Caribbean Cement recorded a solid 48 percent increase in pretax profit to $2.6 billion, from $1.7 billion in 2022 for the third quarter, with the nine months at $5.6 billion, marginally lower than the $5.8 billion reported in 2022. After taxation of $617 million in the third quarter and $517 million in 2022, profit ended at $1.94 billion, up a healthy 60 percent from $1.2 billion in 2022. For the nine months of 2023, profit after accounting for taxation of $1.5 billion and $1.86 billion in 2022 ended at $4.39 billion, from $4.25 billion in 2022.

Earnings per share for the quarter was $2.28, up from $1.42 in 2022 and $5.15 versus $5 for the year to September.

Earnings per share for the quarter was $2.28, up from $1.42 in 2022 and $5.15 versus $5 for the year to September.

Revenues jumped a robust 13.4 percent to $7.0 billion for the third quarter to September this year over the $6.2 billion in the 2022 period and were up 8 percent to $21.27 billion for the nine months to September 2023 compared to $19.68 billion in 2022.

While revenues were racing ahead, cost of sales remained flat during the third quarter at $3.48 billion against $3.42 billion in the September 2022 quarter, but it rose 18 percent in the year to date period from $10.8 billion in 2022 to $12.77 billion. Gross profit in the quarter jumped 28 percent from $2.75 billion to $3.5 billion in the September quarter and, for the year to date, declined from $8.85 billion in 2022 to $8.5 billion. Administrative expenses rose a significant 36 percent from $225 million in the September 2022 quarter to $304 million in 2023 and popped 17 percent from $695 million in the year to September 2022 to $811 million in 2023.

Notwithstanding the increase in revenues, distribution costs fell from $433 million in the September 2022 quarter to $354 million in the current year and moved from $1.2 billion down to $1.1 billion in the nine months to September.

Other expenses, mainly fees paid for management and royalty to the parent company that was flat year over year, rose to $254 million in the September quarter from $166 million in the prior year, and for the nine months, it was marginally down to $669 million from $680 million in the preceding nine month period.

Finance costs for the September quarter fell to $48 million, down from $154 million in the 2022 quarter and for the nine months, from $430 million to $142 million in the current fiscal year to September.

In relation to the cash flows, “Net cash provided by operating activities” was $5.7 billion for the nine months and $2.46 billion for the quarter. The cash flow generation during the quarter and the available cash at the beginning of the period have allowed the Group to invest $4 billion during the nine months of the year and $2 billion during the second quarter, leaving the company with $639 million in cash and bank balance at the end of the period.

In relation to the cash flows, “Net cash provided by operating activities” was $5.7 billion for the nine months and $2.46 billion for the quarter. The cash flow generation during the quarter and the available cash at the beginning of the period have allowed the Group to invest $4 billion during the nine months of the year and $2 billion during the second quarter, leaving the company with $639 million in cash and bank balance at the end of the period.

As a result of the excellent performance, the company paid a dividend of $1.8976 per share, amounting to $1.6 billion, a 37 percent rise over the $1.17 billion paid in 2022 and resulting in Shareholders’ equity ending at $22.76 billion at the end of September, a sizable improvement over the $18.75 billion at the end of September 2022 and $20 billion at the end of December last year.

Total current assets ended at $10.67 billion as of September 2023, compared with $7.47 billion in 2022, with inventories being $4.68 million and $4.53 billion in 2022. Receivables from related parties amounted to $4.1 billion, up from $1.1 billion in 2022, with the 2023 balance including a deposit investment account of J$4 billion, the equivalent of US$26 million in CEMEX Innovation Holding Limited, which generates interest at a rate equal to the Western Asset Institutional Liquid Reserves Fund rate plus 30 basis points on a daily basis.

Caribbean Cement silos

Total current liabilities stood at $7.1 billion, down from $8.2 billion in 2022. There was only $228 million in other financial obligations outstanding at the end of September, down from $1.89 billion at the end of September 2022.

Caribbean Cement “implementation of its requisite business strategies has been paying dividends as the company continues with expansion and the achievement of significant milestones. It also included the company’s ability to adequately supply the local market, having enough spare capacity to export 3,500 metric tonnes of high-early strength cement to the Turks and Caicos Islands. In the next quarter, the company expects to build on its current achievements and maximise its performance as it remains optimistic about its future. The company will also continue to undertake its flagship social impact initiatives of installing concrete pavements in certain communities across the island,” the company stated in their commentary on the results.

With ICInsider.com projected earnings at $7, the stock still has the potential to go higher from the current price of $50.32, with the current PE at just 7 times 2023 earnings compared to an average of 12 for the market. Not to be ignored are a few developments that augurs well going forward. The continuing expansion to hotel rooms and road expansion should ensure continued demand for cement for several years ahead. Immediately, the September quarter profit suggests that earnings in 2024 could exceed $9 per share if the current trend continues into 2024.

