Caribbean Creams profit upgraded to show a 62 percent increase to $56.8 million or 15 cents per share above the 2014 earnings, according the audited financial statements compiled by KPMG, the company’s new auditors.

Caribbean Creams profit upgraded to show a 62 percent increase to $56.8 million or 15 cents per share above the 2014 earnings, according the audited financial statements compiled by KPMG, the company’s new auditors.

The comparative 2014 results were $35 million after a small tax expense. The interim report had profit for the year at $49 million on slightly higher sales than the audit report showed. The major area of change was lower administrative cost of $12 million in the audited accounts versus the preliminary figures. Caribbean Cream enjoyed an increase of 305 percent in profit in the final quarter to reach $25.7 million up from $6.4 million in 2014 quarter, according to the data in the audited accounts and third quarter interim results.

IC Insider is forecasting profit of 244 million for the 2016 fiscal year or 65 cents per share from increased sales revenues that will flow mainly from a 15 percent price increase effected just before the Christmas season.

The stock which was listed on the junior market of the Jamaica Stock Exchange in 2013 at an IPO price of $1, traded at $1.10 on Thursday and has moved up from 65 cents just before the release of the interim results.

Caribbean Cream profit upgrade

Purity profit jumps 204%

A 204 percent increase in profit for Consolidated Bakeries better known as Purity, in the March quarter saw net profit ending at $13.9 million (2014 $4.58 million) from a 15 percent increase in revenues of $226.28 million.

A 204 percent increase in profit for Consolidated Bakeries better known as Purity, in the March quarter saw net profit ending at $13.9 million (2014 $4.58 million) from a 15 percent increase in revenues of $226.28 million.

Gross profit margin increased to 34.2 percent from 30.6 percent in 2014 and contributed much to the increased profit. Lower electricity cost would have made a big contribution to the improvement in this area. Administrative and other expenses rose less than revenues at 6.7 percent and selling and distribution expenses rose by 12.1 percent just below the growth in revenues.

The company earned 6 cents per share well up on that for 2014 and compares with the 8.4 cents reported for the twelve months of 2014, IC Insider is forecasting 20 cents for the full year. With the stock price at $1.15 on the junior market, it boasts a PE of 5.7 and has a net asset value of $2.42.

Consolidated Bakeries that produces and markets baked products such as breads, buns, crackers and cookies has equity of $540 million, loans of $64 million and cash funds of $110 million.

JSE Markets up pace slowing

Grace fell $1 after reporting a decline in Q1 profits

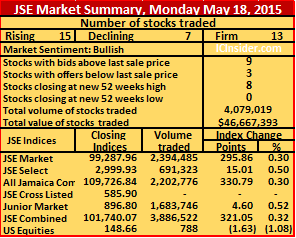

Activity on the Jamaica Stock Exchange, resulted in the prices of 15 stocks rising, including 8 new 52 weeks’ high, 7 declining as 35 securities changed hands, ending in 4,079,019 units trading, valued at $46,667,393, in all market segments. The JSE Market Index gained 295.86 points to 99,287.96, the JSE All Jamaican Composite index rose 330.79 points to close at 109,726.84 and the JSE combined index gained/ put on 321.05 points to close at 101,740.07. Stocks closing at new 52 weeks’ highs, in the main market are, Berger Paints, Desnoes and Geddes, Caribbean Cement, Jamaica Broilers and Radio Jamaica.

IC bid-offer Indicator| At the end of trading, in the main and junior markets, the Investor’s Choice bid-offer indicator shows 9 stocks with bids higher than their last selling prices and 3 with offers that were lower.

