Revenues rose a strong 36.56 percent for the year to August 2014 for junior market listed, AMG Packaging, hitting $607 million but it increased by a much slower pace of 28 percent in the final quarter of the financial year, to $165 million.

Revenues rose a strong 36.56 percent for the year to August 2014 for junior market listed, AMG Packaging, hitting $607 million but it increased by a much slower pace of 28 percent in the final quarter of the financial year, to $165 million.

Those strong gains may have cannibalized sales in the November quarter with flat sales compared with 2013 quarter, with revenues of $151 million. But the performance comes against the back ground of volumes sold, climbing a very strong 19 percent for the year. The fall in volume started from the August quarter as units sold increased by 23.4 percent, management stated in a release accompanying the May results.

While sales increased impressively in 2014 fiscal year margins came under pressure with only 23.7 percent for the year to August down from 33 percent in 2013. For the latest quarter gross profit margin comes out at 25.9 percent but could end up at 31.5 percent for the current year if sales volumes increase by 10 percent for the rest of the fiscal year. Gross profit for the quarter amounted to $34.4 million up from $33.3 million in 2013 but increase mainly administrative cost that rose 28.4 percent eroded profit slightly by 15 percent to $15.4 million from $18 million in 2013. The company got a double whammy, with the Jamaican dollar losing value, resulting in a 28 percent more Jamaican dollars having to be found to purchase a US dollar since September 2012, and the price of paper on the world market moving 22 percent from US$720 per tonnes at September 2012 to US$830 in August 2013 and now US$875, which it has been since June last year.

Receivables are down by $12.7 million from the amount at the end of August last year and so too is amounts in payables by $26 million. Cash funds grew to $33 million from $22 million while inventories is down from to $118 million at August to $113 million, which is nearly 4 months supplies based on sales in the quarter and is up from just two and a half months back in 2013 and seems to be a hedge against devaluation of the Jamaican dollar. But that is only a part of the story. A check on world prices for pulp shows a pretty sharp increase since 2012.

AMG has to continue to grow its business by continued strong volume growth to become a more cost competitive producer with lower unit cost. The company needs to put strategies in place to return volume sales to growth and needs to continue cost containment measures to ensure profit improvement going forward. With increase through put, unit cost of production will fall allowing more growth in gross to flow into overall profits. A bright spot for the company is the fall in the cost of fuel and electricity will help in keeping cost down for the rest of the fiscal year.

IC Insider’s forecast for 2015 is 90 cents per share and $1.50 for 2016 on the assumption that volume sales return reasonable growth.

AMG flat sales push profit down 15%

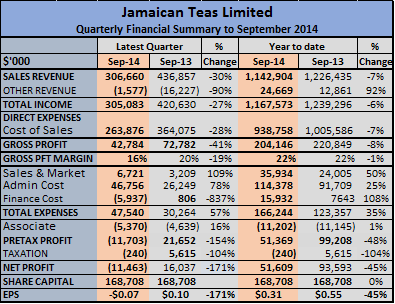

Jamaican Teas 2014 profit drops

Jamaican Teas reported sharply lower profit, last year to September, of $52.7 million versus $93 million in 2013, with earnings per share of 31 cents. The figures were reported in the group’s audited financial statements release last week.

Jamaican Teas reported sharply lower profit, last year to September, of $52.7 million versus $93 million in 2013, with earnings per share of 31 cents. The figures were reported in the group’s audited financial statements release last week.

The results emanated from sale revenues of $1.14 billion down from $1.23 billion in 2013. There was approximately $50 million coffee sales included in the 2013 results with none in 2014. In 2013 the real estate segment contributed $185 million in revenues compared to only $26 million in 2014 with most coming in the September 2013 quarter.

Gross profit margin shrank slightly from 21.89 percent to 21 percent for the year, helping to cut gross profit by $17 million. Other operating income climbed to $24.7 million from $12.9 million in 2013, partially due to losses on sale of, and impairment of investments incurred in 2013, amounting to $13.5 million, but did not occur in 2014.

The Orchid property being developed that should add to Jamaican Teas’ profits in 2015 & 2016.

