Scotiabank reported an 11.75 percent increase in their loan portfolio for the year to October as loans reached $11.8 billion. Most of the growth took place after April and helped to push up revenues and profit in the second half of the year.

Scotiabank reported an 11.75 percent increase in their loan portfolio for the year to October as loans reached $11.8 billion. Most of the growth took place after April and helped to push up revenues and profit in the second half of the year.

At mid-year to April loans, climbed from $10.575 billion at the end of October last year to $10.85 billion, growing by only 2.6 percent, well below the yearly growth to October. At the fiscal mid-point, profits were down in both the April quarter and the half-year, versus the prior year periods. Net income after tax for the July quarter, amounted to $140 million, an increase on the $134 million earned for the same period last year.

For the nine months to June, profits fell to $390 million from $404 million, but it represented an improvement over the decline in the six months results, with profits of $250 million versus $270 million in 2013. The second quarter results of $105 million compared with $128 million, in 2013, was one of the factors pulling down the results, as net revenues fell compared with the prior year.

With things starting to look up from the June quarter, the bank rolled out a respectable 11 percent increase in their October quarter profit after tax to hit $170 million versus $153 million in the same quarter in 2013 and a slight increase in the full year results which moved from $557 million to $560 million.

Loan loss provision rose from $4 million in 2013 to hit $28 million in 2014 and $9 million for the October 2014 quarter. Non-interest expenses were held tightly with virtually no increase in the October quarter with $173 million versus $172 million in 2013 and for the full year $639 million versus $612 million.

Banks make the bulk of their income from lending. If good loans are growing profits will usually grow if not, profits will tend to be much harder to grow. Loans grew 10 percent between July and October or 20 percent annualised but the growth in the October quarter was a more tepid 3 percent or at the rate of 12 percent per annum. This lower rate could well be a more sustainable level going forward, which will be enough to result in increasing profit at a reasonable pace.

Based on the last quarter results, investors should be looking at earnings per share climbing from $3.17 this year to be in the $4 region next year, as the bank overcomes the poor first half of the 2014 fiscal year.

The major concern, has to be the impact that the sharp fall in world oil prices will have on the Trinidad’s economy and the effect on the bank. That is something worth watching. Additionally, interest rates have been moved up, by the country’s Central Bank and could go higher, in the 2015. Rising interest rates can be negative for stocks.

Scotiabank T&T full profit recovery

Lower Q4 profit squeezes Scotia Group

Scotia Group Jamaica (Scotia Group) reported profit after tax of $10.1 billion for the year ended October, 2014, a decrease of $774 million or 7 percent compared with the net income of $10.9 billion in 2013.

The results for the fourth quarter of $2.5 billion represents an increase of $129 million or 5 percent over the same period last year, and a decrease of $188 million or 7 percent compared to the previous quarter ended July, 2014.

Earnings per share were $3.14 compared to $3.37 in 2013, and the Return on Average Equity was 13.41 percent, down from 15.67 percent last year. During the October quarter, income from foreign currency trading fell sharply from the July quarter, from $636 million to only $234 million and insurance revenues dropped from $661 million to $495 million, a fall of $166 million or 25 percent. While insurance income was higher than in the 2013 quarter at $476 million, the foreign exchange trading gains was still well below the $677 million generated in the 2013 quarter. Loan loss impairment fell to $227 million in the October 2014 quarter slightly higher than the $191 million in 2013 but much lower than the $497 million in the July 2014 quarter.

Jackie Sharp, President and CEO said, “Scotia Group experienced another year of solid performance across all business lines. We saw 9 percent growth year over year in our Commercial & SME portfolios; 6 percent growth in our retail loan portfolio; 12 percent growth in mortgages; and our Premium Money Market Fund which is offered by our subsidiary, Scotia Investments surpassed the $10 Billion mark. During the last half of the year, we have seen strong growth and we are poised for another successful year in 2015.”

