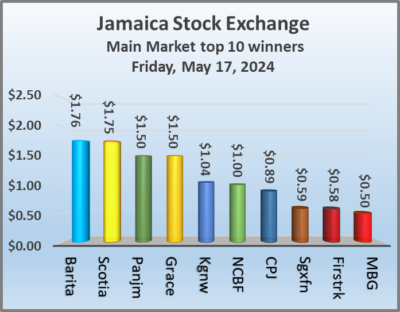

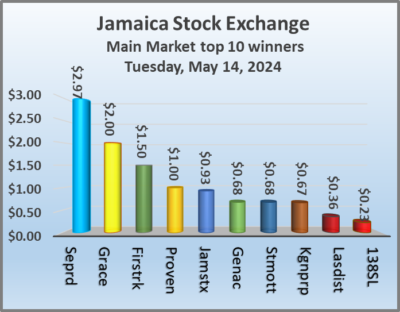

At the close, Barita Investments rose $1.76 and ended at $71.80 with traders dealing in 113 shares, Caribbean Producers rallied 89 cents to $9.30, with 384 stocks crossing the exchange, Eppley Caribbean Property Fund slipped 49 cents to finish at $39.50 with investors swapping 100 shares. First Rock Real Estate increased 58 cents to end at $9.78 in an exchange of 2,431 stock units, GraceKennedy climbed $1.50 in closing at $75.50 with investors dealing in 5,267,115 shares, Guardian Holdings fell 98 cents to close at $369 in switching ownership of 1 stock unit.  Jamaica Broilers popped 49 cents to close at $31 after 22,298 units crossed the market, Jamaica Stock Exchange sank $2.01 to close at $9.25 after an exchange of 3,201 stocks, JMMB Group shed 51 cents to end at $23.50 after 27,027 units were traded. Kingston Wharves advanced $1.04 to close at $26 with an exchange of 8,458 stocks, Mayberry Group gained 50 cents in closing at $8 as 10,016 shares passed through the market, NCB Financial rose $1 to end at $63 as investors exchanged 569,374 stock units. Pan Jamaica gained $1.50 to close at $47.50 with a transfer of 5,734 shares, Sagicor Real Estate Fund popped 59 cents to close at $7.64 after an exchange of 23 stocks, Scotia Group rallied $1.75 in closing at $43.25 with investors transferring 64,233 units. Seprod declined $2 to end at $78, with 614 stock units changing hands and Wisynco Group lost 65 cents to finish at $20.50 after an exchange of 8,096 shares.

Jamaica Broilers popped 49 cents to close at $31 after 22,298 units crossed the market, Jamaica Stock Exchange sank $2.01 to close at $9.25 after an exchange of 3,201 stocks, JMMB Group shed 51 cents to end at $23.50 after 27,027 units were traded. Kingston Wharves advanced $1.04 to close at $26 with an exchange of 8,458 stocks, Mayberry Group gained 50 cents in closing at $8 as 10,016 shares passed through the market, NCB Financial rose $1 to end at $63 as investors exchanged 569,374 stock units. Pan Jamaica gained $1.50 to close at $47.50 with a transfer of 5,734 shares, Sagicor Real Estate Fund popped 59 cents to close at $7.64 after an exchange of 23 stocks, Scotia Group rallied $1.75 in closing at $43.25 with investors transferring 64,233 units. Seprod declined $2 to end at $78, with 614 stock units changing hands and Wisynco Group lost 65 cents to finish at $20.50 after an exchange of 8,096 shares.

In the preference segment, Eppley 7.25% preference share increased 34 cents and ended at $18.84 with investors trading 498 stock units and JMMB Group 7% preference share dropped 50 cents to $2.80 after a transfer of 1,000 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

JSE Main Market rose on reduced trading

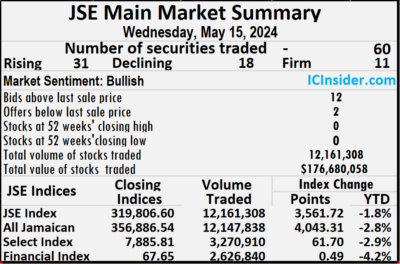

Stocks mostly rose at the close of trading on the Jamaica Stock Exchange Main Market on Wednesday, with the volume of stocks traded declining 61 percent valued 33 percent lower than on Tuesday, with trading in 60 securities up from 59 on Tuesday, with prices of 31 stocks rising, 18 declining and 11 ending unchanged.