Changes in our distributorship in the Florida at the start of the fiscal year resulted in some short-term fall out in sales and increased marketing cost. A new distributor was appointed in the US market that will provide wider distribution in some key cities within that country. Revenues are expected to benefit from this development starting with the December quarter. The 2015 revenues, should also benefit from the completion of sales of 16 units in the first phase of the real estate development in St Thomas. The supermarket in Savanna-la-Mar was close to a break even by year-end and while the one in Kingston remained profitable. The Montego Bay supermarket reported losses in line with what was incurred in the prior year.

There was approximately $50 million increased borrowed funds at the end of the year, putting borrowings at $304 million. The profile of the debt changed markedly, with long-term loans accounting for two thirds of the debt at the end of the fiscal year compared with just 2 percent in 2013. The portfolio of investments including equities, stood at $123 million at the year-end and shareholders’ equity of $635 million.

There was approximately $50 million increased borrowed funds at the end of the year, putting borrowings at $304 million. The profile of the debt changed markedly, with long-term loans accounting for two thirds of the debt at the end of the fiscal year compared with just 2 percent in 2013. The portfolio of investments including equities, stood at $123 million at the year-end and shareholders’ equity of $635 million.The company imports of black and green tea in bulk for packaging and the distribution local and overseas. it also packages and distributes herbal teas and distributes other bottled water, coconut milk and other pre-packaged food items. the group operates supermarkets and is involved in the rental of residential properties and the development of real estate for resale.The stock is listed on the Jamaica Stock Exchange and last traded at $2.50.

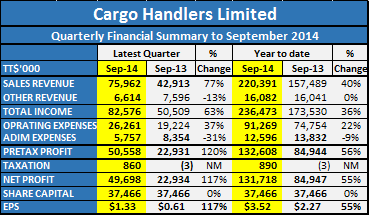

Cargo Handlers’ Q4 profit doubles

Profit for the September quarter at Cargo Handlers is up 117 percent over the 2013 results to $49.7 million from revenues that climbed a very strong 77 percent. Profit rose by a smaller 55 percent, for the nine months ending September this year, to $131.7 million or $3.52 per share from revenues for the nine months of $220 million.

Profit for the September quarter at Cargo Handlers is up 117 percent over the 2013 results to $49.7 million from revenues that climbed a very strong 77 percent. Profit rose by a smaller 55 percent, for the nine months ending September this year, to $131.7 million or $3.52 per share from revenues for the nine months of $220 million.

Other income, mainly foreign exchange gains, fell 13 percent in the quarter and was flat for the year, at $16 million. During the year the company earned $13.6 million from leasing and $8.9 million from management fees charged to a related party – Bulk Liquid Carrier and Petroleum Transport Ltd.

Administrative expenses dropped 31 percent in the quarter and 9 percent for the year but operat9ing expenses climbed 37 percent for the quarter and 22 percent for the year well below the increase in revenues. The company paid a dividend of $1.80 per share during the year for a yield in excess of 13 percent based on the stock price of $13.50 at the start of 2014.

Looking forward the foreign exchange gains earned in the last two years is unlikely to repeat in 2015 as the Jamaican dollar is unlikely to slip to the same degree it did in the recent past, so earnings will need to exclude most of these gains which amounts to just over 40 cents per share. Investors could be looking at earnings per share around $4.80 in 2015. At a price of $16 the stock is undervalued but they are difficult to come by.

Looking forward the foreign exchange gains earned in the last two years is unlikely to repeat in 2015 as the Jamaican dollar is unlikely to slip to the same degree it did in the recent past, so earnings will need to exclude most of these gains which amounts to just over 40 cents per share. Investors could be looking at earnings per share around $4.80 in 2015. At a price of $16 the stock is undervalued but they are difficult to come by.

Equity capital stood at $200 million and net book value at $5.33 per share. There is virtually no borrowings and cash of $93 million.

The company is involved in primarily in stevedoring services and is in the process of acquiring a petroleum haulage company which it now manages pending completion of the sale. The stock is listed on the Jamaican Stock Exchange.

Scotia Investments in transition

Scotia Investments (SIJL) reported net income of $1.79 billion results for the year ended October 2014, down $205 million from the last year. Net income for the quarter was $450 million, down $54 million from the previous quarter, and $123 million from the corresponding quarter last year.

Scotia Investments (SIJL) reported net income of $1.79 billion results for the year ended October 2014, down $205 million from the last year. Net income for the quarter was $450 million, down $54 million from the previous quarter, and $123 million from the corresponding quarter last year.