Net interest income after impairment losses for the year was $22.9 billion, an increase of $57 million compared to 2013. Other revenue for this financial year amounted to $10.9 billion, a reduction of $465 million or 4 percent compared to 2013. Net fee and commission income remained stable year over year, despite the growth in loan and transaction volumes. Net gains on foreign currency activities decreased by $767 million, while net gains on financial assets increased by $520 million compared to the prior year.

Operating Expenses for the year amounted to $20.2 billion, an increase of $527 million or 2.7 percent compared 2013. The Group experienced an increase in the asset, premium and minimum business taxes of $861 million as a result of the increased rates implemented earlier in the year.

Operating Expenses for the year amounted to $20.2 billion, an increase of $527 million or 2.7 percent compared 2013. The Group experienced an increase in the asset, premium and minimum business taxes of $861 million as a result of the increased rates implemented earlier in the year.

Loans, after allowance for impairment losses amount to $145.7 billion as at the year-end is only up by just over $1 billion from the $144.6 billion at the end of the July quarter but increased 8 percent from $134.8 billion in October 2013.

Non-performing loans (NPLs) at October 31, 2014 totaled $4.9 billion, reflecting an increase of $411 million from prior year. Total NPLs now represent 3.32 percent of total gross loans compared to 3.29 percent last year and 3.31 percent as at July 31, 2014.Interest rates are falling on the deposit side that shows up in lower interest cost in the October quarter over that of the July quarter.

Looking ahead|Scotia should be able to manage the net interest income to their benefit going forward as Treasury bill rate continue to fall. The lower foreign exchange earnings in the last quarter is tied up in the revaluation of the Jamaican dollar during the quarter and should show improvement in the January 2015 quarter with some moderate slippage in the value of the Jamaican dollar. The slow growth in lending is likely to continue for a while longer and will act as a drag of accelerated income and profit growth. Investors should be looking for a gradual growth in profit rather than a big spurt, at any rate earnings should be climbing towards the $3.50 level in 2015.

The Board of Directors approved a final dividend of 40 cents per stock unit payable on January 13, 2015. The stock closed at $20, at the end of trading on the Jamaica Stock Exchange on Friday.

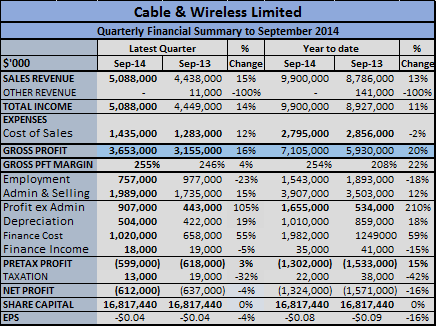

Interest cost jump burdens C&W

Cable & Wireless HQ Kingston

At the same time, profit before finance cost moved from a loss of $179 million in the six months to September, to a profit of $645 million. Higher finance cost, jumped from $730 million to $1.98 billion for the six months, from the year before, resulting in a similar loss as in 2103 of $600 million for the quarter and $250 million lower than in 2013 for the six months, to end at $1.32 billion.

Mobile subscribers grew by 125,000 during the April to September period and Mobile traffic increased by 34 percent and mobile service revenue is up 38 percent, the company reported.At the end of March Cable & Wireless stated that they had 705,000 mobile customers. The increase since March, puts active mobile customers at roughly 830,000, by the end of September. At the end of June this year, Mobile subscriber base increased by 37 percent with revenue increasing by 34 percent, broadband base increased by 12 percent with revenue up 39 percent. The continued strong growth in mobile customers is resulting in increased revenues for the local company, moving them closer to a break-even point.

The company cut employment cost sharply for both the quarter and six months but increased marketing spend to push various mobile and internet plans and boost the customer base, which should redound to benefit increased revenues, going forward.

The company cut employment cost sharply for both the quarter and six months but increased marketing spend to push various mobile and internet plans and boost the customer base, which should redound to benefit increased revenues, going forward.The second half of the year is more profitable for the company, with the revenue to be booked for the telephone directories and lower marketing cost in the final quarter of the year. Lower Treasury bill rates should see the interest rate that is used to book interest, being lowered by almost 25 percent compared with the first half of the year. IC Insider is projecting a profit in 2015/16 as revenues should continue the strong growth with the push to capture a larger portion of the cellular market and the double benefit of lower out payment cost per customer as the base grows and increase revenue from voice and data.

