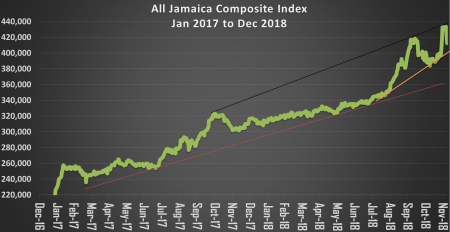

After the main market of the Jamaica Stock Exchange suffered one of its largest declines in its history, with the JSE All Jamaican Composite Index having dived 10,996.27 points on Thursday, the index plunged another 9,551.77 points on Friday to close at 412,491.83 on a day of mostly falling prices.

After the main market of the Jamaica Stock Exchange suffered one of its largest declines in its history, with the JSE All Jamaican Composite Index having dived 10,996.27 points on Thursday, the index plunged another 9,551.77 points on Friday to close at 412,491.83 on a day of mostly falling prices.

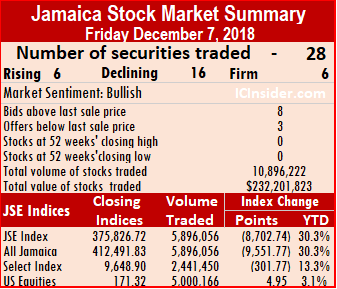

The JSE Index dropped 8,702.74 points, following the fall of 10,018.84 on Thursday to close at 375,826.72 on Friday. The market got hit with the sharp pull back in the prices of some heavily weighted stocks with NCB Financial, Sagicor Group and Scotia Group leading the pack with the former pulling back from $159 to $149.90, the Sagicor declining from $47.50 to $41 and Scotia declining from $59 at the start of Thursday to $54.01 on Friday.

At the end, 28 securities changed hands in the main and US dollar markets with prices of just 6 rising, 16 declining and 6 remaining unchanged compared to 30 securities trading on Thursday.

The main market ended with 5,896,056 units valued at $161,797,148 trading, compared with 1,266,059 units valued at $39,894,741 changing hands on Thursday.

The main market ended with Mayberry Investments trading 1,715,395 units, accounting for just over 29 percent of the volume, followed by Sagicor Group with 1,388,644 units or 23.55 percent of the day’s volume and JMMB Group with 1,314,699 units and 22.30 percent of the day’s volume.

IC bid-offer Indicator|The Investor’s Choice bid-offer indicator reading shows 8 stocks ending with bids higher than the last selling prices and 3 closing with lower offers.

Trading resulted in an average of 226,771 units valued at over $6,222,967, in contrast to 46,891 shares valued at $1,477,583 on Thursday. The average volume and value for the month to date amounts to 128,316 units with a value of $3,599,881 compared to 104,614 units valued at $2,135,092, previously. November closed, with an average of 405,528 valued at $7,755,942, for each security.

