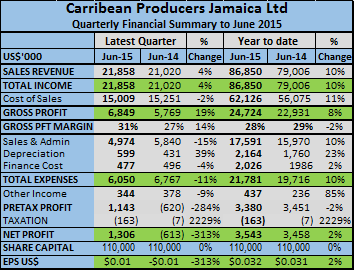

Caribbean Producers reported profit of US$3.54 million or 32 US cents per share for the year to June 2015, versus $3.46 million or 31 cents in 2014, according to the company’s audited financial statements. Sales brought in $86.85 million during the year compared with $79 million in 2014, a gain of 10 percent and for the quarter sales were up just 4 percent over 2014 to $21.86 million from $21 million in 2014 while profit came in at $1.3 million compared with a loss of $613,000 in 2014.

Caribbean Producers reported profit of US$3.54 million or 32 US cents per share for the year to June 2015, versus $3.46 million or 31 cents in 2014, according to the company’s audited financial statements. Sales brought in $86.85 million during the year compared with $79 million in 2014, a gain of 10 percent and for the quarter sales were up just 4 percent over 2014 to $21.86 million from $21 million in 2014 while profit came in at $1.3 million compared with a loss of $613,000 in 2014.

Profit for the latest quarter is 23 percent higher than the $922,000 earned in the March quarter, a period that is usually the highest earner. Earnings per share ended at 32 cents for the year or close to J$3.75.

Gross profit margin jumped in the June quarter to 31 percent and well over the 27 percent enjoyed in the 2014 quarter and higher than the 28 percent for the full year. Gross profit climbed as well by 19 percent to $6.8 million for the quarter much faster than the growth in revenues and was up by 8 percent for the year a bit less than revenue growth. Selling and administrative expenses fell in the quarter, by 15 percent but was up 10 percent for the year.

Profits seem to be moving in the right direction with cost falling in some areas and profit margin improving. At the current price of J$2.50 the stock is undervalued as it should be moving into the J$3 region with these results. The group has been seeing improvement in the St Lucian operations and that could be improved upon in 2016 fiscal year.  Caribbean Producers made a profit of $447,000 in the September 2013 quarter but made on $2,500 profit in 2014, the results for this year’s September quarter should be better as 2014 had certain cost associated with new products and the holding of prices for certain items sold to the hotel sector during that period.

Caribbean Producers made a profit of $447,000 in the September 2013 quarter but made on $2,500 profit in 2014, the results for this year’s September quarter should be better as 2014 had certain cost associated with new products and the holding of prices for certain items sold to the hotel sector during that period.

The bother continues to be the heavy debt, at $24.76 million which is down from $25.2 million in 2014, while equity is up to $19 million from $16 million in 2014 thus improving the debt to equity ratio quite a bit. The probability exists that there should be an improvement in 2016 as well, as profit continue to perform, thus building up equity.

IC Insider is restoring it BUY RATED stamp on this one.

Caribbean Producers BUY RATED again

FCIB from consolidation to expansion

Years of adjustment, heavy loan loss provisioning, contraction and now consolidation at FirstCaribbean International Bank have started to bear fruit and is now leading to expansion. The bank that sprawls over the Caribbean has suffered with the declines in economic activities within the region that saw it writing off large amounts of loans that went bad.

The struggles to overcome the drag that the economic pressures placed on the bank that is a subsidiary of the Canadian Imperial Bank of Commerce has been tough and can be seen in in the performance of loans and assets. At April 2009, loans which stood at US$6.9 billion and assets of $10.6 billion, slipped to just $6 billion and $10.9 billion, respectively by July this year.

The struggles to overcome the drag that the economic pressures placed on the bank that is a subsidiary of the Canadian Imperial Bank of Commerce has been tough and can be seen in in the performance of loans and assets. At April 2009, loans which stood at US$6.9 billion and assets of $10.6 billion, slipped to just $6 billion and $10.9 billion, respectively by July this year.