Trading closed with an exchange of 12,161,308 shares for $176,680,058 compared to 31,493,482 stock units at $262,090,658 on Tuesday.

Trading closed with an exchange of 12,161,308 shares for $176,680,058 compared to 31,493,482 stock units at $262,090,658 on Tuesday.

Trading averaged 202,688 shares at $2,944,668 compared to 533,788 units at $4,442,215 on Tuesday and month to date, an average of 457,154 units at $2,403,909 compared with 482,643 units at $2,349,743 on the previous day and April that closed with an average of 680,802 units at $3,619,595.

Transjamaican Highway led trading with 3.76 million shares for 30.9 percent of total volume followed by Wigton Windfarm with 2.67 million units for 22 percent of the day’s trade and NCB Financial with 1.62 million units for 13.4 percent of the day’s trade.

The All Jamaican Composite Index jumped 4,043.31 points to cease trading at 356,886.54, the JSE Main Index rallied 3,561.72 points to lock up trading at 319,806.60 and the JSE Financial Index popped 0.49 points to finish at 67.65.

The Main Market ended trading with an average PE Ratio of 12.5. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending around August 2025.

Investor’s Choice bid-offer indicator shows 12 stocks ended with bids higher than their last selling prices and two with lower offers.

Investor’s Choice bid-offer indicator shows 12 stocks ended with bids higher than their last selling prices and two with lower offers.

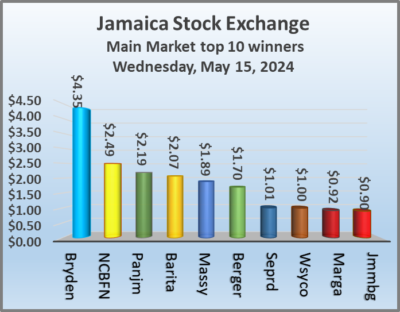

At the close, AS Bryden popped $4.35 to end at $38.35, with 26 stock units clearing the market, Barita Investments rallied $2.07 to $72.11 with traders dealing in 2,624 shares, Berger Paints increased $1.70 and ended at $8.70 and closed with an exchange of just 471 units. Caribbean Cement climbed 50 cents to close at $63.50 with investors dealing in 52,166 stocks, Eppley dipped $2.04 to finish at $37.46 in trading 61 shares, General Accident sank $1.02 in closing at $6.30 after exchanging 34,922 stocks. Guardian Holdings dropped $10 to $360 with investors transferring 396 units, Jamaica Broilers rose 60 cents to close at $31.10 in switching ownership of 46,394 stocks, Jamaica Producers gained 74 cents to end at $22.55 with investors swapping 70,001 shares. Jamaica Stock Exchange shed $2.22 in closing at $9.04 with an exchange of 214,189 stocks, JMMB Group advanced 90 cents and ended at $24.50 after 270,629 units passed through the market, Kingston Wharves rose 60 cents to $26 after an exchange of 501,011 stocks.  Margaritaville climbed 92 cents and ended at $15 with investors trading just one share, Massy Holdings popped $1.89 to $89.89 in an exchange of a mere one stock unit, Mayberry Group lost 50 cents to close at $7.50, with 294 units crossing the market. NCB Financial gained $2.49 to finish at $63.99 in an exchange of 1,624,909 stock units, Pan Jamaica rallied $2.19 to $47.50, with 2,456 shares changing hands, Proven Investments advanced 43 cents in closing at $21.43 with 3,766 units crossing the exchange. Sagicor Group gained 55 cents to $40.55 in trading 9,907 stocks, Scotia Group slipped $1.20 to close at $42, with 161,192 stock units crossing the market, Seprod popped $1.01 in closing at $80 as investors exchanged 9,844 shares and Wisynco Group advanced $1 and ended at $21 after a transfer of 120,383 stocks.

Margaritaville climbed 92 cents and ended at $15 with investors trading just one share, Massy Holdings popped $1.89 to $89.89 in an exchange of a mere one stock unit, Mayberry Group lost 50 cents to close at $7.50, with 294 units crossing the market. NCB Financial gained $2.49 to finish at $63.99 in an exchange of 1,624,909 stock units, Pan Jamaica rallied $2.19 to $47.50, with 2,456 shares changing hands, Proven Investments advanced 43 cents in closing at $21.43 with 3,766 units crossing the exchange. Sagicor Group gained 55 cents to $40.55 in trading 9,907 stocks, Scotia Group slipped $1.20 to close at $42, with 161,192 stock units crossing the market, Seprod popped $1.01 in closing at $80 as investors exchanged 9,844 shares and Wisynco Group advanced $1 and ended at $21 after a transfer of 120,383 stocks.