Earnings per share for the year ended at $4.23 compared to $4.71 in 2013. The Return on Average Equity fell was from 16.55 percent in 20123 to 13.6 percent.

Net interest income for the year was $2.3 billion, down $519 million or 18 percent below last year and for the quarter, $499 million, down $81 million or 14 percent below the July quarter.

Non-interest income, which includes fee income, securities trading gains and net foreign exchange trading income, was $1.89 billion for the year, is up $237 million or 14 percent; and $487 million for the quarter, down $61 million compared with the July last quarter.

Total Operating Income, comprising net interest revenue and other income was $4.17 billion, a reduction of $281 million relative to prior year. Total Operating Income for the quarter of $986 million was down $233 million over the corresponding quarter last year.

Total operating expenses for the year was $1.62 billion, up $33 million or 2 percent compared to 2013. Expenses amount to $364 million for the October quarter, down $32 million or 8 percent against the July 2014 quarter, and it is also down 19 percent, against the 2013, October quarter.

Total on balance sheet assets amount to $72 billion and show a reduction of $1.4 billion compared to last year. At the end of October 2014, total funds under management stood at $151 billion, $96 billion or 64 percent represents off-balance portfolio, compared to 60 percent last year. The Scotia Premium Money Market Fund grew to $10 billion by the end of the year. For 2014, funds managed through the unit trusts and mutual funds increased by 17 percent year over year, due to both growth in volume and appreciation in value of the funds. Management states that “the change is consistent with our strategic initiative to focus on the growth of our unit trusts and mutual fund portfolios.”

Total on balance sheet assets amount to $72 billion and show a reduction of $1.4 billion compared to last year. At the end of October 2014, total funds under management stood at $151 billion, $96 billion or 64 percent represents off-balance portfolio, compared to 60 percent last year. The Scotia Premium Money Market Fund grew to $10 billion by the end of the year. For 2014, funds managed through the unit trusts and mutual funds increased by 17 percent year over year, due to both growth in volume and appreciation in value of the funds. Management states that “the change is consistent with our strategic initiative to focus on the growth of our unit trusts and mutual fund portfolios.”

Shareholders’ equity stood at $13.6 billion as at October 31, 2014, an increase of $1.15 billion or 9 percent compared to last year. Net asset value per share is $32.14 and the stock price $23.40 with the PE ratio just above 5 times 2014 earnings. With interest rates falling and the funds under management rising SIJL should put into a better performance in 2015.

Barita’s ugly Q4 results

Barita Investments had a decent nine months’ performance to June this year, with profit of $156 million versus $77 million in 2013. Profit had dipped for the June quarter from that of 2013 by just under 50 percent. The net result was earnings per share of 35 cents.

Barita Investments had a decent nine months’ performance to June this year, with profit of $156 million versus $77 million in 2013. Profit had dipped for the June quarter from that of 2013 by just under 50 percent. The net result was earnings per share of 35 cents.

With those results investors would be forgiven if they felt that full year’s earnings would be closer to 50 cents per share than the 16 cents they reported. That company reported a loss in the September quarter of $66 million down from a profit of $24 million in 2013, pulling full year results to $71 million compared to $63 million in 2013.

Major contributors to the final quarter’s loss, are increased taxation of $26 million, with a loss before tax of $40 million. Investment impairment resulted in $42 million hit against profit while securities and foreign exchange trading ended up in losses and dividend income fell by $19 million. Net interest income dropped sharply as well, by 60 percent to $45 million while administrative cost was up 17 percent. Barita also picked up a loss of $10 million from an investment in an animated development company GSW Animated Ltd. Barita’s investment in the company is $28 million, for 11.84 percent interest.

For the full year interest expense rose 21 percent but income fell marginally, while income from fees, commission and securities trading were the only areas to show growth. Cost was kept pretty tight with only a 4 percent rise.

In 2013 Barita took a big hit on its investment portfolio when it swapped Government bonds for lower yielding ones, resulting in a write off of capital gains on their holdings. Interest rates rose between 2013 and mid 2014 resulting in a squeeze on interest margins. Some of the reduction on the interest income side was made for by a switch to foreign exchange holdings to benefit from the devaluation of the local dollar. Revaluation of the Jamaican dollar in the September quarter would have negatively affected return in this area. The local dollar slipped in the December quarter which should benefit them. Economic measures being pursued by the Jamaican government along with the sharp drop in oil prices will lead to greater stability or possible some revaluation of the local dollar in the months ahead. This will likely result in a portfolio shift that will improve net interest income. The local stock market is showing signs of improved interest and if this continues, trading income will improve for 2015 and the large investment impairment hit should not occur. The end result is that the company should enjoy better results in 2015.