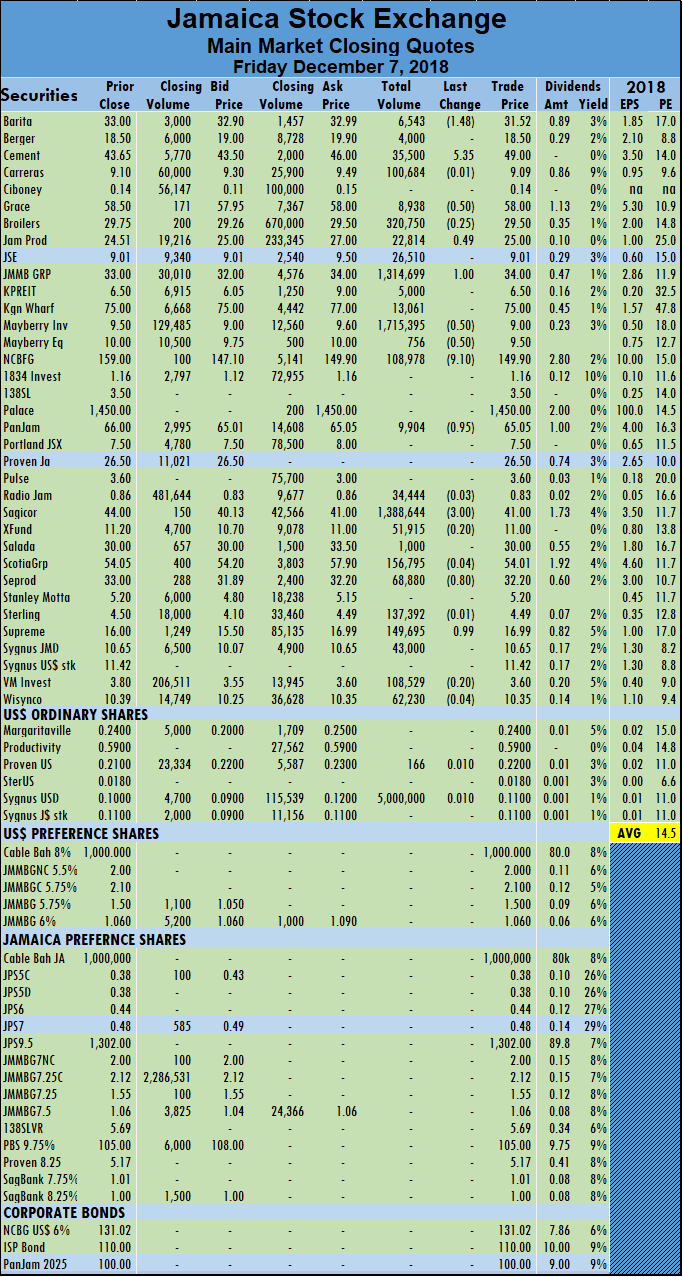

In main market activity, Barita Investments dropped $1.48 to end at $31.52, with 6,543 shares changing hands, Caribbean Cement jumped $5.35 and finished trading 35,500 shares at $49, Grace Kennedy dropped 50 cents and ended trading 8,938 shares at $58.  Jamaica Producers finished trading of 22,814 units with a gain of 49 cents to close at $25, JMMB Group jumped $1 and ended at $34 with 1,314,699 shares changing hands, Kingston Wharves fell 70 cents to $75, with 6,800 stock units changing hands. Mayberry Investments fell 50 cents trading 1,715,395 shares in closing at $9, Mayberry Equities fell 50 cents trading only 756 shares in closing at $9.50, NCB Financial Group dived $9.10 to end trading of 108,978 shares at $149.90, PanJam Investment lost 95 cents to close at $65.05, with an exchange of 9,904 stock units, Sagicor Group fell $3 to finish trading of 1,388,644 shares at $41, Seprod traded 68,880 shares, dropping 80 cents in the process to close at $32.20 Supreme Ventures rose 99 cents and ended at $16.99, with 149,695 shares exchanged.

Jamaica Producers finished trading of 22,814 units with a gain of 49 cents to close at $25, JMMB Group jumped $1 and ended at $34 with 1,314,699 shares changing hands, Kingston Wharves fell 70 cents to $75, with 6,800 stock units changing hands. Mayberry Investments fell 50 cents trading 1,715,395 shares in closing at $9, Mayberry Equities fell 50 cents trading only 756 shares in closing at $9.50, NCB Financial Group dived $9.10 to end trading of 108,978 shares at $149.90, PanJam Investment lost 95 cents to close at $65.05, with an exchange of 9,904 stock units, Sagicor Group fell $3 to finish trading of 1,388,644 shares at $41, Seprod traded 68,880 shares, dropping 80 cents in the process to close at $32.20 Supreme Ventures rose 99 cents and ended at $16.99, with 149,695 shares exchanged.

Trading in the US dollar market amounted to 5,000,166 units valued at $550,037 as Proven Investments rose 1 cents and ended at 22 US cents with just 166 shares changing hands and Sygnus Credit Investments US dollar based ordinary share rose 1 cent trading 5 million units to end at 11 US cents. The JSE USD Equities Index closed with a rise of 4.95 points to close at 171.32.

Modest Junior Market trading on Friday

Trading on the Junior Market of the Jamaica Stock Exchange was modest on Friday with just 60 percent of Thursday’s volume on and just 37 percent of the value.

Trading on the Junior Market of the Jamaica Stock Exchange was modest on Friday with just 60 percent of Thursday’s volume on and just 37 percent of the value.

Trading resulted in an exchange of 990,418 units valued at $3,442,516 compared to 1,715,859 units valued at $9,303,423 on Thursday.

Trading ended with an average of 43,062 units for an average of $149,675 in contrast to 74,603 units for an average of $404,497 on Thursday.

The average volume and value for the month to date amounts to 172,792 units at a value of $556,427, versus 204,876 units at a value of $657,021, previously. November, ended with an average of 190,475 units valued at $653,358 for each security traded.

The market Index rose 10.84 points to close at 3,179.06 after 7 securities advanced, 7 declined, while 9 remained unchanged as 23 securities changing hands versus 23 on Thursday.