In the preference segment, Jamaica Public Service 7% rose $5.40 to finish at $48 with a transfer of 2 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

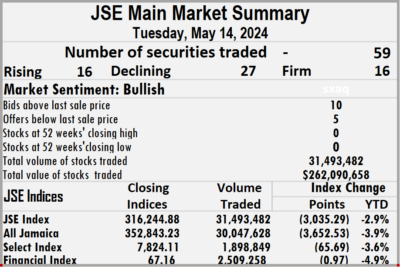

Falling stocks crush risers

Stocks closed mostly lower on the Jamaica Stock Exchange Main Market on Tuesday, with trading in 59 securities compared with 57 on Monday, resulting in prices of 16 stocks rising, 27 declining and 16 ending unchanged, following a sharp pullback in the volume of stocks traded, with a decline of 82 percent with the value 53 percent lower than on Monday.

The market closed with 31,493,482 shares being traded for $262,090,658 down sharply from 176,820,638 units at $563,186,691 on Monday.

The market closed with 31,493,482 shares being traded for $262,090,658 down sharply from 176,820,638 units at $563,186,691 on Monday.

Trading averaged 533,788 shares at $4,442,215 compared to 3,102,116 units at $9,880,468 on Monday and month to date, an average of 482,643 units at $2,349,743 compared to 477,055 units at $2,121,121 on the previous day and April that closed with an average of 680,802 units at $3,619,595.

JMMB Group 7.25% preference share due 2024 led trading with 17.0 million shares for 54 percent of total volume followed by Wigton Windfarm with 7.6 million units for 24.1 percent of the day’s trade, Massy Holdings with 1.40 million stocks for 4.4 percent market share and Transjamaican Highway with 1.17 million units for 3.7 percent of total volume.

The All Jamaican Composite Index dropped 3,652.53 points to end at 352,843.23, the JSE Main Index declined 3,035.29 points to 316,244.88 and the JSE Financial Index skidded 0.97 points to settle at 67.16.

The Main Market ended trading with an average PE Ratio of 12.5. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending around August 2025.

Investor’s Choice bid-offer indicator shows 10 stocks ended with bids higher than their last selling prices and five with lower offers.

Investor’s Choice bid-offer indicator shows 10 stocks ended with bids higher than their last selling prices and five with lower offers.

At the close, AS Bryden sank $4.42 to finish at $34 in switching ownership of 60 shares, Barita Investments skidded 99 cents and ended at $70.04, with 35,146 stock units crossing the market, Berger Paints dropped $1.70 to $7 in trading 51,255 units. Caribbean Cement dropped $1.90 to close at $63 after an exchange of 12,887 stocks, First Rock Real Estate popped $1.50 in closing at $9.80 with investors swapping 2,056 shares, General Accident climbed 68 cents to end at $7.32, with 5,404 units crossing the market. GraceKennedy rose $2 to $76 as investors exchanged 231,553 stocks, Jamaica Broilers fell 55 cents to end at $30.50, with an exchange of 57,823 stock units, Jamaica Stock Exchange rallied 93 cents in closing at $11.26 with investors dealing in 167,533 shares. JMMB Group declined 65 cents and ended at $23.60 after 234,719 stocks crossed the exchange, Kingston Properties increased 67 cents to finish at $7.80 with traders dealing in 3,026 units, Kingston Wharves shed 50 cents to close at $25.40 with 3,933 stock units clearing the market. Lasco Distributors gained 36 cents to end at $5.45 with a transfer of 15,214 shares, Margaritaville dipped 92 cents to end at $14.08 after 13,196 stock units passed through the market, NCB Financial slipped $3 in closing at $61.50, with 154,649 stocks changing hands. Pan Jamaica lost $1.69 and ended at $45.31 after a transfer of 1,000 units, Proven Investments advanced $1 to finish at $21 in trading 473 shares, Sagicor Group dipped 90 cents to close at $40 in an exchange of 78,504 stocks. Seprod rose $2.97 to $78.99 with investors trading 284,751 units, Stanley Motta gained 68 cents to finish at $7.26 after an exchange of one stock unit and Sygnus Credit Investments sank 30 cents and ended at $10.50 with investors transferring 117,075 shares.

