Investors’ attention turned to the Junior Market in both 2020 and 2021 as that market provided better values for stocks and therefore greater opportunities to make higher profits. Projected earnings of the listed companies suggest that the situation is unlikely to change in 2022.

Investors’ attention turned to the Junior Market in both 2020 and 2021 as that market provided better values for stocks and therefore greater opportunities to make higher profits. Projected earnings of the listed companies suggest that the situation is unlikely to change in 2022.

The Main Market of the Jamaica Stock Exchange eked out a modest gain of 1.1 percent in the All Jamaica Composite index at the end of 2021, the index was 21.7 percent lower than the end of 2019.

The PE for the Main market is 14 times 2022 earnings compared to 16 based on 2021 earnings, that does not suggest a big uptick for the market with just a 14 percent increase expected in 2022 over 2021 that would push the index to 499,694 points, still well below the 559,853.26 points the market closed out 2019 at.

There are several stocks in the market, data suggest could more than double in 2022 and investor would be wise to not only pay attention but pick up some of these undervalued stocks in preparation for long term growth as the Jamaican economy rebounds and move into a new stage of long term positive growth that a number of these companies will benefit from.

Banks could be amongst the big performer as they shed the need for continued heavy provisioning of loans as well as grow their book of loans to deliver more income to profits. Added the increase in interest rates will help improve their net interest income.

Banks could be amongst the big performer as they shed the need for continued heavy provisioning of loans as well as grow their book of loans to deliver more income to profits. Added the increase in interest rates will help improve their net interest income.

ICInsider.com data indicates that there are 8 stocks that can double in the Main Market in 2022 into early 2023. 2021 finished with several stocks trading at or above 20 times earnings in the Main Market if that level of valuation continues into 2022 and is more widespread, then the gain in the market could exceed the above potential gains. In the final analysis, the market index is just a simple measure as to how the overall market is doing. It comes down to individual stocks that can do well and that is the case for ICInsider.com TOP15 stocks.

Profit surges 146% at AMG Packaging

ICInsider.com TOP15 2022 selection, AMG Packaging released first quarter results to November, with revenues climbing 55 percent to $270 million from $174 million in 2020 and delivered profit before tax of $45.5 million, 187 percent above just $16.4 million in 2020 and profit after tax rose 146 percent to $35 million from $14.3 million in 2020. The company reported profit after tax of $60.6 million or 12 cents per share for the fiscal year to August 2021.

The latest results were helped by a foreign exchange gain of $4.7 million in the quarter from a loss of $6 million in 2020.

The latest results were helped by a foreign exchange gain of $4.7 million in the quarter from a loss of $6 million in 2020.

Gross profit rose 40 percent from $53 million to $74 million as input cost rose a bit faster than revenues at 61 percent to $196 million from $121 million in 2020.

Administrative and other costs rose modestly from $32.2 million to $33.3 million.

Cash inflows amounted to $52 million up from$23 million in 2020. Working capital needs and acquisition of fixed assets amounting to $18 million resulted in an increase in cash funds of $5 million and ended in cash on hand at $135 million.

AMG new factory space that will house the new machine.

Investment in Fixed assets stood at $468 million up from $362 million in 2020, with current assets at $503 million which includes Inventory of $207 million up from $129 million at the end of November 2020. Current liabilities stood at $197 million while long term liabilities were $102 million and shareholders equity at $643 million.

ICInsider.com projects full year earnings at 35 cents as the results for the full year will benefit from increased efficiencies to flow from the new box making machine that is now on site, with installation expected to be completed in February. the new machine will print in multi colours and open up new business opportunities for the company.

The stock closed on the Junior Market of the Jamaica Stock Exchange today at a new closing high of $3.40 and a PE of 9.7.

The stock traded at the beginning of October last year at $1.70 and is up 100 percent since then.

Profit drop at Elite but watch this stock

Revenue of $118 million for the first quarter in 2020 fell 7 percent to $110 million in the first quarter to September 2021, resulting in a loss of $10.3 million compared to a profit of $16.7 million the previous year for Elite Diagnostic.

Reduced revenues impacted profit margin with a decline to 61.4 percent from 66.25 percent in 2020 and from 63.3 percent for the fiscal year to June. Input cost climbed 6 percent to $42 million from $40 million and gross profit fell 14 percent to $67 million from $78 million.

On the surface, the last reported results for the company may drive fear into the minds of investors but that would lead to a miss of potentially profitable investment for the future. “Net profit was impacted by increased administrative expenses, depreciation and foreign exchange losses”, management advised shareholders in their commentary on the results.

Elite Diagnostics

The report to shareholders continued, “revenue was affected by Covid-19 with reduction of operating hours and reduced procedures. Currently, the company’s operational hours are back to normal. An unusually lengthy breakdown of the CT also impacted our revenues during the quarter. Along with our regular preventative maintenance of the machines, the company has invested in equipment and parts to reduce some of the downtimes of the machine breakdowns”.

“The St Ann location revenue is increasing month over month since all modalities became operational in the first quarter of 2020. The company is cautiously optimistic as the effects of Covid-19 more negatively impact the rural areas of the country. The company continues to see steady demand for imaging services at all locations.”

Administrative expenses rose 13.5 percent to $46 million in the quarter from $40 million and depreciation jumped 44 percent to $25 million from $17.4 million in 2020. Finance cost was steady at $10 million, while foreign exchange movement resulted in a $3 million swing from a surplus of $1 million in 2020 to a loss of $2 million in 2021.

In spite of the loss incurred in the quarter, gross cash flow was positive with inflows of $15 million, down from $28 million in 2020. Additions to fixed assets offset by loan inflows utilized just over $15 million as net cash outflow for the period ended at $503,581. At the end of September, shareholders’ equity stood at $449 million, long term loans at $209 million and short term loans at $10 million. Current assets ended at $679 million, including trade and other receivables of $44 million, cash and bank balances of $39 million. Current liabilities ended the period at just $20 million, with net current assets ending at $659 million.

The results ended with earnings per share being a loss of 3 cents for the quarter, down from 4 cents for the quarter in the prior year. Based on the latest results, most investors would be looking elsewhere for investment opportunities. In doing so, they could miss one of the biggest winners in 2022. IC Insider.com forecasts 30 cents per share for the fiscal year ending June 2022, with a PE of 10 times the current year’s earnings based on the price of $3.05 the stock traded at the Jamaica Stock Exchange Junior Market. The company has more room for revenue growth from the addition of new equipment, continued growth in the relatively new St Ann location and additional branches in the future.

Drax Hall branch of Elite.

The company paid a dividend of 9 cents in October this year 2021. Net asset value is $1.29, with the stock selling at just over 2.4 times book value.