“We have just recently announced that the Rendezvous Branch in Barbados will be converted into a sales centre catering to Platinum Banking, Business Banking, Corporate and International Banking customers. We have opened new branches across the region, most notably the Santa Cruz mini-branch in Jamaica. Another branch at Fairview in the Montego Bay area is under construction. Additionally, we recently opened a Representative Office in Aruba and have plans to open a full service branch in 2016, as part of our expansion plan for the Dutch Caribbean,” Rik Parkhill, Chief Executive Officer of the bank stated in a report to shareholders.

The Bank enjoyed improving net profit of US$34 million in the third quarter, up $11 million or 49 percent over the prior year’s third quarter profit of $22.9 million. For the nine months, net profit attributable to shareholders was $85 million. In 2014 the bank reported a loss of $173 million after taking a one off hit of $116 million for Impairment of intangible assets.

Total revenue during the third quarter and the nine month period declined moderately compared to 2014 primarily due to lower interest earnings from loans and securities.

Operating expenses over the nine month period were down by $3 million and for the quarter $1 million compared with the same periods last year. Loan loss impairment expense was of $7 million in the third quarter and $35 for the year to date, were sharply down, on the $23 million and $193 million for the nine months in 2014 respectively. Results have been converted to US$ at an exchange rate of US$1 to BDS$2.

“ Some countries continue to experience low credit demand, additionally interest margins on loans and securities yields were lower. While productive loans balances are down 1 percent over the prior year, an improved performance over the second quarter of 2015 was recorded with 1 percent or $80.6 million in loan growth as a larger proportion of the sales pipeline was converted into productive loans during the latter half of this quarter. Additionally, non-productive loan balances were down 18 percent to $651 million compared with the same period last year as efforts continue to further strengthen the quality of our loan portfolio,” the bank reported.

The turnaround why commendable, the bank needs to find means of growing its loan portfolio and a reasonable pace again in order to generate attractive profits increases going forward for the stock to be an attractive buy.

FirstCaribbean is listed on the Barbados and Trinidad and Tobago stock exchanges and were last traded at TT$5 and Bds $1.89.

Blue Power disappoints again

For the six consecutive quarters, soap manufacturer, Blue Power, disappoints investors, with a fall in profit compared to the prior year’s results. For the three months to July this year, the company reported profit before tax of $21 million compared to $29 million in the same period last year, a fall of 28 percent.

For the six consecutive quarters, soap manufacturer, Blue Power, disappoints investors, with a fall in profit compared to the prior year’s results. For the three months to July this year, the company reported profit before tax of $21 million compared to $29 million in the same period last year, a fall of 28 percent.

Revenues for the period ended at $306 million that are up 8 percent from the $282 million for the same period last year and a big recovery from $260 million experienced during the poor April quarter.

The five-year tax-free concession the company enjoyed for listing on the junior market ended in April, resulting in an estimated tax liability of $2.19 million which reduces net profits to $18.60. The profit performance helped to generate gross cash flow from operations of $24 million versus $28 million in 2014.

While sales grew, gross profit fell and gross profit margin declined with the former falling to $64 million from $66 million and administrative and other expenses rose 14 percent to $46 million.

The contribution of Lumber Depot division to the before tax was $7.55 million and $6.09 million in 2014, while Blue Power division contributed $13.24 million and in 2014, profit of $22.6 million. Earnings per stock unit for the quarter fell from 51 cents to 33 cents.

Divisional sales had mixed fortunes with the lumber depot division enjoying an increase of $28 million to $212 million, while sales for the Blue Power division, declined by $3.5 million to $90 million in 2015 compared to July 2014 quarter. Sales for both divisions were higher in the July quarter than for April with the Lumber Depot sales also improved from $189 in April 2015 and Blue Power division from $71 million.

Blue Power jumped to a 52 weeks’ high of $14 on Monday

Cash and equivalent has risen to $168 million from $156 million in 2014 and receivables declined to $74 million but Inventories jumped to $266 million from $220 million while loan financing amounts to just $8.7 million.

The stock which was previously given a BUY RATED grade lost it with the declining profits and no clear indication of a strong pick up in revenues to propel profits upwards to warrant a buy rating at this time.