Lasco Distributors gained 36 cents to end at $5.45 with a transfer of 15,214 shares, Margaritaville dipped 92 cents to end at $14.08 after 13,196 stock units passed through the market, NCB Financial slipped $3 in closing at $61.50, with 154,649 stocks changing hands. Pan Jamaica lost $1.69 and ended at $45.31 after a transfer of 1,000 units, Proven Investments advanced $1 to finish at $21 in trading 473 shares, Sagicor Group dipped 90 cents to close at $40 in an exchange of 78,504 stocks. Seprod rose $2.97 to $78.99 with investors trading 284,751 units, Stanley Motta gained 68 cents to finish at $7.26 after an exchange of one stock unit and Sygnus Credit Investments sank 30 cents and ended at $10.50 with investors transferring 117,075 shares.

In the preference segment, Jamaica Public Service 7% shed $5.40 to close at $42.60 in an exchange of 295 units.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

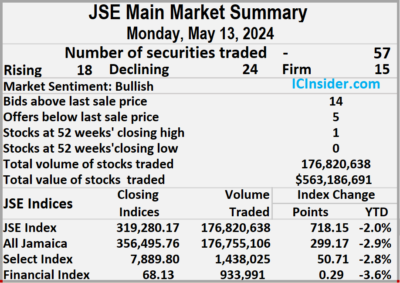

Transjamaican big trade day

Transjamaican Highway ended the trading of 172 million shares to dominate market activity on the Jamaica Stock Exchange Main Market on Monday, with the volume of stocks traded in the overall market surging 998 percent, valued 307 percent more than on Friday, with trading in 57 securities down from 62 on Friday and ending with prices of 18 stocks rising, 24 declining and 15 ending unchanged.

The market closed with 176,820,638 shares trading for $563,186,691 well up from a total of 16,107,185 units at $138,294,154 on Friday.

The market closed with 176,820,638 shares trading for $563,186,691 well up from a total of 16,107,185 units at $138,294,154 on Friday.

Trading averaged 3,102,116 shares at $9,880,468 compared to 259,793 units at $2,230,551 on Friday and month to date, an average of 477,055 units at $2,121,121 compared with 167,265 units at $1,205,421 on the previous day and April that closed with an average of 680,802 units at $3,619,595.

Transjamaican Highway led trading with 172.15 million shares for 97.4 percent of total volume followed by Wigton Windfarm with 1.87 million units for 1.1 percent of the day’s trade and Carreras with 686,809 units for 0.4 percent market share.

The All Jamaican Composite Index increased 299.17 points to end the day at 356,495.76, the JSE Main Index climbed 718.15 points to 319,280.17 and the JSE Financial Index advanced 0.29 points to 68.13.

The Main Market ended trading with an average PE Ratio of 12.4. The JSE Main and USD Market PE ratios are based on the last traded prices and earnings forecasts by ICInsider.com for companies with the financial year ending around August 2025.

Investor’s Choice bid-offer indicator shows 14 stocks ended with bids higher than their last selling prices and five with lower offers.

Investor’s Choice bid-offer indicator shows 14 stocks ended with bids higher than their last selling prices and five with lower offers.