IC bid-offer Indicator| At the end of trading, the Investor’s Choice bid-offer indicator reading shows 3 stocks ended with bids higher than their last selling prices and just 7 with lower offers.

At the close of the market activity, AMG Packaging ended trading with 22,000 stock units, at $1.70, Blue Power concluded trading of 5,000 units at $5.45, CAC 2000 closed at $16.90, trading 5,000 shares, Caribbean Cream ended trading of 1,000 shares with a rise of 70 cents to close at $6, Caribbean Producers finished trading with a loss of 5 cents at $5.35, with 42,624 units changing hands. Consolidated Bakeries closed at $2.15, with 181,111 shares switching owners, Everything Fresh traded 236,237 shares after gaining 9 cents to close at $1.67, Express Catering ended trading with 67,753 shares after rising 40 cents higher to $8, FosRich Group traded at $3.60, with an exchange of 36,824 shares, General Accident finished trading of 2,000 shares at $3.75. GWest Corporation closed with a loss of 5 cents at $1.50, with 6,782 stock  units, Honey Bun ended 28 cents higher at $3.80, with 10,390 units, Indies Pharma traded 84,004 shares to close at $3.15, Iron Rock concluded trading 20 cents higher at $3.70, with 5,000 shares changing hands, Jamaican Teas settled 8 cents higher at $3.78, with an exchange of 24,862 shares. Jetcon Corporation ended trading with a loss of 8 cents at $3.32, with 10,000 stock units changing hands, Knutsford Express closed with a loss of 13 cents at $11.50 and ended trading 1,000 shares, Lasco Distributors ended with a loss of 20 cents at $3.70, and finished trading 166,901 shares, Lasco Financial concluded trading of 5,743 stock units and rose 15 cents higher to $4.15. Lasco Manufacturing finished trading 200 units at $3.45, Main Event settled at $6.50, in exchanging 17,000 shares, Medical Disposables ended trading of 50,000 shares with a loss of 10 cents at $6.40 and Stationery and Office finished trading with a loss of 45 cents at $8.50, with 8,987 stock units changing hands.

units, Honey Bun ended 28 cents higher at $3.80, with 10,390 units, Indies Pharma traded 84,004 shares to close at $3.15, Iron Rock concluded trading 20 cents higher at $3.70, with 5,000 shares changing hands, Jamaican Teas settled 8 cents higher at $3.78, with an exchange of 24,862 shares. Jetcon Corporation ended trading with a loss of 8 cents at $3.32, with 10,000 stock units changing hands, Knutsford Express closed with a loss of 13 cents at $11.50 and ended trading 1,000 shares, Lasco Distributors ended with a loss of 20 cents at $3.70, and finished trading 166,901 shares, Lasco Financial concluded trading of 5,743 stock units and rose 15 cents higher to $4.15. Lasco Manufacturing finished trading 200 units at $3.45, Main Event settled at $6.50, in exchanging 17,000 shares, Medical Disposables ended trading of 50,000 shares with a loss of 10 cents at $6.40 and Stationery and Office finished trading with a loss of 45 cents at $8.50, with 8,987 stock units changing hands.

Prices of securities trading for the day are those at which the last trade took place.

Mostly modest price change on TTSE – Friday

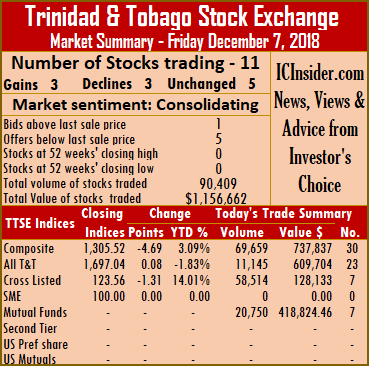

In market activity on the Trinidad & Tobago Stock Exchange on Friday ended with trading in 11 securities against 17 on Thursday, with 3 advancing, 3 declining and 5 remaining unchanged on a day when both the volume a value of trading fell below Thursday’s levels.

In market activity on the Trinidad & Tobago Stock Exchange on Friday ended with trading in 11 securities against 17 on Thursday, with 3 advancing, 3 declining and 5 remaining unchanged on a day when both the volume a value of trading fell below Thursday’s levels.

At close of the market the Composite Index shed 4.69 points on Friday to 1,305.52. The All T&T Index inched 0.08 points higher to 1,697.04, while the Cross Listed Index declined 1.31 points to close at 123.56.

Trading ended with 90,409 shares at a value of $1,156,662 compared to 224,227 shares at a value of $4,223,600 on Thursday.