Reporting to shareholders in the annual report for the year to June, the chairman, Steven Gooden, stated, “we have been fortunate to see an increased demand for imaging services and were prudent to have sought to capitalize on this demand – through the acquisition of new equipment. We will continue to pursue this growth strategy by installing a new MRI system at the Liguanea branch, which we anticipate will be operational beginning early 2022. This new machine, we expect, will serve to reduce the company’s operating hours and thereby its related expenses. Additionally, with the St Ann branch issues finally resolved, the location is now operating at the desired capacity. Looking ahead, the near to medium term holds the classic combination of challenge and opportunity.On the one hand, we see continued challenges in terms of rising prices, compounded by the depreciation of the local currency; the company pays all its rent and purchases equipment and supplies from overseas in US dollar, so any depreciation in the dollar will affect the bottom line. On the other hand, we also see our cash flows remaining stable, if not strong, amid the continued high demand for our services. The demand is so strong that, were it not for dealing with the issues associated with the Drax Hall branch, the company might well have advanced plans for another branch. We intend to approach growing the company’s footprint with alacrity and all seriousness in the coming year”.

Caribbean Cream stock for the main course in 2022

Sale revenues rose 16 percent for the half year, to August 2021 $1.03 billion from $891 million but rose a mere 5.4 percent for the August quarter, to $486 million from $461 million in 2020 at ice cream maker Caribbean Cream. Management attributed the poorer second quarter performance to the several no movement days imposed by the government during the quarter.

Profit melted in the quarter by 85 percent to just $7 million from $47 million in 2020 and fell 17 percent for the six months to August, to $61 million from $74 million in 2020.

The company has not had a consistent and predictable profit outcome for some years, still, the trajectory has generally been up. In 2019 the company posted $89 million after tax that fell to $55 million in 2020 and $101 in 2021. The 2022 fiscal year profit is poised to beat that of 2021, notwithstanding the setback in the second quarter.

Caribbean Cream posted significant gains in profit in Q1.

Improvement in profit margin in the first half of the year was consistent at 41 percent, with the prior year’s six months but has increased over the 37 percent achieved for the fiscal year to February 2021. But it fell from 50 percent in the 2020 august quarter to 44 percent in 2021. The effect, operating profit fell 6 percent in the quarter to $215 million from $230 million but increased 15 percent for the year to date, to $423 million from $369 million in 2020.

Administrative expenses excluding depreciation rose 25.4 percent to $134 million in the quarter and increased 32 percent in the six months to $249 million, from $188 million in 2020. Sales and distribution expenses increased 8 percent to $30.5 million from $28 million in 2020 for the half year and were virtually flat at $15.5 million for the second quarter. Depreciation charge rose from $59 million in 2020 to $62 million in 2021 for the six months. Finance cost rose in the quarter to $6.7 million from $6 million in 2020 and $9 million to $12 million for the six months.

Gross cash flow brought in $151 million versus $160 million in 2020. Working capital growth used up all but $13 million in 2021 versus $81 million used up in 2020. Additions to fixed assets consumed $83 million for the 2021 half year versus $62 million in 2020. Loan repayment and paying $26 million dividends resulted in outflows of $114 million. At the end of December, shareholders’ equity stood at $869 million, with long term borrowings at $303 million and short term loans at $13 million. Current assets ended the period at $408 million, including trade and other receivables of $65 million, cash and bank balances of $103 million. Current liabilities ended the period at $173 million. Net current assets ended the period at $235 million.

The results in the past few years being inconsistent does not mean that the future will continue in that vein. One focus is on taking a more significant share of the market for ice cream and related products while finding avenues to cut costs. The company announced earlier this year that in collaboration with Power Factor Technologies, a power engineering services company, they embarked on a major project to install a 630 kilowatt capacity Combined Heat & Power plant fueled by LNG at the company’s premises. This project is scheduled to come on stream at the start of 2022 and is expected to generate considerable cost savings and should have a positive impact on results for 2022 onwards.

The stock closed 2021 at $5.70 with a PE ratio of 9 much lower than the average for the market around 15 and below many Junior Market stocks trading around 20 times earnings.

Sharp rebound for Dolphin Cove

In March 2020, Jamaica closed its borders to incoming visitors by planes and ships as a result of the emergence of the deadly Covid-19 virus, thus bringing to a halt the important tourist industry and many others that relied on it.

The impact was immediate and devastating to the entertainment attraction entity, Dolphin Cove based in Ocho Rios, with locations on the north coast of the island. For the nine months to September 2020, the company posted revenues of just US$3.6 million and a loss of $864 million, with the September quarter generating revenues of just $320,000 and a loss of $590,000. By the third quarter last year, cruise shipping from which it generates a large portion of income had just 8,381 visitors in 2021 compared to 219,000 for the first nine months of 2019, but visitor arrivals by planes were back to 70 percent of the 2019 numbers for the third quarter and 54 percent in the June quarter and by November last year arrivals were down around 20 percent from the same month in 2019, an indication that the industry could well be nearly back on track in 2022 and provide a considerable boost to the company’s revenues.

Dolphin Cove closed at a 52 weeks’ high on Monday.

The company lost US$1.13 million for 2020, but chalked up a profit of $1 million in the 2021 third quarter, from $2.57 million in operating revenues, and a profit of $2.1 million for the nine months from operating revenues of $5.44 million. While revenues rose 51 percent in the nine months, expenses fell from $3.5 million to $2.9 million, with all categories of cost falling except for finance that rose from $96,000 to $215,000. Although operating revenues spiked 703 percent over the measly income for September 2020 quarter, direct expenses rose 61 percent to $258,000 and other operating expenses rose 139 percent from $548,000 to $1.31 million. The above numbers suggest that costs are down generally, it appears that some costs may have been fully trimmed from the system.

Gross cash flow brought in $2.5 million but growth in working capital, addition to fixed assets resulted in negative funds flow of $149,000 for the nine months. At the end of September, shareholders’ equity stood at US$29 million. Total long term borrowings amount to US$820,000 with bank overdraft at $1 million. Current assets ended the period at $6 million including trade and other receivables of $2.7 million, cash and bank balances of $2 million. Current liabilities ended the period at $2.6 million. Net current assets ended the period at $2.4 million.

At the end of December, the stock traded at $15 with a PE of 11 with the earnings per share of $1.35 and a PE of 5 with ICInsider.com projected earnings of $3 for the current year.

The Junior Market could gain 60% in 2022

The Junior Market continues to offer opportunities for supper stock performance in 2022 with an average PE for the market at 9 times 2022 earnings versus close to 15 at the end of 2021, and offering a potential gain of more than 60 percent to the end of 2022. There are 26 Junior Market stocks that can double in 2022.

The market is technically at a support level that is steering the index upwards, more importantly, it is caught in a triangular formation that is set to push the market sharply upwards once it breaks out, which is not far off. The market is also trading in a channel that goes back to May 2020 and is pointing to a record high of more than 4,000 points in a few months.

Last year finished with a number of stocks trading at or above 20 times earnings in the Junior Market if that level of valuation continues into 2022 then the gain in the market could exceed the above potential gains.

The market will continue to benefit from the recovery of some of the companies that suffered major fallout due to the restrictions placed on operations as a result of the COVID19 epidemic in 2020 into 2021. Stocks that could benefit in a big way are, Access Financial, Main Event, Everything Fresh, Express Catering, Knutsford Express, Jetcon Corporation, Dolphin Cove and Stationery and Office Supplies.