Of import is the higher level of profitability, shown in comprehensive income statement, with gains of $242 million excluding revaluation gains on property. The increased comprehensive income resulted in the capital base of the company rising to $1.67 billion from $1.4 billion at the end of the 2013 fiscal year. Total assets being managed is $13.6 billion.

Of import is the higher level of profitability, shown in comprehensive income statement, with gains of $242 million excluding revaluation gains on property. The increased comprehensive income resulted in the capital base of the company rising to $1.67 billion from $1.4 billion at the end of the 2013 fiscal year. Total assets being managed is $13.6 billion.

Barita should be seen a good play on the revival of the local stock market which is going to happen at some time in the near future, exactly when is unsure at this time, based on valuation and performance of companies it may not be far off.

The company’s stock is listed on the Jamaica Stock Exchange and last traded at $2.18 with net assets of $3.75 per share. Profit may have slipped in 2014 but that is not an indication of a permanent slippage as such the stock remains BUY RATED based on it low price and the potential for higher earnings ahead.

Massy Holdings profit jumps 23% in Q4

![]() For the year to September, profit for Massy Holdings rose only 2 percent, to $555 million or $5.68 cents per share.

For the year to September, profit for Massy Holdings rose only 2 percent, to $555 million or $5.68 cents per share.

Profit for the September quarter amounted to $190 million and is up a strong 23 percent over the 2013 results. The yearly profit is negatively affected by a $58 million cost incurred in relating to the company changing its name and form Neal and Massy to Massy Holdings along with other rebranding expenses. Earnings per share for 2015 should end up around the $6 levels, on the assumption that measures needed in the Trinidad economy to deal with the fall in oil price will not have any serious negative effect on the Group’s operations in that country. The PE for the stock will be around 11 times 2015 earnings and should provide a basis for the price to increase during next year as the target should be around 15.

Total revenues for the year is up 14 percent to $10.7 billion, and up 18 percent in the September quarter to $2.77 billion, the latter benefitted from the acquisitions in Columbia that contributed $123 million in revenues and $2.5 million in segment profit. Additionally, the group acquired majority interest in a supermarket business in St Lucia in late December last year. The income form that operation is included in the October quarter but would not be there in 2013.

Segment profit before rebranding cost saw growth in Automotive and Industrial Equipment increasing by 5 percent, Integrated Retail gaining a mere 2.5 percent, Insurance up by 17.6 percent, Energy and Industrial Gases 52.4 percent, Information Technology Communications 10.3 percent and Other Investments down 21.5 percent. Jamaica contributed 37 percent more in profits to the group in 2014 than in 2013, Trinidad from which the bulk of profit comes saw a 6.7 percent increase and Guyana 4.7 percent.

Massy Holdings is listed on the Trinidad & Tobago Stock Exchange and is involved in a wide range of products and services.

Ethanol losses & loan cost hit JBG profit

Profit fell 30 percent, for the six months ending October this year and a whopping 43 percent for the October quarter at Jamaica Broilers (JBG). With chicken processing being their main product line, the company reported profit of $210 million in the six months to October, down from $301 million for the similar period last year.

Profit fell 30 percent, for the six months ending October this year and a whopping 43 percent for the October quarter at Jamaica Broilers (JBG). With chicken processing being their main product line, the company reported profit of $210 million in the six months to October, down from $301 million for the similar period last year.

JBG reported a net profit of $99 million for the October quarter down from $173 million in 2013. The fall in profit is due to three main factors. Interest cost climbed 106 percent in the latest quarter and 68 percent in the six months period and corporation tax jumped 180 percent in the quarter and 58 percent for the six months against revenue growth of 15 percent in the quarter and 14 percent year to date. The ethanol operations contributed considerably to the lower profit with a loss of $144 million versus $27 million profit in 2013, the loss made in the October quarter was $55 million. Rising profit in the US segment accounted for the bulk of the tax increase.

On a positive note management indicates that “new business in the Ethanol division looks promising with income already received in October and November.”