Profit jumps 129% at Honey Bun

Profit jumped 129 percent over the June 2014 quarter, after taxes for Honey Bun to $17 million for the June 2015 quarter and growth for the nine months period to $64 million versus $41 million, an increase of 58 percent, and cash flow from operation of $98 million from increased sales of 17.5 percent, to $672 million.

Profit jumped 129 percent over the June 2014 quarter, after taxes for Honey Bun to $17 million for the June 2015 quarter and growth for the nine months period to $64 million versus $41 million, an increase of 58 percent, and cash flow from operation of $98 million from increased sales of 17.5 percent, to $672 million.

For the quarter sales grew 20 percent to $218 million from $181 million in 2014, whilst gross profit was up by a larger 24 percent. The company attributes the increase in sales to a strategic restructuring of the sales department. Gross profit margin increased to 45.5 percent up from 44 percent in the June quarter of 2015 versus 2014 and 44.9 percent for the nine months in 2015.

Export sales increased by 48 percent year to date. “The major increase in exports is as a result of our placement in ASDA stores in the UK” Michelle Chong, Chief Executive Officer said, in response to IC Insider.com enquiry, and is in keeping with the Company’s objective of increasing exports.

The problem in the past has been the last quarter with a tendency for lower sales and losses, is the company over this? “The company services a lot of schools and so the summer months are normally reduced due to the holiday season for July and August. We will always have this challenge but we have somewhat overcome a significant portion of it by way of the development of new products that are not directly geared for schools and by targeting other markets also. This has made a significant impact,” Chong stated in response to questions posed to her by IC Insider.com.

Last year there were problems and added cost in the distribution department, it appears that the company is over that for 2015 fiscal. “We have outsourced over 50 of the distribution that was costing us excessively very successfully and last year we were also suffering from 2 of our major distribution vehicles being out of service and so we had to pay a lot for other vehicles to service the deliveries. These critical vehicles are now back in service” Chong said.

Last year there were problems and added cost in the distribution department, it appears that the company is over that for 2015 fiscal. “We have outsourced over 50 of the distribution that was costing us excessively very successfully and last year we were also suffering from 2 of our major distribution vehicles being out of service and so we had to pay a lot for other vehicles to service the deliveries. These critical vehicles are now back in service” Chong said.

Honey Bun would have enjoyed savings in electricity and flour cost with the reduction of prices of oil and wheat on the world market. Chong agrees and indicated, “yes but besides the reduced rates we have also undertaken significant energy conservation on our own. We have also commenced the first phase of a large solar energy project”.

Receivables remained static at $56 million over June 2014 figure while Inventories fell to $45 million from $51 for the same period while payables were up to $59 million from $55 million. The company ended the quarter with $72 million in cash and investments, borrowed funds of $38 million and equity of $363 million. During the fiscal year a dividend totalling $11 million was paid more than twice the $4.7 million paid in the prior fiscal year.

IC Insider’s project a slight loss in the final quarter ending September this year with earnings for the full year to end at 66 cents versus 68 cents reported for the three quarters to June and 43 cents for the fiscal year to September 2014.

Carib Flavours profit up – Now BUY RATED

Ingredients input into Caribbean Flavours products

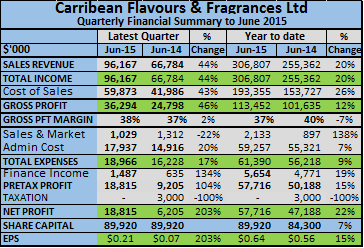

For while the nine months to March showed profit down marginally to $39 million from $40 million, profit for the March quarter was up 20 percent over March 2014 quarter but the June quarter increased by 143 percent to $18.77 million from just $7.6 million for June 2014.

The future much brighter that the past year, for the company that manufactures and distributes flavours mainly for the beverage, baking and confectionery industries and also sells food colouring and fragrances. The company audited financial statements show profit of $58 million or 64 cents per share versus $47 million or 56 cents in 2014, from sales that were up to $307 million from $255 million in 2014. It is the performance of revenues that is the most telling message to flow from the report that points to big improvement in profits to come. Revenues jumped 44 percent in the quarter to reach $96 million the best quarter by far for the financial year.