Access Financial – Earnings per share are projected at $4.80 for the year to March 2023 and $2.60 for the 2022 fiscal year to March. The company showed signs of recovery from the beating taken in 2020 and 2021 as a result of steep provisioning for doubtful loans and a slowdown in lending. That situation started to reverse in 2021 up to September with loans net of doubtful loans up to $4.38 billion versus $3.9 at the end of September 2020. Revenues and profit in 2021 tripled the September 2020 quarter and the 2020 half year results. This trend is expected to gather pace in 2022 and beyond. See full article on the company recently published.

Access Financial – Earnings per share are projected at $4.80 for the year to March 2023 and $2.60 for the 2022 fiscal year to March. The company showed signs of recovery from the beating taken in 2020 and 2021 as a result of steep provisioning for doubtful loans and a slowdown in lending. That situation started to reverse in 2021 up to September with loans net of doubtful loans up to $4.38 billion versus $3.9 at the end of September 2020. Revenues and profit in 2021 tripled the September 2020 quarter and the 2020 half year results. This trend is expected to gather pace in 2022 and beyond. See full article on the company recently published.

AMG Packaging – Earnings per share is projected at 35 cents for the year to August 2022 as new machinery facilitates cutting costs and creating more flexibility in the manufacturing operations. See full article on the company recently published.

Caribbean Brokers – Earnings per share is projected at 40 cents for 2022. The company reported strong earnings in the September quarter, with EPS at 41 cents for the quarter and 33 cents for the nine months. The company tends to get the bulk of its income in short periods with the other quarters reflecting relatively lower income that does not cover the cost. Unfortunately, the company failed to provide investors with appropriate information to fully glean what the results will mean for the full year and beyond. The end result is that the stock has suffered from investors’ interest when it really should have surged well over $4 per share, based on the latest results and what can be expected for the full year.

Elite Diagnostic – Earnings per share are projected at 80 cents for the year to June 2023. The stock is under pressure but that is due to investors not paying adequate attention to what the company is doing and the improvement in sales, quarter over quarter as well as the strong cash flow it’s generating. See full article on the company recently published.

Medical Disposables – Earnings per share are projected at $1.50 cents for the year to March 2023.

Technical indicators for the Junior Market are pointing to a record high of more than 4,000 points in a few months.

Profit after taxation surged 455 percent to $21.5 million for the second quarter to September from a loss of $6 million in 2020. For the year to date, profit after tax spiked 458 percent to $47 million, up from a loss of $13 million in 2020. Income from sales jumped 49 percent to $936 million for the September quarter, up from $630 million in 2020 and climbed 42 percent for the six months ended September 2021 to $1.62 billion, from $1.14 billion in the prior year. The acquisition of majority ownership of Cornwall Enterprises along with new distributorships helped in fueling the sales surge. See full article on the company recently published

Caribbean Cream – Earnings per share is projected at $1.30 cents for the year February 2023 from 65 cents projected for the 2021 fiscal year. Management is building an enterprise that can go up against the competition successfully and deliver superior returns for shareholders. They have cut costs in the past two years and grew their market reach by setting up a distribution depot in the Ocho Rios region that helped to push sales. The implementation of their own power generating plant will lead to a reduction of energy and other utility costs. Excluding the slowdown in sales in the August quarter when the government introduced no movement days, sales increase is been robust and is expected to be on track again for the second half of the year into the 2023 fiscal year.

Dolphin Cove – Earnings per share is projected at $3 for this year and $1.35 for 2021. This company is in a period of major recovery with profit surging and set to get even better with the tourism industry rebounding strongly and closing in on 2019 arrivals. See full article on the company recently published.

Spur Tree Spices – Earnings per share is projected at 19 cents for this year. A recent IPO, this stock is set to do extremely well over the next few years. Expect local sales to surge as a result of the publicity they received due to the IPO. See full article on the company recently published.

Spur Tree Spices – Earnings per share is projected at 19 cents for this year. A recent IPO, this stock is set to do extremely well over the next few years. Expect local sales to surge as a result of the publicity they received due to the IPO. See full article on the company recently published.

Stationery and Office Supplies – Earnings per share is projected at 95 cents for the current year and reflect a full recovery from the fall out of the Covid19 disruption to sales. The company has made major strides since 2020 when sales were badly affected by the shutdown of businesses and schools. That has changed and the company posted a 175 percent increase in pre-tax profit of $78 million versus $29 million for the nine months to September 2020, from a 13.5 percent rise in revenues. Earnings per share for the third Quarter of 2021 was 8 cents, compared to 3 cents in 2020. For the 9 months ended September 2021 earnings per share was up to 31 cents from 11 cents in 2020. reports are that the company had the best four quarter in its history and the performance seems to have carried over into 2022 and should continue to be robust with opening and expansion in the wider economy.

Lasco Distributors – Earnings per share is projected at 50 cents for the year to March 2023. For the half year to September, revenues rose 15 percent to $11.6 billion and profit increased 6 percent to $615 million as margins were squeezed in the period from higher input cost, followed by delayed price increase. With price adjustments since implemented, margins should increase and result in higher profits. Revenues should pick up as tourist traffic rose sharply throughout the year and schools are now back in operation both activities will impact revenues positively.

With earnings per share of 14 cents for the half year, full year earnings should exceed 30 cents making the stock undervalued at $3.45 with a PE of 11, versus the market average of just over 14.

The company has no borrowed funds and possesses $2.8 billion in cash funds, with annual gross cash flows of over $1.2 billion.

Everything Fresh – Earnings per share is projected at 15 cents for the year. The company seems to have turned the corner with a small profit in the September quarter. Importantly, gross cash flow for the nine months to September was positive at $15 million despite a loss of $20 million. The hotel sector is enjoying a strong rise in visitor arrivals with December last year down 24 percent compared to 2019 compared to a fall of 45 percent for 2021 versus 2019 preliminary data shows, this is a very positive development for the company going forward. The current year should see an even greater number of visitors that should better the performance in December. This is good news for a company that markets the bulk of sales to that sector.

Lasco Financial – Earnings per share is projected at 45 cents for the year March 2023. Net Profit for the second quarter ended at $134 million compared with $30 million in the similar period of 2020. The second quarter suffered revenue reduction from $617 million in 2020 to $554 million in 2021, due to disruption in business during the period as a result of no movement days, while cost rose from $400 million to $424 million leaving profit after tax at $59 million from $136 million in 2020. Earnings per share ended September at 10.5 cents and that should climb sharply in the second half with the impact of the high volume Christmas period having a positive impact. The company has cash funds of $1.7 billion at the end of the period as they curtailed lending.

Lasco Manufacturing – Earnings per share is projected at 60 cents for the year March 2023. For the half year to September, revenues rose 13 percent over the $4.1 billion generated in 2020 to $4.65 billion and profit popped 6 percent to $782 million, but the second quarter saw profit falling 3.8 percent to $380 million from revenues that increased 2.7 percent to $2.34 billion. Earnings per share came in at 19 cents for the half year on target for around 40-45 cents for the full year as margins increase based on price adjustments.

Cash on hand stood at $1.8 billion with borrowings at $600 million.

General Accident – Earnings per share are projected at 80 cents for the year.