IC bid-offer Indicator| At the end of trading, in the main and junior markets, the Investor’s Choice bid-offer indicator shows 9 stocks with bids higher than their last selling prices and 3 with offers that were lower.Stocks trading include, Berger Paints ended trading with 81,477 shares changing hands to close 20 cents higher at $2.55, Caribbean Cement closed with 240,866 shares trading, 89 cents higher, at $5.10, Carreras finished trading with 20,385 shares and lost 35 cents to close at $49, Desnoes & Geddes saw trading in 31,000 shares trading 5 cents higher at $7.25. Gleaner closed with 170,739 units trading, with the price unchanged at $1, Grace Kennedy finished trading with 42,032 shares and fell $1 to close at $63.50. Jamaica Stock Exchange concluded trading with 25,000 units trading with the last price unchanged at $3.50, JMMB Group completed trading in 11,506 shares changing hands and jumped $50 cents at $10,the stock closed with an offer at $9.49, Kingston Wharves had dealing in 34,221 units traded at 6 cents up to $6.26.

Mayberry Investments contributed 93,828 units to trading and close unchanged at $3, National Commercial Bank ended trading with 52,070 shares changing hands to close down by 50 cents at $30 and based on today’s trading which saw the bid that was at $30 for several days, to buy an undisclosed amount being pulled, it looks as if the price could fall back below $30, Radio Jamaica closed with 100,000 shares trading at $2.48 after adding 8 cents, Sagicor Group finished trading with 1,127,037 units but remained unchanged at $12, after it trading during the day at $11. Scotia Group ended trading 72,725 units to close 14 cents higher, at $25.30, Scotia Investments closed with 2,300 shares, 75 cents up at $25.50. Jamaica Money Market Brokers 8.75% preference share finished trading with 153,398 units changing hands to close 2 cents higher at $3.02 and Proven Investments 8% preference shares saw trading in 26,805 units with the price ending unchanged at $5, after gaining 50 cents earlier in the day before falling back.

Mayberry Investments contributed 93,828 units to trading and close unchanged at $3, National Commercial Bank ended trading with 52,070 shares changing hands to close down by 50 cents at $30 and based on today’s trading which saw the bid that was at $30 for several days, to buy an undisclosed amount being pulled, it looks as if the price could fall back below $30, Radio Jamaica closed with 100,000 shares trading at $2.48 after adding 8 cents, Sagicor Group finished trading with 1,127,037 units but remained unchanged at $12, after it trading during the day at $11. Scotia Group ended trading 72,725 units to close 14 cents higher, at $25.30, Scotia Investments closed with 2,300 shares, 75 cents up at $25.50. Jamaica Money Market Brokers 8.75% preference share finished trading with 153,398 units changing hands to close 2 cents higher at $3.02 and Proven Investments 8% preference shares saw trading in 26,805 units with the price ending unchanged at $5, after gaining 50 cents earlier in the day before falling back.

D&G profit nearly doubles in Q3

A combination of increased sales’ volume and price adjustment saw Desnoes & Geddes, the producers of the world famous Red Stripe beer, enjoying a 20 percent jump in sales revenues in the March 2015 quarter.

A combination of increased sales’ volume and price adjustment saw Desnoes & Geddes, the producers of the world famous Red Stripe beer, enjoying a 20 percent jump in sales revenues in the March 2015 quarter.

Sales reached $2.96 billion and a near doubling in profit to $367 million for an 88 percent increase from $196 million in 2014. For the nine months to March profit was up a more sedate 29 percent on a 14 percent sales increase to $9.6 billion over 2014.

Local sales rose 20 percent in the March quarter and exports were up only 6 percent, for the year to March exports grew 11 percent and local sales 13 percent.

Earnings per share for the quarter came in at 13 cents and 54 cents for the nine months and should end at 80 cents for the full year and $1.05 for 2016 fiscal year. Gross profit margin increased during the nine months period to 41.4 percent from 39.94 percent and 37.7 percent during the quarter from 36.2 percent.

The March quarter saw a turnaround in the results of the distribution company it’s a joint venture partner with Pepsi in, which contributed $20 million in the quarter compared with a $47 million loss in 2014 and for the nine months, losses increased to $62 million from $46. Marketing cost jumped to a billion for the nine months from $737 million in 2014. Other costs were held fairly tight.

The period ended with net fixed assets increasing by $1.5 billion but the company still ended with cash funds at $1.38 billion and equity of $9.4 billion.

The stock is listed on the Jamaica Stock Exchange and closed last at $7.20, with a PE ratio of 9.