IC bid-offer Indicator| The Investor’s Choice bid-offer ended with 1 stock with the bid lower than the last selling price and 5 with lower offers.

Stocks closing with gains| Clico Investments rose 5 cents and ended at $20.20, with 20,750 stock units changing hands, Massy Holdings climbed $1 and concluded trading at $46, after exchanging just 310 shares  and Trinidad & Tobago NGL finished 8 cents higher at $29.23, exchanging 2,315 shares.

and Trinidad & Tobago NGL finished 8 cents higher at $29.23, exchanging 2,315 shares.

Stocks closing with losses|First Citizens fell 4 cents and settled at $32.76, after exchanging 50 shares, JMMB Group closed with a loss of 3 cents and concluded trading at $1.77, after exchanging 55,000 shares and NCB Financial Group shed 22 cents and settled at $8.70, trading 3,400 shares.

Stocks closing firm|One Caribbean Media concluded market activity at $10.50, with 3,745 shares changing hands, Republic Financial Holdings closed at $107.26, after exchanging 3,161 shares, Sagicor Financial ended at $9.24, with 114 stock units changing hands, Scotiabank completed trading of 20 units at $64.74 and West Indian Tobacco completed trading of 1,544 units at $95.07.

Prices of securities trading for the day are those at which the last trade took place.

Blue Power profit jumped 55%

Sales at Blue Power for the half year of its 2019 fiscal year to October, increased 13 percent to $862 million from $761 million for the same period in 2017, while sales for the second quarter to October were up nearly 12 percent to $426 million from $381 million for the same period in 2017.

Sales at Blue Power for the half year of its 2019 fiscal year to October, increased 13 percent to $862 million from $761 million for the same period in 2017, while sales for the second quarter to October were up nearly 12 percent to $426 million from $381 million for the same period in 2017.

Profits for the six months grew 55 percent to $87 million, from $56 million in the same period last year. For the second quarter profit after tax jumped 52 percent to $26.6 million from $17.5 million in 2017 in spite of picking up foreign exchange losses in the current period. Earnings per stock rose from 10 cents to 15.4 cents for the half year.

Lumber Depot sales rose 9 percent from $544 million to $592 million and the Blue Power division increased 25 percent from $217 million to $270 million for the six months

The Lumber Depot contributed $38 million before tax compared to $32 million in 2017 while Soap Division jumped to $61 million from $2 million in 2017.

Net finance cost was $9.5 million compared to $2.7 million for the quarter and for the six months it was a net inflow of $13 million in 2018 and was flat for the 2017 period.

For the half year, “exports sales of soap accounted for 24 percent of overall soap sales,” Noel Dawes, Managing Director told shareholders, in a report accompanying the financials. He further stated that “sales in the Caribbean market continue to be brisk as greater interest, acceptance and satisfaction of our product range materialize. The increase in export sales over the same quarter in the previous year was 64 percent from $47 million to $77 million.”

The company should earn around 30 cents per share for the current fiscal year and close to 40 cents for the next fiscal year ending April 2020. The stock trades at $5.45 at a PE ratio of 18 times estimated current year’s earnings.

Blue Power has investments and cash funds amounting to $247 million, with current assets of $655 million versus current liabilities of just $131 million and shareholders equity of $839 million.

Why is Fontana IPO priced so low?

Owners and directors along with their advisors ought to know the value of their company. But this publication must ask the question if Fontana has really done so well and will continue to expand, why is it priced so low?

Owners and directors along with their advisors ought to know the value of their company. But this publication must ask the question if Fontana has really done so well and will continue to expand, why is it priced so low?

At a premium over net book value of 88 percent, the stock is one of the cheapest of Junior Market listings, with the vast majority selling at a premium of 3 to 4 net book and an average PE of around 13 excluding the extreme highs and lows. One would expect the stock to be priced closer to 10 times earnings before tax, that would put the price closer to $3 than $1.88 and that would place price to net asset value at a premium of 200 percent, still below the market average. The fact that the company is setting up a new branch and looking for more expansion, makes the case for a higher price more compelling as investors are most likely going to rake in much profit from this stock. The only problem the general public will not get many shares to buy up front as it is set tobe heavily oversubscribed. Investors can expect this one to at least double shortly after listing.From where we sit we think the brokers did the owners out of several million dollars on this issue but then the owners may want Jamaicans to party with them on the 50th anniversary.

Scotia Group stuck in neutral

Investors could find themselves in shark infested waters if they are not careful with the prices of several stocks now at very high levels. Investors need to be careful of being sucked into attractive profit results that are not based on sustainable earnings.