General Accident spreading wings

Net profit after tax of $351 million, was generated for the nine months to September up from $125 million in 2020, with earnings per share of 39 cents versus 14 cents in 2020. Profit in the third quarter was $177 million compared to just $12 million in 2020. Earnings per share in the September quarter was 19 cents.

The company is in an expansion mode, with the establishment of operations in Barbados and Trinidad and Tobago, with both operations expected to break even in 2022. Higher interest rates locally and the ability to increase investment in higher yielding assets are measures expected to boost investment income in 2022.

Jetcon Corporation – Earnings per share is projected at 15 cents for the year but don’t be surprised if it ends as high as 25 cents, depending on how rapid sales increase becomes. On a recovery path from the pandemic slump in 2020, revenues to September 2021 were up 30 percent but and should end the year above that level based on what the company reported in the third quarter, that sales for the fourth quarter are strong, with units sold in November back at regular pre-pandemic levels and already exceeded sales for the third quarter, at $196 million with the upward swing continuing into December, and with increased bookings to date. The improved sales position in the final quarter should result in an increased gross profit margin and a better net position than in 2020.

The above developments augur well for 2022 that should see revenues climbing appreciably again, with growth of 50 percent not out of the picture. If that were to happen it could lift profit margins closer to 20 percent from much lower levels in 2020 and 2021.

Bonus Pick

Honey Bun is our bonus pick for the year. Earnings per share are projected at $1 for the year to September 2022, as revenues continue to climb at a healthy pace. Earnings may be too low for it to qualify for the TOP15, but the stock could double from its current price of $9.30 per share during the year.

Jamaican economy looking good for investment in 2022

Things are setting up nicely in the investment world for 2022, following two somewhat lousy years for the JSE Main Market that fell 22.6 percent in 2020 and rose a mere two percent in 2021, but technical reading is not very positive in the short term, but that is likely to change in the second half. The opposite is true for the Junior Market that is caught in a triangular formation that suggests a big break higher to take the market into record territory and most likely over the 4,000 index mark.

The genesis of such optimism is ro0ted in a number of positive developments in the wider economy and for some individual companies. Results of companies for the 2021 third quarter were some of the best seen for some time, with many doing better than in 2019, before the advent of the Covid19 that resulted in dislocation pressured the bottom line of many and for some opportunities that helped the topline and the bottom line.

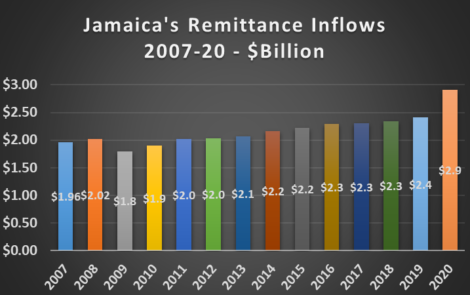

Those developments bode well for profits and stock prices in 2022 when the economy is expected to recover from the sharp decline in 2020. Remittances for 2021 are expected to be over US$600 million more than for the record $2.9 billion intakes in 2020 and the tourism industry is expected to be back at 2019 levels or close to it but is expected to far exceed that in 2020 all things being equal. More growth is expected from exports and the BPO sector, accordingly, the country should see significant additional foreign exchange inflows in 2022 than at any time in its history. Bear in mind that the signal of how well the country is doing in international trade, the net international reserves rose US$104 million in December over November to close the year at $$4 billion and is up fromUS$3.1 billion at the end of 2020. The early signal of tourism performance shows December 2021 behind a similar period in 2019 by just 24 percent compared to a fall of 45 percent for all of 2021 versus 2019.

Those developments bode well for profits and stock prices in 2022 when the economy is expected to recover from the sharp decline in 2020. Remittances for 2021 are expected to be over US$600 million more than for the record $2.9 billion intakes in 2020 and the tourism industry is expected to be back at 2019 levels or close to it but is expected to far exceed that in 2020 all things being equal. More growth is expected from exports and the BPO sector, accordingly, the country should see significant additional foreign exchange inflows in 2022 than at any time in its history. Bear in mind that the signal of how well the country is doing in international trade, the net international reserves rose US$104 million in December over November to close the year at $$4 billion and is up fromUS$3.1 billion at the end of 2020. The early signal of tourism performance shows December 2021 behind a similar period in 2019 by just 24 percent compared to a fall of 45 percent for all of 2021 versus 2019.

Unemployment will dip further in 2022 as most of the economy is expected back to near normal operations that will add to the spending power of Jamaicans and help to lift revenues.

In the financial sector, profits were on the mend and bankers are lending again with good growth taking place in the loan portfolio of some financial institutions.

Tourism expected end 2022 close to that of 2019

In 2021 banks and financial institutions with a few exceptions were pressured with the majority ending the year with a fall in price. These institutions will benefit from the rise in interest rates that will result in increased net interest income. The JSE financial index, a measure of the performance sector in 2020 down 6.5 percent for the year. The star performer was by far the Junior Market with gains of 30 percent with five stocks gaining between 95 and 266 percent.

In the second half of the year, inflation raised its head and the Bank of Jamaica hiked interest rates in response, so far there are no visible effects on the stock market, even as higher interest rates tend to negatively affect stock prices.

On the fiscal side, revenues for 2021 were healthy bettering the 2020/21 fiscal year b some distance. The effect is that the fiscal deficit should return to the 90 percent range again during 2022. Fiscal year 2022/23 should be much better and there could be some tax relief granted. It could be reduced GCT or an increase in the tax threshold. But it should stir the government into doing a comprehensive tax reform thus eliminating many of the minor tax categories. Whether there is tax relief or not, what is clear is that there will be no new taxes for the coming fiscal year.

In our 2021, ICInsider.com stated the period ahead, “seems set to be the year of surprises as many stocks that suffered badly in 2020 could be making a major turnaround in revenues and profit, while some that may not fully recover could start showing good signs of returning to normalcy.” That is exactly what happened during the year with strong gains from the likes of Caribbean Producers, Express Catering, Main Event, Medical Disposables, Radio Jamaica, Stationery and Office Supplies and Dolphin Cove, all of which suffered major setbacks in 2020.

In our 2021, ICInsider.com stated the period ahead, “seems set to be the year of surprises as many stocks that suffered badly in 2020 could be making a major turnaround in revenues and profit, while some that may not fully recover could start showing good signs of returning to normalcy.” That is exactly what happened during the year with strong gains from the likes of Caribbean Producers, Express Catering, Main Event, Medical Disposables, Radio Jamaica, Stationery and Office Supplies and Dolphin Cove, all of which suffered major setbacks in 2020.

The economy is clearly on the mend but there are still lingering concerns with the inability to seriously reduce the spread worldwide as well as in Jamaica. The latest Omicron strain is an example that we may not be out of the woods as yet. The ongoing vaccination of the population in Jamaica although not going as fast as planned continues apace and could support general positive expectations for the near term.

Importantly, PE ratios are rising as investor demand pushes values up as selling wanes at the end of 2021, the average PE ratio of the Junior Market suggests a 60 percent rise for the market while the Main Market is put at just 20 percent, with companies in the latter at a greater stage of developments than the former.