Administrative expenses climbed 11 percent in the quarter and 21 percent for the nine months to October, with the latter growing faster than revenue increase.

Administrative expenses climbed 11 percent in the quarter and 21 percent for the nine months to October, with the latter growing faster than revenue increase.

The United States segment has done exceedingly well, with segment profit moving from $202 million in 2013 to $572 million this year. Ethanol is a concern especially with world oil prices having fallen sharply this year. Other areas have just kept pace with the prior period, the increased debt cost is weighting down on profit and needs to be put on firmer and more cost effective footing. The company makes the bulk of it profit in the second half of the year and with ethanol seems to be generating added revenues things could be looking up in the second half.

Jamaica Broilers borrowed $800 million more since the year-end at the end of April pushing borrowed funds to $7 billion this was used to fund increased inventories that rose by $800 million over the same period.

First Caribbean 2014 profit disappears

First Caribbean International Bank reported a big loss of US$151 million, a huge increase from a loss of just US$22 million in 2013. The news may appear gloomy but there is more to that than meets the eye. The news may well be a strong signal that its time to buy shares of this bank that sprawls over the wider Caribbean region.

First Caribbean International Bank reported a big loss of US$151 million, a huge increase from a loss of just US$22 million in 2013. The news may appear gloomy but there is more to that than meets the eye. The news may well be a strong signal that its time to buy shares of this bank that sprawls over the wider Caribbean region.

Management cleaned shop, resulting in loans loss provision climbing 36 percent to US$206 million in 2014 and impairment cost relating to intangible assets of US$115 million. The latter should not repeat in the near term and loan loses may remain subdued with the heavy write off in 2014.

The October 2014 quarter enjoyed a major turn-around in fortunes as after-tax profit rose to US$24.6 million from a loss of US$66 million in 2013. The quarterly result was helped by a sharp drop in loan loss provision, falling from US$76 million in 2013 to US$13 million and operating expenses declining from US$130 million to $88 million. The July quarter also showed positive results, amounting to US$23 million after tax, suggesting that profit could be back on track.

Net interest revenues were down 1 percent for the year, but fell 7 percent in the October quarter, from the similar quarter, in 2013 as revenues fell 6 percent and interest cost was down by 5 percent. Other income fell in the quarter moderately, but was up for the year, by 2 percent. How will the bank grow its income, is the challenge going forward in the medium term, in a region that is suffering from economic stagnation and beset by high levels of national debt?

Customer deposits ended at US$9.2 billion from $9.8 billion at the end of the 2013 fiscal year while loans fell to US$6.14 billion from US$6.33 billion in 2013 and as high as US$6.83 billion at the end of the 2012 fiscal year. The bank’s balance sheet contracted during the year to $10.78 billion from $11.4 billion in 2013 due mainly to contraction in cash balances and loans but investment securities rose from $2.2 billion to $2.3 billion.

Customer deposits ended at US$9.2 billion from $9.8 billion at the end of the 2013 fiscal year while loans fell to US$6.14 billion from US$6.33 billion in 2013 and as high as US$6.83 billion at the end of the 2012 fiscal year. The bank’s balance sheet contracted during the year to $10.78 billion from $11.4 billion in 2013 due mainly to contraction in cash balances and loans but investment securities rose from $2.2 billion to $2.3 billion.

A final dividend of 1.5 US cents per share payable in January, was declared, it brings the total for the year to 3 US cents. The stock is listed on the Barbados and Trinidad and Tobago stock exchanges.

First Citizens 2014 profit up slightly

Trinidad’sFirst Citizens Bank reported profit of $773 million before taxation for the year to September compared to $745 million in 2013. Profit after tax, amounted to $627 million in 2014, up 2.9 percent over the profit of $609 million of 2013.

Trinidad’sFirst Citizens Bank reported profit of $773 million before taxation for the year to September compared to $745 million in 2013. Profit after tax, amounted to $627 million in 2014, up 2.9 percent over the profit of $609 million of 2013.

For the October 2014 quarter pre-tax profit rose 9 percent over 2013 to reach $180 million from $165 million but profit after tax for the quarter was virtually flat at $149 million versus $145 million in 2013. The information was included in an abridged version of the bank’s results for 2014.

