Government of Jamaica raked in 2.6 percent more tax revenues amounting to $4.9 billion over the $190 billion budgeted to reach $195 billion. Grants fell $3 billion short of budget of $6 billion, and non tax revenues by $800 million resulting in nearly half a billion excess revenue over budget, for the nine months to September.

Government of Jamaica raked in 2.6 percent more tax revenues amounting to $4.9 billion over the $190 billion budgeted to reach $195 billion. Grants fell $3 billion short of budget of $6 billion, and non tax revenues by $800 million resulting in nearly half a billion excess revenue over budget, for the nine months to September.

At the end of the period the fiscal deficit projected, was cut in half, with a deficit of $14 billion. The primary surplus measured in at $51 billion some $11 billion better than planned.

The improved revenues flows came mainly from corporate profit tax of $1.9 billion, SCT on local goods $1 billion, tax on interest $2.6 billion, GCT and SCT on imports of $2 billion. PAYE was off by $474 million, telephone tax $400 million, custom duty $800 million and bauxite levy $500 million.

On the expenditure side, recurrent payments are down by $7.3 billion fueled mainly by $3.4 billion reduction in interest payments and $3.9 million in wages. Capital expenditure is under spent by $6.5 billion.

Lasco Distributors blow out profits

Lasco Distributors with responsibility to distribute “I Cool” drink.

The Gross profit for the period was S1.1 billion, an increase of $299 million or 36 percent over the prior year. The Gross Profit margin for the quarter was $628 million, or 32 percent over the same period last year. Gross profit margin for the august 2015 quarter is 17.26 percent versus 17.5 percent in 2014 and year to date 16.2 percent in 2015 and 16.28 percent in 2014.

The huge gain came from increased revenues of 34 percent for the quarter, amounting to $6.95 billion and 36 percent for the six months of $3.64 billion.

“This growth was driven mainly by contributions from our iCool and Unilever lines of business, both of which have been doing very well”, Peter Chin, Managing Director reported to shareholders in the directors’ report accompanying the financial data.

An interesting element of the results is the 10 percent growth in revenue over the June quarter a continuation of the quarter over quarter growth evident from late in 2014 with an average of 8 percent for the last three quarters.

Earnings per stock for the six months amount to 11 cents and 7 cents for the quarter. IC Insider projects profit of 34 cents for the current year and 50 cents for the year to March 2017.

Cost were held well below the growth in revenues with Operating Expenses in the latest quarter rising to $396 million from $377 in 2014 and for the six months this year the company incurred $779 million versus $658 million in 2014 for a rise of 18 percent.

Cash flow from operations increased by 94 percent to $391 million from $202 million for the similar period to September 2014 swelling Cash and Equivalents at the end of the Period to $904,043 compared with $191,277.

The company’s shares are listed on the junior market of the Jamaica Stock Exchange. Its principal activity is the distribution of pharmaceutical and consumable items, ii distributes all of Lasco Manufacturing’s products locally.

The stock may be considered fully priced currently with a PE of 10 being one of the higher priced junior market stocks, but with strong growth expected and lower interest rates to come, investors with a long term time horizon may want to accumulate from now, bearing in mind the limited supply available.

All Jamaica at new record high

The JSE all Jamaica Composite index is at a new all-time high of 139,537.61 at 11.13am on Monday morning after gaining 2,027.33 points, breaking the old record close of 138,917.59 set on 24th of January 2005.

The JSE all Jamaica Composite index is at a new all-time high of 139,537.61 at 11.13am on Monday morning after gaining 2,027.33 points, breaking the old record close of 138,917.59 set on 24th of January 2005.

The rise in the price of Cable & Wireless shares by 20 cents or 24.4 percent for the day would be the main contributor to the rise. Others to contribute would be Caribbean Cement up $1.72 to $16.72, Mayberry Investments up 50 cents to $3.50 and Sagicor Real Estate X Fund up $1.05 to $9.20.

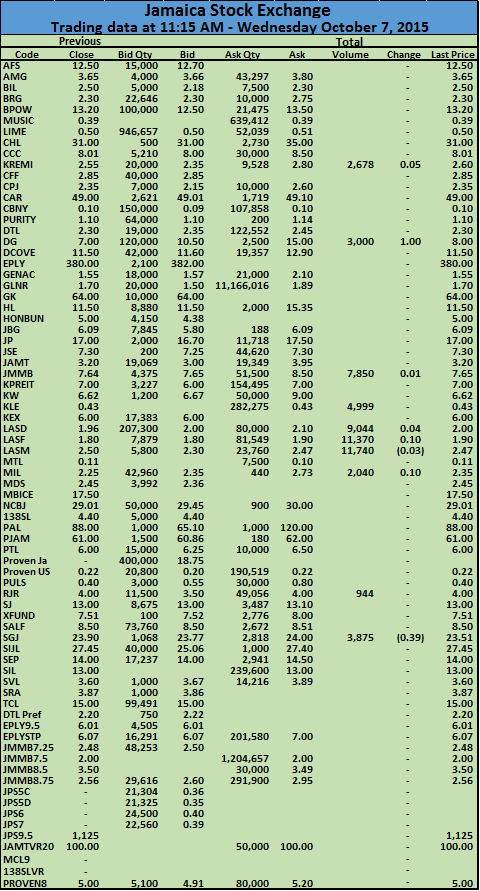

D&G offer pushes JSE, juniors at new high

Activity on the Jamaica Stock Exchange on Wednesday morning has been slow but the news dominating the market is a J$31 offer proposed by Heineken to buy out all the shares in Desnoes & Geddes it does not now own. Heineken bought out the subsidiary of Diageo that owned the shares in Desnoes & Geddes thus giving them majority holdings in the local company. D&G traded at $8 with an increase of $1, the bid is now quoted at $10.50.