The country should see a full recovery from the important tourism sector during 2022 and this publication expects greater flows of foreign exchange with tourism back to normal and remittances holding close to the trend of 2021.

Coming soon – Junior Market could jump 60% in 2022

Berger Paints holds some promise

Berger Paints held the number one spot in ICInsider.com’s TOP15 list for 2021 based on its performance for the nine months ended September 2020, which has changed with the failure for sales growth to continue into the final quarter.

![]() Revenues climbed eight percent in the September quarter to $574 million, with a gross profit of $304 million. Profit suffered a sharp fall in the June quarter, with sales negatively impacted by the partial closure of some businesses resulting from the spread of the covid-19 pandemic in the country. Revenues for the nine months were down, with profit after tax coming in with a loss of $60 million. Revenues for the fourth quarter to December failed to enjoy the level of growth in the September quarter and dipped against the similar quarter in 2019.

Revenues climbed eight percent in the September quarter to $574 million, with a gross profit of $304 million. Profit suffered a sharp fall in the June quarter, with sales negatively impacted by the partial closure of some businesses resulting from the spread of the covid-19 pandemic in the country. Revenues for the nine months were down, with profit after tax coming in with a loss of $60 million. Revenues for the fourth quarter to December failed to enjoy the level of growth in the September quarter and dipped against the similar quarter in 2019.

Audited financials for the full year show revenue for 2020 of $2.37 billion, six percent below 2019 figures, with the fourth quarter dipping just two percent at $877 million versus $892 million in 2019. Losses suffered in the earlier part of the year were simply too much for the company to overcome and recoup. Profit before tax for the year was down a noticeable 72 percent to $12 million, but profit before tax for the December quarter of $38 million was vastly better than the loss of $9 realised in the 2019 period. The December quarter profit after tax of $32 million was vastly better than the $11 million in 2019.

Direct operating cost declined by 4 percent or just $38 million to $1.22 billion for 2021. Staff cost also declined from $558 million to $512 million.

At $211 million, cash and bank balances fell 64 percent in 2020, down from the $585 billion recorded at the end of 2019 as the company paid down the $655 million owed to fellow subsidiaries by $552 million. Current assets of $1.3 billion include trade and other receivables of $575 million and inventories of $446 million, down from $639 million in 2019.

Berger Paints is one of IC Insider’s TOP 10 stocks.

Current liabilities ended at $484 million for the financial year, down from $1 billion in 2019, with amounts owing at the end of 2020 include $148 million due to the parent company and $102 million due to fellow subsidiaries. Shareholders’ equity closed out the year at $1.15 billion. The only interest bearing debt was for leasing, amounting to $65 million.

Earnings per share for 2020 was just 5 cents compared to 14 cents in 2019. IC.com projects 2021 earnings of $1.50 as the company benefits from recovery of sales that fell out in 2020 due to the effects of Covid and increased sales from a buoyant construction sector, relatively new automotive paints and better data usage from the new IT system.

The stock last traded at $13 on the Main Market of the Jamaica Stock Exchange and is now at the lower end of the ICTOP10 stocks for 2021 at a PE of 9 times 2021 earnings, but it could surprise with better than expected results.

Why the Top 15 Junior Market stock picks?

Junior Market stocks were affected by the dislocation caused by the COVID-19 virus more than their Main Market counter path, with their prices suffering more as well, but since March last year, the Junior market delivered greater returns than the majors. For 2021 to date, Junior Market stocks are up almost 10 percent while the main market is down modestly.

ICTOP10 Junior Market stocks now.

The future for some stocks in 2021 is clear, but for others, it is a bit hazy as they await the resumption of normal business operations. This publication sets out the rationale for the TOP15 selection in the Junior Market.

Since we published the TOP 15 lists at the beginning of the year, the Junior Market is up almost 10 percent with outstanding performances from some of the selections, with most moving out of the TOP 15 lists except Grace Kennedy and Caribbean Cream. Jamaican Teas is up 69 percent, Mailpac 31 percent, Caribbean Cream 11 percent, Lumber Depot up 60 percent, QWI Investments up 38 percent, and Grace Kennedy up 19 percent.

Assumptions were made pertaining to recovery and the extent for some stocks in the TOP15 list. Some investors may start to react to recovery potential for some and drive prices up before full recovery takes place. Stocks falling into this category are Caribbean Producers, Elite Diagnostics, Express Catering, Jetcon Corporation, Main Event, Stationery and Office Supplies.

The forecast is for price movements to get to their targets by March 2022. Earnings per share for some stocks are based on 2021/22 EPS for companies with year ending up to July 2021.

Lasco Financial –EPS 50 cents Current PE 5.4

Lasco Financial made large provisions for loan losses in the 2020 fiscal year amounting to $651 million and plunged it into a $57 million loss for the year. They provided an additional $193 million in the June quarter that pushed the quarterly results into a $106 million loss.

Provision for loan losses was down to $152 million at the half-year and fell further to just $9 million for the nine months to December, thus reversing the provisions up to September.

The company recorded profit after tax for the September 2020 quarter of $136 million, with Profit after tax for the six months to September amounting to $30 million.

The December 2020 revenues were down from September by $88 million to $527 million and below the 2019 quarter by $73 million. The main reason for the fall in revenues in December versus 2019 is due to a $70 million fall in interest income from loans. Loan interest income grew from$143 million in the September quarter to $158 million in the December quarter. Profit to December is up to $154 million from $77 million in 2019. Full-year results could come in at $300 million

In their September quarterly, the company indicated that “there will now be a shift towards lending again, however, as opportunities for lending are now beginning to manifest as businesses are adjusting to the new normal, with some embracing new opportunities.” The shift to increase lending will add to revenues and profit going forward, with IC Insider.com projecting 20 cents per share to March and 50 cents for the fiscal year 2022. The company traded at $2.76 at the end of December and last traded at $2.70.

Shareholders equity stood at $1.69 billion and borrowed debt of $1.7 billion at the end of December 2020.

Caribbean Cream – EPS 95 cents Current PE 5.

Caribbean Cream – EPS 95 cents Current PE 5.

“A breath of fresh air” is how the recently opened Ocho Rios Caribbean Cream depot was described by a customer, according to the principals of the company in a report to shareholders accompanying the third-quarter results. This new location is expected to contribute positively to the growth of the product and results going forward.

For the November quarter, profit after tax grew 36 percent to $11 million and 96 percent to $85 million for the year to date. Revenue improved by 11 percent for the quarter to $441 million and eight percent for the nine-month period. Administrative and marketing expenses grew by 15 percent for the quarter and four percent for the year, totaling $127 million and $343 million, respectively.

Earnings per share doubled from 11 cents to 22 cents for the nine months and moved from two cents to three cents for the November quarter. The final quarter is the best for revenue generation and profit. Accordingly, ICInsider.com forecast is for full-year earnings of 50 cents for the year to February 2021 and 95 cents for the following year. Shareholders’ equity grew by 12 percent over November 2019 to $818 million and the company has loans payable of $226 million. The company traded at $4.20 at the end of December and at $4.65 on Friday.

Caribbean Producers – EPS 65 cents Current PE 4.