Citizens had assets of $34.9 billion at the end of September marginally down from the $35 million at the end of June. Since June customer deposits fell from $26.5 billion to $25.7 billion. The bank did not report details on loans at September. At the end of June this year, there was no growth in this asset which stood at $13.75 billion, slightly down on the amount at September 2013 and is hardly likely to have changed much since with flat assets.

Earnings per share amounted to $2.50 for 2014. The stock remains on the Buy Rated list with earnings per share of $2.75 projected for 2015 and a target price in the around $45.

A final dividend of 61 cents per share payable in December was declared, and it brings the total for the year to $1.18, up from $1.09 per share paid as the final dividend for the 2013, the amount was paid in January 2014.

The dividend policy of the Citizens is to distribute to its ordinary shareholders funds surplus to the operating capital and strategic requirements of the Group, as determined by the Directors, with an annual target dividend pay-out percentage range of 45 to 55 percent of net profit after-tax.

The company was listed on the Trinidad and Tobago Stock Exchange in September 2013, after a successful public share issue.

NCB 2014 profit trumps 2013 by a KM

National Commercial Bank net profit for 2014 hit $11.6 billion, a big jump from the NDX affected $8.58 billion in 2013. Earnings per share for the year ended at $4.73 just below IC Insider forecast of $4.80.

National Commercial Bank net profit for 2014 hit $11.6 billion, a big jump from the NDX affected $8.58 billion in 2013. Earnings per share for the year ended at $4.73 just below IC Insider forecast of $4.80.

The 2013 profit was negatively affected by a huge $1.5 billion charge, from losses picked up when they exchanged high yielding government bonds for lower yielding ones and $680 million written off relating to the attempt to list on the New York Stock Exchange. The group is reporting net profit of $2.87 billion, for the September quarter compared to $1.8 billion in 2013, the latter was affected by a number of one off charges.

The 2013 full year was also negatively impacted by a $281 million hit from receivership expenses, an increase over the amount spent in 2012 of $172 million and a healthy rise in Technical, consultancy and professional fees of $1.09 billion compared with $846 million in 2012.

This year results benefited from a few one off items as well. Gain on acquisition of subsidiary contributed $301 million and gain on sales of shares in Kingston Wharves added $349 million but this is in lieu booking their share of profits for the quarter had they not sold. The group suffered a loss of $200 million on securities impairment and critically, although loan loss provision is up $200 million, the large increase in the final quarter is $700 million more than at the same time in 2013. For the full year, loan losses amount to $2.2 billion versus $2.1 billion for the previous year.

Salaries allowances and benefits cost was down in the quarter to $2.6 billion from $2.9 in the similar quarter, and for the year to $11.5 billion versus $11.2 billion in 2013. Other operating cost was up to $10.4 billion for the full year, from $9.4 billion in 2013 and for the quarter $3.1 billion from $2.8 billion.

Growth| For 2014, loans grew pretty strongly by 12 percent, moving from $143.6 billion to $157 billion and customer deposits of $202 billion, increased by $23.8 billion, or 13 percent, resulting in net interest income being steady, in the September quarter, for both years, as well as in the June quarter at roughly $6 billion each. Net interest income was up $1 billion for the year over 2013 to reach $24.66 billion from $23.56 billion. Fees and commission income moved up to $10.6 billion net, compared to $9.7 billion in 2013. Premium income grew to $7 billion from $5 billion in 2013. Gains on sale of debt securities and foreign exchange trading gains jumped to $2.6 billion versus $1 billion in 2013.

Segment| Segment results were mixed with strong increases in some, while other areas fell below the 2013 performance. Retail & SME, reported improved profits for 2014 of $1.56 billion versus $793 million in 2013. Payment Services climbed down from $2.1 billion to $1.57 billion in 2014, Corporate Banking ended 2014 with $500 million versus $850 million previously, Treasury & Correspondent Banking jumped from $1.87 billion in 2013 to $3.7 billion in the latest year. Wealth, Asset Management and Investment Banking moved down from $3.88 billion to $3.6 billion, Life Insurance and Pension Fund Management climbed from $2.17 billion to $2.9 billion and General Insurance income of $557 million in 2013 jumped to $1.28 billion.

NCB hiked their final dividend for the year to 96 cents per shares. IC Insider’s forecast for the 2015 earnings is $5.75 per share and with the current price at just over $18 per share the stock is severely undervalued with significant upside potential.