Profit for the September quarter was marginally lower than the June quarter. Still, revenues from loans of $300 million in the September period were slightly higher than the $294 million in the June quarter.

Profit for the September quarter was marginally lower than the June quarter. Still, revenues from loans of $300 million in the September period were slightly higher than the $294 million in the June quarter. According to the company’s commentary on the results, “business loans accounted for 82 percent of the total loan portfolio, while personal loans accounted for the remaining 18 percent. Secured loans constituted 81 percent of the portfolio, with unsecured loans making up the remaining 19 percent. The collateralised loan strategy has proven instrumental in maintaining the loan portfolio quality, with non-performing loans holding steady at 9 percent, remaining within budgeted expectations and below the sector average.”

According to the company’s commentary on the results, “business loans accounted for 82 percent of the total loan portfolio, while personal loans accounted for the remaining 18 percent. Secured loans constituted 81 percent of the portfolio, with unsecured loans making up the remaining 19 percent. The collateralised loan strategy has proven instrumental in maintaining the loan portfolio quality, with non-performing loans holding steady at 9 percent, remaining within budgeted expectations and below the sector average.”

Current assets ended the period at $590 million compared with $639 million in 2022. Trade and other receivables amount to $137 million, inventories amount to $156 million, down from $394 million in 2022 and cash and bank balances ended at $297 million. Current liabilities ended the period at $120 million. Net current assets ended the period at $469 million.

Current assets ended the period at $590 million compared with $639 million in 2022. Trade and other receivables amount to $137 million, inventories amount to $156 million, down from $394 million in 2022 and cash and bank balances ended at $297 million. Current liabilities ended the period at $120 million. Net current assets ended the period at $469 million.

The company expended $489 million on investment property and $169 million on development expenditure during the year, reducing the overall cash on hand to just $90 dollars compared to $217 million in the prior year. According to the audit report, three apartment units were contracted for sale which should result in a loss of $32 million and realise $117 million in total cash, data from the audited statement suggests.

The company expended $489 million on investment property and $169 million on development expenditure during the year, reducing the overall cash on hand to just $90 dollars compared to $217 million in the prior year. According to the audit report, three apartment units were contracted for sale which should result in a loss of $32 million and realise $117 million in total cash, data from the audited statement suggests.

Direct Expenses fell 33 percent in the July quarter to $204 million from $304 million in 2022 and rose 28 percent from $583 million to $748 million in 2023. Gross profit slipped 25 percent to $224 million from $298 million in the quarter and jumped 64 percent to $839 million from $511 million for the nine months.

Direct Expenses fell 33 percent in the July quarter to $204 million from $304 million in 2022 and rose 28 percent from $583 million to $748 million in 2023. Gross profit slipped 25 percent to $224 million from $298 million in the quarter and jumped 64 percent to $839 million from $511 million for the nine months.

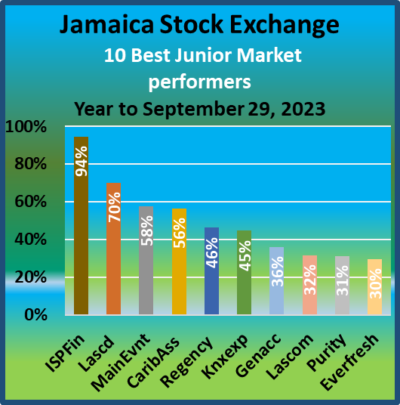

ISP Finance, a microfinancing company led the Junior Market following news that two new directors with experience in the financial service sector and who had worked with in the past in arranging deals for them were appointed to the board. There was also speculation that the majority shares could probably change hands sooner rather than later. There is also the expectation for increased lending to customers is expected to impact revenues and profit positively following a decline in the half year profit when loans jumped to nearly a billion dollars from under $800 million. Lasco Distributors profits for the fiscal year to March jumped and was followed by improved results in the June Quarter as investors rewarded the performance with s solid price movement. Main Event continued to recover from the damage to revenues and profits during the COVID, bouncing back as profit more than doubled to $216 million from $104 million for the nine months to July. Movement in Caribbean Assurance Brokers’ stock price follows profit jumping from just $4.5 million in the June 2022 half year to $18 million this year. Regency Petroleum profit fell from $51 million to $25 million for the half year but hope for improved profits drove the stock with new gas stations being opened or to be opened. General Accident migrated from the Junior Market to the Main Market on the last day of the month, with the increased stock price spurred by profit surging 195 percent to $165 million in the 2023 half year.