This company’s profit was badly affected by dislocation in the tourism sector and full recovery will depend on the industry recovering substantially as a large portion of its revenues is dependent on the fortunes of the sector. CPJ started their new fiscal year with an improvement over the final quarter ended in June 2020 but notably off the mark compared with the corresponding quarter for 2019.

Revenues dropped by 65 percent from September 2019 to US$9.3 million, with gross profit falling 64 percent to US$2.4 million from 2019 out turn. The improvement over the June quarter coincides with the reopening of hotels and it should pick up further with Jamaica’s tourist arrivals hitting the 90,000 mark in December, from an average of less than 50,000 in the September quarter. Revenues in the December quarter climbed further to $15 million

Selling and administrative expenses declined slower than gross profit, falling by 51 percent, while depreciation charges jumped from $767 million to $1.07 million. CPJ moved from a loss of US$258 thousand in 2019 to a loss of US$1.85 million in the September quarter and $850,000 in the second quarter.

Shareholder’s equity stood at US$15.3 million with loans payable of $30.4 million and is highly over-leveraged at the end of 2020. The overleveraging at this time is a big negative just in case things take a longer time to return to some level of normality. Regardless, this is an area of operations that needs urgent attention.

The stock is likely to be a late bloomer, with earnings per share projected at 65 cents for the 2022 fiscal year ending June, assuming near full recovery in the hotel sector. The stock traded $2.80 at the end of December and traded at $2.67 on Friday. The potential for recovery exists, but the heavy debt loan makes it a riskier investment.

Main Event revenues recovering.

Main Event – EPS 67 cents Current PE 4.6

The arrival of COVID-19 virtually crippled the entertainment industry as nighttime curfews and social distancing halted many entertainment activities, a big earnings area for the company.

For the quarter ending July 2020, revenues were slashed 87 percent to $59 million and for the nine months to July 2020, dropped 31 percent from $1.37 billion to $945 million. Expenses were down by 98 percent for the quarter to $19 million and 31 percent for the year to $521 million.

MEEG recorded a net loss of $46 million for the July quarter and a net profit of $8.7 million for the year to date.

The depreciation charge accounted for $31 million of the quarter’s loss and $95 million for the nine months, resulting in positive profit before the depreciation charge and a small quarterly cash loss in the July quarter.

For the full year, the company reported a loss of $18 million with a depreciation of $148 million for a strong positive profit before depreciation. In the final quarter, revenues climbed over July quarter by 69 percent to $101 million and recorded a much lower loss of $27 million than in the third quarter with a depreciation charge of $53 million. It is unclear when the operation will return to good health. The early signs of improved revenues and positive cash flows augur well and placed them in a good position to weather the current economic storm with positive cash flow.

Cash funds amount to $132 million and loans of $238 million. Shareholders equity stood at $534 million at October 2020.

The company traded at $3.20 at the end of December and traded at $3.04 on Friday.

Elite Diagnostic – EPS 60 cents Current PE 4.6

The company came to market in 2018, with the previous year’s pretax profit at $60 million from just one location. Since then they have tripled locations with revenues rising 67 percent from $263 million in 2018 fiscal year to $439 million last year, but profit fell sharply with startup cost out weighting revenue increase.

ICInsider.com TOP10 Main market stocks.

A number of negative developments were at play driving up cost without the necessary increase in revenues. Expansion by its very nature incurs cost ahead of revenue generation. The company encountered problems with equipment, resulting in unscheduled repairs and cost and loss of revenues and finally, the advent of Covid-19 reduced opening hours and revenues.

The first quarter numbers to September last year were heavily impacted by reduced operating hours resulting in curtailed operations. The Directors note that a CT machine was not functional for an extended period, adversely affecting procedures they were able to undertake. The compounded fallout was net loss of $10.3 million for the September quarter down 162 percent from a net profit $16.7 million recorded for the September 2019 quarter and is a slight improvement over the June quarter’s loss of $12.5 million.

For the year to June 2020, net profit came in at just $8.6 million, an 83 percent drop from the previous year’s profit of $51 million as well as a decline from a profit of $23 million up to December 2019 with the March 2020 quarter showing strong promise with revenues of $236 million and profit of $21 million.

Revenue slipped by 7 percent for the September quarter to $110 million compared to 2019 but importantly, was up 20 percent over the June 2020 quarter. Operating expenses increased by six percent year-over-year to $42 million. The Directors state that the company has seen month-over-month revenue growth at the recently opened St. Ann location and expect to positively impact revenues for 2021.

The history of the company suggests, investors need to be patient for things to return to normal and for the St Ann branch to start generating adequate revenues and then profit.

Shareholder’s equity stood at $449 million at the end of September 2020, down from $460 million at the end of June 2020 and borrowed funds stood at $219 million. At the close of 2020, Elite Diagnostic traded at $3 at the end of December and traded at $2.76 on Friday. Earnings of 60 cents per share projected for the 2021/22 fiscal year.

Jetcon Corporation – EPS 15 cents Current PE 5

Jetcon Corporation – EPS 15 cents Current PE 5

Reeling from the impact of COVID-19, profit at Jetcon dropped significantly year-over-year, for the quarter and the nine month period ending September 2020, which is expected to lead to vastly reduced 2020 full year results compared to 2019. A profit of $2 million was reported for the September quarter, down 91 percent from 2019 and $5.6 million for the year to date, a decline of 88 percent. The result was an improvement over the June’s quarter loss of $6.7 million. Sales fell 45 percent for the quarter to $153 million and by 38 percent to $467 million for the year but reflected a 78 percent improvement on the June quarter’s figures of $86 million.

Administrative and other expenses was flat at $23 million for the September quarter versus the similar period in 2019 and fell to and $71 million year to date versus $80 million in 2019.

The industry goes through years of boom and bust and could be returning to a period ahead of growth in revenues. The industry has gone through three years of declining sales, an unusual development that bodes well going into 2021 as it could mean that the downward cycle is at an end. Importantly, due to the poor sales in the second quarter last year, resulting in a loss, the company should enjoy better June quarter results all things being equal if the country continues on its current path of recovery.

Net current assets stood at $444 million at September 2020. Shareholders equity stands at $552 million and it has very limited debt that provides a good base for continued operations going forward.

The company traded at 79 cents at the end of December and traded at 77 cents on Friday with earnings per share that could rise in the region of 15 cents for 2021 assuming some major about-turn in demand for cars.

Medical Disposables – EPS 80 cents Current PE 5.6

Medical Disposables enjoyed a 12 percent increase in revenue during the quarter ending September 2020 to $630 million. For the six months, revenues hit $1.14 billion, only a two percent increase but Direct Expenses jumped 11 percent for the quarter to $480 million and $877 million for the six months. There was an after tax loss of $6 million compared to an after-tax profit of $6 million for the quarter ending September 2019. The six month figures stood at a loss of $13 million and a profit of $23 million respectively. The General Manager notes the impact of the one-off finance cost pushed the charge for the quarter to $36 million, without which the company would have generated a profit around $20 million. The company reported profit of $25 million or ten cents per share in the December quarter, up from $6.5 million in 2019, with sales rising moderately from $603 million to $626 million.