JSE profit surged – 2016 could be big

Jamaica Stock Exchange reported a huge jump in first quarter earnings showing profit of $87 million or 62 cents, up from a loss of $3 in 2014, after tax. Revenues jumped from $82 million to $253 million, on the back of 10 fold increase in cess, due to primarily to the transfer of ownership of the controlling interest in Scotia Group, from the Canadian parent, to one set up to own the Caribbean entities directly.

Jamaica Stock Exchange reported a huge jump in first quarter earnings showing profit of $87 million or 62 cents, up from a loss of $3 in 2014, after tax. Revenues jumped from $82 million to $253 million, on the back of 10 fold increase in cess, due to primarily to the transfer of ownership of the controlling interest in Scotia Group, from the Canadian parent, to one set up to own the Caribbean entities directly.

Total cess income jumped to $161 million compared to only $15 million. Access Financial managing director switched ownership of his shares to a company, resulted in a transaction over the exchange of $1 billion and Pan Jamaican Investments had a $1.3 billion transaction in March. While the latter two unusual transactions would have increased the cess around $12 million, the cess for Scotia Group is estimated by IC Insider at around $120 million, leaving around $40 million as cess from normal ongoing operational activities. Trading values grew by 27 percent in the first quarter, including the two transactions in March. Fee income which rose by 67 percent would have been partially impacted by the big one off transactions, but increased value traded and a slight increase in listing fees would also have helped.

In the second quarter to mid May trading has increased 333 percent to $2.6 billion, the amount is equal to the total value traded for the entire second in 2014. The increased value of trading will lead to increased fees. In the 2014 second quarter, income from cess was only $10 million and fee income $45.5 million. Not only will the cess rake in more funds from the increased volume of trading now on the way but also from an increase in the rate charged for cess over the 2014 level.

While the increased trading activity so far will lead to increased fees for the second quarter, the potential income will be no more than around $100-120 million and will be sufficient to produce a profit for the quarter and help in lifting profit for the full year beyond $1 per share.

Looking forward, with more unit trust schemes being set up there will be more demand for stocks to satisfy the demand of equity funds. The Stock Exchange is poised to take over repo trading and acting as the registrar for them and result in additional fee income is going in the not too distant future, also of great import is that rising stock values increases the base for listing fees to be levied in 2016.

The exchange has cash and investments of $500 million with a working capital ratio of 2:1 and equity of $650 million. The stock remains IC Insider BUY RATED and is now available at $3.50 which it traded at on Friday, but won’t remain that way forever and investors should be buying this one for big long-term gains.

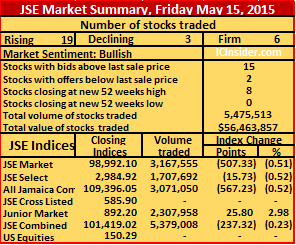

19 stocks rose only 3 fell on JSE

Hardware & Lumber gained $1.25 to a new high of $12 in response to news that Grace is in negotiation to sell their interest in the company

The rally started last year fuelled by falling money market rates with Treasury bill rate falling from over 9 percent to below 7 percent. The current rally is be fuelled by rising profits from the majority of companies reporting first quarter results.

The JSE Market Index lost 507.33 points to 98,992.10, the JSE All Jamaican Composite index fell 567.23 points to close at 109,396.05 and the JSE combined index declined 237.32 points to close at 101,419.02.

IC bid-offer Indicator| At the end of trading, in the main and junior markets, the Investor’s Choice bid-offer indicator shows 15 stocks with bids higher than their last selling prices and 2 with offers that were lower.

