The initial public offer of shares in Jamaica Fibreglass Products is expected to come to the Jamaican Capital market in October, our source advises, with Spur Tree Spices to come shortly after.

The company produces fiberglass based furniture and beddings, with revenues said to be in the region of $600 million, is expected to raise approximately $250 million for expansion purposes. The prospectus of the Metry Seaga owned company is said to be at an advanced stage of preparation and should be moving through the various stages for approval soon.

Spur Tree Spices, with revenues, said to be just over $1 billion, should also be coming in October, if all goes well, with a view to pull in $250 million. GK Capital are brokers of the two issues that are slated to list on the Junior Market. The prospectus of the company that has been manufacturing seasonings and sauces since 2006 for the local and export markets is also at an advanced stage of readiness, ICInsider.com gathers.

Spur Tree Spices, with revenues, said to be just over $1 billion, should also be coming in October, if all goes well, with a view to pull in $250 million. GK Capital are brokers of the two issues that are slated to list on the Junior Market. The prospectus of the company that has been manufacturing seasonings and sauces since 2006 for the local and export markets is also at an advanced stage of readiness, ICInsider.com gathers.

ICInsider.com is informed that the prospectus for one issue is in a draft form currently, so it should be ready to move to the regulators shortly. IPOS are subject to approval, primarily by the Jamaica Stock Exchange and Financial Securities Commission, before the prospectus can be released to the public as such, the exact timing is subject to signing off by them.

One source advised IC Insider.com that there are several potential listing candidates in the Manufacturing sector, with a number of them expressing interest in the listing. Another source advises that there are a number of potential listings in the NCB Capital Markets pipeline. The disruption to business caused by covid-19 is creating delays in some of the issues.

What appears to be a rush to list is a marked departure from the situation that existed before the advent of the Junior Market, with many business owners now seeing the major benefits that listings bring and the usefulness of long term capital.

In the meantime, Sygnus Real Estate Finance IPO that is seeking to sell 207.6 million up sizeable by 38.86 million units to raise a maximum of US$15 million, is extended to Friday, September 10.

New IPOS expected in October

IPOs coming in your future

Jamaica Stock Exchange investors should be seeing a new IPO coming to the market sometime in July, subject to regulatory approval, with Sygnus Real Estate Finance getting ready to blast out of the box reports reaching this publication indicate.

The company, which is said to be dedicated to investing in and funding real estate developments through a combination of debt capital as well as equity capital, has projects on its books already, with developments in St Ann, St Catherine and Kingston, which the principals expect to extract extra value by way of creative acquisition and disposal. The company strategy is to fund new developments through real estate notes secured by a charge over the properties.

The company, which will be separate from Sygnus Credit Investments, could benefit from funding from them and is expected to raise $3 to $4 billion in the region. The company is coming to the market at a time of unprecedented construction of buildings in the country. Reports reaching ICInsider.com indicate strong buying interests locally and from overseas in townhouses and detached units in the country’s hills, and many see Jamaican real estate as cheap.

Reports reaching ICInsider.com indicate strong buying interests locally and from overseas in townhouses and detached units in the country’s hills, and many see Jamaican real estate as cheap.

Also coming around July is Jamaica Fibreglass Products that produces furniture and bedding, to raise approximately $230 million for expansion purposes and Spur Tree Spices may make it towards the end of the year to pull in around $250 million. The company says it has been manufacturing all in one seasoning and sauces since 2006 for the local and export markets.

There has also been chatter in the marketplace that Jamaican Teas may consider a spin-off of its manufacturing arm into a separately listed company.

Oversubscribed

Future Energy Source Company Initial Public Offer of 500 million shares, which ICInsider.com indicated last week should be snapped up quickly by investors, with the company having long-term prospects for strong growth, did just that, with investors snapping the shares within two days of the opening.

NCB Capital Markets, the brokers for the issue, reported on Thursday that the issue, priced at 80 cents per share and opened on Wednesday, closed on Thursday the Junior Market IPO issue was oversubscribed. The successful closure of the issue will see the listings of companies rising to 42 from the current 41 on the Junior Market of the Jamaica Stock Exchange.

NCB Capital Markets, the brokers for the issue, reported on Thursday that the issue, priced at 80 cents per share and opened on Wednesday, closed on Thursday the Junior Market IPO issue was oversubscribed. The successful closure of the issue will see the listings of companies rising to 42 from the current 41 on the Junior Market of the Jamaica Stock Exchange.