A case in point is Scotia Group. In the July quarter the interim results showed a big jump in profits, but that was based on an unsustainable rise in foreign exchange earnings due to the slippage of the Jamaican dollar, resulting in nearly $2 billion raked in for the quarter. For the October quarter only $396 million is reported for that line item, but the year shows a big jump from $2.5 billion to $4 billion. Net interest income is on the slide, falling from $26.64 billion in 2017 to $25.2 billion in 2018 and in the quarter the decline continues with October falling to $6.1 billion from $6.3 billion in July and $6.7 billion in the October quarter in 2017. While loan provisioning is down, year over year to October, to $1.9 billion from $2.2 billion it rose in the final quarter to $744 million from $695 in 2017 and $620 million in July this year. Net fee income has been steady for the various quarters at just over $2 billion but fell in the fiscal 2018 year to $8.1 billion from $8.6 billion.

Operating expenses rose to $5.74 billion in the October quarter from $5.1 in July and $5.18 billion for the 2017 final quarter. For the full year operating expenses rose to $22 billion from $21.3 billion. The group had a gain on disposal of a subsidiary of $753 million which saved profit from falling for the latest year with a rise to $12.78 billion from $12.17 billion in 2017. For the quarter, profit dropped to just $1.6 billion from $3.36 billion in 2017.

Importantly, the loan portfolio that rose strongly in the July quarter to $177 billion is up at a slower pace of 3.2 percent to $183 billion, an annual pace of 13 percent, but it needs to increase further to really deliver a reasonable increase in profit going forward.

The stock closed at $54.05 on the Jamaica Stock Exchange on Thursday, but its recent profit performance does not send very encouraging signals to buy.

Fontana IPO set for heavy oversubscription

Fontana’s prospectus initial public offer, first mentioned by IC Insider.com is now out but with confusion as to the pricing. The price seems to be $1.88 except for reserved shares at $1.69 each.

Fontana’s prospectus initial public offer, first mentioned by IC Insider.com is now out but with confusion as to the pricing. The price seems to be $1.88 except for reserved shares at $1.69 each.

Whether the price is 1.88 or $2 the stock is priced very attractively priced for investors at a PE that is well below that of the Junior Market that it will be listed on and is expected to be heavily oversubscribed. The general public has been allocated 113,434,802 shares at a PE ratio of just 6.4 times 2018 earnings, well below the market average of more than 15, but things get even better as the interim results to September this year show a huge jump in profit from $11.5 million to $51 million before tax, with sale revenues up just 5.5 percent to $936 million while cost of sales declined from $650 million to $640 million, thus improving gross profit margin. While revenues grew just 5.5 percent in the quarter administrative cost climbed faster by nearly 10 percent to $223 million. At the same time inventories rose 19 percent to $680 million over the levels at September 2017 and are up 15 percent from June 2018 figure, a development that requires clarification. The PE ratio based on the interim figures suggest that the PE will fall to around 6 or less for the 2019 fiscal year, with good prospects for continued growth in the business.

The Company, in March 2013 acquired the former Azmart location in Barbican Square, Kingston and opened its Ocho Rios location in November 2013. There has been significant growth in sales from these locations. Kingston and Ocho Rios branches now represent 27 percent and 16 percent of the total sales, respectively, the Company stated. Revenues from the Ocho Rios branch increased from $113 million in 2014 to $536 million in 2018, while revenues at the Kingston branch grew from $508 million in the 2014 fiscal year to $871 million in 2017 with growth slowing to 5 percent in the financial year 2018.

The new Waterloo Square location which will open in financial year 2019, is expected to add 28,000 square feet of retail space, an increase of over 40 percent and bolster sales. It is expected that the Waterloo Square store will provide greater buying power to negotiate more favourable terms and rebates with key pharmaceutical partners on the local market. The company is seeking further opportunities to expand its branch network in growing communities such as Montego Bay and Portmore. The anticipated increase in sales will provide greater critical mass to support the sourcing of higher volumes of inventory directly from China with greater margins.

The Company invites Applications for 124,937,565 Subscription Shares, which are to be newly issued. The Company is also inviting Applications on behalf of the Selling Shareholder for 124,937,400 shares. A total of 136,440,163 shares that are initially reserved for priority applications. The minimum amount to be raised by the Company from the sale of the Subscription Shares is $234,040,086.