Small fall in profits at Blue Power.

Image courtesy of Graur Codrin/FreeDigitalPhotos.net

Lumber division revenue fell from $366.8 million in 2013 and that of the Soap Division grew from $154 million to hit, $360.8 million and $175.7 million respectively, resulting in total revenues falling 6 percent in the October quarter to $259 million and rising 3 percent for the six months to $536 million. Sales in the Lumber Depot division fell from $191 million last year, to $176 million this year, there were some one off sales, in 2013. Profit in the lumber division fell as well, from $29 million to $17 million for the half year. Notwithstanding, pressure on sales, margin improved during the year. The company held a tight lid on cost in the latest quarter, but administrative cost climbed 20 percent for the six months.

Earnings per share are still strong at 91 cents and should go on to approach the $2 level, by year-end. The stock last sold at $6.50, is undervalued and should enjoy some recovery in price. IC Insider is maintaining its BUY RATED status on the stock although a return to growth in profit s may have to await the 2016 fiscal year.

Earnings per share are still strong at 91 cents and should go on to approach the $2 level, by year-end. The stock last sold at $6.50, is undervalued and should enjoy some recovery in price. IC Insider is maintaining its BUY RATED status on the stock although a return to growth in profit s may have to await the 2016 fiscal year.The stock is listed on the junior market of the Jamaica Stock Exchange. The company primarily manufactures soaps and trade in Lumber.

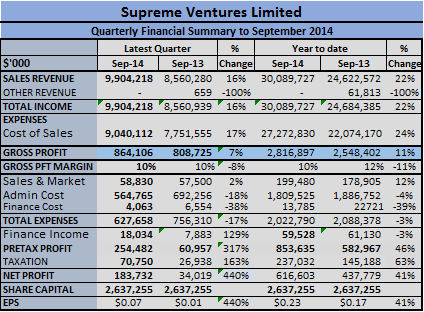

Profit jump 440% at Supreme Ventures

Profit for the September quarter, at Supreme Ventures jumped 440 percent over the 2013 results, hitting $184 million in the process and a sharp climb from the $34 million realized in the 2013 period.

Profit for the September quarter, at Supreme Ventures jumped 440 percent over the 2013 results, hitting $184 million in the process and a sharp climb from the $34 million realized in the 2013 period.

For the nine months ending September this year, profit after tax rose by a strong 41 percent, to $617 million, with earnings per share of 23 cents, putting the company on target to hit 30 cents per share for the full year to December. The gambling industry can have fettle results from time to time as has happened in the past at this company.

The strong improved profit results, flowed from a 16 percent sales rise in sales revenue in the quarter, to $9.9 billion and a stronger 22 percent for the nine months, to $30.1 billion. Gross profit grew at a slower pace of 7 percent for the three months and 11 percent for the nine months.

Segment results| Segment results show Supreme with challenges. While lottery earnings, climbed 35 percent for the year to date, to reach $1.22 billion and other areas grew from $102 million to $108 million, Sports betting losses are worsening even as revenues climbed from $177 million in 2013 to $418 million in 2014. The sharp growth in sports betting is attributable to betting on world cup football games. The segment lost $87 million in 2013 and $148 million in 2014 so far. Revenues fell for the Gaming and hospitality segment, from $394 million in 2013, to $314 million in 2014, but the losses were reduced from $440 million to $376 million. There are no noticeable improvements in the losses in the September quarter, for either loss making segments.

Administrative expenses dropped 18 percent, in the quarter due mainly to lower charges for professional fees, compared with the 2013, quarter and 4 percent for the nine months to September. While taxation increased, it was much slower than the growth in pretax profit. If the company could cut out the segment losses or sharply reduce them, earnings could jump as the losses amount to about 20 cents per share after tax.