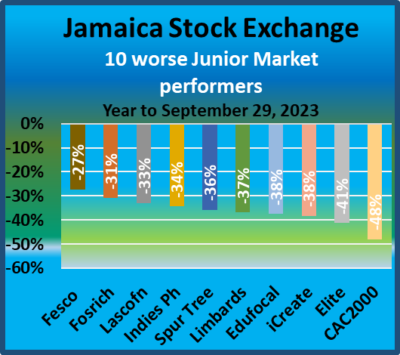

ISP Finance, a microfinancing company led the Junior Market following news that two new directors with experience in the financial service sector and who had worked with in the past in arranging deals for them were appointed to the board. There was also speculation that the majority shares could probably change hands sooner rather than later. There is also the expectation for increased lending to customers is expected to impact revenues and profit positively following a decline in the half year profit when loans jumped to nearly a billion dollars from under $800 million. Lasco Distributors profits for the fiscal year to March jumped and was followed by improved results in the June Quarter as investors rewarded the performance with s solid price movement. Main Event continued to recover from the damage to revenues and profits during the COVID, bouncing back as profit more than doubled to $216 million from $104 million for the nine months to July. Movement in Caribbean Assurance Brokers’ stock price follows profit jumping from just $4.5 million in the June 2022 half year to $18 million this year. Regency Petroleum profit fell from $51 million to $25 million for the half year but hope for improved profits drove the stock with new gas stations being opened or to be opened. General Accident migrated from the Junior Market to the Main Market on the last day of the month, with the increased stock price spurred by profit surging 195 percent to $165 million in the 2023 half year. Fesco stock price declined sharply for the period even as the net profits for the June quarter were marginally higher than that of the similar 2022 period, with revenues marginally higher. The stock price pulled back from heady levels in 2022 to adjust to the earnings in the last fiscal year of just under 23 cents per share with indications that it may not significantly improve in the current fiscal year to warrant the high premium it had in 2022. Fosrich, on the other hand, had a sharp decline in profits for the second quarter and the half year but it too enjoyed a big premium in the stock price in 2022, investors readjusted their expectations by marking the price down, although both stocks got a two day bounce at the end of September that improved their performance year to date. Lasco Financial had a third less profit in the 2023 fiscal year than the prior year and reported vastly poorer results in the third quarter to June and that seemed to have encouraged more selling of the stock. Revenues and profit bounced in the third quarter for Limners and Bards but are still down year to date compared with last year and that did not help the stock that lost value during the period. Edufocal profit bounced in 2023 and may not necessarily justify the 38 percent fall in the stock price, while iCreate had totally disastrous results in the 2022 fiscal year as well as in the first half of 2023, with the company’s performance continuing to raise questions about its future. Elite and CAC 2000 suffered a reversal in fortune that is reflected in the decline in stock prices of both companies.

Fesco stock price declined sharply for the period even as the net profits for the June quarter were marginally higher than that of the similar 2022 period, with revenues marginally higher. The stock price pulled back from heady levels in 2022 to adjust to the earnings in the last fiscal year of just under 23 cents per share with indications that it may not significantly improve in the current fiscal year to warrant the high premium it had in 2022. Fosrich, on the other hand, had a sharp decline in profits for the second quarter and the half year but it too enjoyed a big premium in the stock price in 2022, investors readjusted their expectations by marking the price down, although both stocks got a two day bounce at the end of September that improved their performance year to date. Lasco Financial had a third less profit in the 2023 fiscal year than the prior year and reported vastly poorer results in the third quarter to June and that seemed to have encouraged more selling of the stock. Revenues and profit bounced in the third quarter for Limners and Bards but are still down year to date compared with last year and that did not help the stock that lost value during the period. Edufocal profit bounced in 2023 and may not necessarily justify the 38 percent fall in the stock price, while iCreate had totally disastrous results in the 2022 fiscal year as well as in the first half of 2023, with the company’s performance continuing to raise questions about its future. Elite and CAC 2000 suffered a reversal in fortune that is reflected in the decline in stock prices of both companies.

Administrative costs declined marginally from $2.98 billion to $2.92 billion in the current period, distribution costs rose four percent from $690 million to $720 million, finance costs almost doubled, moving from $320 million to $633 million, taxation moved up from $332 million to $393 million during the 2023 quarter.

Administrative costs declined marginally from $2.98 billion to $2.92 billion in the current period, distribution costs rose four percent from $690 million to $720 million, finance costs almost doubled, moving from $320 million to $633 million, taxation moved up from $332 million to $393 million during the 2023 quarter. Cash inflows before working capital requirements for $3.4 billion and is up from $2.6 billion in the previous year after working capital funding rose, the group ended up with a negative cash flow of $2 billion that is up from $1 billion in the previous year.

Cash inflows before working capital requirements for $3.4 billion and is up from $2.6 billion in the previous year after working capital funding rose, the group ended up with a negative cash flow of $2 billion that is up from $1 billion in the previous year.