The Company was established in 1968 at the Manchester Shopping Centre in Mandeville by Shinque “Bobby” Chang and Angela Chang. Today, the Company is run by Kevin O’Brien Chang (Chairman), Anne Chang (Chief Executive Officer) and Raymond Therrien (Chief Operating Officer) with the support of Independent Directors. The Company operates pharmacies and retail stores in Jamaica with 5 locations across the island and 330 employees. Its core business is the sale of pharmaceutical products through licensed pharmacies, and a range of beauty and cosmetic items, housewares, home décor, toys, baby items, electronic, school and souvenir products.

The Company recorded revenues of $3.4 billion in financial year 2018, representing an increase of $272 million or 8.66% over the prior year and an increase of approximately 91% from $1.76 billion in 2014. Pretax profit for 2018 declined 6 percent from $322 million in 2017 to $303 million after rising from $237 million in 2016 that was up more than 100 percent over the 2015 profit of $115 million. The slowdown in 2018 is attributed to the state of emergency in Montego Bay and road construction in the Barbican area.

The stock has been accorded IC Insider.com critical BUY RATED accolade.

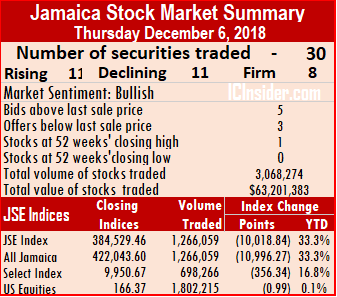

Huge dive in JSE main market – Thursday

Barita climbs to a new high of $33 on Thursday.

After two days of modest gains the main market of the Jamaica Stock Exchange, suffered one of its largest declines in its history, with the JSE All Jamaican Composite Index plunging 10,996.27 points to 422,043.60 and the JSE Index nosediving 10,018.84 points to close at 384,529.46 on a day of modest volume.

At the end, 30 securities changed hands in the main and US dollar markets with prices of 11 stocks rising, 11 declining and 8 remaining unchanged compared to 28 securities trading on Wednesday.

Barita Investments ended trading at another record close of $33.

The main market ended with a mere 1,266,059 units valued at $39,894,741 changing hands, compared with 4,455,571 units valued at $87,653,782 that were exchanged on Wednesday.

The main market ended with Seprod leading with 342,787 units, accounting for 27 percent of the day’s trades, followed by JMMB Group with 168,541 units or 13 percent of the day’s volume.

IC bid-offer Indicator|The Investor’s Choice bid-offer indicator reading shows 5 stocks ending with bids higher than the last selling prices and 3 closing with lower offers.

Trading resulted in an average of 46,891 units valued at an average of $1,477,583 for each security traded. In contrast to 171,368 units for an average of $3,371,299 on Wednesday. The average volume and value for the month to date amounts to 104,614 units valued at $2,135,092 compared to 123,855 units with a value of $2,354,261, previously. November closed, with an average of 405,528 valued at $7,755,942, for each security.