Elsewhere, trading so far has seen the junior market at a new all-time high with only a few of the stocks being active. Overall only 10 securities have traded at 11:15 am with a volume of a mere 57,540 units, 2 stocks declined and 6 gained.

Elsewhere, trading so far has seen the junior market at a new all-time high with only a few of the stocks being active. Overall only 10 securities have traded at 11:15 am with a volume of a mere 57,540 units, 2 stocks declined and 6 gained.

Trading activity resulted in the JSE Market Index 535.63 points to 98,338.12. The JSE All Jamaican Composite index rose 598.60 points to 108,854.67, the JSE combined index 617.64 points to be at 102,281.64 and the junior market is up 12.53 points to 1,056.68 for a new record and is not very far off from the all-time high of 1,040.59.

HEINEKEN J$31 offer for D&G shares

Heineken N.V. (“HEINEKEN”) is to make an offer to acquire all of the minority shareholders shares in Desnoes & Geddes at US$0.259 per shares or the equivalent of J$31, the company stated in a release today. Udiam shall offer US$ 0.259 (the “Offer Price”) for each D&G Share. The Offer Price is the same price per D&G Share as Heineken International paid to Diageo in respect to the Acquisition.the offer represents a huge premium on the last traded price of the stock of $8 in trading today. The bid on the stock is now at $10.50.

Heineken N.V. (“HEINEKEN”) is to make an offer to acquire all of the minority shareholders shares in Desnoes & Geddes at US$0.259 per shares or the equivalent of J$31, the company stated in a release today. Udiam shall offer US$ 0.259 (the “Offer Price”) for each D&G Share. The Offer Price is the same price per D&G Share as Heineken International paid to Diageo in respect to the Acquisition.the offer represents a huge premium on the last traded price of the stock of $8 in trading today. The bid on the stock is now at $10.50.

Heineken N.V. (“HEINEKEN”) today has announced that Heineken International B.V. (“Heineken International”), a wholly-owned subsidiary of HEINEKEN, has acquired the entire issued share capital of Udiam Holdings AB (“Udiam”) from a subsidiary of Diageo plc (Diageo plc and its subsidiaries being “Diageo”) for the sum of US$420,992,826 (the “Acquisition”). Udiam owns 1,625,549,827 shares in D&G, which constitutes approximately 57.87% of the share capital of D&G. Heineken International has also acquired a small shareholding which Diageo  held directly in D&G. The price paid by Heineken International to Diageo for Udiam, and the direct shareholding, equates to US$ 0.259 per D&G share. Prior to the Acquisition, another subsidiary of HEINEKEN already owned 434,033,141 D&G shares, which constitutes approximately 15.45% of the share capital of D&G. Following the Acquisition, HEINEKEN indirectly owns 2,059,610,670 shares, which constitutes approximately 73.32% of the share capital of D&G.

held directly in D&G. The price paid by Heineken International to Diageo for Udiam, and the direct shareholding, equates to US$ 0.259 per D&G share. Prior to the Acquisition, another subsidiary of HEINEKEN already owned 434,033,141 D&G shares, which constitutes approximately 15.45% of the share capital of D&G. Following the Acquisition, HEINEKEN indirectly owns 2,059,610,670 shares, which constitutes approximately 73.32% of the share capital of D&G.

As a consequence of the Acquisition, and pursuant to Regulation 12(1) of the Jamaican Takeover Code, Udiam intends to make an offer (the “Offer”) to the shareholders of D&G for the acquisition of any and all of the shares which HEINEKEN does not, directly or indirectly, currently own (the “D&G Shares”). The Offer will be made through a formal tender offer pursuant to the Jamaican Takeover Code and applicable requirements.

Interest saved cuts Phillips’ cost by $10B

Peter Phillips’ assertion that there will be a near $9 billion cut in the 2015/16 budget might have come as a shock to the country already reeling from the pains of severe economic adjustments but much of the work has already be done with a sharp $4.7 billion cut in interest payments to August.

Peter Phillips’ assertion that there will be a near $9 billion cut in the 2015/16 budget might have come as a shock to the country already reeling from the pains of severe economic adjustments but much of the work has already be done with a sharp $4.7 billion cut in interest payments to August.

The savings works out at more than $10 billion for the full year and might be even more with Treasury bill rate continuing to fall as such the Minister’s work seems a mere formality of recognizing that interest cost was over estimated in the first place and not for the first time.