Stocks in the main market trading to close at a 52 weeks’ high, are Berger Paints, Desnoes & Geddes, Hardware & Lumber, Jamaica Stock Exchange, JMMB Group and Mayberry Investments. In trading, Barita Investments ended with 622,050 shares changing hands to close at $2.35, Berger Paints closed with 55,162 shares trading, 27 cents higher at $2.35, Cable & Wireless finished trading with 619,569 shares to gain 1 cent to 47 cents, Caribbean Cement saw trading in 3,351 shares, to close 1 cent higher at $4.21. Carreras closed with 32,376 shares changing hands to close 35 cents up at $49.35, Desnoes & Geddes finished trading with 14,650 shares and gained 10 cents in trading to close at $7.20, Grace Kennedy concluded trading with 307,283 units trading with the last price unchanged at $64.50, Hardware & Lumber completed trading in 9,092 shares changing hands and jumped $1.20 at $12 as investors responded to news that Grace is discussing selling their stake in the company. Jamaica Broilers had dealing in 48,730 units traded at $5.16 to remain unchanged at the end. Jamaica Stock Exchange contributed 244,616 shares, the price jumped 60 cents or 21 percent in response to the company’s huge jump in their first quarter results showing profit of $87 million or 62 cents and ended at $3.50. Trading was halted for an hour after the price exceeded 15 percent. JMMB Group ended with 27,855 shares changing hands to close up by 10 cents at $9.60, Mayberry Investments closed with 12,289 shares trading at $3,after adding 12 cents, National Commercial Bank finished trading with 468,084 units unchanged at $30.50. Pan Jamaican Investment ended trading with 14,769 units 12 cents higher, at $58.25, Sagicor Group closed with 191,168 shares trading 15 cents lower at $12. Scotia Group finished trading with 88,383 shares changing hands to close 84 cents lower at $25.16, Seprod saw trading in 335,400 shares ending 25 cents up at $18.50 and Jamaica Money Market Brokers 7.50% preference share ended with 68,650 units trading with a 5 cents rise to $2.15.

Stocks in the main market trading to close at a 52 weeks’ high, are Berger Paints, Desnoes & Geddes, Hardware & Lumber, Jamaica Stock Exchange, JMMB Group and Mayberry Investments. In trading, Barita Investments ended with 622,050 shares changing hands to close at $2.35, Berger Paints closed with 55,162 shares trading, 27 cents higher at $2.35, Cable & Wireless finished trading with 619,569 shares to gain 1 cent to 47 cents, Caribbean Cement saw trading in 3,351 shares, to close 1 cent higher at $4.21. Carreras closed with 32,376 shares changing hands to close 35 cents up at $49.35, Desnoes & Geddes finished trading with 14,650 shares and gained 10 cents in trading to close at $7.20, Grace Kennedy concluded trading with 307,283 units trading with the last price unchanged at $64.50, Hardware & Lumber completed trading in 9,092 shares changing hands and jumped $1.20 at $12 as investors responded to news that Grace is discussing selling their stake in the company. Jamaica Broilers had dealing in 48,730 units traded at $5.16 to remain unchanged at the end. Jamaica Stock Exchange contributed 244,616 shares, the price jumped 60 cents or 21 percent in response to the company’s huge jump in their first quarter results showing profit of $87 million or 62 cents and ended at $3.50. Trading was halted for an hour after the price exceeded 15 percent. JMMB Group ended with 27,855 shares changing hands to close up by 10 cents at $9.60, Mayberry Investments closed with 12,289 shares trading at $3,after adding 12 cents, National Commercial Bank finished trading with 468,084 units unchanged at $30.50. Pan Jamaican Investment ended trading with 14,769 units 12 cents higher, at $58.25, Sagicor Group closed with 191,168 shares trading 15 cents lower at $12. Scotia Group finished trading with 88,383 shares changing hands to close 84 cents lower at $25.16, Seprod saw trading in 335,400 shares ending 25 cents up at $18.50 and Jamaica Money Market Brokers 7.50% preference share ended with 68,650 units trading with a 5 cents rise to $2.15.

JSE back at August 2008 levels

Scotia rose to $27 during trading to help push market on Monday

Today’s trading resulted in the prices of 13 stocks rising, 9 declining as 32 securities changed hands, ending in 3,376,261 units trading, valued at $34,457,428, in all market segments with the market indices continuing to record gains. The market closed with 6 new 52 weeks high in the junior and main market.