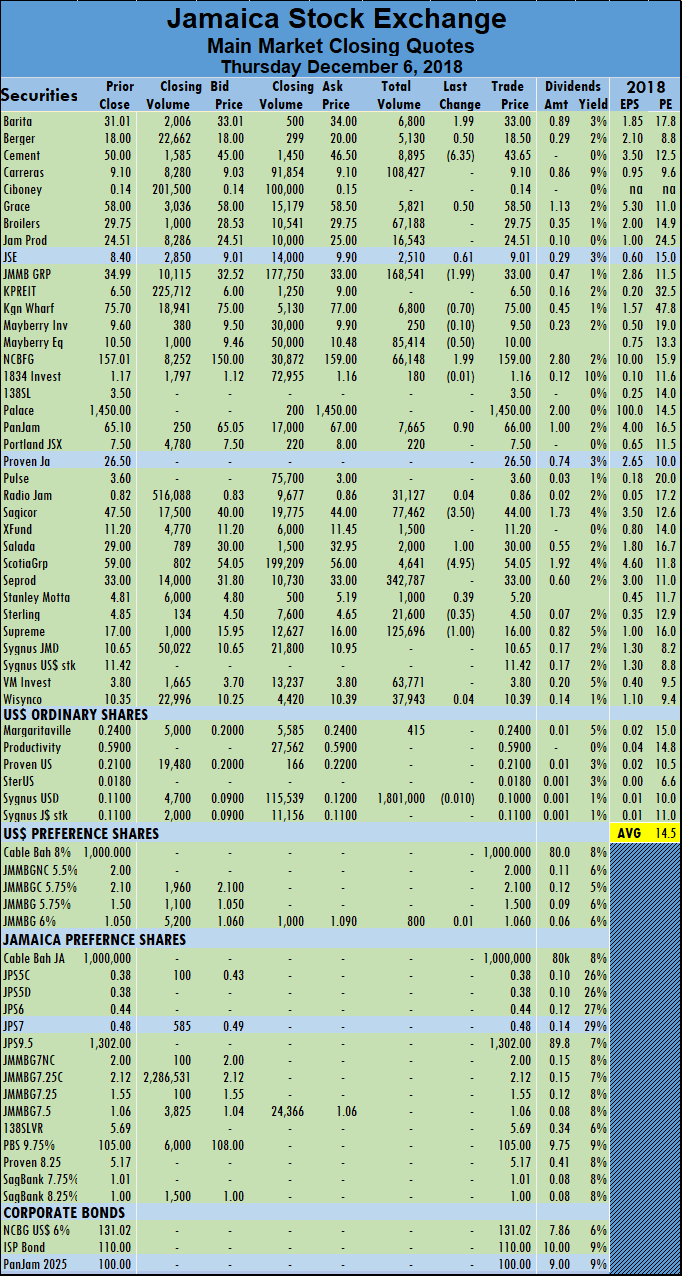

In main market activity, Barita Investments jumped $1.99 to end at a record close of $$33, with 6,800 shares changing hands, Berger Paints gained 50 cents and ended at $18.50, with 5,130 stock units trading, Caribbean Cement dropped $6.35 and finished trading 8,895 shares at $43.65, Grace Kennedy rose 50 cents and ended trading 5,821 shares at $58.50. Jamaica Stock Exchange rose 61 cents to $9.01, trading 2,510 shares, JMMB Group dropped $1.99 ending at $33 with 168,541 shares changing hands, Kingston Wharves fell 70 cents to $75, with 6,800 stock units changing hands. Mayberry Equities fell 50 cents trading 85,414 shares in closing at $10, NCB Financial Group added $1.99 to end trading of 66,148 shares at $159, PanJam Investment added 90 cents to $66, with an exchange of 7,665 stock units, Sagicor Group fell $3.50 to finish trading of 77,462 shares at $44, Salada Foods ended trading with a rise of $1 to close at $30 trading 2,000 stock units, Scotia Group traded 4,641 shares and dropped $4.95 to close at $54.05 Supreme Ventures lost $1 and ended at $16, with 125,696 shares exchanged.

stock units changing hands. Mayberry Equities fell 50 cents trading 85,414 shares in closing at $10, NCB Financial Group added $1.99 to end trading of 66,148 shares at $159, PanJam Investment added 90 cents to $66, with an exchange of 7,665 stock units, Sagicor Group fell $3.50 to finish trading of 77,462 shares at $44, Salada Foods ended trading with a rise of $1 to close at $30 trading 2,000 stock units, Scotia Group traded 4,641 shares and dropped $4.95 to close at $54.05 Supreme Ventures lost $1 and ended at $16, with 125,696 shares exchanged.

Trading in the US dollar market amounted to 107,117 units valued at $22,155 as JMMB 6% preference share rose 1 cent and ended trading at $1.06 with 800 stock units and Margaritaville ended at 24 US cents with 415 shares changing hands and Sygnus Credit Investments US dollar based ordinary share lost 1 cent trading 1,801,000 units to end at 10 US cents. The JSE USD Equities Index closed with a rise of 1.11 points to close at 167.36.

Junior Market inched higher – Thursday

![]() Trading on the Junior Market of the Jamaica Stock Exchange ended on Thursday with a miniscule increase in the Index of 2.46 points to 3,168.22 after 11 securities advanced, 5 declined, while 7 remained unchanged as 23 securities changed hands versus 23 on Wednesday.

Trading on the Junior Market of the Jamaica Stock Exchange ended on Thursday with a miniscule increase in the Index of 2.46 points to 3,168.22 after 11 securities advanced, 5 declined, while 7 remained unchanged as 23 securities changed hands versus 23 on Wednesday.

Trading resulted in an exchange of 1,715,859 units valued at $9,303,423 compared to 5,429,367 units valued at $18,378,072 on Wednesday.

Trading ended with an average of 74,603 units for an average of $404,497 in contrast to 236,059 units for an average of $799,047 on Wednesday. The average volume and value for the month to date amounts to 204,876 units at a value of $657,021, versus 247,680 units $739,994, previously. November, ended with an average of 190,475 units valued at $653,358 for each security traded.

IC bid-offer Indicator| At the end of trading, the Investor’s Choice bid-offer indicator reading shows 4 stocks ended with bids higher than their last selling prices and just 3 with lower offers.

