IC TOP10 stocks are now based on earnings for 2021/22 fiscal years. Of the January listing, Access Financial Services moved out of the TOP 10 Junior Market list while Main Market QWI Investment and Carreras fell from the Main market list with increased prices.

Coming into the TOP10 are Fesco, the latest IPO that is expected to come to market shortly, with the prospectus having been released but temporarily withdrawn to correct some errors. JMMB Group and Sygnus Credit Investments are now in the TOP10 Main market listing.

Coming into the TOP10 are Fesco, the latest IPO that is expected to come to market shortly, with the prospectus having been released but temporarily withdrawn to correct some errors. JMMB Group and Sygnus Credit Investments are now in the TOP10 Main market listing.

Since the start of the year, the Junior Market is up 10.5 percent, with 11 companies’ stock rising between 20 and 63 percent, including four with gains from 49 percent up. The Main Market, on the other hand, is marginally down for the year by less than one percent, with five stocks recording gains between 21 percent and 47 percent and Ciboney rising 500 percent for the year to date.

The Junior Market and the Main Market moves are supported by technical indicators, pointing to robust gains ahead and back up by some companies reporting positive profit results.

This week’s focus: Grace Kennedy had outstanding results for 2020 with much more to come in 2021; expect the price to move sharply over the next few weeks. Caribbean Cement reported a 70 percent rise in profit for 2020 and is projected to earn $6.70 for 2021, the stock is an ideal candidate to move higher in the weeks ahead.

This week’s focus: Grace Kennedy had outstanding results for 2020 with much more to come in 2021; expect the price to move sharply over the next few weeks. Caribbean Cement reported a 70 percent rise in profit for 2020 and is projected to earn $6.70 for 2021, the stock is an ideal candidate to move higher in the weeks ahead.

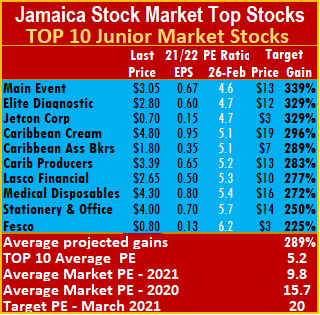

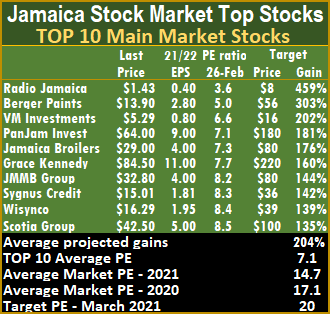

The top three stocks in the Junior Market can gain between 329 to 339 percent are Main Event followed by Elite Diagnostic and Jetcon. With expected gains of 202 to 459 percent, the top three Main Market stocks are Radio Jamaica, followed by Berger Paints and VM Investments.

The local stock market’s targeted average PE ratio is 20 based on profits of companies reporting full year’s results, up to the second quarter of 2021. The Junior and Main markets are currently trading well below the market average, a clear indication of strong gains ahead. The JSE Main Market ended the week, with an overall PE of 14.7 and the Junior Market 9.8 based on ICInsider.com’s projected 2021-22 earnings. The PE ratio for the Junior Market Top 10 stocks average a mere 5.2 at just 53 percent of the market average. The Main Market TOP 10 stocks trade at a PE of 7.1 or 48 percent of the PE of that market.

The local stock market’s targeted average PE ratio is 20 based on profits of companies reporting full year’s results, up to the second quarter of 2021. The Junior and Main markets are currently trading well below the market average, a clear indication of strong gains ahead. The JSE Main Market ended the week, with an overall PE of 14.7 and the Junior Market 9.8 based on ICInsider.com’s projected 2021-22 earnings. The PE ratio for the Junior Market Top 10 stocks average a mere 5.2 at just 53 percent of the market average. The Main Market TOP 10 stocks trade at a PE of 7.1 or 48 percent of the PE of that market.

The average projected gain for the Junior Market IC TOP 10 stocks is 289 percent and 204 percent for the JSE Main Market, based on 2021-22 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.

The average projected gain for the Junior Market IC TOP 10 stocks is 289 percent and 204 percent for the JSE Main Market, based on 2021-22 earnings. IC TOP10 stocks are likely to deliver the best returns up to March 2021 and ranked in order of potential gains, based on likely gain for each company, taking into account the earnings and PE ratios for the current fiscal year. Expected values will change as stock prices fluctuate and result in movements in and out of the lists weekly. Revisions to earnings per share are ongoing, based on receipt of new information.

Persons who compiled this report may have an interest in securities commented on in this report.

This publication has been rightly calling for all prospectuses to include forecasts of income and profits for three years at a minimum, but prior to the FESCO issue only new companies have been doing so. The lack of forecast is a disservice to the investing public.

This publication has been rightly calling for all prospectuses to include forecasts of income and profits for three years at a minimum, but prior to the FESCO issue only new companies have been doing so. The lack of forecast is a disservice to the investing public. ”FESCO’s current market share of transportation fuels at September 2020 is 4.65 percent up from 3.8 percent in 2019 and 3.5 percent in 2018 and it estimates that its market share will increase to 5.3 percent by March 2021 and 7 percent by December 2021”, the prospectus further stated.

”FESCO’s current market share of transportation fuels at September 2020 is 4.65 percent up from 3.8 percent in 2019 and 3.5 percent in 2018 and it estimates that its market share will increase to 5.3 percent by March 2021 and 7 percent by December 2021”, the prospectus further stated. The projection for revenues to March this year is $6 billion, with profit of $151 million for earnings per share before tax of 7 cents and a price earnings ratio of 11.4 that compares well to

The projection for revenues to March this year is $6 billion, with profit of $151 million for earnings per share before tax of 7 cents and a price earnings ratio of 11.4 that compares well to