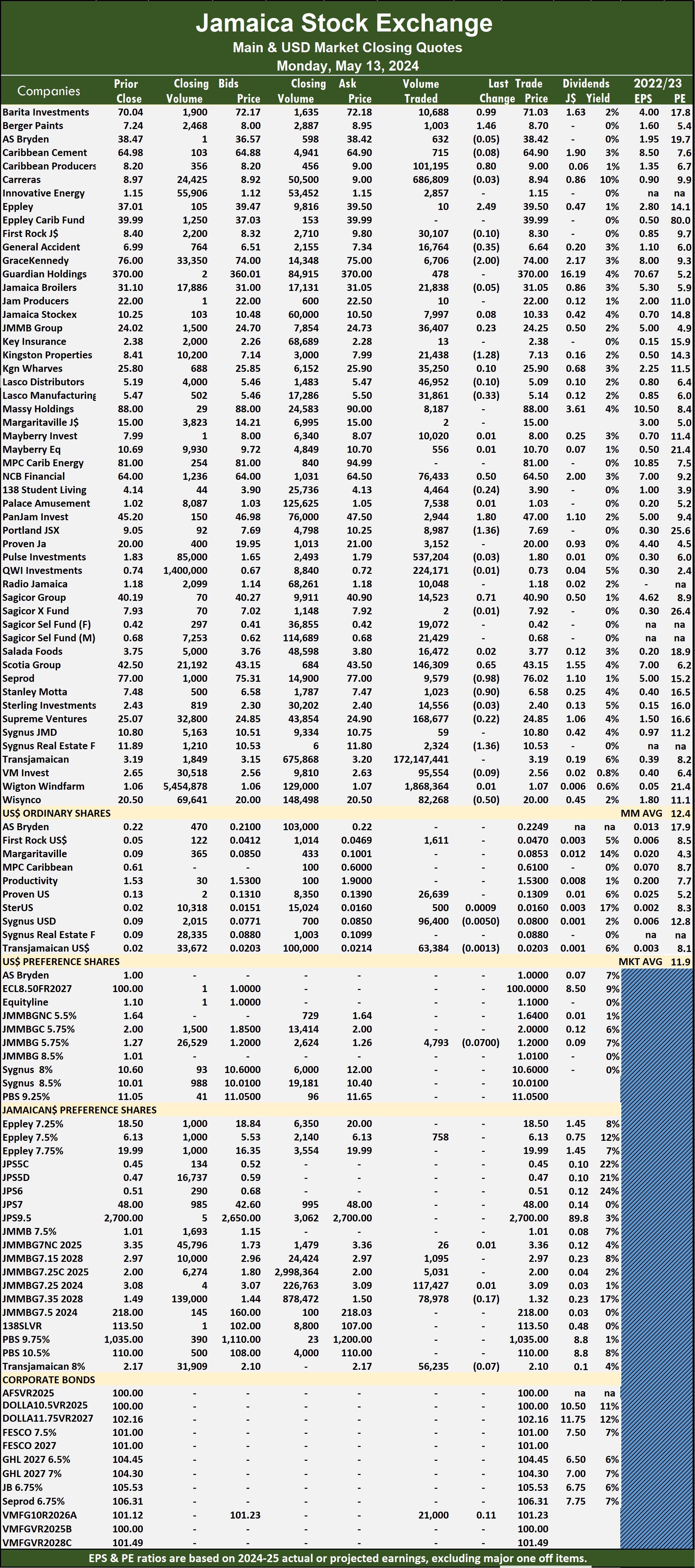

At the close, Barita Investments climbed 99 cents in closing at $71.03 after exchanging 10,688 shares, Berger Paints rose $1.46 to a 52 weeks’ high of $8.70 with investors swapping 1,003 stocks, following the release of solid first quarter results last week, Caribbean Producers advanced 80 cents to finish at $9 after 101,195 shares changed hands. Eppley popped $2.49 and ended at $39.50 as investors exchanged 10 stock units, General Accident sank 35 cents to close at $6.64 with 16,764 shares clearing the market, GraceKennedy dropped $2 to end at $74 with an exchange of 6,706 units. Kingston Properties lost $1.28 to $7.13, with 21,438 stocks crossing the market, Lasco Manufacturing fell 33 cents to finish at $5.14 with investors dealing in 31,861 stock units, NCB Financial gained 50 cents and ended at $64.50 with a transfer of 76,433 shares.  Pan Jamaica rallied $1.80 to end at $47 after 2,944 stock units crossed the exchange, Portland JSX skidded $1.36 in closing at $7.69 in trading 8,987 stocks, Sagicor Group increased by 71 cents to close at $40.90 after 14,523 units passed through the market. Scotia Group climbed 65 cents to $43.15 in an exchange of 146,309 stocks, Seprod shed 98 cents to close at $76.02 with traders dealing in 9,579 units, Stanley Motta declined 90 cents and ended at $6.58 after an exchange of 1,023 shares. Sygnus Real Estate Finance dipped $1.36 to finish at $10.53 with investors trading 2,324 stock units and Wisynco Group slipped 50 cents to end at $20 after a transfer of 82,268 shares.

Pan Jamaica rallied $1.80 to end at $47 after 2,944 stock units crossed the exchange, Portland JSX skidded $1.36 in closing at $7.69 in trading 8,987 stocks, Sagicor Group increased by 71 cents to close at $40.90 after 14,523 units passed through the market. Scotia Group climbed 65 cents to $43.15 in an exchange of 146,309 stocks, Seprod shed 98 cents to close at $76.02 with traders dealing in 9,579 units, Stanley Motta declined 90 cents and ended at $6.58 after an exchange of 1,023 shares. Sygnus Real Estate Finance dipped $1.36 to finish at $10.53 with investors trading 2,324 stock units and Wisynco Group slipped 50 cents to end at $20 after a transfer of 82,268 shares.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.

Prices of securities trading are those for the last transaction of each stock unless otherwise stated.