At the close of the market activity, AMG Packaging ended 10 cents higher at $1.70, with 45,300 stock units changing hands, Cargo Handlers settled at $15, trading 8,130 shares, Caribbean Producers finished trading of 4,784 units, at $5.40, Consolidated Bakeries closed at $2.15, trading 2,000 shares, Derrimon Trading ended at $2.65, with an exchange of 111,364 shares. Elite Diagnostic finished trading with 15,140 stock units and rose 2 cents to $2.87, Eppley settled at $9, in exchanging 385 units, Express Catering ended trading with a loss of 20 cents at $7.60, with 14,000 shares, FosRich Group traded 5,200 shares with a loss of 40 cents at $3.60. General Accident finished trading 25 cents higher at $3.75, with 64,860 shares, GWest Corporation closed 10 cents higher at $1.55, with 10,000 stock units trading, Indies Pharma traded 411,391 shares and gained 3 cents to close at $3.15, Jamaican Teas settled at $3.70, while exchanging 42,931 shares, Jetcon Corporation ended trading 4,700 stock units for 40 cents higher at $3.40. Key Insurance traded 14,900 units, with a loss of 2 cents at $4.98, Lasco Distributors ended with a loss of 10 cents at $3.90, exchanging 3,000 shares, Lasco Financial concluded trading with 166,552 stock units, 20 cents higher at $4, Lasco Manufacturing finished 15 cents higher at $3.45, with 117,500 units. Main Event settled at $6.50, trading 1,129 shares, Medical Disposables ended trading 51,500 shares and gained 30 cents to close at $6.50, Paramount Trading closed with a loss of 2 cents at $2.95, in an exchange of 6,906 shares, SSL Venture Capital traded 15,798 shares and added just 1 cent to end at $1.80 and Stationery and Office finished trading 30 cents higher at $8.95, with 598,389 stock units changing hands.

General Accident finished trading 25 cents higher at $3.75, with 64,860 shares, GWest Corporation closed 10 cents higher at $1.55, with 10,000 stock units trading, Indies Pharma traded 411,391 shares and gained 3 cents to close at $3.15, Jamaican Teas settled at $3.70, while exchanging 42,931 shares, Jetcon Corporation ended trading 4,700 stock units for 40 cents higher at $3.40. Key Insurance traded 14,900 units, with a loss of 2 cents at $4.98, Lasco Distributors ended with a loss of 10 cents at $3.90, exchanging 3,000 shares, Lasco Financial concluded trading with 166,552 stock units, 20 cents higher at $4, Lasco Manufacturing finished 15 cents higher at $3.45, with 117,500 units. Main Event settled at $6.50, trading 1,129 shares, Medical Disposables ended trading 51,500 shares and gained 30 cents to close at $6.50, Paramount Trading closed with a loss of 2 cents at $2.95, in an exchange of 6,906 shares, SSL Venture Capital traded 15,798 shares and added just 1 cent to end at $1.80 and Stationery and Office finished trading 30 cents higher at $8.95, with 598,389 stock units changing hands.

Prices of securities trading for the day are those at which the last trade took place.

Fontana another IPO another set of errors

This is an unfortunate development for yet another issue, that seems very attractively priced. The directors have all signed off on the document that has gone through the Financial Services Commission, the Jamaica Stock Exchange and the Company Office of Jamaica, so why the errors and important ommission.

The introduction in the prospectus speaks to a price of $1.88 except for reserved shares at $1.69 but later on in the body of the document it speaks to a price of $2 for each share, making it unclear exactly what the price really should be? In the interim results to September, there are two issues, one is an error and the other, information that really needs clarification. The interim cash flow has no profit, nor depreciation and it therefore is not balanced and needs correcting.

The gross profit in the interim results jumped sharply,even as revenues grew just 5.5 percent with inventories are up 19 percent at the end of the quarter over 2017 and 15.5 percent over June this year. Why the big jump in inventories with sales are just rising moderately? Importantly, this raises questions about the accuracy of the inventory levels and the gross profit margin for 2018. Management should explain the sharp changes in this area so that investors can better understand why there is such a sharp jump in the quarterly profit.

This publication finds it difficult to once more raising issues relating to a prospectus. We are concerned that enough care is not going into them. The breach of GWest Corporation relating to the non-disclosure of information relating to an extraordinary meeting that was said to approve the issue of preference shares that was never brought to investors’ attention is fresh and has not been properly dealt by the regulators or the company. The regulators seem to have turned a blind eye to it. We need to raise the standards if the capital market integrity is the be enhanced.