The company that trades as Fesco reports earnings of $92 million before taxation for the period to December last year from revenues of $4.35 billion and is projecting pretax profit of $151 million for the year to March 2021 and $264 million for the 2022 fiscal year. The plant is for two new gas stations to be added to the current 14 before the end of 2021.

Fesco IPO opens next week

Future Energy Source Company (Fesco) initial public offer of shares will open at 9 am on Wednesday, March 31 and close on April 9, at 4 PM, unless it closes earlier.

The issue comprises 300 million new shares with 200 million to be sold by existing shareholders at 80 cents each. If successful, the total issued shares will be 2.5 billion, with the shares slated to list on the Jamaica Stock Exchange Junior Market.

The projection shows a profit of $151 before taxes for the year ended March 2021 from revenues of $7 billion and earnings per share of 7 cents. The company forecast revenues of $106 billion and a profit of $264 million or 10.5 cents per share for 2022.

ICInsider.com had earlier done a detailed review of the offer and rated it a buy with long term growth prospects as there is much room for expansion as it currently has only 14 service stations under its banner. NCB Capital Markets is the lead broker.

FESCO worth a buy-in

Investors need to separate investments that can make them money from a great investment to hold long term. It is against this background that the latest IPO should be viewed.

Future Energy Source Company Limited (Fesco) initial public offer is set to open on February 25, with 500 million shares for sale at 80 cents each, with 200 million units being sold by existing shareholders.

Of the total, 325 million units are reserved for priority applicants and 175 million for the wider public to list on the Junior Market. The shares are not a great investment on the surface, but an opportunity exists to profit from an investment in the short to medium term. If all the shares offered for sale are subscribed to, the number of issued shares will rise to 2.5 billion units and the company will collect $240 million before expenses for the portion offered by them.

Proceeds from the company’s subscription of shares will support the growth of the existing businesses and allow the company to pursue strategic investment opportunities and pay the expenses of the issue.

The company was incorporated in February 2013 and made the first fuel sale in November of that year. In 2014, the first FESCO branded service station was unveiled in Mandeville and have grown to fourteen branded Service Stations. Two additional service stations, are to be opened this year, one at Ferry on Mandela Highway by April and the second at Beechwood Avenue, St. Andrew in June.

”Our current market share for transportation fuel is approximately 4.65 percent (April 2020- September 2020) and is expected to increase to 5.3 percent by March 2021 and 7 percent by December 2021. We estimate that FESCO’s market share reflects three (3) main facts: a) we are a relatively new company (operating for just over six (6) years) whose initial strategy has been to grow organically rather than through acquisitions; b) as at September 2020, we have very little presence in the Kingston and St. Andrew (KSA) fuel market. Our KSA offerings are limited to FESCO Stony Hill and FESCO Rock Hall, both of which are in the more rural parts of St. Andrew; and c) the dominance of the multinational brands in the industrial and commercial space where they provide fuels to private clients”, the prospectus states.

”FESCO’s current market share of transportation fuels at September 2020 is 4.65 percent up from 3.8 percent in 2019 and 3.5 percent in 2018 and it estimates that its market share will increase to 5.3 percent by March 2021 and 7 percent by December 2021”, the prospectus further stated.

FESCO’s sales significantly outstripped the 2019 performance in litres sold. In fact, FESCO’s April through September 2020 sales in litres of transportation fuels sold is 6.6 percent ahead of its performance for the same period in 2019 despite the impact of COVID-19 and the overall market declining 13.9 percent.

FESCO is yet to enter the commercial or retail LPG market estimated at 13,957,716 or between J$1.5 billion to $1.9 billion monthly.

Revenues increased from $3.754 billion in 2016 to $5.94 billion in 2020 representing a compounded average growth (CAGR) of 12.1 percent. Over the period, gross profits increased from $28.2 million to $178.3 million, with a CAGR of 58.6 percent. FESCO increased its gross profit margin to its dealers as its brands became more recognized and demanded by customers from 0.75 percent in 2016 to 3 percent in 2020.

From the 2015 financial year through to the 2020 financial year, average monthly volumes increased from 2,502 million litres to 3,743 million litres, a CAGR of 8.4 percent. Pre-tax profits increased by J$87 million or 172 percent to $137 million in 2020 up from $50 million in 2019.

Revenues over the period April 2020 to September 2020 was $2.811 billion down 5.84 percent from the comparative period of September 2019, a decline of $175 million from 2019 turnover of $2.99 billion. Profit before taxes for the period to September 2020 was $65 million, similar to that earned in 2019.  The projection for revenues to March this year is $6 billion, with profit of $151 million for earnings per share before tax of 7 cents and a price earnings ratio of 11.4 that compares well to Tropical Battery that listed in January and now has a PE of 14.6. ICInsider.com forecasts 13 cents per share to March 2022 with the PE at 6 and the price rising to $2.50 by then. The prospectus was withdrawn due to projections to 2025 that appears to overstate the forecasted administrative costs by approximately $100 million per annum.