According to the company’s board, “the economic environment has allowed the company to grow its revenues and profits by securing new markets for fragrances and increasing the volume of sales of flavours to existing and new customers in foreign markets. Based on the outlook for the coming year, it is expected that the company will continue to improve its profits whilst increasing its market share in the domestic and overseas markets”.

According to the company’s board, “the economic environment has allowed the company to grow its revenues and profits by securing new markets for fragrances and increasing the volume of sales of flavours to existing and new customers in foreign markets. Based on the outlook for the coming year, it is expected that the company will continue to improve its profits whilst increasing its market share in the domestic and overseas markets”.IC Insider has projected profits for 2016 at $100 million or $1.10 per share with increased sales and improving profit margins.

Net asset value is $2.25 per share, with the price of the stock on the junior market trading at $2.55 for a PE of just over 3 and 2.3 based on the forecast, indicative of much upside price potential.

General Accident lousy results

General Accident reported lousy first quarter results for 2015, with profit of $26 million and followed that up with even worse figures for the June quarter, just $457,000, and $26.6 million for the first half of 2015, compared with $88 million and $187 million respectively, in 2014. |

General Accident reported lousy first quarter results for 2015, with profit of $26 million and followed that up with even worse figures for the June quarter, just $457,000, and $26.6 million for the first half of 2015, compared with $88 million and $187 million respectively, in 2014. |

Investors were not pleased with the numbers and marked the stock down to a 52 weeks low of $1.30 from which it has made some recovery to $1.50 where it is now trading on the junior market of the Jamaica Stock Exchange.

“For the first half of the year, gross written premium grew to $3.8 billion, an increase of 10 percent over the same period last year despite a sharp contraction in property rates, operating costs also increased by 8 percent in line with our expectations”, management said in their report accompanying the results.

The report when on to state, “Nevertheless, claims charges saw a significant increase by 30 percent to $413 million from $316 and from $169 million for the June 2014 quarter to $228 million in 2015. This sharp increase in claims negatively impacted both our loss ratio and combined ratio which worsened from 86 percent (2014) to 106 percent for comparable periods, respectively”.

The company reported an underwriting loss of $59 million for the half year versus a surplus of $69 million in 2014 and for the Jun e quarter, a loss of $45.6 million compared to a surplus of $20 million.

Investment| Investments delivered reduced income for the first half of 2015 with $94 million earned, below the $125 million generated in 2014 and for the June quarter $50 million versus $68 million in 2014.

“Over short periods of time, our loss ratios may experience significant volatility. Nevertheless, we remain confident that the consistent application of General Accident’s standards and practices will continue to produce underwriting profits over the long-term. As a result, we expect our performance in the second half of the year to improve significantly” Paul Scott, Chairman and Sharon Donaldson, Managing Director reported to shareholders.

Looking forward, investment income could be under threat with lower inflation and interest rates locally and less likelihood of robust gain in the forex market. It will take good management of the various resources to grow income and profits going forward beyond 2015.

Earnings per share for the six months, came out at just 3 cents, down from 18 cents last year.

Profit grows at Jamaican Teas

Jamaican Teas reported profit of $27 million in the June quarter, 35 percent ahead of the March quarter and an 8 percent increase from the similar period in 2014. Nine months’ profit to June was $70 million, an increase of 13 percent over the similar period in the prior year.

Jamaican Teas reported profit of $27 million in the June quarter, 35 percent ahead of the March quarter and an 8 percent increase from the similar period in 2014. Nine months’ profit to June was $70 million, an increase of 13 percent over the similar period in the prior year.

Earnings per share came in at 16 cents for the quarter and 42 cents for the nine months should end around 80 cents for the full year if the houses with signed agreements are handed over and would put the PE ratio at 4 times earnings, net asset value is $4.36 per share for a discount to the last traded price of $3.10. Investors should not lose sight of the unrealized gains on investments which stood at $12 million.