Up to August, apart from the big drop in interest cost capital expenditure was underspent buy $4 billion with just spent out of the $16.3 billion budgeted for the 5 months period. The wages bill was underspent by $3.4 billion with just $$67.9 billion spent out of $71.3 planned. Other areas of recurrent expenditure saw arise of $1.4 billion above budget.

Collector of Taxes office, Constant Spring, Kingston.

Government borrowed $14 billion less in the local market than budgeted taking only $5.8 billion in new funds as opposed to almost $20 billion planned. But they borrowed $255 billion on the foreign side versus $59 billion planned but paid out $180 billion more than budgeted.

Imports & exports down to June

Petroleum imports help cut trade deficit to June

Traditional domestic exports during the 2015 review period grew 3.6 percent over 2014 to US$407 million, while Non-Traditional exports earned declined by a large 29.4 percent or US$92 million to US$220 million in 2015.

Import of buses for JUTC added to the Jamaica’s imports to June.

Excluding motor cars there was an increase in Consumer Goods of 8.7 percent or US$67 million to US$839 million during January to June 2015 compared to the same period in 2014. Expenditure on Capital Goods accounted for US$273 million of imports, up from US$256 million in 2014.

Jamaica ekes out 0.6% growth in Q2

The Mining sector grew the most in Q2

This growth in the June quarter was attributed to improved performance in both the Goods Producing industries and Services industries of 0.8 percent and 0.5 percent respectively, the Statistical Institute of Jamaica (STATIN) said in its report on the economy release at the end of September.

“During the first quarter this year, the Jamaican economy grew by 0.4 percent when compared to the similar quarter of 2014. This growth was due mainly to a 0.6 percent increase in the Services industries” Statin said when they released the first quarter numbers in July. The reports are preliminary as Statin will revise them when more data becomes available.

According to Statin “all industries within the Goods Producing industries recorded higher levels of output: Agriculture, Forestry and Fishing (0.3 percent), Mining and Quarrying (4.1 percent) Manufacturing (0.2 percent) and Construction (0.9 percent).

Agriculture was negatively affected by drought conditions

“The Services industries recorded higher levels of output with the exception of the Producers of Government Services industry which declined by 0.2 percent. Increased output was recorded for: Electricity & Water Supply (0.7 percent), Hotels and Restaurants (1.4 percent), Transport, Storage and Communication (1.4 percent), Wholesale and Retail Trade; Repairs; Installation of Machinery and Equipment (0.3 percent), Finance and Insurance Services (0.4 percent), Real Estate, Renting and Business Activities (0.5 percent) and Other Services (0.5 percent).The Hotels & Restaurants industry was positively impacted by higher tourist arrivals from two of the main markets; the United States of America (USA) and Europe. Growth in Electricity & Water Supply was tempered by drought conditions which affected water production during the review period. Compared with the first quarter of 2015, the economy grew by 1.5 percent. This was largely attributed to an increase in the Goods Producing industries (2.8 percent) and the Services industries (1.1 percent)” the report stated.

Real estate to get a boost

The real estate industry is set to get a boost as Jamaica National Building Society is set to announce a lowering mortgage rates, IC Insider.com has been reliably informed. The announcement could come as early as next week IC Insider.com has learnt.

The real estate industry is set to get a boost as Jamaica National Building Society is set to announce a lowering mortgage rates, IC Insider.com has been reliably informed. The announcement could come as early as next week IC Insider.com has learnt.

Details were not available, but from indications it could result in the current flagship rate of 9.5 percent dropping to 8.5 percent. The move will be a welcomed for the society’s borrowers and will act as a stimulus to the housing market that has seen increased building cost as a result of the falling value of the Jamaican dollar pushing the cost of housing upwards. The decline will come against the background of lowering of repo rates by the country’s central bank and a continuous lowering of Treasury bill rates since early 2014.

The move by Jamaica National is expected to see other long term lenders following the JN lead and should result in an all round fall in borrowing cost for mortgages.

Food prices push inflation in August

‘Vegetables and Starchy Foods’ had the strongest impact on the division moving up by 8.5%

‘Food and Non-Alcoholic Beverages’ recorded the highest movement for the month of 2.1 percent. ‘Vegetables and Starchy Foods’ had the strongest impact on the division moving up by 8.5 percent as drought conditions persisted in the growing areas. The upward overall movement was, however, tempered by declines of 2.3 percent and 0.5 percent in the divisions ‘Housing, Water, Electricity, Gas and Other Fuels’ and ‘Transport’ due to lower petrol prices and reduction in air fares.

Other divisions that recorded increases are: ‘Alcoholic Beverages and Tobacco’ 0.2 percent, ‘Clothing and Footwear’ 0.3 percent, ‘Furnishings, Household Equipment and Routine Household Maintenance’ 0.2 percent, ‘Health’ 0.1 percent, ‘Recreation and Culture’ 0.4 percent, ‘Miscellaneous Goods and Services’ 1.3 percent, while ‘Restaurants and Accommodation Services’ recorded a 0.2 percent increase. ‘Education’ and ‘Communication’ remained unchanged.