The projection for revenues to March this year is $6 billion, with profit of $151 million for earnings per share before tax of 7 cents and a price earnings ratio of 11.4 that compares well to Tropical Battery that listed in January and now has a PE of 14.6. ICInsider.com forecasts 13 cents per share to March 2022 with the PE at 6 and the price rising to $2.50 by then. The prospectus was withdrawn due to projections to 2025 that appears to overstate the forecasted administrative costs by approximately $100 million per annum.

The company’s financial status strong with Shareholders’ equity at the end of September at $255 million, borrowings amount to just $63 million and cash on hand of $99 million.

First, the negatives. If the company succeeds with the IPO, it will have the largest board of directors of any Junior Market company, with 11 members. That is a great sign of management weakness. Grace Kennedy and NCB Financial have nine directors, while Scotia Group has 11. Those are vastly bigger and more complex entities that FESCO. The company relies solely on distributors for revenues in a sector that has been subject to industrial disputes from time to time and government regulations. Gross profit margin is primarily subject to worldwide price fluctuation in global petroleum prices.

On a positive note, the downturn in demand for petrol seems to be easing and should help boost revenues in the immediate period ahead. This year’s opening of two new service stations will help grow revenues by ten to twenty percent in a full year. One of the new stations will be owned and operated by the company. The company is relatively small, commanding less than 10 percent of the market, leaving much room for above-average growth with good scope for gain in market share. Additional, with the local economy poised to grow that, should aid growth as well.

Alliance IPO is now

Shareholders of Alliance Financial Services will offer later this month just over 1.25 billion shares to the public for purchase at $1.59 each, for a total consideration of $1.99 billion.

The Invitation opens at 9 am on December 28 and will close at 4 pm January 11, subject to the Selling Shareholders’ right to close the issue at any time after it on the Opening Date once the shares are fully subscribed.

The Invitation opens at 9 am on December 28 and will close at 4 pm January 11, subject to the Selling Shareholders’ right to close the issue at any time after it on the Opening Date once the shares are fully subscribed.

During its sixteen (16) years of operation, the company has grown to become a notable Cambio and remittance service provider in Jamaica.

The company reported a $709 million profit for the year to September 2020, from revenues of $1.5 billion. The 2020 profit equates to earnings per share of 11.3 cents for a PE of 14 but using the 2019 earnings the PE would have been 12.7, with both below the Jamaica Stock Exchange Main Market average of 17.

JMMB Securities are brokers for the offer.

Airbnb more than doubles IPO price

The very popular Airbnb listing that follows its recent IPO hit the market today and only recently started trading with nearly 30 million shares exchanged up to 2 pm, with the price more than doubling.

The stock issue price was US$68, but it started trading at US$147.61 and moved up to a high of $165, but it is now trading at $148.34 for a rise of $118. The company is a booking service for travelers in non-traditional accommodations.

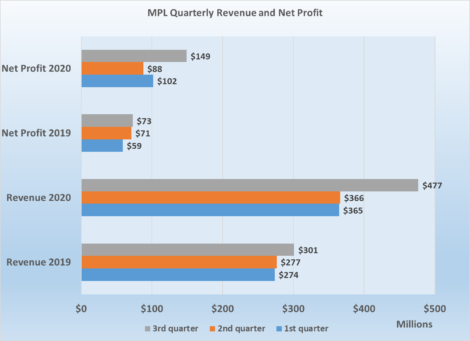

Mailpac Q3 profit surges 129%

MailPac Group (MGL) continues to enjoy increasing strong profit growth despite the current pandemic, with revenue jumping 58 percent in the September quarter over the 2019 quarter and profit more than doubling.

Mailpac dominated trading on Thursday with 84% of the total volume of the market on Tuesday.

The company recorded net profit of $149 million for the quarter, a solid 129 percent jump from the $65 million the operation recorded for the September 2019 quarter. For the year-to-date, there was an even more sizeable growth of 150 percent, moving from $203 million in 2019 to $339 at the end of September 2020.

Revenues grew 58 percent over the September 2019 quarter, from $301 million to $477 million, and grew a stunning 30 percent over the June 2020 quarter with revenues of $366 million. For the year to September, revenues rose to $1.2 billion, 42 percent more than the $851 million recorded at the end of September 2019.