Administrative expenses dropped 18 percent, in the quarter due mainly to lower charges for professional fees, compared with the 2013, quarter and 4 percent for the nine months to September. While taxation increased, it was much slower than the growth in pretax profit. If the company could cut out the segment losses or sharply reduce them, earnings could jump as the losses amount to about 20 cents per share after tax.

The financials remain strong with equity of close to $3.9 billion and cash and investments of $1.9 billion against current liabilities of $1.6 billion.

Lasco Manufacturing dominates juniors

Heating of raw material to make bottles for Lasco’s new drinks

At the close of the market, there were 1 stock with the bid higher than the last selling price and 5 stocks with offers that were lower. The junior market continues to exhibit weakness with 7 securities closing with no bids to buy. There were 5 securities that had no stocks being offered for sale.

Cargo Handlers concluded trading with 500 shares while gaining 90 cent $15, the high first reached in February this year. Lasco Distributors ended trading with 407,000 shares and increased of 10 cents to $1.50, Lasco Financial closed with 3,000 shares as the price climbed 1 cent to 94 cents. Lasco Manufacturing finished trading with 2,483,104 shares changing hands, to close 3 cents higher to $1.02, Paramount Trading saw trading in 15,255 shares as the price climbed 5 cents to $2.60, Caribbean Cream ended with 457,500 shares changing hands, to close at 71 cents and Access Financial ended with 100 shares changing hands to close at $10.01.

Blue Power released six months results to October showing profits of $52 million compared to $55 million in the same in 2013. For the three months profit declined to $22.8 million from $25.2 million as the lumber division contributed lower revenues than in 2013. Earnings per share are still strong at 91 cents and should go on to approach the $2 level by year end.

Mayberry profit up & down but buy

Brokerage house, Mayberry Investments has a long history of profit up one year and down the next, which provides alert investors with good buying opportunities.

Admittedly, this is not peculiar to Mayberry alone, but that is no solace to many of the investors who bought the stock years ago, when performance and the stock price were much better than now. A buying opportunity may now be presenting itself once more, as the stock is undervalued around the $1.50 level.

Admittedly, this is not peculiar to Mayberry alone, but that is no solace to many of the investors who bought the stock years ago, when performance and the stock price were much better than now. A buying opportunity may now be presenting itself once more, as the stock is undervalued around the $1.50 level.

While profit is up for the nine months to September this year, profit dropped 59 percent before tax, for the September quarter, compared to that of 2013, but improved sharply from a loss of $25 million for the nine months ending September last year, to a profit of $239 million this year. Last year, Mayberry suffered a loss of $338 million relating to the government of Jamaica debt exchange program. During the September quarter this year, the company enjoyed a tax credit of $14 million moving profit after tax to $54 million compared to $80 million in 2013. For the nine months, to September this year, profit after tax, amounted to $278 million versus $61 million last year.

Net interest income, declined for 2014, compared with both periods last year, but major improved trading and investment gains over the similar period last year and recovery of bad loans, helped to improve total net income. There was slower exchange rate trading gains, in the September quarter, but for the nine months, it was slightly lower than for 2013. Administrative expenses climbed 29 percent, in the quarter and 26 percent for the nine months, to September, slower than growth in income.

At the end of 2013, Mayberry had $3 billion invested in equity but for 2014 to date there is a decline in the value that negatively affected reserves, by approximately $260 million. Funds tied up in this area of investment, is one factor for the underperformance of the company, as the local stock market has not been performing well.  All of that could change going forward as the local economy continues to improve and interest rates fall, leading to increased profits for listed companies and more demand for stocks, thus pushing prices upwards. Mayberry remains a good way to profit from any upsurge that the Jamaican stock market will enjoy going forward, with the high level of stocks held plus increased brokerage fees from executing trades for investors. At $1.50 for the stock currently and likely earnings of around 30 cents for 2014, the stock present an opportunity for good return going forward.

All of that could change going forward as the local economy continues to improve and interest rates fall, leading to increased profits for listed companies and more demand for stocks, thus pushing prices upwards. Mayberry remains a good way to profit from any upsurge that the Jamaican stock market will enjoy going forward, with the high level of stocks held plus increased brokerage fees from executing trades for investors. At $1.50 for the stock currently and likely earnings of around 30 cents for 2014, the stock present an opportunity for good return going forward.