TheJSE Market Index gained 1,291.03 points to 98,710.56, the JSE All Jamaican Composite index rose 1,443.44 points to close at 109,081.28 and the JSE Combined Index closed at 100,708.70 with a gain of 1,293.92 points.

The JSE All Jamaican Composite index closed at the highest level since it closed on August 28, 2008 at 109,877.58. Based on Monday’s close, the market has now crossed over the resistance trend line, just below today’s close. With Scotia Group pulling back from today‘s high of $27, there is no certainty that it will remain above resistance at the close on Tuesday, even if it does not pull back, the 115,000 mark, just 6,000 points away, is likely to be a real test as most first quarter results would have been released this week.

The JSE All Jamaican Composite index closed at the highest level since it closed on August 28, 2008 at 109,877.58. Based on Monday’s close, the market has now crossed over the resistance trend line, just below today’s close. With Scotia Group pulling back from today‘s high of $27, there is no certainty that it will remain above resistance at the close on Tuesday, even if it does not pull back, the 115,000 mark, just 6,000 points away, is likely to be a real test as most first quarter results would have been released this week.IC bid-offer Indicator| At the end of trading, in the main and junior markets, the Investor’s Choice bid-offer indicator shows 11 stocks with bids higher than their last selling prices and 4 with offers that were lower.

Stocks trading include, Berger Paints trading 2,705 shares at $1.80 after shedding 15 cents. Cable & Wireless ended with 196,631

shares to close up 3 cents at 46 cents, Caribbean Cement ended with 15,074 units with the price falling 49 cents to $4.50, Carreras traded just 2,000 shares and declined 85 cents to $48.10, Desnoes & Geddes traded 252,106 shares $6.90 while adding 30 cents, Gleaner finished trading 886,808 units at $1, Jamaica Broilers ended trading with 7,634 shares at a new 52 weeks’ high of $5.25 after posting a gain of 45 cents. Jamaica Stock Exchange ended with 607,587 units and lost 3 cents at $2.90, JMMB Group closed with 35,677 shares at $9.10, for a gain of 39 cents. Mayberry Investments had dealing in only 1,669 shares to close at $2.80, to gain 5 cents, while National Commercial Bank contributed 845,891 shares at $30. Radio Jamaica traded gained 19 cents while 25,185 shares traded at a new 52 weeks’ high of $2.19, Sagicor Group completed trading with 191,940 units at $12, with a 10 cents loss. Scotia Group traded 16,348 shares to close at $25.02 to lose 98 cents compared to Friday’s close but traded at a new intraday high of $27. Scotia Investments had 10,000 units trading at $24.60 to gain 10 cents and Jamaica Money Market Brokers 7.50% preference share traded 50,000 units at $2.11.

shares to close up 3 cents at 46 cents, Caribbean Cement ended with 15,074 units with the price falling 49 cents to $4.50, Carreras traded just 2,000 shares and declined 85 cents to $48.10, Desnoes & Geddes traded 252,106 shares $6.90 while adding 30 cents, Gleaner finished trading 886,808 units at $1, Jamaica Broilers ended trading with 7,634 shares at a new 52 weeks’ high of $5.25 after posting a gain of 45 cents. Jamaica Stock Exchange ended with 607,587 units and lost 3 cents at $2.90, JMMB Group closed with 35,677 shares at $9.10, for a gain of 39 cents. Mayberry Investments had dealing in only 1,669 shares to close at $2.80, to gain 5 cents, while National Commercial Bank contributed 845,891 shares at $30. Radio Jamaica traded gained 19 cents while 25,185 shares traded at a new 52 weeks’ high of $2.19, Sagicor Group completed trading with 191,940 units at $12, with a 10 cents loss. Scotia Group traded 16,348 shares to close at $25.02 to lose 98 cents compared to Friday’s close but traded at a new intraday high of $27. Scotia Investments had 10,000 units trading at $24.60 to gain 10 cents and Jamaica Money Market Brokers 7.50% preference share traded 50,000 units at $2.11.