Gross profit rose to 50 percent from 44 percent in the June quarter but fell to 48 percent for the nine months compared to 52 percent in 2019.

Direct expenses jumped 57 percent from $150 million for the September 2019 quarter to $236 million for the September 2020 quarter and 15 percent over the June 2020 quarter. For the year to date, the expenses climbed by 52 percent from $410 million in 2019 to $623 million in 2020. Gross profit stood at $240 million for the quarter ending September 2020, up from $150 million in 2019 and $584 million for the year to date versus $442 million in 2019.

Administrative, selling and promotion expenses increased 22 percent over the second quarter and slipped two percent from the September 2019 quarterly figure of $86 million to $84 million. The Executive Chairman attributes the increase in expenses in the third quarter over the second quarter to its expanding operations, the partnership with PriceSmart presumably one such notable factor.

Administrative, selling and promotion expenses increased 22 percent over the second quarter and slipped two percent from the September 2019 quarterly figure of $86 million to $84 million. The Executive Chairman attributes the increase in expenses in the third quarter over the second quarter to its expanding operations, the partnership with PriceSmart presumably one such notable factor.

For the nine months to September, selling and promotion expenses amount to $30 million, up from $29 million in 2019, while administrative and general expenses dropped to $199 million, from $218 million in 2019. Overall, these expenses were down seven percent from $246 in 2019 to $228 million at the end of September 2020. The effect, operating profit, rose a strong 140 percent over the comparative quarter to $157 million from $65 million in 2019 and an 82 percent increase for the nine-month period, moving from $195 million to $356 million.

Finance costs rose for the quarter from $352,000 in 2019 to $11 million in 2020, while the nine months to September ended at $31 million from $3 million for 2019.

Mailpac CEO Khary Robinson.

Gross cash flow brought in $346 million but MGL recorded trade and other payables increase of $127 million, spent $12 million on the acquisition of fixed assets and paid $225 million in dividends to end with cash and equivalents of $309 million at the end of September. Shareholders’ equity stood at $467 million. Current assets ended the period at $369 million and Current liabilities at $185 million.

Earnings per share came out at 6 cents for the quarter and 14 cents to September. IC Insider.com is forecasting Mailpac will end the year at 20 cents per share for PE of 11 times earnings and they should go on to earn 33 cents in 2021.

At the IPO, the company projected a profit of $317 million in 2020, while IC Insider.com projected $356 and 14 cents per share. The nine months’ results are just below our full year’s forecast.

The stock is priced below the average of the Junior Market of 12 and offers strong upside potential. The strong current growth continues the trend since 2017, when revenues grew 12.2 percent, 25.7 percent in 2018 and 28.8 percent for the first half of 2019. The company offers a convenient way to shop and far less costly than traditional ways. Listing on the stock exchange provides greater credibility that augurs well for increased business. MGL provides clients with physical addresses in Miami, Florida, where they can receive all goods purchased are flown to Jamaica. The company clears all goods and delivers them to the customers at their homes or for collection.

On the negative side, the main asset owned is the brand and technology that drives the business. Other entities could break into the market and squeeze profit margin longer term.

Coming off a robust third quarter, MGL is entering what is normally the busiest time of the year for the company that should continue the solid growth experienced in 2020 so far.

The stock currently trades at $2.13 on the Junior Market of the Jamaica Stock Exchange. The company paid an interim dividend of 5 cents per share in July 2020 and 5 cents per share in October and more is expected, with the company promising at the time of the IPO that the Directors intend to pursue a dividend policy that projects an annual dividend of up to 75 percent of net profits available for distribution.

Virtues & pitfalls of OPAs & stock splits

A reader of IC Insider.com asks the following question. In general, based on what l have read, listed companies can raise capital faster than getting a loan. I think there is a risk for the company that the Additional Public Offer (APO) can be undersubscribed. What are other ways APOs may hurt the company?

An APO is just like an IPO but it is usually better as the former is already listed and has followers and a wide number of shareholders who are familiar with the company’s history of management and financial wellbeing.

An APO is just like an IPO but it is usually better as the former is already listed and has followers and a wide number of shareholders who are familiar with the company’s history of management and financial wellbeing.

Shares issued to the public can be undersubscribed if the pricing is out of line with investors’ expectations or if market conditions change adversely after the issue opens. Bear in mind that the management and their Broker would get a sense from the market whether the issue will be taken up or not. Brokers will usually do roadshows to pitch an issue or get feedback from their clients before pricing and going to market with the issue. At least with an APO, the market has already determined the value investors place on the company so pricing is easier than for an IPO that has to be priced off the indicative market valuation.