Stockholders’ equity stands at $3.6 billion, which translates to a book value of $3.04 per share with total assets of $23 billion up from $21.3 million at the end of September last year.

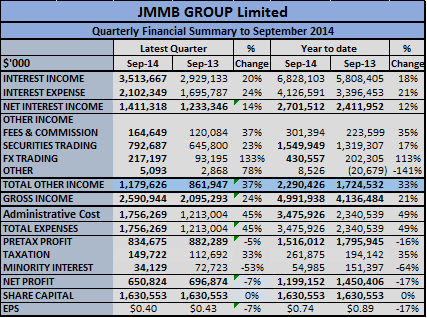

JMMB makes strong recovery in Q2

Profit for September quarter at Jamaica Money Market Brokers (JMMB) made a spirited recovery from the fall of 27 percent, in the June quarter to a more moderate 7 percent decline to reach $651 million from $697 million in September 2013. For the year to date, the decline is down to 17 percent to $1.2 billion.

Profit for September quarter at Jamaica Money Market Brokers (JMMB) made a spirited recovery from the fall of 27 percent, in the June quarter to a more moderate 7 percent decline to reach $651 million from $697 million in September 2013. For the year to date, the decline is down to 17 percent to $1.2 billion.

Two main issues led to this performance, the main income generator, Interest income grew 20 percent in the quarter and 18 percent year to date but net interest income grew much more slowly at 14 percent and 12 percent respectively. Other revenues rose 37 percent in the September quarter and 33 percent for the six months but expenses jumped 45 percent in the quarter and 49 percent for the six months ending September this year, to $3.5 million. JMMB made some progress in cutting cost in the quarter but much more will be needed in the months ahead if the pace of increased cost is to be kept in line with or below the growth rate of income. “Expenses associated with the expansion of the Group through the acquisition of IBL accounted for $715 million (63 percent) of this increase and the remaining $421 (37 percent) is explained by costs associated with integration, growth in subsidiaries in the regional markets, increase in asset tax and normal inflationary increases,” Management states.

The banking segment had improved the results from $125 million in 2013 to $269 million in 2014, partially due to the acquisition of the Intercommercial Bank in October 2013, while financial and related services moved from $1.69 billion down to $1.25 billion.

The banking segment had improved the results from $125 million in 2013 to $269 million in 2014, partially due to the acquisition of the Intercommercial Bank in October 2013, while financial and related services moved from $1.69 billion down to $1.25 billion.

Total assets grew from $172 billion in September last year to $224 billion in September, this year. The growth in asset is 10 percent or annualised at 20 percent since the fiscal year end in March. Equity stood at $20 billion at the end of September. The growth in assets is pretty strong and should result in strong increase in profits going forward.

JMMB stock last traded on the Jamaica Stock Exchange at $7 and on the Trinidad Stock Exchange at TT 45 cents.

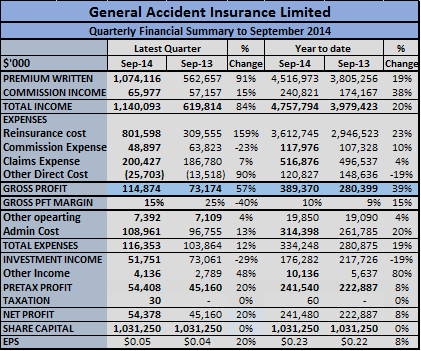

Profit up at General Accident but just

Profit for General Accident rose only 8 percent, for the nine months ending September this year, to $241 million or 23 cents per share.

Profit for General Accident rose only 8 percent, for the nine months ending September this year, to $241 million or 23 cents per share.