The group is enjoying strong export sales since the commencement of its current financial year with an increase of 48 percent from $194 million to $287 million for the nine months with the latest quarter, moving from $76 million to $103 million. This contributed to the overall increase in sales which moved from $300 million to $324 million, an increase of 8 percent over prior year quarter and $936 million for the period to June compared to $834 million in the prior year.

The export performance comes mainly from changes in the distribution channel in the New York area which started in December 2014 and normalization of sales in the Florida area, following a shift from two distributors to one in 2014. Local sales for the manufacturing segment that are up 2.5 percent for the nine months, suffered an 8 percent fall in the June quarter.

Delivery of the vast majority of the 29 houses completed in the group’s real estate development, is expected to start in September, with sales revenue and profit to be booked in the quarter.

According to Jamaican Teas in their report to shareholders, “the month of August commenced with a significant backlog of export orders resulting expected increase export sales for the September quarter over 2014. Our retails sales have also shown a slight upturn ahead of last year and local sales have improved with the first month’s sales being ahead of the prior year”.

According to Jamaican Teas in their report to shareholders, “the month of August commenced with a significant backlog of export orders resulting expected increase export sales for the September quarter over 2014. Our retails sales have also shown a slight upturn ahead of last year and local sales have improved with the first month’s sales being ahead of the prior year”.

Taxation| Jamaican Teas has now marked its fifth year of being listed on the Junior Market of the Jamaica Stock Exchange, accordingly, effective with the September quarter, the Company will be subjected to taxation at 50% of the standard corporate rate, resulting in a tax charge of 12.5 percent.

At June, shareholders equity stood at $723 million and borrowings at $408 million. With the completed sale of the houses borrowings should fall to $200 million.

Consolidated Bakeries profit falters

Profit in the June quarter dipped to $881,000 compared with $4.3 million in 2014 for Consolidated Bakeries. For the six months profit was up to $14.8 million from $8.9 million as revenues climbed just 2 percent to $398 million. For the quarter revenues fell 11 percent to $171 million as there was a shift in sales relating to Easter occurring in first quarter in 2015 versus the second quarter in 2014.

Profit in the June quarter dipped to $881,000 compared with $4.3 million in 2014 for Consolidated Bakeries. For the six months profit was up to $14.8 million from $8.9 million as revenues climbed just 2 percent to $398 million. For the quarter revenues fell 11 percent to $171 million as there was a shift in sales relating to Easter occurring in first quarter in 2015 versus the second quarter in 2014.

“Furthermore in our efforts to streamline the company we initiated product rationalization this quarter, thus reducing non profitable items thereby contributing to gross profit increases. This initiative slowed sales growth, which we intend to grow in the coming months,” management stated in a report to shareholders accompanying the interim Financials.

“During the second quarter gross profit increased to $68 million compared to $61 million for the same period in 2014. It should also be noted that increased expenses impacted profit from operations. The majority of these expenses can be attributed to our increased marketing activities. We deliberately planned these activities to aggressively reposition our brands against other major players in the market. Our merchandising and promotional ![]() teams were expanded to support this new thrust. We believe these expenses are worthwhile for the long-term growth of the business”, the management’s report went on to state.

teams were expanded to support this new thrust. We believe these expenses are worthwhile for the long-term growth of the business”, the management’s report went on to state.

The improvement in gross profit in spite of the decline in sales is a big positive going forward as it will help to boost the bottom-line at a faster pace than before, if sales increase. Administrative cost rose 18 percent, well ahead of the growth in gross profit of 12 percent, to $41.5 million in the quarter and for the half year by 11 percent to $$79.8 million. Selling and distribution expenses rose 21 percent for the quarter to $26.4 million and for the six months grew 24 percent to $50 million.

Earnings per share came in at 7 cents for the half year but only 0.04 cents in the quarter, the full year results seems set to be around 10 cents.

The company added $20 million to fixed assets, had borrowings of $57 million and cash and investments of $122 million.