One more question? if there’s a stock split after an APO ( thinking of PanJam), might it be better to buy shares after the APO as they could buy more shares for less money, is my understanding correct?

Stock splits tend to cause the stock price to rise because the news of the split and the lower share price stimulate short-term interest and if investors wait until after the split they are likely to pay more for the stock in real terms. In the case of PanJam buying in the APO could be the best bet. It, however, depends on the timing of the split as well as that of the APO. The odds are that the split would take place before the APO and if history is anything to go by the stock price will rise and result in a higher APO price than the price before the split. Buying the stock now before the announced stock split may be the better move.

Motta for income & long term gain

The Musson Group is disposing of all their interest in Stanley Motta Limited in a scheduled sale of all the 757,818,862 ordinary shares currently owned.

Our source states that the business which is a solely a real estate venture is not part of Musson’s core business. If the shares are listed it would be the fifth company connected to the group to do so.

ALorica, parent company of the prime tenant at 58 Half Way Tree Rd.

The offer has 227,348,547 shares reserved mostly for family members of the majority shareholders of the Musson group and 529,970,315 units for the General Public for purchase at $5.31 per share. All the net proceeds will be payable to selling Shareholders. Sources indicates that General Accident Insurance will make be taking up a large block of the shares that offered to the public.

The Company intends to apply to the Jamaica Stock Exchange for the listing on the Main Market of all the Shares and to make such application as soon as is conveniently possible following the close of the offer. The offer opens on July 6, with July 20 set as the closing date.

A business process outsourcing and technology park consisting of five buildings totalling over 200,000 square feet of rentable commercial office space at.

The company owns 58 Half Way Tree Road in Kingston, next door to the new Kingston, comprising 200,000 square feet of rentable space that is fully leased with the lease quoted in US dollar. Tenants are responsible for all expenses arising by reason of occupation, including insurance, property tax and maintenance expenses. The weighted average tenor and annual rent per square foot are 4.7 years and US$12.09, respectively.

The anchor tenant is Jamaica Agent Services Limited, the local subsidiary of Alorica Inc. Alorica is a US based global business process outsourcing firm and the third largest provider of customer experience solutions in the world. The company has over 100,000 employees and operates from 140 locations in 16 countries around the world in North America and the Caribbean, Latin America, Europe, China, the Philippines, and Japan. Alorica serves over 600 clients many of which are on the annual list of the 500 largest companies in the United States as compiled by Fortune magazine. Under the terms of Stanley Motta’s two leases with Alorica, who took possession of Units 2, 3 and 4 each as a “cold hard shell” and paid to complete the buildings at its own expense including all interior walls, ceilings and finishes.

Site plan of 58 Half Way tree road.

The complex will be managed by Felton Property Management Services Limited, a subsidiary of Musson. Felton will be responsible for all day-to-day on-site property management, administration and accounting services.

The property is a designated Free Zone, accordingly, Stanley Motta is exempt from corporate income tax on the rental income of Free Zone property.

The Board expects to distribute approximately 90% as dividends subject change from time-to-time if circumstances dictate.

The Projected Valuation obtained from an independent appraiser, using the income capitalization approach, for Unit 4 at completion is US$21.3 million or approximately $2.63 billion using rates of exchange as at December 31, 2017 and $2.79 billion using the weighted average selling rate according to the Bank of Jamaica as of June 19.

The Company’s sole source of direct income is from the rental of units in the technology park. Its only other source of income is from dividends from Unity Capital, whose sole income is derived from the rental of office space in its building at 58 Half Way Tree Road. The lack of diversification means that the Company is particularly exposed to risks affecting the property market.

The Invitation is underwritten by the Underwriter up to a maximum of the equivalent of US$21 million.

The stock is not for all investors in the short term. Investors looking for relatively high return in US dollars with modest capital appreciation over time may find this an attractive offer. While most investors may view the income in US dollars as a big positive, they ought to be aware that continued devaluation of the local currency going forward is not guaranteed. Of note is that the rental income for a full year is likely to be in the order of US$2.5 million with most expenses picked up by tenants, it should net out around the same amount tax free. The yield on investment will translate to just under 7 percent. The property has room for some amount of expansion which is done could increase the revenues and profit. The new leases while priced at $12 per square foot is set to rise to $14 dollar at renewal in 5 years and should go higher on renewal thereafter.

With Jamaica, on target to lower the fiscal deficit to 60 percent of GDP and with government maintaining balanced fiscal operations inflation going forward is likely to remain low and should result in low interest rates, against this back drop ground, the income from this operation could see investors ultimately acquiring the stock as a good income play and then drive up the price over time.