While ICInsider.com is projecting ongoing earnings of 30 cents per share for the fiscal year to March. The performance is expected to improve, with earnings of 80 cents per share for the 2022 fiscal year.

The company had net current assets of $374 million, inclusive of cash and bank balances of $23 million at the end of September, a 271 percent increase over the company’s cash position at the end of September 2019. Total equity stood at $846 million with borrowings of $735 million.

Medical Disposables ended the calendar year at $4.25 at the end of December and traded at $4.20 on Friday with earnings of 60 cents per share. Investment in the stock is not without some risk in the short term, but there could be upside surprises if the company attracts new business lines as they have been doing in recent years.

Caribbean Assurance Brokers – EPS 35 cents Current PE 5

According to the Chairman’s report decline in commission in all four divisions as well as a delayed renewal period for the international health insurance product, contributed to sluggish revenue for the period to September 2020. Total revenue for the quarter dropped 61 percent to $79 million and down by 37 percent for the nine months to $23 million. The company recorded a loss of $10 million, a drop from a profit of $62 million for the corresponding quarter in 2019. For the six-month period, losses stood at $23 million, down from a profit of $57 million recorded at the end of September 2019. Shareholders equity stood at $278 million at the end of September 2020, up from $230 million at the end of December 2019. CAB has net current assets of $107 million, a 12 percent increase over the corresponding period. At the close of 2020, the stock traded at $1.89 and at $1.76 on Friday, with earnings per share of 25 cents for 2020.

Access Financial – EPS 2.70 cents Current PE 7.6

Access Financial is the classic case where looking ahead rather than focusing heavily on the recent past can pay off richly. The advent of Covid-19 in Jamaica meant dislocations for many businesses and loss of jobs. Access had to face this onslaught head-on resulting in a massive increase in provisioning for expected credit losses. Most of that seems to be behind them now, with the September quarter showing recoveries of some doubtful loans and lower provisions made for additional expected losses. The company still provided $111 million in the quarter for doubtful debt and $178 million for the six months, compared with $105 million and $185 million in 2019 respectively and made further provision of $111 million in the December 2020 quarter, putting total provisions around $800 million and covering more than half of loans overdue for up to 30 days. This is an indication that provisions in the near future could be much more moderate than in the past two years.

Profit suffered in the current fiscal year as net profit fell 75 percent to $28.5 million for the September quarter and 77 percent to $62 million for the six-month period. For the December quarter, Profit before taxation rose to $94 million from $33 million in the September quarter, compared to $121 million in December 2019 after another round of heavy loan loss provision.

Net operating income fell 20 percent for the six months at $887 million and 20 percent from September 2019 at $457 million, but the latter was an improvement on the June 2020 quarter of $430 million, by six percent. For the December quarter, it grew to $460 million. Meanwhile, at $370 million, total interest income fell 12 percent from the September 2019 quarter versus 2019, but was down only two percent from the June quarter and increased further to $387million in the December quarter.

At the end of September, Loan receivables were down 13 percent to $3.9 billion from $4.47 billion at March 2020 and $4.4 billion at the end of September 2019 as the company increased bad debt provision curtailed lending up to that point. Loans advanced rose to just over $4 billion, which is an encouraging sign in pursue of an increase in revenues and profit going forward.

Shareholders’ equity stood at $2.3 billion. The company had loans payable of $2.65 billion, down from $3.1 billion in December 2019 and $3.2 billion at the end of March 2020. Cash and cash equivalents ended at $555 and total assets at $5.5 billion.

The stock ended trading in 2020 at $23.50 and traded at $21 on Friday. With earnings of $1 per share projected for the current fiscal year that would result in a PE ratio of 21 and a 2022 forecast of $2.70 per share, suggesting good potential upside for the stock price.

Stationery & Office Supplies – Montego Bay office.

Stationery and Office Supplies – EPS 70 cents Current PE 6

Gross profit was down 19 percent for the quarter and 26 percent for the nine months ending September closely matching the fall in sales that fell 18.6 percent to $240 million from $295 for the quarter and down 24 percent to $712 million from $933 million for the nine months to September 2020. Net profit for the quarter fell 70 percent to $7 million and 75 percent for the nine months to $29 million.

The Board of Directors notes that its third-quarter corresponded with a surge in COVID-19 cases in Jamaica. Despite falling below 2019 numbers, the company managed to improve its performance over the June quarter. SOS also acquired property on the adjoining lot and finished its new warehouse, a sign of expected growth in operations going forward.

Shareholders’ equity increased by five percent to $625 million, but net current assets fell by nine percent to $343 million, with a strong cash position of $112 million, up from $87 million at the end of September 2019 and $62.5 million at the end of December 2019, the company is set to weather the continued COVID storms.

The company should be seeing improved results in 2021, with schools and some businesses reopening, especially since June last year. The company should be seeing marked improvement in numbers in the March to September periods compared to 2020, when many businesses closed or operated with reduced activities.

The company’s stock traded at $4.54 at the end of December and on Friday at $4.50 with expected earnings of 20 cents per share for 2020. The stock is about fully valued but undervalued based on improved 2021 earnings.

Jamaican Teas CEO John Mahfood

Jamaican Teas – EPS 30 cents Current PE 11

The company enjoyed increased profit with interim results for the December first quarter of the 2021 fiscal year show sales rising 41 percent to $611 million and profit attributable to shareholders jumping 321 percent to $117 million from just $28 million in 2019.

The highlight for the quarter was the strong gain in export sales of 88 percent over the prior year. This contributed to manufacturing sales climbing 48 percent to $428 Million for the quarter.

What is known subject to continuity, since the end of the 2020 fiscal year, QWI Investments net asset value has gained 15 cents or around $200 million and with more apartment sales to be completed in the second quarter, the group should see these contributing to profit subsequent to the December quarter.

The group has borrowings of $432 million and cash funds of $317 million at the end of December. Investments amount to $1.7 billion with shareholders’ equity of $1.8 billion.

After a three-to-one stock split in November last year, the company enjoys increasing buying interest, with the price hitting record highs in recent weeks. Jamaican Teas ended the calendar year with the stock at $1.99 and traded at $3.35 on Friday. It is the leading Junior Market stock for the year to date.

General Accident – EPS 90 cents Current PE 5.6

Last year, the group recorded results of the Trinidad subsidiary, for the full year, compared to a few months in 2019, and the Barbados startup, for a shorter period. Up to the second quarter, the company seems to be bettering the operating performance of 2019 but clams provisions relating to Trinidad subsidiary. The full-year results showed profit down to 32 cents per share at $323 million for shareholders of the company.

Net premiums earned increased by 3 percent from $801 million to $823 million for the December quarter and by 14 percent from $2.45 billion to $2.8 billion for the year. Gross premium income jumped 52 percent from $1.78 billion to $2.7 billion in the final quarter and 12 percent from $10.7 billion to $12 billion with insurance ceded rising sharply. Claim expenses rose in the quarter from $218 million to $428 million and for the year by 49 percent from $1.2 billion to $1.79 billion. Management expenses slipped by 4 percent for the quarter to $348 million from $361 million and rose 21 percent for the year from $992 million to $1.2 billion. Investment income dropped for the quarter from $116 million to $61 million and fell from $230 million to $202 million for the year. Other income also fell in both periods, with the year ending at $19 million from $202 million.