Access Q1 profit jumps 72%

A fifteen percent jump in revenues at Access Financial Services saw profit before tax almost doubling to $157.6 million, up from $79 million in 2014. After providing $20 million for corporation taxes Access ended with $137 million profit or 50 cents per share for an increase of 72 percent. The good fortune did not all come from ongoing income and expenditure as loan losses fell from $39 million in the March 2014 first quarter to only $3 million in the latest quarter. Gains from the purchase of loan portfolios from Appliance Traders and Proven Investments resulted in a one off profit of $11 million. These acquisitions increased loans on the books to $1.5 billion from $1.1 billion at March 2014 and the profit pushed the equity capital to $900 million.

A fifteen percent jump in revenues at Access Financial Services saw profit before tax almost doubling to $157.6 million, up from $79 million in 2014. After providing $20 million for corporation taxes Access ended with $137 million profit or 50 cents per share for an increase of 72 percent. The good fortune did not all come from ongoing income and expenditure as loan losses fell from $39 million in the March 2014 first quarter to only $3 million in the latest quarter. Gains from the purchase of loan portfolios from Appliance Traders and Proven Investments resulted in a one off profit of $11 million. These acquisitions increased loans on the books to $1.5 billion from $1.1 billion at March 2014 and the profit pushed the equity capital to $900 million.

For the full year earnings should touch $2 per share, the stock is priced at $15.10 with a potential PE of 7.5, with its growth potential and limited available shares on the market, this valuation may be considered low.

Proven Investments who bought out the Mayberry Holdings last year December, is laughing all the way to the bank for having picked up the block of shares at a bargain price of $9 each.

Access is a junior market listed company on the Jamaica Stock Exchange and is primarily involved in payroll based lending.

Mayberry post good Q1 numbers

Mayberry Investments released first quarter results for 2015, showing earnings of $82 million or 7 cents per shares, after booking the full amount of asset tax amounting to $49 million in the quarter. In the prior year the company reported profit of $76 million or 6 cents per share reflecting total asset tax of $6 million. The quality of the earnings is encouraging with no one area being dominant especially areas that are less predictable such investment gains. Helping with the improved results are increases in net interest income amounting to $22 million as interest expenses fell while interest income held close to 2014 levels, dividend income rose by $29 million and trading gains by $18 million as other operating expenses fell by $25 million and bad debts declined by $14 million. The improvements were offset by a fall out of the share of profits of $31 million from the former associate, Access Financial Services. Based on these latest results, profit for the full year should come in around 30 cents per share. Profits should, however, get a big boost from stock market gains, with the upward movement of stock prices since the end of the first quarter as well as increased commission from equity trading with volumes in the overall market increasing around 40 percent so far this year. Mayberry is likely to see substantial gains in the equity portfolio which stood at $3 billion at the end of December last year, with the recovery in the local stock market, to date with more expected during the remainder of the year. IC Insider sees the gains to be had from the large pool of equities as the most appealing attraction for future gains from an investment in this investment bank’s stock, accordingly, the stock is seen as Buy Rated for medium to long-term investment.

Mayberry Investments released first quarter results for 2015, showing earnings of $82 million or 7 cents per shares, after booking the full amount of asset tax amounting to $49 million in the quarter. In the prior year the company reported profit of $76 million or 6 cents per share reflecting total asset tax of $6 million. The quality of the earnings is encouraging with no one area being dominant especially areas that are less predictable such investment gains. Helping with the improved results are increases in net interest income amounting to $22 million as interest expenses fell while interest income held close to 2014 levels, dividend income rose by $29 million and trading gains by $18 million as other operating expenses fell by $25 million and bad debts declined by $14 million. The improvements were offset by a fall out of the share of profits of $31 million from the former associate, Access Financial Services. Based on these latest results, profit for the full year should come in around 30 cents per share. Profits should, however, get a big boost from stock market gains, with the upward movement of stock prices since the end of the first quarter as well as increased commission from equity trading with volumes in the overall market increasing around 40 percent so far this year. Mayberry is likely to see substantial gains in the equity portfolio which stood at $3 billion at the end of December last year, with the recovery in the local stock market, to date with more expected during the remainder of the year. IC Insider sees the gains to be had from the large pool of equities as the most appealing attraction for future gains from an investment in this investment bank’s stock, accordingly, the stock is seen as Buy Rated for medium to long-term investment.