D&G profit fell in Q4

Profit fell to $815 million for Desnoes & Geddes, the brewers of the famous Red Stripe beer, in the final quarter of the fiscal year to June, versus $1 billion in 2014. Earnings per share came in at 83 cents with $1.12 in 2014. The latter includes gain on sale of investments in Eastern Caribbean breweries, equal to 35 cents per share. IC Insider is forecasting $1.05 per share earnings, for the year to June 2016.

Profit fell to $815 million for Desnoes & Geddes, the brewers of the famous Red Stripe beer, in the final quarter of the fiscal year to June, versus $1 billion in 2014. Earnings per share came in at 83 cents with $1.12 in 2014. The latter includes gain on sale of investments in Eastern Caribbean breweries, equal to 35 cents per share. IC Insider is forecasting $1.05 per share earnings, for the year to June 2016.

Revenues came in at $4.4 billion for the quarter versus $3.8 billion in 2014, for the full year $16 billion versus $14.3 billion. Sales growth was helped by a combination of increased volume, product mix and price increase, the company stated. Royalties earned amounted to $533 million in the year and $525 million in 2014.

General, selling and administrative expenses were virtually static for the year at $1.26 billion compared to $1.22 billion but marketing cost rose 37 percent to $1.37 billion against an increase of 15.7 percent to $5.46 billion in gross profit.

For 2015, the company paid a dividend of 13 cents in March while a dividend 27 cents was paid in December last year, providing a yield of 12 percent based on the stock price of $4.10 on August 21 last year. Based on the increased profit and past dividend payments, investors can expect to see an increase for the next dividend payment.

The company’s stock last traded at $7 on Friday on the Jamaica Stock Exchange giving it a PE ratio of 8.4 and a 100 percent premium to net asset value.

The stock valuation may be on the high side just now compared with others in the market, there are a few things investors should focus on. These include the likelihood of increased sales that should occur in the period leading up to the next general elections, with the high dividend yield and falling interest rates the stock will become more attractive as an income generator in the not too distant future.

KLE and C2W Music burnt up cash

Junior market entertainment companies, KLE Group and C2W Music continue to burn cash with relatively large losses in the in the quarter and six months to June with one having shredded shareholders capital and the other on the edge of doing so.

Junior market entertainment companies, KLE Group and C2W Music continue to burn cash with relatively large losses in the in the quarter and six months to June with one having shredded shareholders capital and the other on the edge of doing so.

C2W Music reported revenues of just US$4,976 in the June quarter and US$6,028 for the half year but cost rose in the quarter over that of 2014 with US$16,000 versus $12,193 and for the half year US$28,866 versus US$93,605. Finance cost ended at US$1,381 for the quarter and US$2,762 for the year to June. The company reported a loss of US$12,297 and for the six months and US$25,649 in 2014.

The cash burn for the company has virtually wiped out the share capital with only US$17,402 left out of US$1,286,619 raised when it went public, forcing them to seek loan funding which amounted to US$80,950 at June. The results are well off track from what investors were promised when the company had its IPO.

Over at KLE Group the focus is said to be on cost containment and the launching of franchising of the Tracks and Records concept as well as some new income stream.

Over at KLE Group the focus is said to be on cost containment and the launching of franchising of the Tracks and Records concept as well as some new income stream.

For the quarter to June revenues amounts to $54 million with a loss of$12.85 million versus $8.3 million in 2014. For the six months, revenues was $103 million compared with $128 million with losses of $34.6 million and $20.9 million in 2014.

The company has burn through all the equity is raised and more and ended up with negative equity of $10.56 million at June and borrowings of $99 million. While borrowings have grown and payables have fallen from $116 million in June 2014 to $84 million, the composition of the amount tells the story of a company with serious challenges, with GCT due of $7.34 million versus just $146,000 in 2014 and Statutory payables of $10.7 million up from $2.3 million in June 2014 and credit card payables of $9.8 million, at the end of last year June the amount was at $7.2 million.

The lack of capital is driving the nail in the coffins of both companies as revenues are just not there at least currently, to allow for survival.