It is the performance in 2021 that is important and that should climb nicely with the expansions getting more matured, while the Jamaican operation continues to add to profit.

Shareholders’ equity was $2.6 billion at the end of December. The company traded at $6.19 at the end of December and traded at $5.30 on Friday with earnings of 32 cents per share.

Lumber Depot dominated trading with

Lumber Depot – EPS 22 cents Current PE 12.5

Lumber Depot operates a full-service hardware store and acquired the assets and liabilities of the Lumber Depot business from the Blue Power Group effective August 2019.

Net profit jumped 76 percent for the October quarter from $20.5 million to $36.1 million and ended at $66 million for the six months to October 2020, representing a 79 percent increase from the corresponding period in which the business operated in the prior half in its own right as under the Blue Power group for a quarter.

The company recorded revenue of $338 million for the quarter, a seven percent year-over-year improvement. Administrative expenses fell 15 percent to $39 million for the quarter ending at $77 million for the half-year.

“We have had downturns in some areas that have impacted us, such as the Gordon Town Road collapse but we are able to see improvements in sales in other areas that have helped to balance any shortfalls. Revenues and profits continue to be steady similar to the 2nd quarter which you will see when our next set of financials are published, “ the company’s Chief Accountant, Adrienne Jones, informed ICInsider.com in response to a request about the company’s operations currently.

Shareholders equity grew by 34 percent to $258 million from $192 million at the end of April 2020. The stock price was $1.56 at the end of December and traded at $2.50 on Friday. Earnings per share came in at 5 cents for the quarter and nine cents for the half-year is projected by ICInsider.com at 20 cents for the current fiscal year and 22 cents for the 2022 fiscal year.

Lasco Distributors – EPS 40 cents Current PE 8.5

Profit before taxation increased by 55 percent year-over-year for the December quarter moving from $188 million to $291 million. Pre-tax profit for the nine months climbed 41 percent from $618 million to $870 million. Taxation tripled for the quarter to $48 million and more than doubled for the nine-month period from $60 million to $139 million, leaving net profit rising 41 percent from $172 million to $243 million for the quarter and by 31 percent to $731 million for the nine months.

Revenue improved by six percent for the quarter to $5.2 billion and for the nine-month period to $15.2 billion. Operating expenses declined by 11 percent for the quarter and 12 percent for the nine months to $663 million and $2.02 billion, respectively, as management focused on cutting cost.

The company does all the sales for the manufacturing company; as such improved sales by them will positively impact revenues and profit.

Cash and investments climbed to $2.3 billion at the end of 2020, while shareholders equity stood at $6 billion at the end of December 2020 while borrowings were negligible. Lasco Distributors last traded at $3.68 on Friday with projected earnings of 30 cents per share to March and 40 cents for 2022.

Mailpac – EPS 30 cents Current PE 12

The Group continues to enjoy increasing strong profit growth despite the current pandemic, with revenue jumping 58 percent in the September quarter over the 2019 quarter, with profit more than doubling, helped by a is healthy profit margin at 62 percent. Revenues climbed from $301 million to $477 million and grew a stunning 30 percent over the June 2020 quarter with $366 million. For the year to September, revenues rose to $1.2 billion, 42 percent more than the $851 million recorded at the end of September 2019.

The company recorded a net profit of $149 million for the quarter, a solid 129 percent jump from the $65 million recorded for the September 2019 quarter. For the year-to-date, there was an even more sizeable growth of 150 percent, moving from $203 million in 2019 to $339 at the end of September 2020.

For the full year to December, Mailpac reported a 42 percent increase in revenues for the December quarter with a $512 million realised profit of $104 million, up from $97 million pretax for 2019. Cost of sales jumped 70 percent for the final quarter, much higher than the increase in revenues. Profit for the year ended at $443 million, with earnings per share of 18 cents with the increased direct cost in the final quarter robbing it of greater earnings. IC Insider.com believes that this type of business will continue to grow as persons are attracted to the convenience that the service affords.

At the end of December, cash and equivalent stood at $292 million, while Shareholders’ equity stood at $571 million with little or no borrowings. A dividend of 6 cents was declared, payable in March and brought the total for the year to 15 cents.

The stock ended 2020 trading at $2.87 at the end of December and traded at $3.75 on Friday but traded as high as $4.43 in February before pulling back to close at $3.75 on Friday. ICInsider.com projects earnings per share of 30 cents for 2021.

45% gains for ICTOP15 stock

Robust gains for some stocks after less than a month of trading in 2021 have shaken up ICTOP 15 stocks forcing a number of them out or at the edge of moving out of the 2021 TOP list. Jamaican Teas now the lead stock for the year, dropped out of the Junior Market list this week, with a rise of 45 percent since the start of the year.

Jamaican Teas is the leading JSE stock for 2021 to date with a 45% increase in price.

This brings to two, stocks that have migrated from the Junior Market TOP15 so far. Jamaica Producers fell out of the Top 15 Main Market list with the price dropping to $19.81, from $21 but Margaritaville suffered a greater fall to replace it.

Jamaican Teas one of the top 15 stocks for 2021 scaled record highs this past week as more and more investors piled into the stock since the three for one stock split in November last year. The gain also follows the directors’ report for the September quarter results that stated “Subsequent to the year-end, overall sales increased by 47 percent in October 2020, with export sales increasing 85 percent and a 10 percent increase in domestic sales. We have good orders in hand for November and these developments, along with booking of more real estate sales, hopefully, improvement in the investment portfolio should result in a good first quarter for the financial year 2021.”

Mailpac was the first to drop out of the list and now has gains of 29 percent so far in 2021. Lumber Depot surged to $2.10 on Friday but closed at $1.95 from $1.46 last week and now sits at 15th spot on the Junior Market TOP15 for 2021, with a 25 percent gain for the year to date. Reports in the newspapers indicate bullish sales expectations from Caribbean Cement and rising prices for some construction inputs.

MailPac is the Junior Market second-best performing stock for 2021.

The news pushed investors to snap up Lumber Depot stock and drove the price much higher, since. QWI Investments is up 17 percent since the end of last year to trade at 90 cents with the net asset value rising since the latter part of last year to sit at $1.18 as gains in both local and overseas stocks continue to add to the value of the company’s portfolio. The stock is now at 14th spot on the Main Market list. A large number of shares were overhanging the market and pressuring the stock price. Once they were bought out, the supply has shrunken leaving room for the price to recover.

Caribbean Cream posted eleven percent growth in sales for the November quarter and eight percent for the nine months, with profit rising 96 percent for the nine months and a 37.5 percent increase for the third quarter. The stock is up 18 percent for the year at the close on Friday and remains at the seventh position on the 2021/22 TOP15 list.

With interest rates at low levels on government bonds and expected to remain low for a protracted period, investors are becoming more comfortable with PE of 20 times earnings or more, according to the TOP 15 rankings the above stocks still have room to gain over 90 percent from the current price for the rest of the year.

It pays to read ICInsider.com.