Lasco’s new I Cool drinks – demand exceeded supply in the December quarter

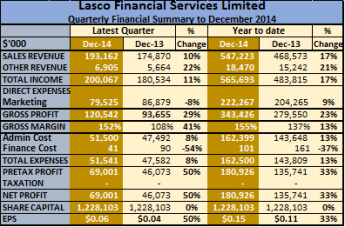

Revenue for the nine months to December increased by 16 percent to $3.3 billion. “This performance was mainly due to increased sales volume in the export markets as well as the introduction of the iCool line of products. The export division revenue year to date, shows a 53 percent growth over the same period in the 2013” Dr. Eileen Chin, Managing Director stated in her report accompanying the financials. Additionally, finance cost increased in the quarter, as well as year to date, with the quarterly figure rising 180 percent to $45 million and the nine months, to $102 million from just $18 million in the prior year’s nine months period, much faster than the increase in revenues. The increases above helped to pressure profit for the period, resulting in slight 5 percent reduction in net profit for the nine months, amounting to $426 million, from the prior year.

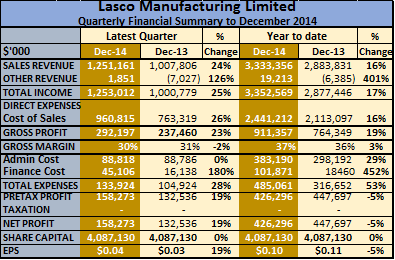

“There was also an increase in operating expenses during the period due to a significant investment in marketing to support and promote the introduction of our new iCool line,” Chin also states in her report. “Operationally, we are meeting our growth milestones. Lasco Manufacturing is well positioned in the current environment to deliver increased growth. We have completed a significant transformation that provides us with a strong asset base. Importantly, we expect strong growth in the 2015-16 financial year driven by ongoing success in our local and export markets. The integration of our business process and product extension portfolio has contributed positively to this quarter’s results. This integration is also expected to have further positive impact on profitability during the 2015-2016 financial year. We are on target to deliver on the promise to improve efficiencies and productivity, reduce operational costs, and increase product portfolio, sales and profitability”, said Chin.

“There was also an increase in operating expenses during the period due to a significant investment in marketing to support and promote the introduction of our new iCool line,” Chin also states in her report. “Operationally, we are meeting our growth milestones. Lasco Manufacturing is well positioned in the current environment to deliver increased growth. We have completed a significant transformation that provides us with a strong asset base. Importantly, we expect strong growth in the 2015-16 financial year driven by ongoing success in our local and export markets. The integration of our business process and product extension portfolio has contributed positively to this quarter’s results. This integration is also expected to have further positive impact on profitability during the 2015-2016 financial year. We are on target to deliver on the promise to improve efficiencies and productivity, reduce operational costs, and increase product portfolio, sales and profitability”, said Chin.Lasco recorded gross profit margin of 30 percent, in the December quarter from 23 percent in the same period in 2013, the margin, year to December, is 37 percent. Administrative and marketing expenses were flat in the quarter and up 29 percent year to date, compared with the prior year.

Earnings for the full year to March should end up around 15 cents per share. With new products to be added to its portfolio when the dry products factory is activated, revenues going forward should grow strongly. Increased finance cost and depreciation charge will be a drag on earnings for a while. At a stock price of $1, the stock is a buy to benefit from strong future income and above average profit growth.

Shareholders’ equity stood at $3 billion at December, borrowed funds stands at $1.4 billion. Work in progress stood at $2.26 billion, this amount relates to the dry product factory and when completed will swell fixed assets to $3.3 billion but it will result in increased depreciation charge and the funding for it will result in finance cost hat was being capitalised being expended against revenues.