For the similar period last year, the company reported a net profit of $223 million, putting them on target to exceed 30 cents per share for the full year to December. Profit for the September quarter amounted to $54 million and is up 20 percent over the 2013 results. Premium income grew 91 percent in the quarter and 19 percent for the year to date period, but commission income was up 15 percent in the quarter, and 38 percent for the nine months to September. Underwriting profit climbed 57 percent in the quarter and 39 percent for the year to date. Investment income declined sharply due to slower exchange rate movement in 2014, versus 2013. Administrative expenses climbed 13 percent in the quarter and 20 percent for the nine months to September. The sharp increase in premium income in the September quarter should lead to higher income in the December quarter and raise earnings beyond the level enjoyed in the period to date.

“The company ended the quarter with a book value of $1.62 billion and generated a return on average equity for shareholders for the nine months period of 21 percent,” management stated in a release with the results. Equity at end of September last year was $1.35 billion.

“The company ended the quarter with a book value of $1.62 billion and generated a return on average equity for shareholders for the nine months period of 21 percent,” management stated in a release with the results. Equity at end of September last year was $1.35 billion.

Insurance reserves at the end of the period, stood at $2.1 billion, and is covered by cash and investments, of just over $2 billion.

With the stock trading at $1.53, on the junior market of the Jamaica Stock Exchange it is severely undervalued and has lots room to run accordingly, remains IC Insider BUY RATED.

Sagicor Group bounced head in Q3

Banking profit fell to a loss of $16 million this year so far, from a profit of $271.8 million for the nine-month period to September last year, helping to pressure Sagicor Group’s profit for the third quarter and year to date.

Banking profit fell to a loss of $16 million this year so far, from a profit of $271.8 million for the nine-month period to September last year, helping to pressure Sagicor Group’s profit for the third quarter and year to date.

The financial group saw a sharp fall in profit in the quarter, from $1.56 billion to $1.1 billion. “Post-acquisition losses relating to the RBC Jamaica acquisition that was completed effective June 2014 amounted to $231 million, including rebranding and restructuring costs” the Sagicor management said in a release with the result.

The Group produced net profits of $3.84 billion, with $3.79 billion available to stockholders, for the nine months to September. This outcome was better than last year by a mere 2.5 percent. Earnings per stock unit came out at $0.99. Profit for third quarter amounted to $1.08 billion compared with $1.52 billion for 2013 after minority interest. The current period results and the nine months profits were impacted by costs for rebranding and rationalizing operations, following the RBC Jamaica acquisition, higher taxes and lower unrealised FX gains in 2014 compared to 2013. The 2013 results included the negative impact of the Government of Jamaica NDX debt swap.

Segments| The group’s performance for the nine months disguises what has taken place in the segments. Individual insurance generated 20.5 percent more profit than it did in 2013, to reach $1.3 billion, employees’ benefit jumped 26.3 percent to $2.3 billion and investment banking climbed 83 percent to $569 million, this segment would have had the negative impact of the NDX in 2013. The category, All Other fell sharply, from $272 million to $79 million.

Revenues and Expenses| Revenue grew 9.6 percent above prior year, to hit $34.2 billion. The 2013 revenue included the realised capital losses as a result of the debt exchange. “2014 Net Premium Income, in aggregate, was slightly below that for 2013. Net Investment income was higher than in the prior year, reflecting business growth and units’ appreciation in the Segregated Funds. The 2013 Net investment Income number also includes capital losses from the NDX and PDX,” the manager’s statement said.

“Group administration expenses of $7.52 billion were 35 percent more than in 2013. The significant increase includes post acquisition expenses for the RBC portfolio and one-time costs for re-branding the RBC portfolio and rationalization of operations. The Banking Group also had operating costs associated with the new flagship Hope Road branch which was opened in December 2013,” management explained in their report to shareholders.

The increased administration cost which was $3.4 billion in the third quarter was $1.6 billion more than the amount incurred in 2013 due to the added ongoing cost associated with running the RBC banking operation. The results for the December quarter should see a sharp reduction in this category of expense and therefore help improve the profit to what would normally be expected.

Assets| With the acquisition of RBC Jamaica operations the total group assets now sits at $262 billion up from $189 billion at September 2013 and equity stands at $42 billion.