Total assets climbed to $23.7 billion from $21.8 billion at March 2014 with equity of $4.3 billion and the stock last traded on the Jamaica Stock Exchange on Friday at $2.75, close to a PE of 9 based on this year’s estimated earnings.

Will JSE scale resistance?

Scotia closed at a new 52 weeks’ high on Friday at $26

The big question with some profit taking on Friday is whether the market has enough fuel to clear resistance around 109,000 points on the all Jamaica Composite index on this leg of the rally, or will it have to wait until summer, when the market usually resumes it advance after what is normally a softening after mid-May. Even if it does scale the pending resistance there is another at 115,000 points which is likely to be the first real test before it moves on.

In the first hour of trading on Friday the all Jamaica Composite index was up 653.67 points to 108,085.44 and the JSE index put on 584.65 to 97,819.86, sometime after the indices slipped back with a fall in the price of a number of large company stocks.

At the close, theJSE Market Index advanced 184.32 points to 97,419.53, theJSE All Jamaican Composite index rose 206.07 points to close at 107,637.84 and the JSE combined index gained 287.20 points to close at 99,424.78.

At the close, theJSE Market Index advanced 184.32 points to 97,419.53, theJSE All Jamaican Composite index rose 206.07 points to close at 107,637.84 and the JSE combined index gained 287.20 points to close at 99,424.78.IC bid-offer Indicator| At the end of trading, in the main and junior markets, the Investor’s Choice bid-offer indicator shows 12 stocks with bids higher than their last selling prices and 5 with offers that were lower.

In trading, Barita Investments ended with 100,000 shares changing hands, 1 cent higher, at $2.31. Caribbean Cement closed with 66,000 units trading at $4.99 with a 1 cent slippage, Desnoes & Geddes finished trading with 264,406 shares to end at $6.60, by shedding 40 cents, Grace Kennedy saw trading in 13,244 units unchanged at $65.50, Jamaica Broilers ended with 40,831 shares trading but lost 20 cents to $4.80. Jamaica Stock Exchange closed with 375,000 units changing hands but remained at $2.93, JMMB Group finished trading with a fall of 29 cents with 867,080 shares to end at $8.71. Mayberry Investments concluded trading with 203,163 shares and gained 10 cents, at $2.75,

National Commercial Bank ended unchanged at $30, in trading 126,642 units, Sagicor Group had dealing in 157,550 units and ended at $12.10, with a 10 cents increase. Scotia Group contributed 1,967,501 shares with a $50 million value to close at a new 52 weeks high of $26 after rising $1, Seprod ended trading with 36,900 shares at $18.25, down 25 cents and Jamaica Money Market Brokers 8.75% preference share traded closed with 148,603 at $3.10.

National Commercial Bank ended unchanged at $30, in trading 126,642 units, Sagicor Group had dealing in 157,550 units and ended at $12.10, with a 10 cents increase. Scotia Group contributed 1,967,501 shares with a $50 million value to close at a new 52 weeks high of $26 after rising $1, Seprod ended trading with 36,900 shares at $18.25, down 25 cents and Jamaica Money Market Brokers 8.75% preference share traded closed with 148,603 at $3.10.The stocks to watch for the week ahead include Barita with a bid at $2.30 with one offer at $5, Cable & Wireless with the bid of 44 cents, last sale 43 cents, Jamaica Producers with the bid of $18.52 and an offer at $25. JMMB Group having a bid at $8.72 versus last sale of $8.71, National Commercial Bank is well supported by NCB Capital Market with an undisclosed amount being bought at $30, Mayberry bid $2.75 to but 128,962 units. Pan Jamaican Investment bid at $58 and no stock on offer. Radio Jamaica with a last selling price of $2 and a bid at $2.20 and Scotia Investments with a bid at $24.80 against a last sale price of $24.50.